That “low-cost” card reader you bought outright might actually be the most expensive piece of kit in your shop. Many UK business owners choose to buy hardware to avoid monthly fees, only to find themselves stuck with obsolete tech when security regulations shift. When weighing up card machine rental vs buying UK, the right choice depends on more than just the initial price tag. You’ve likely felt the sting of hidden markups or the frustration of a long-term contract that feels like a trap. We believe in a no-nonsense approach that puts clarity and honesty first.

You deserve a payment setup that supports your growth instead of holding it back. This guide will show you how to calculate the best value for your business by comparing total costs, contract flexibility, and ongoing technical support. We’ll explore how the 2026 removal of the £100 contactless cap and mandatory PCI DSS v4.0 compliance impact your hardware choice. You’ll gain the confidence to decide whether a mobile card machine you own or a countertop terminal you rent offers the fairest deal for your till.

Key Takeaways

- Understand how the rapid shift to a cashless society and strict security regulations make your choice of hardware a critical business decision.

- Learn how to calculate the true break-even point in the card machine rental vs buying UK debate to ensure your payment setup remains profitable as volume grows.

- Discover why rental models often suit established businesses by bundling technical support and automatic upgrades to prevent hardware obsolescence.

- Evaluate the freedom of the pay-as-you-go model for smaller ventures, where owning your device removes monthly overheads during quieter periods.

- Find out how PurePay Hub provides transparent, jargon-free merchant services that balance high-quality hardware with fair, sustainable transaction rates.

Understanding the UK Card Payment Landscape in 2026

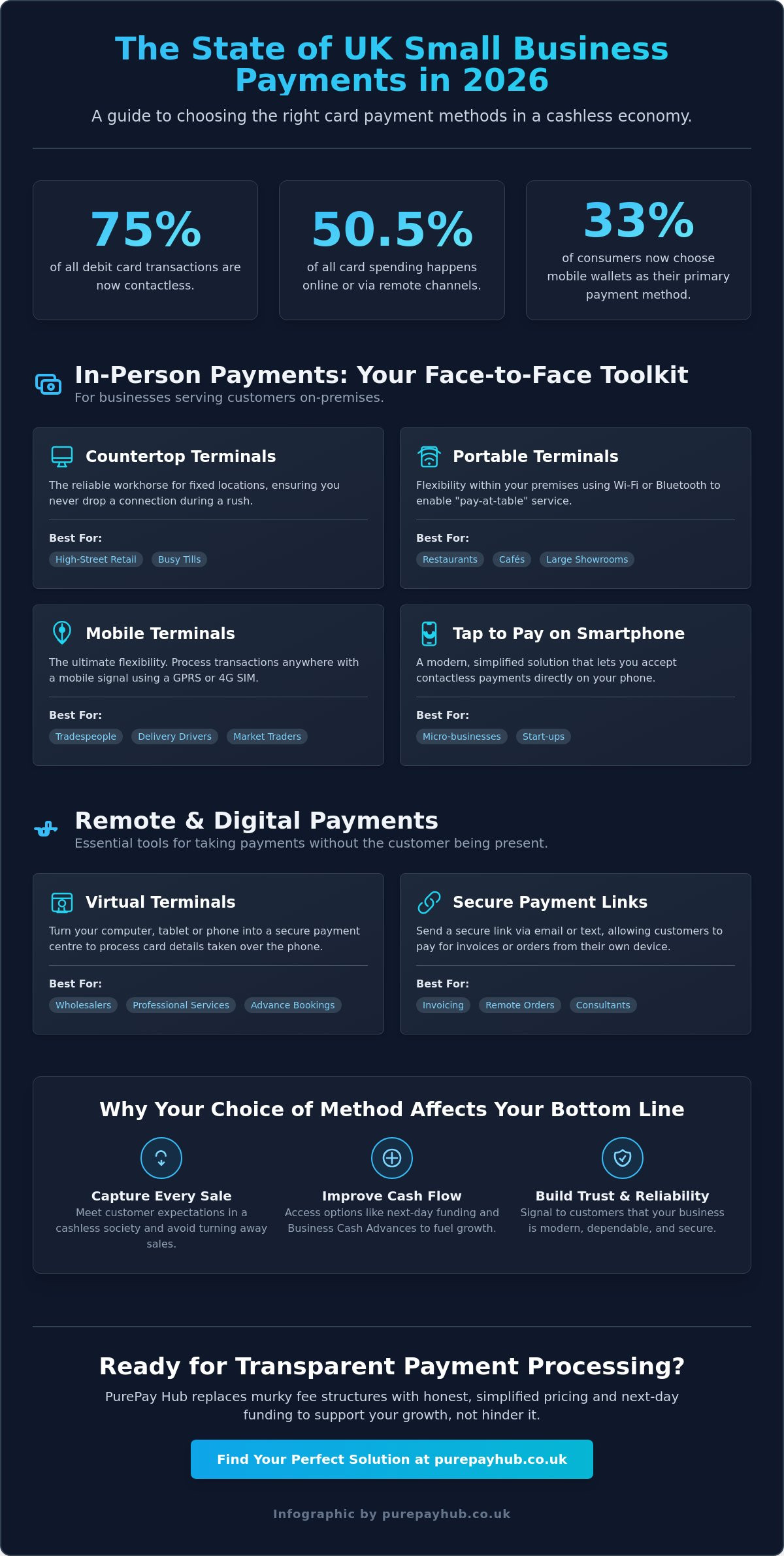

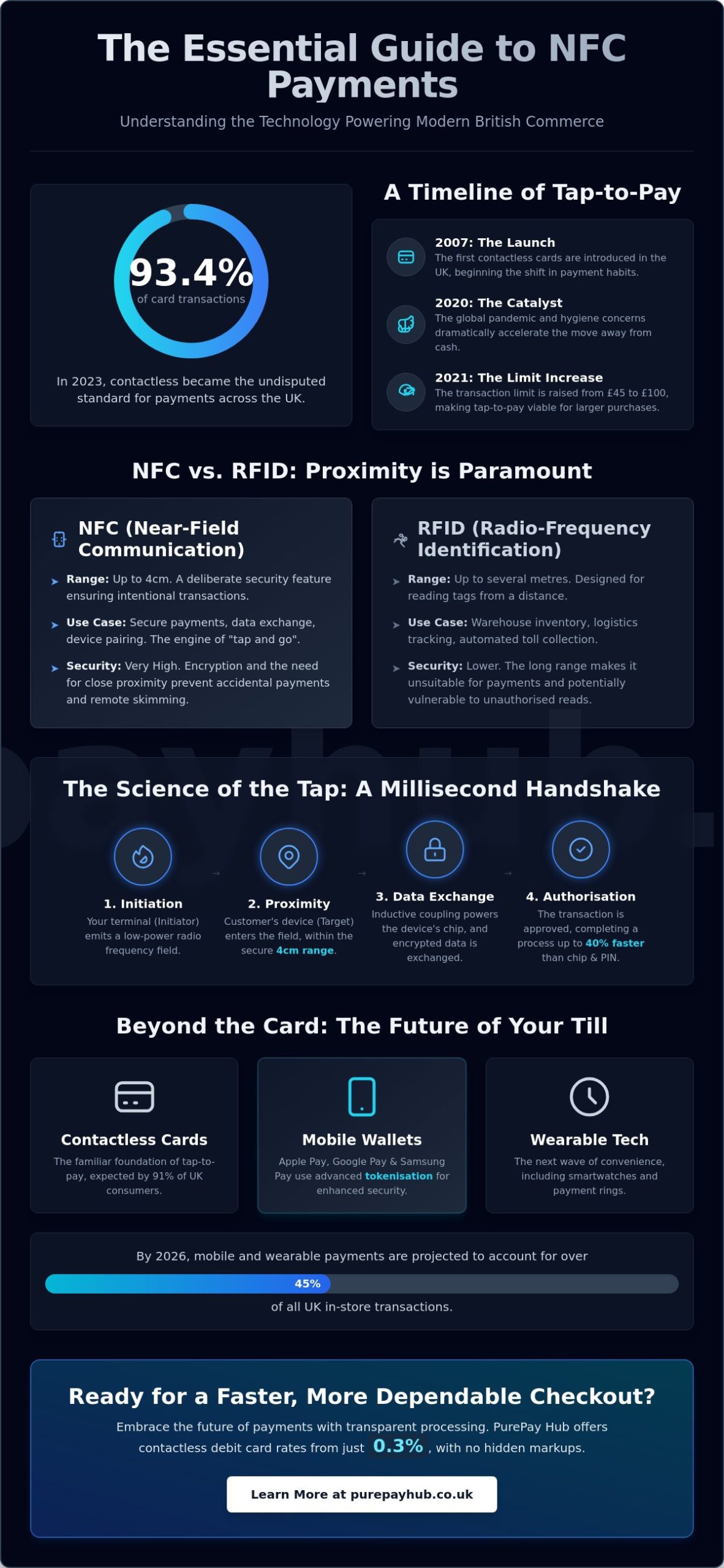

British consumers have largely moved away from physical coins and notes. By late 2025, contactless payments accounted for 76% of all debit card transactions in the UK. This isn’t just a trend; it’s the new standard for every high street shop and local cafe. The Payment Systems Regulator (PSR) has recently enforced stricter rules on contract transparency. These changes prevent merchants from being trapped in long-term, opaque agreements that don’t serve their interests. This regulatory shift makes the debate of card machine rental vs buying UK more relevant than ever. You now have more power to choose a path that truly fits your business model.

Your decision between ownership and a managed service directly impacts your daily cash flow. Buying hardware outright requires an immediate capital outlay. That money might be better spent on stock, staff, or marketing. Rental models spread this cost into predictable monthly payments. At PurePay Hub, we believe in a no-nonsense approach to these costs. A managed service often includes support and maintenance, providing a stabilising force for your finances. Whether you need a countertop card machine or a mobile unit, your choice will dictate how smoothly your till operates during the busiest periods.

The Evolution of Card Machines

The days of clunky, dial-up hardware are gone. Modern businesses now rely on integrated smart terminals that do much more than just process a transaction. If you’re interested in the technical background, you can explore what is a payment terminal to see how these devices have evolved from basic swipe tools into high-speed computers. Digital wallet adoption is soaring. In 2024, 57% of UK adults were registered for a mobile wallet. For a growing SME, a basic card reader might feel restrictive. You need a device that handles inventory, integrates with your EPOS, and processes Apple Pay or Google Pay instantly.

Regulatory Standards and Security

Security is a non-negotiable part of modern trade. As of March 31, 2025, every UK merchant must be fully compliant with PCI DSS v4.0 standards. This update introduced mandatory multi-factor authentication and more frequent vulnerability scanning. Staying compliant is a significant burden if you own your hardware. You’re responsible for every software patch and security update. Managed rental services simplify this. They often automate these security requirements, ensuring your terminal is always up to date. The Financial Conduct Authority (FCA) oversees the industry to ensure fairness, but the practical task of protecting cardholder data remains your responsibility. A managed service acts as a reliable partner in this process.

The Case for Card Machine Rental: Managed Services and Support

Choosing a rental model is often about more than just avoiding an initial purchase price. It is a strategic decision to prioritise business continuity. When you compare card machine rental vs buying UK, the most immediate benefit is the preservation of your capital. Instead of spending hundreds of pounds on hardware, you keep that cash for stock or marketing. This approach turns a lumpy capital expense into a predictable, fixed monthly operating cost. It simplifies your bookkeeping and ensures there are no nasty surprises when a device needs replacing.

Technology in the payments industry moves at a relentless pace. A machine that is top-of-the-range today might struggle with new security protocols or software updates in two years. Rental agreements solve this problem by offering continuous hardware upgrades. You aren’t stuck with obsolete kit that slows down your service. Instead, your provider ensures your terminal remains compliant with the latest UK Payment Services Regulations. This peace of mind is invaluable for busy merchants who don’t have time to track regulatory shifts.

Hardware Maintenance and Swap-Out Services

Downtime kills profit. Imagine your card terminal failing on a busy Saturday afternoon whilst a queue of customers waits. If you own the device, you’re responsible for the repair or the cost of a new unit. With a managed rental service, technical support is part of the package. Most professional contracts include a swap-out service where a faulty machine is replaced within one business day. The cost of a single day of lost sales often far outweighs a year of rental fees. A reliable portable card machine from a managed provider acts as an insurance policy for your revenue.

Software Updates and Remote Management

Modern payment terminals are sophisticated computers that require regular maintenance. Managed rental services handle automatic security patching and feature updates remotely. This is particularly useful if you manage multiple terminals across different sites. You can ensure every device is running the same software version without manual intervention. These systems also offer seamless integration with cloud-based EPOS systems. This connectivity allows for real-time reporting and better inventory management. By choosing a managed path, you delegate the technical headaches to experts, allowing you to focus on serving your customers and growing your brand.

Buying Outright: Ownership, Flexibility, and Pay-As-You-Go

Buying your hardware outright feels like the ultimate freedom for many new ventures. You pay for the device once and it’s yours. There are no monthly rental fees to worry about during a slow month. This “pay-as-you-go” model is particularly attractive for micro-businesses or seasonal traders who only need to process payments occasionally. Onboarding is typically fast and digital, letting you start taking cards within days. However, when evaluating card machine rental vs buying UK, the initial purchase price is often a distraction from the true cost of doing business.

The real expense isn’t the plastic and silicon in your hand; it is the transaction rate attached to it. Most “buy-only” providers use a flat-rate fee structure. Whilst this is simple to understand, it is rarely the most cost-effective path for a growing merchant. As your volume increases, those higher flat rates eat into your margins far more than a modest monthly rental fee would. You are essentially trading a low monthly overhead for a permanent tax on your growth. This is the “Total Cost of Ownership” trap that many small businesses fall into during their first year of trade.

The Hidden Costs of Ownership

Ownership brings a level of responsibility that can be stressful during peak times. If your owned terminal stops working, you are the one who pays for the fix. Batteries eventually lose their capacity, and screens can crack during a busy shift. Unlike a managed service, there is no “next-day swap” included in your purchase price. You’ll either pay for an out-of-warranty repair or buy a whole new unit, all whilst losing sales in the meantime. There is also the risk of technical obsolescence. As network standards shift or security requirements tighten, an owned device can quickly become a paperweight that you cannot upgrade without buying a new one.

Transaction Fee Structures for Owned Devices

Simplicity often comes at a premium. Flat-rate providers usually charge significantly more per transaction than traditional merchant accounts. They don’t offer bespoke pricing for high-volume traders because their model relies on a “one size fits all” approach. According to recent UK Payment Market Trends, the dominance of debit cards and contactless payments means your transaction volume will likely grow faster than you expect. For a busy retail or hospitality environment, the “Interchange-plus” models typically found with managed services are almost always cheaper than the flat rates found on owned devices. You must decide if the lack of a monthly fee is worth the long-term drain on your profits.

The Decision Matrix: Which Model Suits Your Business?

Choosing between card machine rental vs buying UK shouldn’t be a guessing game. It requires a cold, hard look at your growth trajectory rather than just your current bank balance. Many small business owners make the mistake of choosing a payment setup based on where they are today. A smarter approach is to choose based on where you plan to be in twelve months. If your monthly turnover is climbing, those “no-fee” readers with high transaction rates will quickly become a heavy tax on your success. You need a model that scales with you, not one that penalises your hard work.

The break-even point is the most critical metric in this decision. For micro-businesses processing very low volumes, buying a basic reader often makes sense. However, once your sales reach a consistent level, the lower transaction rates offered by managed rental accounts usually offset the monthly fee. This transition is a hallmark of a maturing business. It marks the shift from a “side hustle” mentality to a professional operation that values efficiency and long-term profit over short-term savings.

High-Volume vs. Low-Volume Merchants

High-volume businesses almost always find better value in a rental model. Traditional merchant accounts often provide “Interchange-plus” pricing, which is significantly more transparent than the flat rates found on bought devices. Seasonal businesses, like Christmas markets or summer festivals, might prefer the “pay-as-you-go” flexibility of an owned device. But if you find yourself processing payments every day, it’s time to consider a managed terminal. Moving from a bought reader to a professional setup is simpler than you think and can save you hundreds of pounds in transaction fees over a single year.

Sector-Specific Requirements

Your industry dictates your hardware needs. In hospitality, you need robust, portable card machines that can handle a full shift on one charge and integrate seamlessly with your EPOS system. Retailers, on the other hand, prioritse countertop reliability and blistering checkout speeds to keep queues moving. For mobile services like plumbers or electricians, 5G connectivity is the 2026 standard. You can’t afford to stand on a doorstep waiting for a 3G signal that no longer exists. Modern rental units now include biometric security, such as fingerprint or facial recognition, ensuring that high-value transactions are as secure as possible. This level of tech is rarely found on entry-level readers you buy outright. Future-proofing your business means choosing a partner who provides the latest hardware as standard.

PurePay Hub: Transparent Solutions for UK Merchants

PurePay Hub acts as a stabilising force for your business finances. We understand that the debate over card machine rental vs buying UK often leaves merchants feeling skeptical and frustrated. Our approach removes the guesswork by balancing high-grade hardware with industry-leading transaction rates. We don’t believe in the opaque pricing models used by traditional banks. Instead, we offer a no-nonsense service that prioritises your profit margins and operational efficiency.

Cash flow is the lifeblood of any regional business. Waiting days for your funds to clear is a burden you shouldn’t have to carry in 2026. We provide next-day funding as standard to ensure your revenue is available when you need it most. This commitment to speed extends to our support. We provide a modern fintech experience without losing the personal touch that local business owners value. Whether you are using a countertop card machine or our online payment gateway, our systems are designed to keep your trade moving without interruption.

We support your long-term growth with a suite of integrated tools. Our EPOS Systems provide the deep insights you need to manage inventory and staff effectively. If you need to expand or refurbish your premises, our Business Cash Advance offers a fair and flexible way to access capital based on your card turnover. We are more than just a terminal provider; we are a dedicated partner in your business development.

A Partnership Approach to Payments

We treat every merchant as a long-term ally rather than a distant account number. Our fee structure is built on a foundation of honesty and integrity. You will never find hidden markups or surprise “admin fees” in our statements. This transparency is a core identity of the PurePay Hub brand. If you ever run into a technical snag, you won’t be directed to an automated chatbot. You’ll have access to UK-based support experts who understand the local market and can provide decisive resolutions quickly.

Getting Started with PurePay Hub

Moving your payment processing to a fairer provider is a simple, stress-free process. Our onboarding is designed for efficiency, taking you from your initial enquiry to taking live payments with minimal fuss. We help you customise your setup to match your specific trade environment. You can choose from a range of hardware options to suit your needs:

- Countertop Card Machine: Ideal for fixed retail points and fast-paced checkouts.

- Portable Card Machine: Perfect for hospitality businesses serving customers at tables.

- Mobile Card Machine: The standard for tradespeople and mobile services requiring 5G connectivity.

You deserve a payment partner that values your business as much as you do. Take the first step toward a more transparent and supportive merchant service today. Get a transparent quote from PurePay Hub today.

Secure Your Business Future with a Smarter Payment Strategy

The choice between ownership and rental isn’t just about a one-off payment. It’s about ensuring your till never stops ringing during a busy Saturday. We’ve explored how the card machine rental vs buying UK decision impacts your long-term margins and technical resilience. Owning a device might offer a quick start for a side hustle. However, a managed service provides the security of automatic updates and hardware that never goes obsolete. Your business deserves a setup that’s as modern and dependable as the service you provide.

You don’t have to tolerate the stress of hidden markups or opaque fee structures. We focus on clarity and fairness. With debit card rates starting from 0.3% and next-day access to your funds, we help you keep your cash flow healthy and your finances stable. Take control of your processing costs and build a partnership that actually supports your growth. It’s time to move away from distant financial institutions and work with a local expert who values your success.

Switch to a fairer way of taking payments with PurePay Hub

Frequently Asked Questions

Is it cheaper to rent or buy a card machine in the UK?

The answer depends on your monthly transaction volume and your need for technical support. Buying a machine often has a lower upfront cost, but it usually comes with higher transaction fees that can eat into your profits. Renting a machine typically offers lower rates and included maintenance, making it more cost-effective as your sales grow. When evaluating card machine rental vs buying UK, you should calculate the total cost of ownership over two years rather than just the initial price.

What is the average monthly rental cost for a card terminal?

Monthly rental costs vary based on the specific hardware you choose and the length of your service agreement. These fees generally cover the physical device, mandatory security updates, and access to technical support. You’ll find that a fixed monthly fee provides more stability for your business budgeting than the unpredictable costs of repairing or replacing owned hardware. We recommend requesting a transparent quote to see exactly what is included in your service package.

Can I switch from buying to renting if my business grows?

You can certainly upgrade your payment setup as your business matures. Many small traders start with a basic bought reader to keep overheads low during their first few months. Once your turnover reaches a consistent level, switching to a managed rental service allows you to access professional-grade hardware and lower transaction rates. This transition is a logical step for any business that wants to prioritise efficiency and profit as they scale.

Are there hidden fees in card machine rental contracts?

Traditional providers often hide extra charges in their contracts, but modern fintech companies are moving toward a no-nonsense approach. The Payment Systems Regulator (PSR) has introduced new rules to ensure UK merchants receive clearer information about their agreements. You should always look for a provider that offers a transparent breakdown of every cost. Avoid contracts that include vague “admin fees” or “PCI management charges” without a clear explanation of the value they provide.

Do I need a merchant account if I buy my own card reader?

You always need a merchant account or a payment processing service to accept card payments. Some providers that sell readers outright bundle the hardware and the account together for simplicity. Managed rental services often provide a dedicated merchant account, which can offer more bespoke pricing and better stability for established businesses. This setup ensures that your funds are handled securely and reach your bank account as quickly as possible.

What happens if my rented card machine breaks?

Technical support is a core benefit of a managed rental agreement. If your machine fails, your provider will usually troubleshoot the issue remotely or send a replacement unit to your premises. This swap-out service often happens as quickly as the next business day. This minimises downtime and prevents the frustration of turning away customers during a busy shift. If you own your machine, you’re responsible for the cost and delay of a repair.

How long are typical card machine rental contracts in 2026?

Contract lengths have become much shorter and more flexible in 2026. You’ll find many agreements now range from 12 to 18 months, which is a significant improvement over the old four-year lock-ins. This shift gives you the freedom to review your payment setup and ensure it still meets your needs as your business evolves. Always check the notice period and exit terms before signing any new agreement.

Does buying a card machine affect my transaction rates?

Buying a machine outright often limits you to a flat-rate transaction model, which can be more expensive for high-volume traders. Managed rental services generally provide access to more competitive, variable rates that save you money as your sales increase. Choosing card machine rental vs buying UK is often a trade-off between low monthly overheads and the long-term savings of a professional merchant account. You must decide which model offers the best value for your specific growth trajectory.