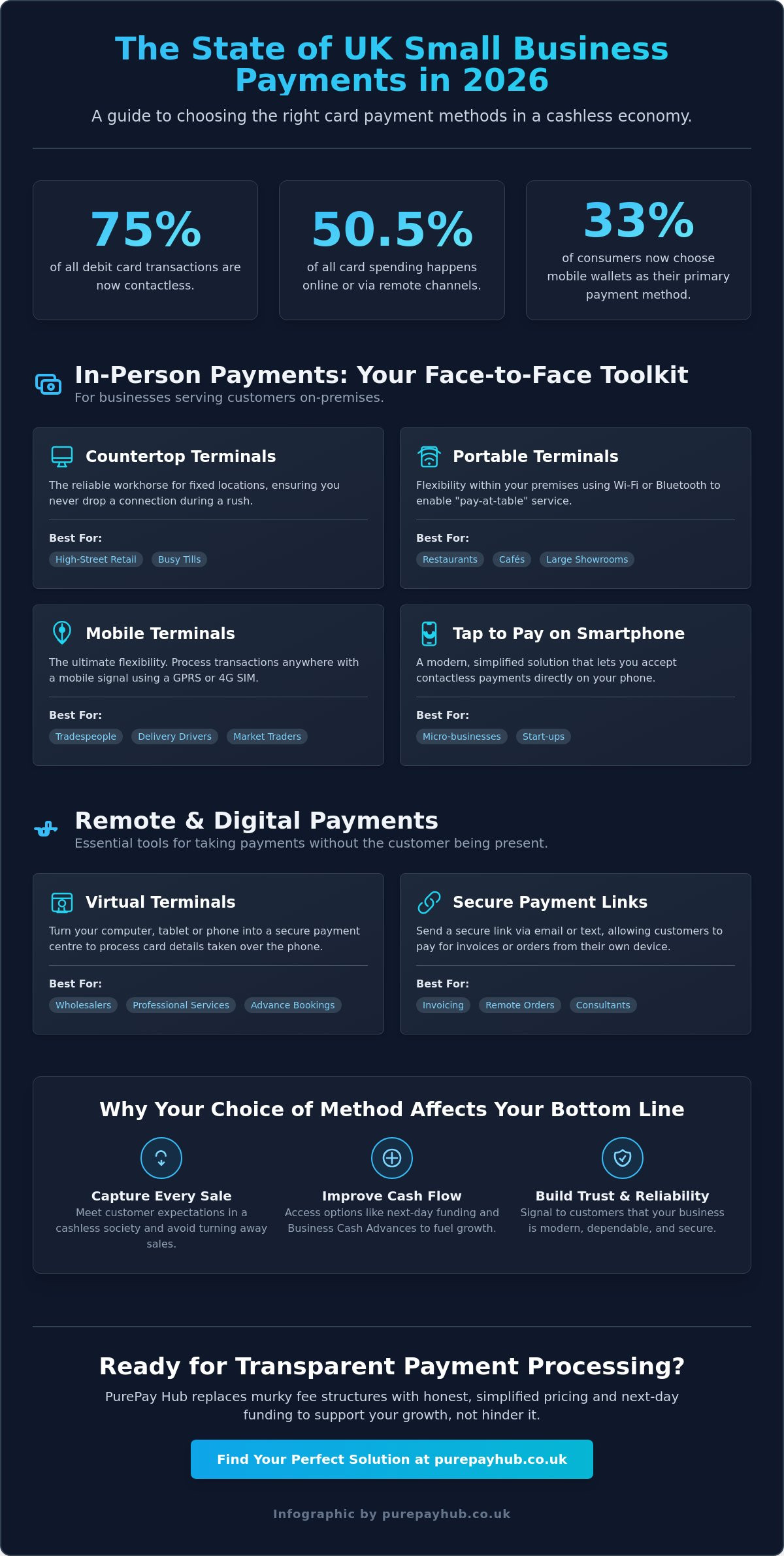

In January 2026, contactless payments accounted for a staggering 75% of all debit card transactions across the UK. Since the mandatory £100 limit was removed on 19 March 2026, the way your customers pay has shifted permanently. Finding the most efficient card payment methods for small business UK shouldn’t feel like a battle against hidden “non-compliance” fees or complex contracts. You’ve likely grown tired of waiting days for your funds to clear or dealing with hardware that fails during a busy Saturday afternoon.

We believe that payment processing should be a transparent partnership that fuels your cash flow, not a cost centre filled with markups. This guide promises to show you the most cost-effective ways to accept card payments, from physical terminals to remote payment links. We will explore the latest transaction-based pricing models and next-day funding options available to you right now. You’ll gain the clarity needed to choose reliable hardware that stays connected, allowing you to focus on growing your business with absolute confidence.

Key Takeaways

- Understand why offering diverse card payment methods for small business UK is essential in 2026 to capture every sale in an increasingly cashless economy.

- Compare the benefits of countertop, portable, and mobile hardware against remote solutions like virtual terminals and secure payment links.

- Learn how to decode complex merchant statements and move toward a transparent, transaction-based pricing model that removes hidden markups.

- Discover how next-day funding and Business Cash Advances can improve your cash flow and provide the capital you need for growth.

- Identify the specific payment setup your industry requires, from “pay-at-table” hospitality tech to integrated EPOS systems for retail shops.

The Evolution of Card Payment Methods for Small Business UK

The UK’s journey toward a cashless society has reached a definitive milestone in 2026. By January of this year, contactless transactions accounted for 75% of all debit card activity. We’ve moved beyond the era where “cash only” signs were acceptable. For modern SMEs, providing robust card payment methods for small business UK is no longer a luxury; it’s a fundamental pillar of trade. If you aren’t equipped to handle digital payments, you’re effectively turning away a massive portion of the market that no longer carries a physical wallet.

At the centre of this evolution is the PurePay Hub. We position our service as a stabilising force for your finances, ensuring that your payment infrastructure is as reliable as your service. This “Pure” approach is built on transaction-based clarity. It removes the murky fee structures used by competitors and replaces them with honest, simplified pricing that supports your growth rather than hindering it. Whether you’re taking payments face-to-face via a mobile terminal, online through a gateway, or remotely using secure payment links, transparency is our default setting.

Current UK Payment Trends and Consumer Behaviour

Shoppers in the UK have embraced digital convenience with record-breaking speed. The history of contactless payments shows how quickly we moved from niche adoption to total market dominance. Since 19 March 2026, banks have had the freedom to set their own contactless limits, effectively ending the old £100 cap for many providers. This change has made mobile wallets the primary choice for 33% of consumers. If your checkout is slow or your hardware drops connection, you aren’t just losing time. You’re losing the trust of a customer who expects an instant, secure experience. Speed has become a primary currency in the British retail and hospitality sectors.

Why Your Choice of Method Affects Your Bottom Line

The decision to limit your payment options directly impacts your profit margins. Cash-only policies are increasingly rare, especially whilst 50.5% of all card spending now happens online or via remote channels. Beyond the risk of lost footfall, manual bookkeeping for cash sales often leads to errors that cost businesses hours of administrative time. By using integrated card payment methods for small business UK, you automate your record-keeping and reduce the risk of manual mistakes. Secure, professional interfaces don’t just process money; they signal to your customers that your business is dependable and modern. This reliability is what turns a one-time visitor into a loyal advocate for your brand.

In-Person vs Remote: Comparing Your Payment Options

Every UK merchant has a unique workflow. A florist might need a countertop machine for their shopfront in the morning but require a secure payment link for a wedding order in the afternoon. Choosing the right card payment methods for small business UK isn’t about finding a one-size-fits-all device. It’s about building a toolkit that mirrors how you actually trade. Whether you are serving customers face-to-face or taking orders over the phone, your setup must be fast, reliable, and entirely transparent.

Physical Terminals: Countertop to Mobile

For businesses with a fixed location, countertop card machines remain the reliable workhorse. These devices plug directly into your power supply and ethernet port, ensuring they never run out of battery or drop a Wi-Fi signal during a rush. They are the gold standard for high-street retail where speed at the till is a priority. If your business involves moving around a premises, such as a restaurant or a large showroom, portable units are the better fit. These use Wi-Fi or Bluetooth to allow for “pay-at-table” service, which significantly improves the customer experience.

Mobile card machines represent the ultimate flexibility for tradespeople, delivery drivers, and market traders. These devices use GPRS or 4G SIM cards to process transactions anywhere with a mobile signal. You don’t need to rely on a customer’s guest Wi-Fi or a patchy hotspot. Many micro-businesses in 2026 are also adopting “Tap to Pay” technology. This allows you to accept contactless payments directly on your smartphone without needing any additional hardware at all. It’s a simplified, modern solution for those just starting their journey.

Remote and Digital Payment Methods

Remote payments are often the missing piece in a merchant’s strategy. Virtual terminals turn your computer, tablet, or phone into a secure payment centre. They allow you to take card details over the phone and process them through a secure web-based dashboard. This is a vital tool for wholesalers, professional services, and any business that takes bookings in advance. It removes the need for physical contact whilst maintaining high security standards.

Payment links have become one of the most popular card payment methods for small business UK due to their sheer simplicity. You generate a unique “pay now” button and send it to your customer via email, SMS, or WhatsApp. The customer pays at their convenience using their own device. This method is particularly effective for chasing invoices or taking deposits. For those with a website, an online payment gateway is essential. It provides a seamless checkout experience that keeps your brand front and centre. If you’re looking to upgrade your current setup, exploring transparent payment solutions can help you find the right balance between hardware and digital tools.

Deciding between a standalone card reader and an integrated EPOS system depends on your growth plans. Standalone readers are excellent for simplicity. However, an integrated EPOS system connects your payments directly to your inventory and accounting software. This link reduces manual entry errors and gives you a real-time view of your business health. It’s a disciplined approach to management that saves hours of administrative work every week.

Decoding Merchant Fees: The PurePay Hub Transparency Model

Most merchants feel a sense of dread when their monthly statement arrives. It’s often a dense document filled with acronyms like MSC, IFR, and PCI, designed to confuse rather than clarify. Understanding the fee structure behind card payment methods for small business UK is the first step to protecting your margins. We believe in a different standard. Our “Pure” approach replaces industry jargon with absolute clarity, ensuring you know exactly where every penny of your transaction fee is going.

The cost of taking a payment is split into three main parts: the interchange fee, the card scheme fee, and the merchant service charge. Under the UK’s Interchange Fee Regulation (IFR), domestic consumer card fees are capped at 0.2% for debit cards and 0.3% for credit cards. However, many providers add significant markups on top of these base rates. Whilst typical transaction fees for small businesses range from 1.4% to 2.5%, some “flat-rate” providers charge a premium for simplicity. We advocate for a transaction-based model that reflects the actual cost of processing, giving you a fairer deal on every sale.

Breaking Down the Costs of Taking Cards

Debit cards remain the favourite method for daily transactions in Britain. Because of the 0.2% interchange cap, these are the most cost-effective payments to process. Credit cards are slightly more expensive due to their 0.3% cap and the additional risk involved for the bank. You should also consider your hardware costs. Monthly

Selecting the Right Setup for Your Business Type

Every industry has a distinct rhythm. A local butcher has different operational needs than a mobile plumber or a high-street solicitor. The goal is to match your choice of card payment methods for small business UK to your specific customer behaviour. When you align your hardware with how your clients actually prefer to pay, you remove friction from the sale. This alignment is the foundation of a disciplined, professional merchant strategy.

Retail and Hospitality Configurations

High-street shops prioritising high throughput need countertop machines at permanent checkout points. In a busy retail environment, every second saved reduces queues and prevents lost sales. Integrated EPOS systems are essential here. They link your card machine directly to your stock levels and accounting software. This integration removes the need for tedious double-entry and stops staff from making manual pricing errors. It provides a real-time view of your business health, allowing for more accurate stock management and financial planning.

For UK pubs and cafes, the “pay-at-table” model is now the expected standard. Since the 19 March 2026 change to contactless limits, customers expect to settle bills quickly without leaving their seats. Portable machines using Wi-Fi allow your team to take payments anywhere on the premises. This flexibility keeps the atmosphere relaxed whilst ensuring your table turnover remains high. Reliable hardware that doesn’t drop its connection is the difference between a smooth service and a frustrated customer.

Service-Based and Mobile Business Needs

Mobile trades and delivery drivers face the unique challenge of patchy connectivity. Relying on a customer’s home Wi-Fi is often unprofessional and unreliable. Mobile card machines with GPRS or 4G SIMs ensure you can take payments in the field, whether you’re in a city centre or a rural village. Payment links are also a brilliant tool for collecting deposits before work begins. You can send a link via WhatsApp or email, allowing the customer to pay instantly from their own device. This method has seen massive growth, especially as digital wallet preferences reached 33% of UK customers by early 2026. To find the perfect configuration for your trade, you can view our full range of merchant solutions today.

By choosing card payment methods for small business UK that fit your specific workflow, you build a foundation for growth. Whether you need the speed of an integrated retail till or the mobility of a GPRS-enabled reader, the right setup ensures you never miss a sale. A transparent partnership with your processor means you can scale your equipment as your business expands.

Maximising Growth with PurePay Hub Solutions

Taking payments is the heartbeat of your enterprise. However, the right card payment methods for small business UK should do more than just process a transaction. They should act as a catalyst for your expansion. We don’t just provide hardware; we offer a partnership that prioritises your financial health. This starts with our commitment to simplicity and ends with your business reaching its full potential through reliable, honest service.

Accelerating Your Cash Flow

The standard 3-5 day wait for funds to clear is a relic of the past. It’s a delay that many SMEs simply cannot afford whilst managing daily overheads and supplier invoices. We’ve replaced this friction with next-day funding as a standard feature. Getting your money into your bank account within 24 hours ensures your cash flow remains fluid and predictable. It allows you to reinvest in stock or pay your team without the stress of a clearing cycle.

Our “Hub” approach centralises all your payment data into one clean, modern dashboard. You can track every sale across your mobile readers, countertop units, and virtual terminals in real time. This transaction-based reporting removes the guesswork from your finances. You won’t have to sift through complex statements to find hidden costs. Instead, you get a transparent view of your earnings, helping you maintain a disciplined approach to your business accounting.

Funding Your Future Growth

Sometimes, growth requires a capital injection that traditional banks are slow to provide. A Business Cash Advance offers a modern alternative by using your future card sales to fund current projects. Unlike a rigid bank loan with fixed monthly costs, this is a flexible arrangement where you repay as you earn. Repayments are calculated as a small percentage of your daily card takings, meaning they stay in sync with your actual performance.

If you have a quieter month, your repayments naturally decrease in proportion to your sales. This makes it a much safer option for card payment methods for small business UK than traditional debt. It’s a fair way to fund a new piece of equipment, a marketing campaign, or a shop fit-out. We know that time is your most valuable asset, so our onboarding process is designed to be completed within 24 hours. You don’t have to navigate corporate jargon or wait weeks for a decision. Once you’re live, our dedicated UK support team is always on hand to help you navigate any challenges.

We are here to ensure your payment infrastructure is a source of strength, not a cause of frustration. If you’re ready to experience a more transparent way of working, you can Get a transparent quote from PurePay Hub today. Let’s build a partnership that puts your growth first.

Future-Proof Your Business with Transparent Payments

The UK’s transition to a truly digital economy is complete. With contactless payments dominating 75% of debit transactions as of January 2026, your choice of card payment methods for small business UK determines your daily efficiency. You’ve seen how the right mix of hardware and remote links can streamline your operations. Now it’s time to ensure your processing costs are just as efficient as your service.

We believe in a partnership where your success comes first. This means providing debit rates from 0.3% and ensuring next-day access to your funds to keep your cash flow moving. We’ve removed the stress of hidden monthly compliance fees and complex contracts. You deserve a payment partner that acts as a reliable ally for your growth. Switch to PurePay Hub for transparent, transaction-based card payments and take control of your financial future today. Your business is ready for the next level of clarity.

Frequently Asked Questions

What are the cheapest card payment methods for small business UK?

Debit cards are the most cost-effective option because domestic interchange fees are capped at 0.2% under UK regulations. To keep costs low, you should choose a provider that offers transparent, transaction-based pricing rather than tiered models that hide markups. Avoiding monthly “non-compliance” fees and choosing hardware with no hidden rental costs will also protect your margins. For many SMEs, the most efficient card payment methods for small business UK are those that align fees directly with your actual sales volume.

Do I need a business bank account to take card payments?

Yes, you must have a dedicated business bank account to clear funds from a merchant services provider. UK regulations and anti-money laundering rules require a clear separation between personal and professional finances. This ensures that your tax records remain accurate and that your business income is easily auditable. Whilst some micro-payment apps might offer workarounds, a professional merchant account will always require a verified business bank account to ensure next-day funding arrives safely.

How long does it take to set up a card machine for my business?

Digital onboarding for a new merchant account can be completed in as little as 24 hours. Once your application is approved, physical hardware such as countertop or portable machines are typically dispatched via next-day courier. This means you can go from your initial enquiry to taking your first payment in just two or three working days. We prioritise speed and simplicity to ensure your trade isn’t interrupted by lengthy administrative delays or complex paperwork.

Can I take card payments on my phone without a machine?

Yes, you can accept contactless payments directly on a compatible smartphone using “Tap to Pay” technology. This has become a major trend in 2026 for mobile traders and service providers who don’t want to carry extra hardware. Alternatively, you can use payment links or virtual terminals to process transactions via your phone’s web browser. These methods are perfect for micro-businesses that need a flexible, software-led approach to their daily sales.

What is the difference between a merchant account and a payment gateway?

A merchant account is a dedicated holding area where your funds sit after a sale before being settled into your bank account. A payment gateway is the digital “tunnel” that securely sends card data from your website or virtual terminal to the banks for authorisation. Think of the gateway as the digital card machine and the merchant account as the temporary vault. You need both to accept online or remote payments, but they are often bundled together in one transparent package.

How much are typical card machine transaction fees in the UK?

For small businesses, typical transaction fees for card payment methods for small business UK range from 1.4% to 2.5% per sale. These rates depend on whether you are processing a domestic debit card, which is capped at 0.2% interchange, or a credit card, which is capped at 0.3%. Some providers offer flat-rate pricing, such as 1.69%, whilst others provide bespoke rates for businesses with a turnover exceeding £75,000. Always check for hidden “admin” fees that can inflate these base percentages.

Is it legal to charge customers extra for using a credit card in the UK?

No, it is illegal to charge customers a surcharge for using a consumer credit or debit card in the UK. This ban was introduced in January 2018 under the Payment Services Directive 2 (PSD2) to protect shoppers from unfair costs. You must build your processing fees into your general pricing strategy rather than adding them at the point of sale. This rule applies to both online and face-to-face transactions, ensuring a fair and transparent experience for every customer.

What happens if my card machine loses its Wi-Fi connection?

Professional card machines are designed with built-in redundancy to prevent lost sales during a connection failure. Most portable and mobile units will automatically switch to a GPRS or 4G mobile signal via a roaming SIM card if the Wi-Fi drops. Some devices also offer an “offline mode” or “Store and Forward” feature, which allows you to capture payment details and process them once the connection is restored. This ensures your checkout remains fast and reliable even in areas with patchy internet coverage.

Leave a Reply