Did you know that 87% of UK retail transactions are now cashless? In 2026, your payment terminal is the most critical piece of equipment in your building. Finding the best card machine for small retail shop owners is no longer just about convenience; it is about survival. You’ve likely felt the frustration of high transaction fees draining your daily takings or the stress of waiting days for funds to clear. Managing the latest PCI DSS v4.0 compliance standards shouldn’t feel like a second job when you’re busy serving customers.

We understand that every penny counts. You deserve a payment partner that offers total transparency and reliability during your peak hours. This guide will show you how to choose a card machine that slashes overheads and provides the next-day funding your cash flow needs. We will break down the latest merchant service trends, from the removal of contactless limits to the most dependable hardware on the market. By the end, you’ll have a clear path to a fairer, more efficient way to get paid.

Key Takeaways

- Identify why the best card machine for small retail shop owners in 2026 must serve as a central hub for growth rather than a simple card reader.

- Master the difference between restrictive flat-rate pricing and transparent interchange plus models to significantly reduce your monthly overheads.

- Protect your shop’s cash flow by selecting a payment partner that provides next-day funding and deep integration with your EPOS systems.

- Explore how modern tools like payment links and virtual terminals allow you to take secure payments anywhere without needing a physical terminal.

- Learn how PurePay Hub offers a fairer partnership with transparent transaction rates of 0.3% for debit and 0.5% for credit cards.

What is the Best Card Machine for a Small Retail Shop in 2026?

The definition of what a payment terminal is has undergone a radical transformation. Gone are the days when a card reader was merely a peripheral device tucked away at the end of a counter. In 2026, the best card machine for small retail shop owners acts as a central business hub. It synchronises your physical sales with your digital inventory; it tracks staff performance; and it ensures your cash flow remains fluid. If your current machine only “takes payments,” it is already holding your business back.

Choosing the right hardware requires a clear understanding of your shop’s daily rhythm. You aren’t just looking for a piece of plastic and silicon; you’re looking for a reliable partner that won’t fail during a busy Saturday afternoon rush. Modern retail management now relies on the seamless integration of hardware and software to eliminate manual errors and save hours of administrative work. Efficiency is the key to protecting your margins.

The Retail Shift: Why Cashless is No Longer Optional

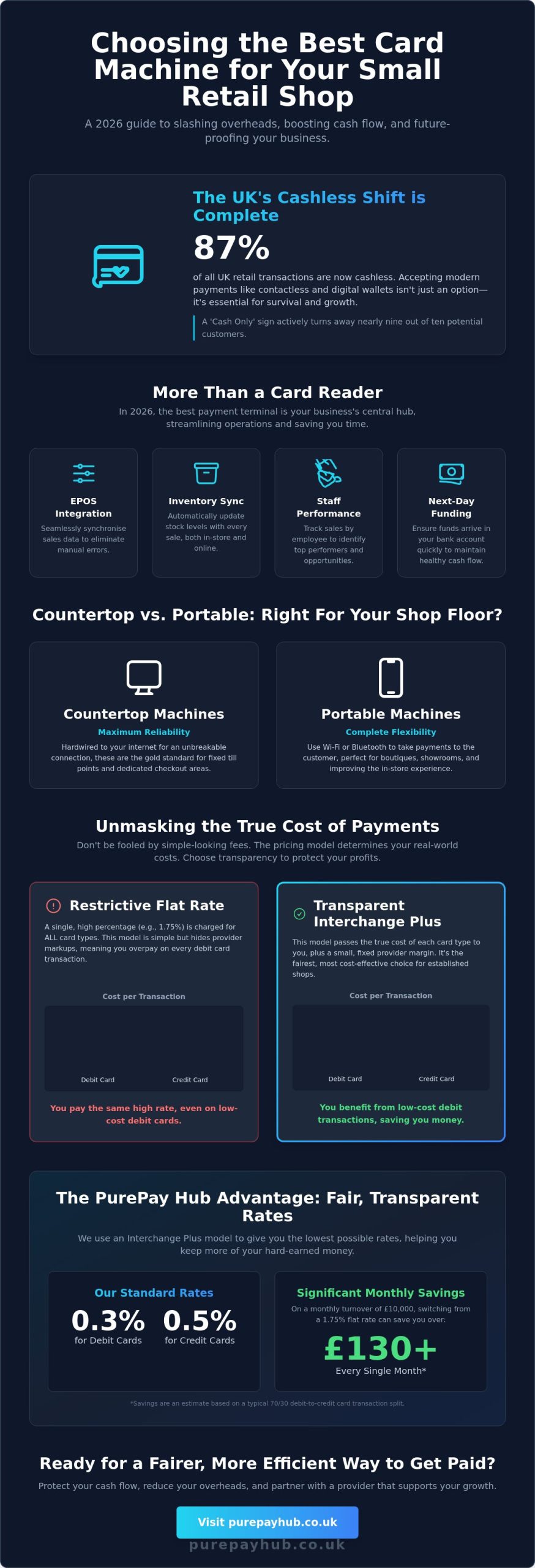

British consumer behaviour has shifted permanently. Recent data shows that 87% of UK retail transactions are now cashless. With the mandatory £100 contactless limit having been removed in March 2026, customers now expect the same “tap and go” convenience for high-value purchases that they once reserved for a coffee or a magazine. Digital wallets like Apple Pay and Google Pay have become the standard. If you display a “Cash Only” sign, you aren’t just being traditional; you’re actively turning away nearly nine out of ten potential customers. Accepting every major card and mobile wallet is the bare minimum for any shop aiming for growth.

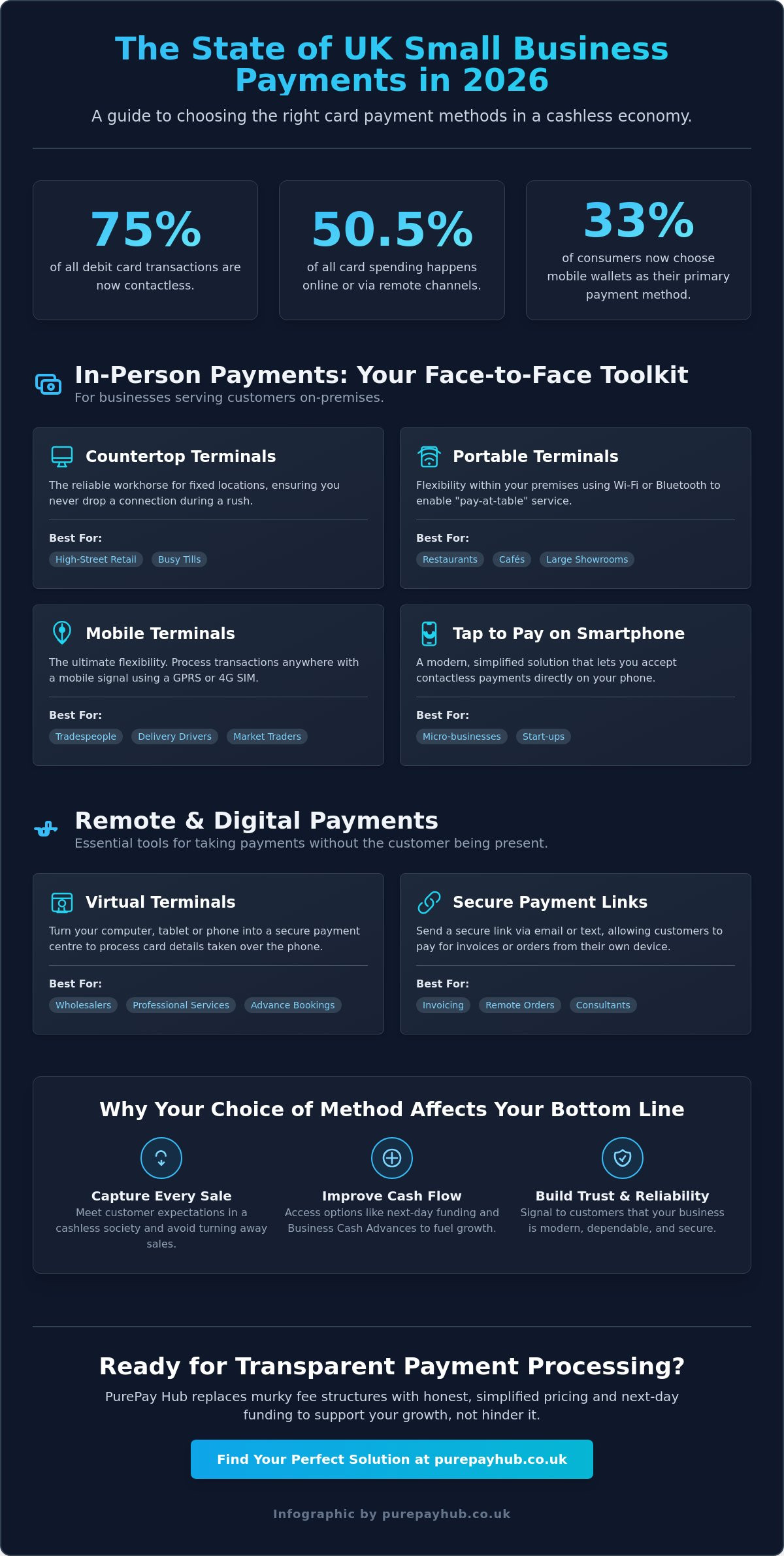

Countertop vs. Portable: Which Suits Your Shop Floor?

Selecting the best card machine for small retail shop environments often comes down to your physical layout. Countertop machines remain the gold standard for fixed till points. They offer the highest level of reliability because they are usually hardwired to your internet connection. This makes them perfect for traditional retailers with a dedicated checkout area.

Portable machines offer more flexibility. They use Wi-Fi or Bluetooth to allow you to take the payment to the customer. This is a game-changer for boutique clothing stores or furniture showrooms where closing the sale on the shop floor feels more personal and less transactional. Mobile readers are a different category entirely. Whilst they are popular for market stalls or pop-up events, they often rely on expensive flat-rate fee models that can eat into the margins of a permanent retail shop. For a dedicated storefront, a professional Countertop or Portable solution is almost always the more cost-effective choice.

Understanding the Real Cost of Payment Processing

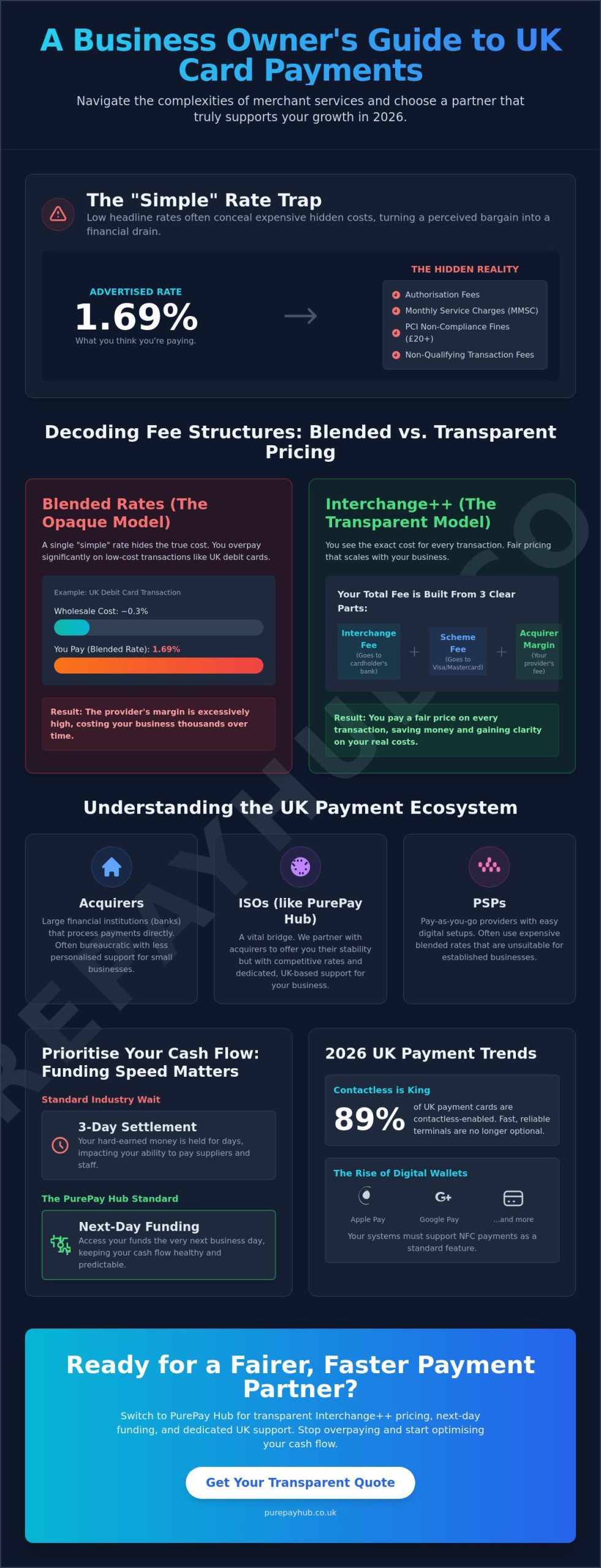

Merchant statements are often designed to be confusing. They hide markups behind complex terminology to prevent you from seeing exactly where your money goes. If you are searching for the best card machine for small retail shop operations, you must look past the headline price of the terminal. The true cost of your service is found in the transaction fees and the underlying pricing model. Many providers rely on “Flat Rate” models that charge a single high percentage regardless of the card type. This is simple, but it is rarely the most cost-effective choice for a growing business.

Established retailers benefit far more from an “Interchange Plus” model. This approach breaks down the cost into three parts: the interchange fee set by the card brand, the scheme fee, and the provider’s margin. It prevents your provider from hiding extra profits in a bloated flat rate. Whilst some best mobile credit card readers marketed to casual sellers use flat rates for simplicity, a professional shop needs more precision. Transparency is the only way to ensure you aren’t overpaying for every sale you make.

Transaction Fees: Debit vs. Credit Card Rates

Debit cards are the backbone of UK retail sales. They are significantly cheaper for providers to process than credit cards, yet many “no-nonsense” apps charge you the same high rate for both. This means they are pocketing the difference every time a customer pays with a standard bank card. Interchange Plus is the most transparent pricing structure for merchants. By using this model, you can access debit rates as low as 0.3%, compared to the 1.75% often found with entry-level apps. On a monthly turnover of £10,000, that difference represents hundreds of pounds kept in your own pocket rather than handed to a payment processor.

Hardware Rental vs. Outright Purchase

The “No Monthly Fee” myth is a common trap. Providers who don’t charge a rental fee for their hardware almost always compensate by inflating your transaction commissions. Buying a cheap reader outright might save you a few pounds today, but it can lead to expensive downtime if the device fails during a peak period. Professional merchant services usually offer hardware on a rental basis. This model includes several vital benefits:

- Automatic Upgrades: Your hardware stays current with the latest security and software standards.

- Inclusive Support: If your machine breaks, your provider is responsible for a swift replacement.

- Lower Rates: Monthly rental fees are usually offset by significantly lower transaction commissions.

Leasing a professional Countertop Card Machine ensures your till point remains a reliable pillar of your business. Switching to a transparent model like the one offered by PurePay Hub can immediately improve your bottom line by aligning your costs with your actual sales volume.

Top Features to Look for in a Retail Card Machine

When you search for the best card machine for small retail shop use, you must look beyond the sleek design of the hardware. The device is only as good as the features supporting your daily operations. Reliability is your first priority. A machine that loses connection during a Saturday afternoon rush isn’t just an inconvenience; it’s a direct loss of revenue. You need a terminal that offers dual-connectivity, switching seamlessly between Wi-Fi and 4G roaming SIMs to ensure zero downtime. This redundancy protects your business from local internet outages or weak signals.

Security is the next critical pillar. As of June 2026, all UK businesses must be fully compliant with PCI DSS v4.0. This is no longer a “tick-box” exercise but a requirement for continuous monitoring. With 43% of UK companies experiencing a data breach in the last year, robust encryption is your first line of defence. Your merchant partner should handle the heavy lifting of compliance. This ensures your shop operates within the UK Payment Services Regulations 2017 without you needing to become a cybersecurity expert yourself.

Next-Day Funding: Protecting Your Cash Flow

Standard settlement periods of three to five business days are a relic of the past. In a modern retail environment, your cash needs to be as agile as your inventory. Next-day funding ensures that Tuesday’s sales are in your bank account by Wednesday morning. This speed allows you to restock popular items immediately and maintain a healthy cash position. PurePay Hub understands that for a small shop, liquidity is life. We prioritise rapid settlements so you can focus on growth rather than waiting for your own funds to clear.

Integrated EPOS and Inventory Management

The best card machine for small retail shop environments is one that communicates perfectly with your other systems. Integrating your card machine with EPOS Systems eliminates the need for manual data entry at the till. When a sale is made, your inventory levels should update automatically. This reduces human error and slashes the time spent on end-of-day cashing-up. Instead of reconciling stacks of paper receipts, you get a clean, digital overview of your business performance. This integration turns your payment terminal into a powerful tool for queue busting and precise stock management.

Strategic Growth: Beyond Just Taking Payments

Selecting the best card machine for small retail shop use involves more than comparing hardware specs. It is about choosing a platform that acts as a gateway to essential financial tools. Your payment data is a valuable asset that can be used to prove the health of your business and unlock opportunities for expansion. Many shop owners don’t realise that their daily takings can become a bridge to the capital they need for growth. By moving beyond a simple “plug and play” reader, you gain access to a professional merchant profile that carries weight with lenders and suppliers alike.

We often hear from merchants who feel trapped by high fees but worry that switching is too difficult. They dread the potential for downtime or the complexity of setting up a new system. PurePay Hub solves this through a disciplined, managed onboarding process. We act as your supportive partner, organising the technical transition so you don’t miss a single sale. This straight-talking approach ensures you move from an expensive consumer app to a professional merchant account without the stress of traditional banking hurdles.

Unlocking Capital with Business Cash Advances

One of the most powerful benefits of a professional payment partner is the ability to access Business Cash Advance funding. Unlike a rigid bank loan with fixed monthly repayments, a cash advance is designed for the natural ebb and flow of retail. You receive an unsecured lump sum based on your average card turnover. Repayment is simple; you pay back a small, agreed percentage of your future card sales. If you have a quiet month, your repayments automatically decrease. This “repay as you earn” model protects your cash flow during seasonal dips, making it an ideal way to fund shop renovations or seasonal stock purchases.

Virtual Terminals and Remote Payments

The best card machine for small retail shop environments is one that doesn’t limit you to the physical counter. Modern retail is omnichannel. You should be able to take orders over the phone securely using a Virtual Terminal. This turns your computer or tablet into a secure payment point, allowing you to process transactions for local deliveries or bespoke orders without the customer needing to be present.

You can also use Payment Links to close sales directly through social media or email. By sending a secure link to a customer, you provide a professional checkout experience that mirrors an online store. These tools allow you to expand your local shop into a regional delivery hub, ensuring you never lose a sale just because a customer couldn’t make it to your storefront.

Ready to scale your retail business with a partner that values transparency? Contact PurePay Hub today to secure a fairer rate for your shop.

Why PurePay Hub is the Partner Your Shop Deserves

Choosing the best card machine for small retail shop owners often feels like a choice between two evils: high-street banks with archaic systems or faceless fintech apps with predatory flat rates. PurePay Hub was founded to offer a third way. We provide a transparent, professional alternative that treats you as a partner rather than just another transaction. Our goal is to stabilise your business finances through honest pricing and reliable hardware.

We don’t hide behind corporate jargon or complex fee structures. Instead, we offer a straight-talking service that prioritises your margins. By providing you with a dedicated merchant ID and professional support, we ensure your shop has the same financial tools as the national chains. You deserve a partner that understands the regional retail landscape and advocates for your success.

Transparent Rates and Fair Partnership

Profitability in retail is won in the small percentages. Whilst other providers might push you toward a 1.75% flat rate, we offer a model built on genuine clarity. Our competitive rates allow you to keep more of your hard-earned money from every sale:

- Debit Cards: 0.3% per transaction.

- Credit Cards: 0.5% per transaction.

- Zero Hidden Markups: No surprise fees for PCI compliance or statement access.

We believe that a fair partnership starts with knowing exactly what you are paying for every tap or swipe. This commitment to honesty is why so many UK merchants are moving away from restrictive app-based readers and joining the PurePay Hub community. We provide the stability your business needs to thrive in an increasingly cashless economy.

Getting Started: A Seamless Transition

We know that the biggest barrier to switching is the fear of disruption. You can’t afford a single hour of downtime at your till point. That is why we provide a managed onboarding process designed specifically for busy retailers. We handle the technical heavy lifting, from setting up your Countertop Card Machine to ensuring your EPOS Systems are perfectly synced. Our team also manages your transition to the latest PCI DSS v4.0 standards, giving you total peace of mind that your customer data is secure.

It’s time to reclaim the revenue your shop is losing to opaque fee models. Switching is simple; the savings start from the very first transaction you process. Don’t let high commissions hold back your retail growth any longer. Get a transparent quote from PurePay Hub today and discover how a fairer payment partner can transform your shop’s bottom line.

Take Control of Your Shop’s Financial Future

Your choice of payment hardware determines more than just how you take money. It dictates your cash flow, your inventory accuracy, and your ability to scale. Finding the best card machine for small retail shop owners in 2026 means looking for a partner that prioritises your margins over their own commissions. You’ve seen how transparent pricing models and integrated EPOS systems can remove the daily friction of running a busy storefront. Moving away from expensive, faceless apps is the first step toward reclaiming your revenue and stabilising your business.

By choosing a provider that offers debit card rates from 0.3% and next-day access to your funds, you ensure your shop remains agile and well-stocked. You don’t have to navigate these technical shifts alone. Our team provides the UK-based professional support you need to make the switch without missing a single sale. It is time to move beyond simple card reading and start using a payment system that actively supports your growth.

Join PurePay Hub for fairer, faster retail payments

We look forward to helping your business thrive with the honesty and clarity you deserve.

Frequently Asked Questions

What is the cheapest card machine for a small retail business?

The cheapest option depends on your transaction volume rather than just the upfront hardware cost. Whilst a basic mobile reader might cost less initially, a professional terminal with lower transaction rates often results in the lowest total cost of ownership for an established shop. You should always calculate the combined cost of hardware and monthly commissions to find the true value.

How much are the typical monthly fees for a card machine in the UK?

Monthly fees vary significantly based on your provider and the specific hardware you choose. Some providers offer “no monthly fee” models but compensate with higher transaction commissions; others charge a fixed rental fee for professional hardware to provide you with much lower processing rates. It is a balance between fixed overheads and variable transaction costs.

Can I get a card machine with next-day funding?

Yes, next-day funding is a standard feature for professional merchant services designed to support retail cash flow. This ensures your daily takings are settled into your account by the following morning, allowing you to restock inventory and manage overheads without waiting days for funds to clear. It is a vital tool for maintaining liquidity in a busy shop.

What is the difference between a merchant account and a card reader?

A card reader is the physical hardware used to take a payment, whilst a merchant account is the financial backend where your funds are held and processed. You need both to accept card payments; the reader captures the customer’s data, and the merchant account ensures the money is securely verified and transferred to your bank account.

Do I need a business bank account to use a card machine?

Most professional merchant service providers require you to have a dedicated business bank account to receive your settled funds. This is a standard security requirement in the UK that helps you keep your personal and professional finances separate whilst ensuring compliance with anti-money laundering regulations. It also projects a more professional image to your suppliers and partners.

How long does it take to switch card machine providers?

Switching providers typically takes between three to five working days once your application is approved. A managed onboarding process ensures that your new hardware arrives and is fully configured before you deactivate your old service. This prevents any disruption to your shop’s daily operations and ensures you don’t miss a single sale during the transition.

Are there card machines with no monthly contract?

Yes, several providers offer rolling monthly contracts or pay-as-you-go models with no long-term commitment. These are often considered the best card machine for small retail shop owners who are just starting out or running seasonal pop-up events. However, established shops usually find that a fixed contract offers much more competitive transaction rates and better hardware support.

What happens if my card machine loses its Wi-Fi connection?

Professional terminals with dual-connectivity will automatically switch to a 4G roaming SIM if your local Wi-Fi fails. This ensures you can continue taking payments without any interruption to your service. If your machine is a Wi-Fi only model, you may need to rely on a mobile hotspot until your primary internet connection is restored.