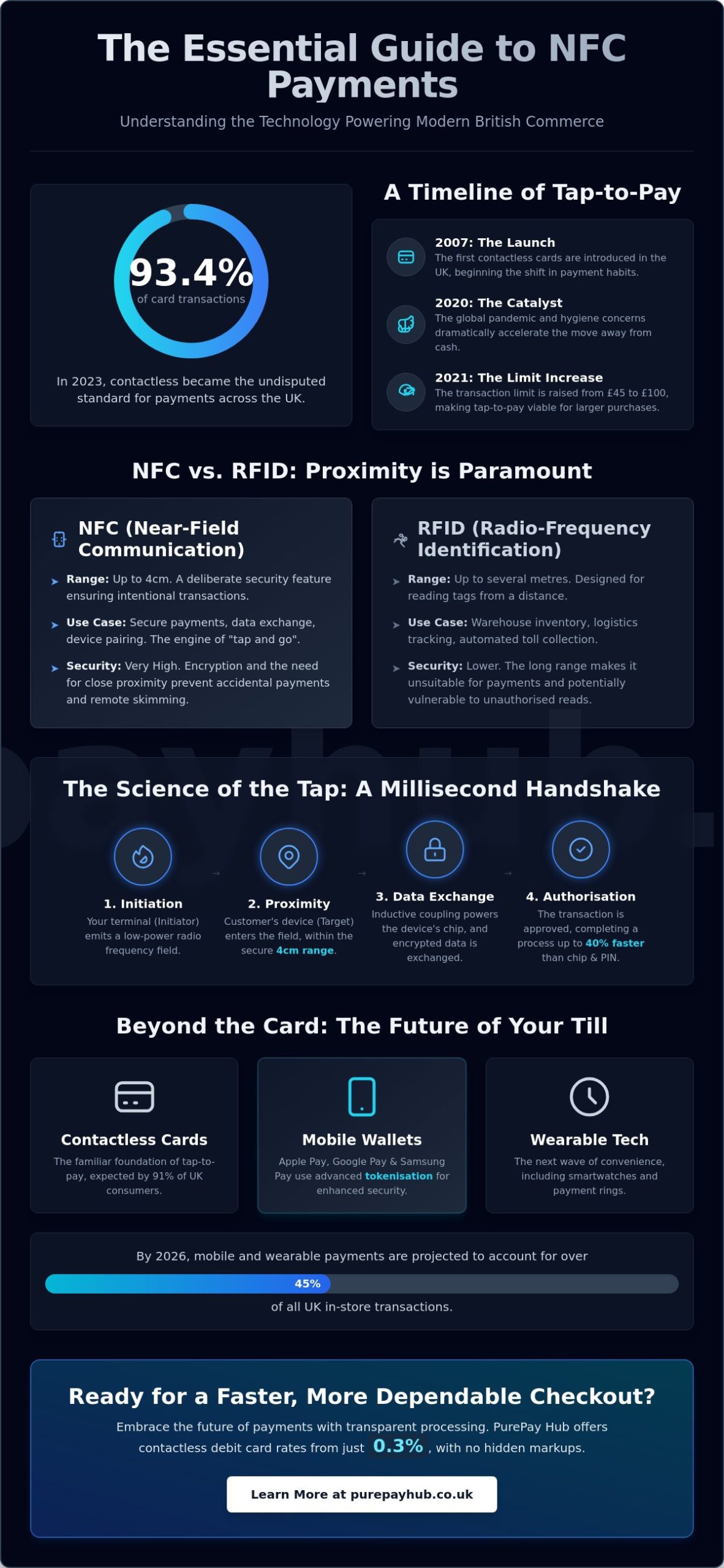

According to UK Finance, contactless payments accounted for 93.4% of all card transactions in 2023. By 2026, a merchant without a reliable nfc strategy will struggle to keep pace with the expectations of the British high street. You likely feel the pressure of peak-hour queues and the constant need to reassure customers that their digital data is safe. You don’t want technology to be a barrier; you want it to be a bridge to better service.

We believe in a pure and transparent approach to payment processing that puts the merchant first. This guide will show you how Near-Field Communication works to streamline your operations whilst improving customer satisfaction. You will learn the clear differences between NFC and RFID, discover how to integrate mobile wallets like Apple Pay seamlessly, and find out how to secure your business against modern fraud. We are moving beyond the jargon to give you the clarity you need for a faster, more dependable checkout hub.

Key Takeaways

- Understand why contactless payments have become the non-negotiable standard for British consumers and how this shift impacts your daily operations.

- Master the mechanics of nfc technology, from the deliberate 4cm security range to the advanced tokenisation that keeps your transactions safe from fraud.

- Identify the ideal hardware for your specific business flow, whether you require a fixed countertop terminal or a portable device for mobile service.

- Discover how to eliminate hidden markups and access transparent processing rates, with debit card charges starting from just 0.3% for contactless payments.

- Learn how to streamline your checkout process to reduce queues and significantly enhance customer satisfaction through modern payment solutions.

What is NFC and Why is it Essential for UK Merchants?

Near-field communication (NFC) is a short-range wireless technology that allows two devices to communicate when held within 4 centimetres of each other. NFC is a proximity-based data transfer protocol operating at 13.56 MHz. For a British business owner, it’s the invisible engine behind every “tap and go” transaction at your till. Unlike older systems, it offers a secure, encrypted handshake that protects both your revenue and your customer’s data. This technology turns a standard payment terminal into a high-speed gateway for modern commerce.

Understanding the difference between NFC and RFID is vital for your point of sale. While RFID can track items from several metres away, NFC is strictly limited to close range. This physical proximity is a security feature; it ensures that a customer cannot accidentally pay for someone else’s shopping whilst standing in a queue. It provides the “tap and go” experience that 91% of UK consumers now expect at the checkout. At PurePay Hub, we see this technology as the foundation of a transparent and efficient transaction model.

The Evolution of Contactless Payments in the UK

The UK payment landscape changed forever in 2007 with the introduction of the first contactless cards. Adoption was steady until the COVID-19 pandemic in 2020. During that period, hygiene concerns accelerated a massive shift away from cash. In October 2021, the UK government increased the contactless limit from £45 to £100. This change allowed merchants to process the vast majority of all card transactions via contactless, significantly increasing average transaction speed. Contactless is no longer a convenience; it’s the default behaviour for 87% of UK shoppers.

NFC Beyond the Credit Card

Your customers are increasingly leaving their physical wallets at home. The rise of mobile wallets like Apple Pay, Google Pay, and Samsung Pay has turned smartphones into secure payment hubs. These digital wallets use tokenisation to hide actual card details, making them even more secure than traditional plastic. Beyond phones, wearable technology is gaining ground. Smartwatches and even payment rings now utilise this technology to facilitate instant transactions. By 2026, these alternative form factors are expected to account for over 45% of all in-store payments in the UK. We provide the clarity and tools you need to accept every tap with confidence.

How NFC Technology Works: The Science of the Tap

NFC technology isn’t magic. It’s precision engineering designed for the modern UK high street. At its core, the process involves an “Initiator” and a “Target.” Your card terminal acts as the initiator, constantly emitting a small radio frequency field. When a customer brings their phone or card within 4cm, that device becomes the target. This 4cm limit is a deliberate security feature. It ensures that transactions only happen when intended, preventing accidental payments from passersby or “skimming” from a distance. It’s a short-range constraint that provides a long-range sense of security for your customers.

There are three distinct modes of nfc operation that power today’s digital economy. Card Emulation is the most common for merchants, allowing a smartphone to act exactly like a physical credit card. Reader/Writer mode lets your terminal pull data from smart tags or posters. Peer-to-Peer allows two devices to swap information directly. This system operates at the speed of light, making it significantly faster than the old magnetic stripe method. Traditional stripes rely on physical friction and analogue data reading, which is slow and prone to wear. NFC uses digital packets sent via radio waves, reducing transaction times by up to 40% compared to older contact-based methods. For a busy London cafe or a retail shop in Birmingham, these seconds saved per customer directly translate to shorter queues and higher turnover.

Inductive Coupling Explained

NFC relies on inductive coupling to transfer power and data simultaneously. Your terminal’s internal antenna creates an electromagnetic field. When a contactless card enters this field, the card’s own antenna picks up the energy. This powers the chip without needing a battery. Physical contact isn’t actually necessary. The term “tap” is simply a user-friendly way to describe bringing two antennas into close proximity. It’s a pure, wireless handshake that happens in milliseconds, ensuring the data remains encrypted and the connection remains stable throughout the brief interaction.

Data Exchange Protocols

Security relies on strict global standards to maintain integrity. Most payment systems use ISO/IEC 14443. This protocol ensures that a terminal in Manchester can talk to a card issued in New York without friction. Implementing NFC correctly means choosing hardware that adheres to these standards whilst remaining updateable. As software evolves, your hardware must stay compatible with new encryption methods. At PurePay Hub, we believe your payment nfc setup should be a stable foundation for your business growth. If you want to simplify your checkout and remove technical headaches, you can explore our transparent terminal options to find a partner that values your time.

Security and Trust: Is NFC Safe for Your Business?

Many UK business owners worry about nfc signals being “skimmed” by digital pickpockets. This fear often stems from early contactless adoption, but the technology has moved on. Modern payment standards make it incredibly difficult for fraudsters to intercept usable data. While 2024 industry data suggests that physical card theft is still a threat, digital nfc interception is practically non-existent in real-world retail environments. To understand the full landscape of NFC security threats and solutions, we need to look at how data is shielded during every tap. Security isn’t just an add-on; it’s the foundation of a Pure payment environment.

The Power of Tokenisation

Tokenisation is your strongest shield against data breaches. When a customer taps their device, the system doesn’t transmit the actual 16-digit card number. Instead, it sends a “token,” which is a random string of numbers that only the bank can decode. If a hacker intercepted this token, it would be useless for any other transaction or merchant. Tokenisation ensures the merchant never actually “sees” or stores the customer’s real card details. By keeping sensitive data out of your Hub, you lower your liability and protect your business from the fallout of a potential data leak. It’s a transparent way to handle sensitive info without the risk.

Dynamic CVV and Encryption

Every tap creates a unique cryptographic signature that validates the transaction. Unlike a physical card where the CVV is static and printed on the back, mobile wallets use a dynamic version. This security code changes for every single tap. “Replay attacks,” where a fraudster tries to use intercepted data for a second time, are virtually impossible because the bank’s system rejects any code that has already been used. This entire process happens within the Secure Element (SE) chip. This hardware is physically isolated from the rest of the smartphone’s operating system, meaning even if a phone is infected with malware, the payment keys remain untouched.

Mobile NFC payments offer a distinct advantage over physical cards through biometric verification. A lost contactless card can be used by anyone until it’s cancelled. A smartphone requires FaceID, a fingerprint, or a passcode before the nfc chip activates. This simple step eliminates a massive portion of fraudulent activity at the point of sale. For your business, using modern hardware also simplifies your PCI DSS compliance. These devices are built to meet the latest security standards, ensuring your partnership with us is based on honesty and technical integrity. You get to focus on growth while the hardware handles the heavy lifting of data protection.

Implementing NFC: Choosing the Right Hardware for Your Shop

You probably already have the foundation for nfc payments sitting on your counter. Take a look at your current terminal. If you see the four curved waves symbol, you’re likely ready to accept contactless payments. However, hardware manufactured before 2020 often lacks the processing power to handle the complex encrypted handshakes required by the latest digital wallets. Upgrading your kit isn’t just a technical necessity; it’s a commitment to your customer’s time.

Countertop vs. Mobile NFC Terminals

Fixed countertop units are the reliable workhorses of the UK high street. They thrive in environments with high transaction volumes, like boutiques or local convenience stores. Because these units typically use wired Ethernet connections, they offer a level of stability that wireless units can’t always match. You won’t have to worry about a “searching for signal” message during a busy Saturday afternoon rush.

Portable and mobile units are essential for hospitality and service-based businesses. Data from UK Finance shows that contactless payments accounted for 93% of all card transactions in 2023. To capture this demand at the table or on the move, you need hardware with robust battery life. Prioritise devices that offer 4G or 5G failover. If your shop’s Wi-Fi stutters, the terminal switches to mobile data instantly, keeping your revenue flowing without a hitch.

Setting Up Your NFC Payment Zone

The physical placement of your terminal dictates the rhythm of your shop. Place the unit at a natural elbow height to ensure the “tap” feels intuitive for the customer. A cluttered counter leads to awkward retries and “failed taps.” Use clear visual indicators to show exactly where the nfc sensor is located on the device. This simple step reduces transaction times by several seconds per person, which adds up during peak hours.

- Keep the tap zone clear of metal objects or other electronic interference.

- Train staff to recognise when a thick phone case or a “wallet” style cover is blocking the signal.

- Ensure the terminal screen is visible to the customer for immediate “Approved” feedback.

Integration is where your hardware truly becomes a Hub for your business. When your terminal speaks directly to your EPOS system, inventory management becomes automatic. You won’t need to manually count stock or reconcile receipts at the end of a long shift. Every tap updates your records in real-time, providing a pure, transparent view of your daily performance. This synergy eliminates human error and protects your profit margins.

PurePay Hub: Transparent NFC Processing for UK SMEs

PurePay Hub operates on a simple principle: your hard-earned revenue belongs to you. We’ve built our “Pure” approach to eliminate the murky markups that often drain UK small businesses. When your customers tap to pay, you shouldn’t have to guess what the final cost will be. We offer competitive rates that reflect the actual cost of processing, with debit card charges starting from just 0.3% for nfc payments. This isn’t a teaser rate; it’s our commitment to fairness.

Cash flow is the lifeblood of any local shop or service provider. Waiting a week for your funds to clear is a relic of the past. We provide next-day funding, ensuring your nfc sales revenue reaches your bank account the very next business day. By centralising your payment data through our Hub, we give you the insights needed to track busy periods and manage stock more effectively. We don’t just process payments; we provide the clarity you need to grow.

Simplified Fee Structures

Many providers lure merchants in with a flat-rate model that seems simple but hides significant costs. These opaque structures often mean you’re overpaying for low-risk debit transactions. Our transaction-based model is different. We break down exactly where every penny goes. We organise your monthly statements so they’re easy to read at a glance, removing the stress of deciphering complex financial jargon.

- No hidden markups: You pay for the service you use, nothing more.

- Clear reporting: See your daily totals and fee breakdowns without the headache.

- Fairness for SMEs: We provide the same transparent pricing to a local café that we would to a larger retailer.

British merchants deserve a partner that respects their bottom line. We prioritise honesty because we know that trust is built through consistent, predictable costs. You’ll never find a surprise fee on a PurePay Hub statement.

Getting Started with PurePay Hub

We’ve streamlined our onboarding process to be as fast as a contactless tap. Moving from your initial enquiry to taking your first payment happens in record time. We know you’re busy running a business, so we’ve removed the bureaucratic hurdles that slow down traditional bank applications. Our team handles the heavy lifting so you can focus on your customers.

Our hardware range fits every business type. Whether you need a robust countertop terminal for a boutique in Manchester or a sleek mobile solution for a food stall in London, we’ve got you covered. Every device we provide is fully nfc-enabled and ready for the 2026 payment landscape. It’s time to move away from providers that hide behind fine print. Join the UK’s most transparent payment hub today and experience processing as it should be.

Future-Proof Your Business with Modern Payments

The shift toward a cashless society isn’t just a passing trend; it’s the operational standard for 2026. By mastering nfc technology, you ensure your shop stays competitive whilst providing the seamless security your customers now expect as standard. You’ve seen how the science of the tap reduces queues and how fully PCI compliant hardware protects your hard-earned revenue from modern threats. It’s time to strip away the complex fee structures and hidden markups that too often plague the UK merchant industry.

PurePay Hub offers a partnership built on honesty and clarity. We provide debit card rates starting from 0.3% and ensure you have next-day access to your funds to keep your cash flow healthy. You deserve a payment partner that values your business growth as much as you do. Our hardware is reliable and straightforward, keeping your shop safe without the typical corporate jargon or confusing contracts. We’re here to help you navigate the future of payments with total confidence and pure transparency.

Switch to PurePay Hub for transparent, low-rate NFC processing

Take control of your processing today and watch your business thrive in a digital-first economy.

Frequently Asked Questions

What is the current contactless payment limit in the UK for 2026?

The standard contactless limit for physical cards in the United Kingdom remains £100 throughout 2026. This limit was established by the Financial Conduct Authority in October 2021 to balance merchant convenience with fraud prevention. Whilst physical cards are capped at this amount, mobile wallet transactions via Apple Pay or Google Pay often have no fixed limit because they use secure biometric authentication like FaceID or fingerprint scanning.

Can I accept Apple Pay and Google Pay with a standard NFC card machine?

You can accept Apple Pay, Google Pay, and other digital wallets on any standard card machine equipped with nfc technology. These mobile wallets use the same radio frequency standards as physical contactless cards to transmit payment data securely. Your terminal doesn’t require special software updates for each phone brand; it simply needs an active NFC reader to process the encrypted token sent from the customer’s device.

Do I pay higher transaction fees for NFC or contactless payments?

You won’t pay higher transaction fees for NFC or contactless payments compared to traditional chip-and-pin transactions. At PurePay Hub, we ensure your costs remain transparent and transaction-based regardless of how the customer chooses to pay. Most UK acquirers treat all card-present transactions under the same fee structure, so you can offer your customers the speed of contactless without worrying about hidden markups or price hikes.

Is it possible for a customer to be charged twice if they tap their card twice?

It’s impossible for a customer to be charged twice for a single transaction if they accidentally tap their card or phone twice. NFC terminals are designed to process only one authorised transaction at a time and will automatically close the payment window once the first tap is successful. If a customer taps again, the machine will display an “Already Paid” or “Transaction Complete” message, protecting your business from duplicate entries.

What should I do if a customer’s NFC payment is declined but their chip-and-pin works?

If a contactless payment is declined but the chip-and-pin works, it’s usually due to a security check known as Strong Customer Authentication (SCA). UK regulations require banks to prompt for a PIN after a customer reaches a cumulative contactless spend of £300 or after five consecutive taps. Simply ask the customer to insert their card into the reader; this resets their contactless counter and allows the transaction to proceed safely.

Does my business need a specific type of internet connection for NFC terminals?

Your NFC terminal requires a stable internet connection but doesn’t need a specific high-speed fibre line to function correctly. A standard Wi-Fi connection with speeds of at least 2 Mbps or a reliable 4G mobile data signal is sufficient for processing payments. The data packets sent during an NFC transaction are extremely small, typically measuring less than 15 kilobytes, so reliability is more important than raw bandwidth.

How far away does a card need to be for the NFC terminal to pick it up?

A card or mobile device must be within 4 centimetres of the terminal for the NFC reader to pick up the signal. This short range is a deliberate security feature designed to prevent accidental payments from people walking past your counter. For the best results, we recommend customers tap their card directly against the screen or the contactless symbol, ensuring the transaction completes in under two seconds.

Can NFC technology be used for things other than payments in my shop?

NFC technology serves many purposes beyond taking payments, such as managing digital loyalty schemes or sharing shop information. You can use nfc tags to share your guest Wi-Fi password or to trigger digital coupons when a phone is tapped against a shelf display. In 2026, 45 percent of UK retailers are expected to use these tags for smart shelving, where customers tap a label to see detailed product origins.

Leave a Reply