What if the biggest barrier to your next sale isn’t your stock or your prices, but the final thirty seconds your customer spends at the till? You have likely seen it happen: a shopper spots a long queue, sighs, and leaves their basket behind. It is a frustrating way to lose revenue, especially when outdated card machines or clunky EPOS systems are the primary culprits. Improving checkout experience in store is no longer just a luxury for UK retailers; it is a vital strategy for survival in a market where 42% of consumers still prefer shopping in person but have zero patience for friction.

We understand that you want a till point that works as hard as you do, without hidden fees eating into your hard-earned margins. This guide shows you exactly how to eliminate queues, modernise your payment hardware, and create a seamless journey that keeps customers coming back. We will explore the latest 2026 trends in portable card machines and intelligent EPOS systems, giving you the practical tools to turn your checkout from a bottleneck into a genuine competitive advantage.

Key Takeaways

- Understand the psychology of “queue anxiety” and how modern standards for speed directly influence customer loyalty and basket abandonment.

- Learn how to optimise your shop floor layout and use clear signage to guide customers naturally toward a frictionless point of sale.

- Discover how upgrading to high-speed payment hardware is the simplest way of improving checkout experience in store whilst protecting your margins.

- Explore strategies for training your team to balance technical efficiency with a professional, helpful British service style.

- See how integrating your EPOS and card machines through PurePay Hub creates a unified data view and supports your cash flow with next-day funding.

The Psychology of the Queue: Why Checkout Speed Matters in 2026

In 2026, a frictionless checkout is no longer a luxury; it is the baseline for modern British retail. UK shoppers have been conditioned by the lightning speed of online shopping to expect the same level of efficiency on the high street. When a customer reaches the end of their journey, they want to pay and leave without a struggle. This final interaction is your “Last Impression”. It is the memory that lingers long after they have left the shop. Even if your service was impeccable and your products are perfect, a slow or confusing till experience can sour the entire visit and stop a customer from returning.

This is where “Queue Anxiety” becomes a genuine threat to your bottom line. It is that sinking feeling a shopper gets when they see a line snaking through the aisles. It leads directly to basket abandonment. If the perceived wait time outweighs the value of the purchase, the customer will simply walk away. In 2026, consumer behaviour prioritises speed over almost all other in-store factors. Shoppers value their time more than ever, and they will reward businesses that respect it with their loyalty.

The Cost of a Poor Checkout Experience

A clunky till point does more than just lose a single sale. It damages your brand’s “Social Proof”. When passers-by look through your shop window and see a stagnant queue, they often decide not to enter at all. They assume your business is inefficient or understaffed. There is also a significant digital fallout to consider. A single bad experience often leads to negative online reviews, where “slow service” is a recurring complaint that deters potential visitors. Whilst some retailers have integrated self-checkout systems to manage the flow of smaller baskets, the primary goal remains the same: reducing the physical and mental effort required to finish a transaction. Improving checkout experience in store is about protecting your reputation as much as your revenue.

Setting Benchmarks for Your Store

You cannot improve what you do not measure. Start by tracking your average transaction time from the moment the first item is scanned until the payment is confirmed. Identify your “Peak Friction” hours; these are the times when your staff are busiest and your card machines are under the most pressure. Having a clear data view allows you to see where the bottlenecks actually occur. Improving checkout experience in store requires a clear target to aim for. The “Golden Three Minutes” is the maximum acceptable wait time for UK shoppers; once that limit is passed, customer satisfaction drops significantly. By making small, intentional changes to your workflow, you can ensure your team consistently hits this benchmark, even during the busiest periods of the day.

Optimising Your Physical Layout for Frictionless Flow

Your shop floor is more than just a showroom; it is a guided journey. Whilst the “Decompression Zone” at your entrance lets customers adjust to your environment, the path leading to the till must be equally intuitive. Improving checkout experience in store starts with a layout that removes physical barriers and psychological stress. If a customer feels trapped or crowded, their patience evaporates. You should aim for a flow that feels open and logical, guiding the shopper toward the exit without forcing them through a maze.

Research from Harvard Business School highlights the concept of Last Place Aversion, where customers at the end of a queue feel the highest level of dissatisfaction. You can combat this by using curved queuing paths or wider aisles that make the space feel expansive rather than cramped. Strategic placement of impulse items is a classic retail tactic, but you must avoid creating bottlenecks. Use low-profile shelving that doesn’t obstruct the view of the till. If customers can see the staff, their anxiety decreases. Bright, warm lighting at the point of sale also makes the wait feel shorter by creating an inviting atmosphere that signals the end of their journey.

Implementing Effective Line-Busting Strategies

Static counters often become the biggest hurdle during peak hours. You can solve this by deploying staff with a Portable Card Machine to process transactions amongst the aisles. This “line-busting” technique prevents a single long queue from forming and keeps the shop floor moving. Train your team to identify “Peak Friction” moments. When more than three people are waiting, a second “floating” till should open immediately. Reducing the physical footprint of your countertop payment centre also frees up space, making the area feel less congested and more professional.

Signage and Communication

Confusion is the enemy of efficiency. Use clear, favourite visual cues to direct customers to the correct area. If you have separate points for collections or returns, signpost them boldly. Improving checkout experience in store also means being transparent about technology. Clearly display that you accept Apple Pay, Google Pay, and all major contactless cards. This small detail prevents the “fumble for the wallet” moment at the till. During exceptionally busy periods, a staff member should manage the queue, offering a friendly greeting and a realistic estimate of the wait time to keep morale high.

Leveraging Modern Payment Hardware to Eliminate Bottlenecks

Your hardware is the engine room of your store. If your card machine is five years old, it is likely running on outdated processors that struggle with modern encryption standards. This creates a lag of several seconds per transaction. Whilst a few seconds sounds minor, it adds up to hours of lost productivity over a month of trading. Improving checkout experience in store requires hardware that processes payments at the speed of the customer’s intent. You need a system that responds instantly, ensuring the final step of the journey is as swift as the first.

Reliability is equally critical for a professional retail environment. A card terminal that loses its Wi-Fi connection during a busy Saturday afternoon is a disaster for shop floor morale and customer trust. Modern devices now feature “Always-On” connectivity with automatic 4G or 5G failover. If your broadband dips, your terminal switches to a mobile network instantly. This prevents the frustration of a stalled queue and ensures you never have to turn a customer away because your system is “down”.

Security should never be a bottleneck for your business. PCI compliance is a non-negotiable requirement for UK retailers, but it shouldn’t mean a clunky or slow interface. Modern terminals handle complex security protocols in the background, keeping your data safe whilst maintaining a rapid transaction flow. This balance of safety and speed is what defines a dependable payment partner.

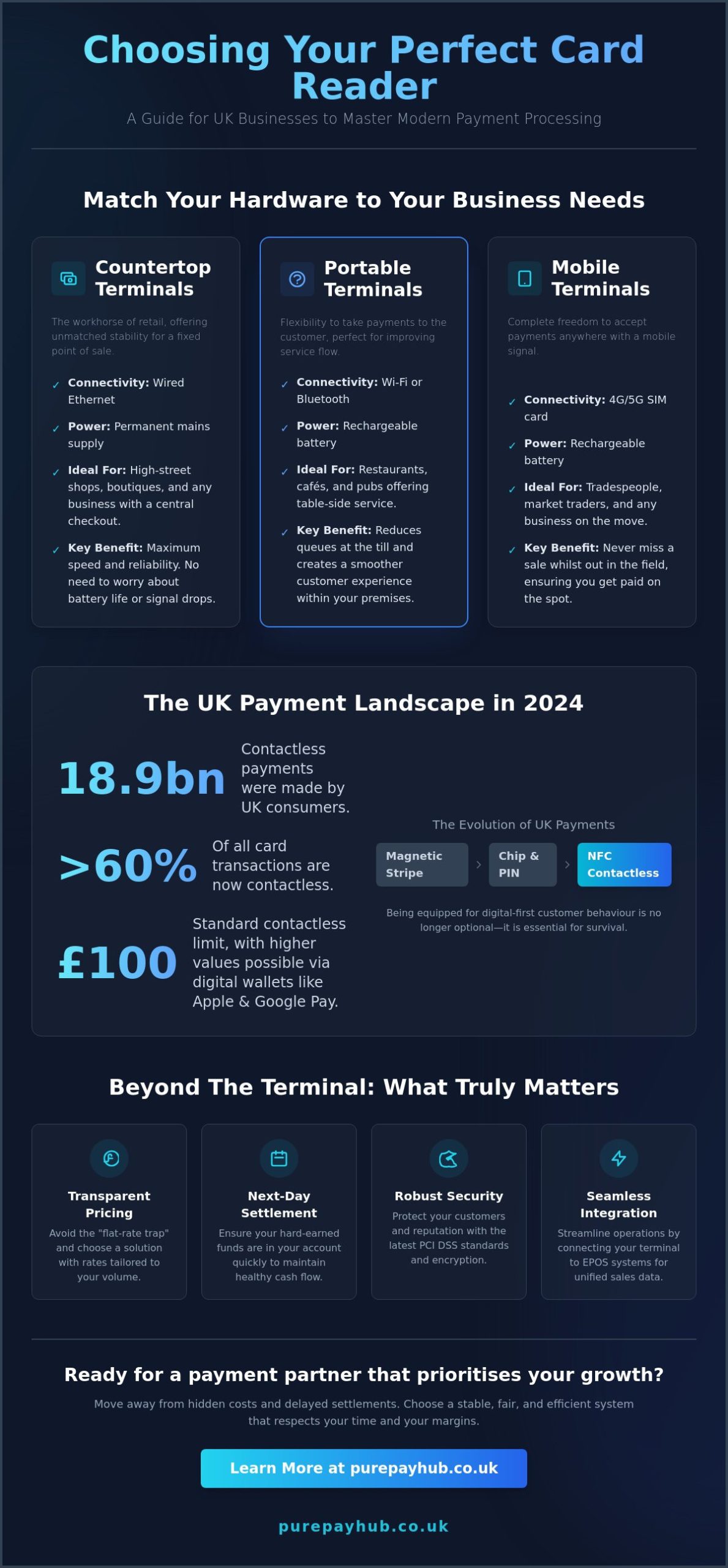

Choosing the Right Terminal for Your Store

- Countertop Card Machine: These are the workhorses of the high street. They are best for high-volume, fixed-position retail environments like newsagents, boutiques, or pharmacies where transactions happen at a central point.

- Portable Card Machine: These units are ideal for hospitality or large showrooms. They allow you to take the till to the customer, which is a highly effective way of reducing physical queues.

- Mobile Card Machine: Essential for pop-ups, market stalls, or “line-busting” during seasonal peaks. They offer the ultimate flexibility for businesses on the move.

The Rise of Digital Wallets

UK shoppers have fully embraced the digital wallet. In 2024, almost 95% of eligible in-store card transactions were contactless, and that trend has only accelerated. By 2026, Apple Pay and Google Pay have moved from being alternatives to being the preferred choice for many. These platforms use biometric authentication, such as FaceID or TouchID, which is significantly faster than entering a PIN. As the £100 single-transaction limit was removed in March 2026, customers can now use their phones for even larger purchases. Improving checkout experience in store means being ready for this shift. Preparing your hardware for the next wave of wearable payment technology, including smartwatches and payment rings, ensures your business remains modern and accessible.

Staff Training and the Human Element of the Transaction

Technology provides the framework, but your team provides the friction-free reality. Improving checkout experience in store requires a delicate balance between high-speed processing and a warm, professional British service style. Your staff are the face of your business. If they appear stressed or overwhelmed by a long queue, that tension transfers to the customer. A confident, well-trained employee can make a three-minute wait feel like thirty seconds simply through calm advocacy and clear communication.

Technical hitches are inevitable in retail. Whether it is a slow Wi-Fi signal or a momentary lag in the payment gateway, your staff must be trained to handle these moments without panicking. Instead of staring at a loading screen in silence, they should keep the conversation flowing. This prevents the customer from focusing on the delay. Discretion is also vital when resolving payment issues. If a card is declined, your team should handle it quietly. Suggesting an alternative method, such as trying a different terminal or using Payment Links for remote settlement, allows the customer to resolve the issue without embarrassment or stalling the rest of the queue.

The “Speedy Upsell” is a skill that combines sales with efficiency. Train your staff to suggest small, relevant items only whilst they are already scanning the main basket. If the suggestion requires a long explanation, it is not a checkout upsell. It should be a natural, five-second addition that increases your average basket value without adding a single minute to the total transaction time. This approach keeps the queue moving whilst maximising the potential of every visitor.

Efficiency Through Expertise

Every team member must be a “Power User” of your software. They should know the shortcuts and common functions by heart. Standardising the “Wrap and Pack” process is another simple way to shave seconds off every sale. By creating a favourite internal “Checkout Handbook”, you ensure that new starters adopt these efficient habits from day one. Investing in modern EPOS Systems ensures your team has the tools they need to maintain this high standard of service even during peak seasonal rushes.

Managing Returns and Exchanges

Mixed queues are a primary cause of frustration. A customer buying a single item shouldn’t be stuck behind someone processing a complex return. Where space allows, a separate desk for exchanges is vital for maintaining the main queue flow. Moving toward digital receipts also speeds up the post-purchase experience, as they are easier to store and retrieve than crumpled paper. An integrated EPOS system can process a return in under 30 seconds. This speed ensures that even the less pleasant parts of the shopping journey remain frictionless and professional, protecting your brand reputation and improving checkout experience in store for everyone.

Future-Proofing Your Store with PurePay Hub Solutions

PurePay Hub provides the stabilising force your business needs to thrive in a competitive market. By integrating your EPOS system directly with your card machines, we eliminate the need for manual data entry. This reduces human error and ensures your records are always accurate. Improving checkout experience in store is far easier when your back-office and your shop floor speak the same language. You get a unified data view that shows exactly how your store is performing in real-time, allowing you to make informed decisions with confidence and clarity.

Cash flow is the lifeblood of any retail operation, yet many traditional providers make you wait days for your funds to clear. We provide next-day funding as standard to ensure your business stays liquid and responsive. This allows you to maintain high stock levels and keep your shop floor morale high. When you aren’t waiting for your money, you can react faster to customer trends and seasonal demands. Our transparent pricing, including 0.3% debit rates, ensures you keep more of your hard-earned revenue. You can then reinvest these savings into better store layouts or staff development. If a technical hitch occurs, our 24/7 UK-based support is always ready to help. Your checkout will never stay offline for long.

Streamlining Your Back-Office

Automated reporting saves you hours of tedious admin time every week. It frees up managers to spend more time on the shop floor amongst the customers, where they are needed most. By using your transaction data, you can accurately predict your busiest periods with precision. This allows you to schedule enough staff for peak checkout times, preventing the queue anxiety that often leads to basket abandonment. Integrated systems simply make your business run more smoothly and professionally, turning your data into a tool for growth.

Scaling with Ease

Your business should never be held back by its technology or its finances. With PurePay Hub, you can add new terminals instantly as your customer base grows. Whether you need an extra Countertop Card Machine for a new till point or a Mobile Card Machine for a seasonal pop-up, the process is seamless and fast. We also offer a Business Cash Advance to help you fund store refurbishments or layout changes. This support ensures you can continue improving checkout experience in store as your brand evolves, keeping you ahead of the competition whilst maintaining a fair and honest partnership with your payment provider.

Click here to see how PurePay Hub can transform your in-store checkout experience today.

Take Control of Your Store’s Final Impression

Your checkout is the ultimate moment of truth for your business. By optimising your physical layout and investing in high-speed hardware, you remove the barriers that cause basket abandonment. We have explored how a combination of strategic signage, expert staff training, and reliable technology creates a journey that customers actually enjoy. Improving checkout experience in store isn’t just about speed; it’s about building lasting trust through every transaction.

You deserve a payment partner that prioritises your growth with fair, transparent terms. We offer debit card rates from 0.3% and provide next-day access to your funds, ensuring your cash flow remains as steady as your service. Our structure is built on honesty, with no hidden fees to worry about. It’s time to move away from clunky systems and opaque pricing models that hold your business back.

Upgrade your checkout experience with PurePay Hub today. Let’s turn your till point into your greatest asset and ensure every customer leaves your store with a smile.

Frequently Asked Questions

How can I reduce queues in my small shop without hiring more staff?

You can reduce queues by deploying portable payment technology that allows your team to process sales anywhere on the shop floor. This approach focuses on improving checkout experience in store by removing the reliance on a single fixed till point. By using line-busting techniques during busy periods, your existing staff can handle more transactions without the need for additional headcount. A logical layout and clear signage also help customers navigate your store more efficiently.

Is a portable card machine better than a countertop one for retail?

The choice depends on your specific shop layout and typical transaction volume. A Countertop Card Machine is a robust workhorse for businesses with a dedicated till area and high-speed requirements. However, a Portable Card Machine offers the flexibility to take payments directly to the customer, which is ideal for large showrooms or boutique environments. Many modern UK retailers now use a combination of both to ensure they can manage peak times effectively.

What is the fastest way to process a card payment in-store?

Contactless payments using digital wallets like Apple Pay or Google Pay are currently the fastest method available. These systems use NFC technology and biometric authentication, such as FaceID, which eliminates the need for a customer to enter a PIN. Since the single-transaction limit was removed in March 2026, these methods are even more efficient for higher-value sales. This speed is a critical factor in improving checkout experience in store for time-pressed shoppers.

How much do integrated EPOS systems cost for UK small businesses?

Costs for integrated EPOS systems vary based on the complexity of your inventory and the number of terminals you require. Rather than looking for the lowest headline price, you should focus on a transparent fee model that avoids hidden markups. A fair partner will provide a clear breakdown of costs, allowing you to understand exactly how your investment supports your back-office efficiency and real-time stock management without any unexpected surprises.

Can I use a mobile card reader for line-busting during busy periods?

Yes, a Mobile Card Machine is specifically designed for this purpose and is an essential tool for managing seasonal peaks. These devices connect via 4G or 5G networks, allowing your staff to process payments anywhere in the store or even outside. This flexibility prevents a single long queue from forming and ensures you don’t lose sales because of a perceived wait time at the main counter.

What are the benefits of Apple Pay for in-store checkout speed?

Apple Pay significantly reduces the total time spent at the till by removing the physical steps of finding a wallet and entering a PIN. The transaction is authenticated almost instantly via the customer’s phone or watch, making it one of the most frictionless methods available. It also offers enhanced security through tokenisation, which protects both your business and your customers from fraud whilst maintaining a rapid transaction flow.

How do I switch card machine providers without interrupting my store operations?

Switching providers is a straightforward process that involves a short period of parallel running. You should set up your new card machines and EPOS system whilst your current contract is still active to ensure there is no gap in service. A reliable provider will guide you through the configuration and testing phases, ensuring your team is fully trained before you make the final switch to the new system.

What is next-day funding and how does it help my retail business?

Next-day funding ensures that the money from your card sales is cleared into your business bank account on the following working day. This rapid access to your revenue is a vital stabilising force for your finances, allowing you to pay suppliers and manage stock levels without delay. It removes the stress of waiting for traditional clearing cycles, giving you a much clearer view of your daily cash position.