In 2025, 67% of people in the UK used apple pay for point-of-sale transactions, proving that mobile wallets are now a standard expectation rather than a luxury. You have likely felt the frustration of watching a queue grow whilst a customer fumbles for a physical card or cash. It is a common pain point that leads to lost sales and unnecessary stress for your team. You deserve a payment partner that prioritises your efficiency over complex fee structures and opaque banking jargon.

Discover how accepting Apple Pay can streamline your checkout, enhance your security, and lower transaction friction for your UK business. We believe in providing a fair, transparent path to modernising your till without the usual industry headaches. This guide covers everything from the latest 2026 interchange fee regulations to how our portable card machines and EPOS systems integrate seamlessly with NFC technology. We will help you move from confusion to confidence, ensuring your processing costs remain predictable and your customers stay satisfied.

Key Takeaways

- Understand why UK consumers are rapidly moving away from physical cards and how this shift affects your checkout speed.

- Discover how tokenisation and biometrics in apple pay work together to shield your business from fraudulent chargebacks.

- Clear up the confusion around processing fees with a transparent breakdown of merchant service charges for mobile wallets.

- Learn how to quickly audit your card machine hardware to ensure you are ready for the latest NFC technology.

- Find out how to secure predictable processing rates and get your merchant services up and running in a matter of days.

What is Apple Pay for Businesses and Why Does it Matter?

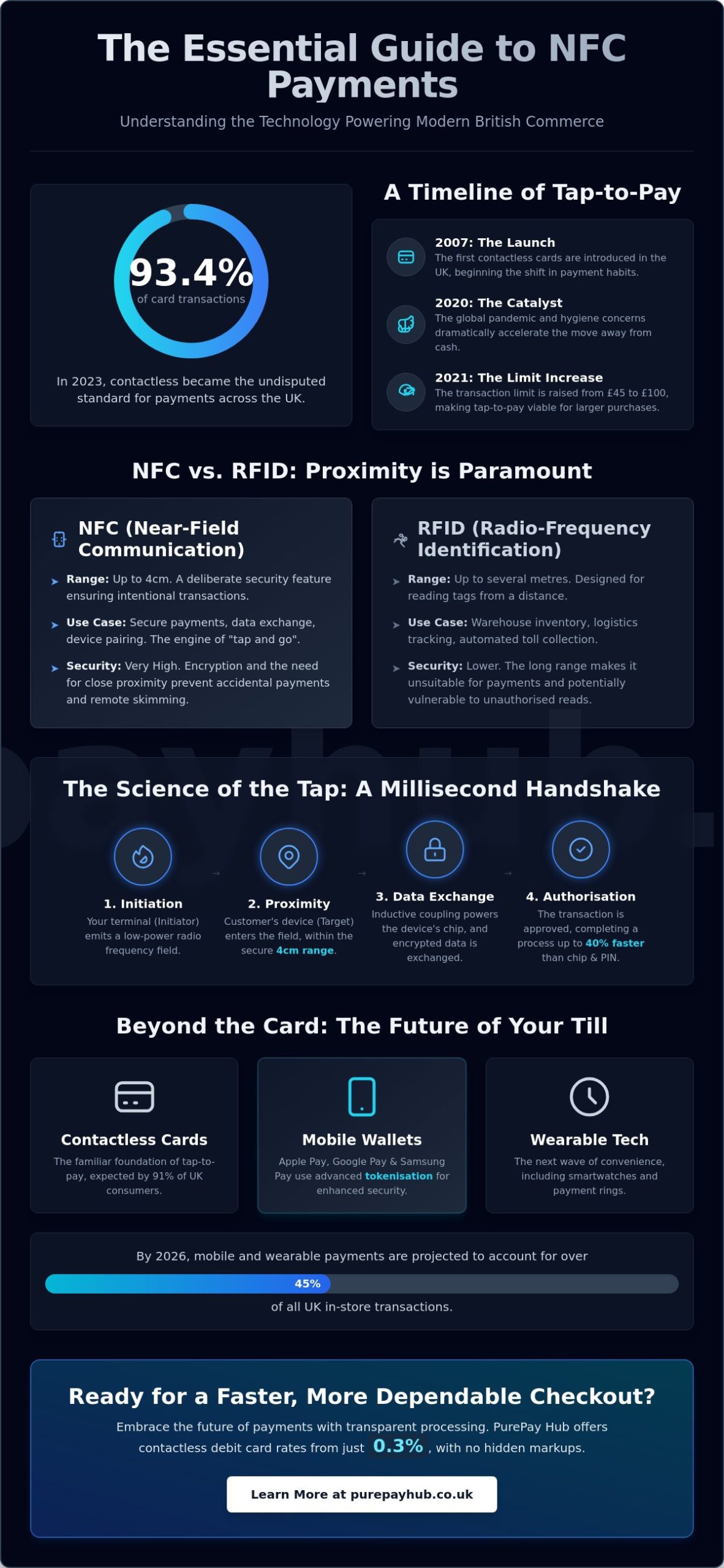

The way we pay has changed forever. For a modern merchant, understanding What is Apple Pay is the first step toward a more efficient till. It is a mobile payment and digital wallet service that allows customers to pay using an iPhone or Apple Watch via Near Field Communication (NFC) technology. Whilst consumers see a sleek app, you see a tool that reduces checkout friction. By 2026, the shift is undeniable. Over half of all UK contactless payments are now mobile-based, driven by a desire for speed and security.

Accepting apple pay requires more than just a bank account. You need an NFC-enabled terminal, such as a Portable Card Machine or a Countertop Card Machine, to bridge the gap between the customer’s device and your merchant account. This technology fits perfectly into the UK’s rapid move toward a cashless society. It is no longer about just ‘taking cards’; it’s about meeting your customers exactly where they are. We see this as a partnership between your business and the latest financial tech.

The Growth of Digital Wallets in the UK

Data from UK Finance shows that 57% of UK adults were registered for a mobile wallet in 2024. By 2025, adoption surged even further, with 67% of the population using the service for point-of-sale transactions. Regional businesses are moving away from cash-only models because digital wallets encourage spontaneous purchases. A customer who forgets their physical wallet can still buy from you if they have their phone. This flexibility builds immediate loyalty and ensures you never lose a sale to a ‘cash only’ sign. It makes your business feel modern and accessible to every demographic.

Core Terminology for Merchants

NFC stands for Near Field Communication. It is a short-range wireless technology that allows two devices to talk when they are close together. Your physical card reader or EPOS System detects the encrypted signal from an iPhone and processes it instantly. This differs from a Virtual Terminal, which is used for keyed-in remote payments. Whilst ‘Contactless’ and ‘Apple Pay’ seem the same at the till, the backend involves different layers of security. This process, known as tokenisation, ensures that sensitive card data is never actually shared with your hardware, protecting both you and your customer.

How Apple Pay Works: Security and Tokenisation Explained

Security shouldn’t be a headache for a busy business owner. In an industry often viewed with skepticism, apple pay offers a level of protection that traditional magnetic stripe or even Chip and Pin methods simply cannot match. The foundation of this system is tokenisation. This process replaces sensitive card data with a unique, encrypted identifier called a “token”. When a customer taps their iPhone against your Portable Card Machine, your hardware never actually “sees” or stores their 16-digit card number. This ensures that even if your local system were compromised, there is no usable financial data for a criminal to steal.

Biometric authentication adds another layer of calm advocacy for your business. By requiring Face ID, Touch ID, or a passcode, the system confirms the user’s identity before the transaction is even broadcast. This significantly reduces the risk of fraudulent chargebacks. For you, the merchant, this often results in a liability shift. Because the authentication is handled securely on the device, the risk for “card-present” fraud typically moves away from your business and toward the card-issuing bank. You can find more detail on these technical safeguards in this overview of Apple Pay security and privacy.

The Process of a Transaction

The journey from a tap to your bank account is remarkably swift. First, the customer’s device sends the digital token to your Payment Gateway. The gateway then passes this token to the card network for verification. Because there is no physical card to insert or mechanical chip to read, these transactions are typically faster than traditional methods. This speed reduces queues and keeps your customers happy. Choosing the right NFC-enabled terminal is the first step toward securing your till and speeding up your throughput.

PCI Compliance and Data Protection

Managing data protection is a heavy burden for regional merchants. However, using mobile wallets simplifies your PCI DSS compliance requirements. Since you aren’t storing actual credit card numbers on your local servers or EPOS Systems, the scope of your security audits is greatly reduced. This isn’t just a technical benefit; it’s a brand promise. You can confidently reassure your customers that their data is safe, positioning yourself as a modern, dependable business partner in the local community. It is a no-nonsense approach to safety that lets you focus on growth rather than red tape.

Accepting Apple Pay: Merchant Costs and Business Benefits

A common misconception amongst regional business owners is that modern mobile wallets carry hidden premiums. This simply isn’t true. Accepting apple pay typically costs exactly the same as a standard contactless card transaction. You pay your agreed Merchant Service Charge (MSC) to your processor, and that is it. Apple does not charge merchants a penny extra for the privilege of using their platform. By removing this barrier, you can focus on what really matters: moving customers through your shop faster and more securely.

Speed is a silent revenue generator. When you reduce queue times during peak hours, you capture sales that might otherwise be lost to frustration. Features like “Express Mode” allow for even faster transactions in high-volume retail environments, as customers don’t even need to wake their device. This efficiency doesn’t just improve the atmosphere of your shop; it directly boosts your throughput at the till. It is a no-nonsense way to modernise your service without increasing your overheads.

Fee Structures for UK Small Businesses

Understanding your costs requires looking at two main components: interchange fees and processor markups. In the UK, domestic interchange fees are capped at 0.2% for debit cards and 0.3% for credit cards. Transparent, fixed-rate pricing models often provide the best value for apple pay volume because they offer predictability. Contrast this with the hidden costs of cash. Between bank deposit fees, insurance premiums, and the risk of theft, digital payments are often the more cost-effective choice for a disciplined business. We prioritise clarity, ensuring you know exactly what leaves your account every month.

The Hidden Value of Digital Payments

Digital payments often lead to higher average transaction values. When customers aren’t limited by the physical cash in their pockets, they feel more comfortable making spontaneous additions to their baskets. Beyond the immediate sale, these systems integrate seamlessly with digital loyalty programmes and e-receipts. This allows you to build a direct relationship with your local community. Reconciliation also becomes a breeze. Instead of counting coins at the end of a long shift, your EPOS Systems and Portable Card Machines provide digital-first reporting that organises your finances in seconds.

Setting Up Apple Pay on Your Card Machine or EPOS

Transitioning to mobile payments is simpler than traditional banks suggest. It starts with a clear, no-nonsense audit of your current setup. You don’t need a degree in computer science to get your business ready for 2026. Follow these five steps to ensure your till is fully optimised for apple pay.

- Audit your hardware: Look for the universal contactless symbol on your current terminal. If your machine was manufactured before the mid-2010s, it likely lacks the necessary NFC chip.

- Enable acceptance: Contact your merchant service provider. They must toggle mobile wallet acceptance on your account backend to ensure tokens are processed correctly.

- Update your EPOS software: Running the latest version of your EPOS Systems software prevents integration glitches and ensures security patches are current.

- Train your team: Your staff should know that customers don’t need to ‘wake’ their device to pay. Simple cues make the process feel seamless for everyone involved.

- Display signage: Use official decals to show you are modernised. Letting customers know you accept their favourite payment method reduces hesitation at the point of sale.

Hardware Requirements

Your choice of hardware should mirror your business layout. A Countertop Card Machine is a stabilising force for fixed retail points. However, if you run a restaurant or a busy showroom, a Portable Card Machine allows you to take the till to the customer. This flexibility is essential for maintaining high throughput. Regardless of the model, a stable Wi-Fi or 4G connection is non-negotiable. Mobile transactions rely on real-time token verification; a dropped signal means a lost sale. We also understand the importance of cash flow, which is why we prioritise next-day funding for businesses processing high volumes of mobile payments.

Common Integration Troubleshooting

Even the best systems encounter occasional hiccups. If a customer’s apple pay is declined whilst their physical card works, it is usually a bank-side security check rather than a hardware fault. Ask them to try again or use their physical card. Handling refunds is also slightly different. You will need the last four digits of their Device Account Number, found in their Apple Wallet, rather than their physical card number. Finally, remember that Apple Pay often bypasses the standard £100 contactless limit through biometric authentication. This allows for larger transactions without the need for a PIN. If you are ready to upgrade your hardware, explore our range of NFC-enabled card machines today.

Why PurePay Hub is the Ideal Partner for Apple Pay Integration

Choosing a payment partner is about more than just hardware. It is about finding a fair ally that values your time and your bottom line. We provide a refreshingly transparent fee structure with rates starting from 0.3% for debit and 0.5% for credit. This includes all apple pay transactions, ensuring you never face hidden markups or “premium wallet” surcharges. Our goal is to provide a stabilising force for your finances, allowing you to plan your growth with total certainty.

Efficiency is at the heart of our no-nonsense onboarding process. We understand that regional merchants can’t afford to wait weeks for new equipment. You can have your NFC-enabled terminal delivered and ready for the till in days. Once you are up and running, our next-day funding ensures your cash flow remains healthy as your digital volume grows. If you ever need help, our UK-based support team is just a phone call away. They understand the local business landscape and speak your language, not corporate jargon.

Growth Beyond Payments

Your transaction data is more than just a record of sales. It is a roadmap for your future development. By building a consistent history of apple pay and card transactions, your business may qualify for a Business Cash Advance. This flexible funding option is based on your future sales, providing the capital you need to renovate, restock, or expand. Our reporting tools also allow you to track mobile versus physical card trends, giving you the insights needed to future-proof your business against the next wave of digital payment innovation.

Take the Next Step with PurePay Hub

The “PurePay Promise” is simple: clarity, fairness, and direct partnership. We aren’t a distant financial institution; we are a supportive ally to the UK’s local merchant community. Whether you need a free rate review to see how much you could save or a hardware upgrade to a modern Portable Card Machine, we are here to help. Modernising your checkout shouldn’t be a struggle. It should be the catalyst that takes your business to the next level. Get your Apple Pay-ready card machine from PurePay Hub today.

Future-Proof Your Business with Confident Payment Solutions

The transition toward a digital-first economy represents a significant opportunity to strengthen your regional business. By embracing apple pay, you secure your transactions through advanced tokenisation whilst providing the rapid checkout experience your customers now expect. You don’t have to settle for the opaque fee structures or the frustratingly slow settlement times often found with traditional banks. Efficiency and transparency are within your reach when you choose a partner that prioritises your growth.

Modernising your till should be a straightforward step toward long-term development. We act as your reliable local expert, ensuring your move to mobile payments is both smooth and cost-effective. You can focus on serving your community whilst we manage the technicalities of your financial processing with honesty and integrity. It is time to replace confusion with informed confidence and a stable financial foundation.

Switch to PurePay Hub for transparent Apple Pay rates and next-day funding. Benefit from debit rates starting at 0.3%, next-day funding as standard, and a total absence of hidden monthly markups. We are ready to help you stabilise your finances and build a more resilient business today.

Frequently Asked Questions

Do I need a special card machine to accept Apple Pay?

You need a terminal equipped with Near Field Communication (NFC) technology. Most modern Countertop Card Machines and Portable Card Machines include this as standard. If your current hardware displays the universal contactless symbol, it is already capable of communicating with an iPhone or Apple Watch. If you are using an older device, upgrading to a modern NFC-enabled terminal is a quick and straightforward process that ensures you don’t miss out on mobile sales.

Is Apple Pay more expensive for merchants than standard card payments?

No, it is not more expensive. You simply pay the standard Merchant Service Charge agreed with your processor for a contactless transaction. Apple does not charge merchants any additional fees for the privilege of using their platform. This makes apple pay a cost-effective way to speed up your checkout without increasing your overheads or dealing with the hidden markups often found in traditional banking contracts.

What is the transaction limit for Apple Pay in the UK for 2026?

Whilst the standard UK contactless limit for physical cards remains at £100, mobile wallets operate differently. Because the customer authenticates the payment using Face ID or Touch ID, they can often complete transactions well above this limit. This is known as Consumer Device Cardholder Verification Method (CDCVM). It allows your business to accept larger payments securely without the customer needing to remember their physical card or PIN.

How do I process a refund for a customer who paid with Apple Pay?

Processing a refund is simple but requires the customer’s Device Account Number rather than their physical card number. They can find these last four digits in their Apple Wallet under the card’s information. You then enter this number into your card machine or EPOS System to match the original transaction token. This ensures the funds are returned safely to the correct account whilst maintaining the security of the customer’s actual card details.

Does Apple Pay work without an internet connection on the customer’s phone?

Yes, the customer’s device does not require an active internet connection to complete a purchase. The communication happens via short-range radio waves between the phone and your terminal. However, your card reader or Online Payment Gateway must have a stable connection to the internet to authorise the transaction with the bank. This ensures that the digital token is verified and the funds are secured in real-time.

Are Apple Pay transactions secure for my business?

Mobile payments are significantly more secure than traditional card methods. Tokenisation ensures that sensitive card data is never shared with your business hardware or stored on your servers. Additionally, biometric authentication nearly eliminates the risk of fraudulent transactions from lost or stolen devices. This security architecture protects your business from the stress of chargebacks and simplifies your overall PCI compliance requirements.

How long does it take for Apple Pay funds to reach my bank account?

The time it takes for funds to reach your account depends entirely on your merchant service provider. Many traditional banks still take three to five working days to settle funds. We understand that cash flow is the lifeblood of a regional business, which is why we provide next-day funding as standard. This ensures that your apple pay revenue is available for you to use almost immediately.

Can I accept Apple Pay on my website as well as in-store?

Absolutely. You can accept mobile payments online by integrating an Online Payment Gateway into your website checkout. This provides a ‘one-tap’ purchase experience that reduces cart abandonment. For businesses without a full website, Payment Links offer a no-nonsense way to accept these payments via email or SMS. Both methods use the same secure tokenisation technology to protect your business and your customers.