What if your most powerful marketing tool isn’t a glossy advert or a costly social media campaign? Most regional business owners are exhausted by the relentless cycle of ad fatigue and diminishing returns. You’ve likely felt the pressure to constantly create content whilst your real work sits on the back burner. This disconnect between chasing new leads and keeping current ones happy is often caused by 2. The “Invisible Marketing” Gap. It’s the missed opportunity to let your operations do the selling for you.

We believe that business growth should be simple and transparent. You don’t need a massive marketing budget to stay relevant; you need a system that works in the background. This guide explores how background automation and frictionless payments can build brand loyalty without constant manual effort. We will look at how tools like EPOS systems and virtual terminals create a professional, reliable image that earns trust. You’ll discover how to reclaim your time and build a brand that sells itself during every checkout.

Key Takeaways

- Understand how to bridge 2. The “Invisible Marketing” Gap by aligning your active advertising with a seamless, passive customer experience.

- Learn why “cognitive fluency” drives brand loyalty by making every interaction feel effortless for your customers.

- Discover why your card machine or EPOS system acts as a vital brand ambassador that can reduce buyer’s remorse instantly.

- Identify the specific friction points in your current customer journey where manual marketing can be replaced by background automation.

- Explore how PurePay Hub supports SME growth through transparent rates and reliable, quiet payment technology.

What is the Invisible Marketing Gap and why does it matter?

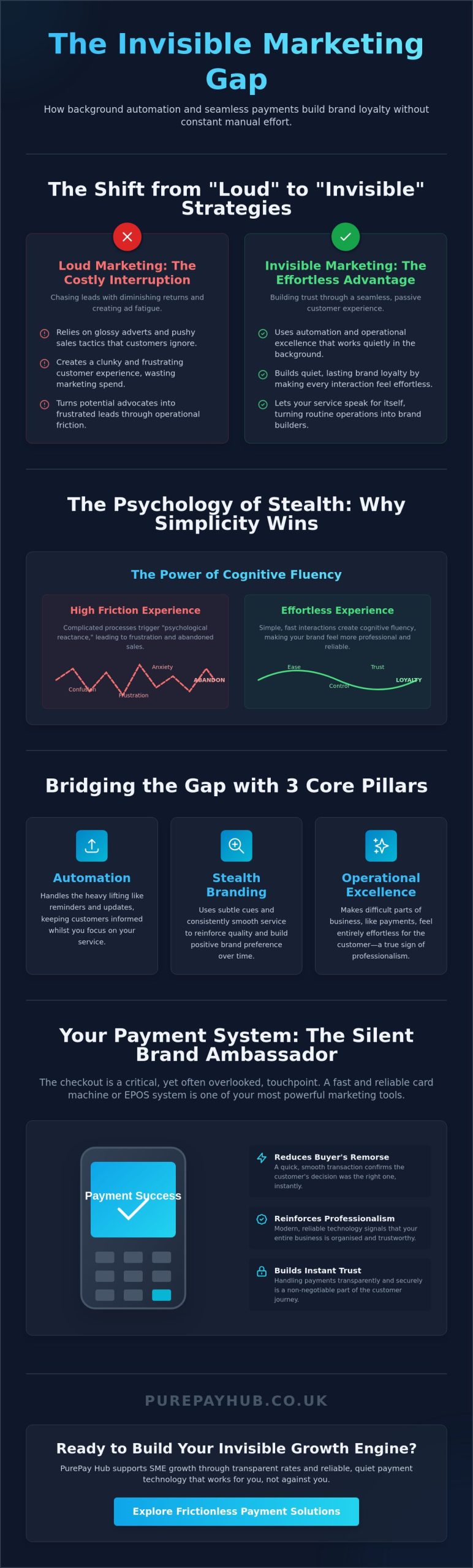

Traditional advertising is louder than ever, yet consumers have never been better at tuning it out. Ad fatigue isn’t just a buzzword; it’s a measurable decline in how people respond to flashy banners and pushy sales tactics. This disconnect creates a specific problem for regional businesses. You spend money to get people through the door, but if the actual experience feels clunky, that investment is wasted. We call this 2. The “Invisible Marketing” Gap. It represents the distance between your active advertising and the passive customer experience you provide every day.

In 2026, brand loyalty is built on trust and ease rather than volume. People don’t want to be sold to; they want their problems solved without fuss. This shift relies on three essential pillars: automation, stealth branding, and operational excellence. Automation handles the heavy lifting whilst you focus on the customer. Stealth branding uses subtle cues to reinforce your quality. Operational excellence makes the difficult parts of business, like payments, feel entirely effortless. When these pillars work together, they build a quiet brand loyalty that lasts longer than any social media campaign.

The evolution from “Loud” to “Invisible” strategies

Consumer behaviour has moved away from the era of the flashy billboard. Today, customers favour frictionless interactions that respect their time. This is where the “mere exposure effect” comes into play. By providing a consistently smooth service, you build a positive brand preference in the customer’s mind without them even realising it. Whilst large corporations often feel cold and distant, SMEs can use invisible marketing to highlight their local expertise and reliability. It’s about being dependable, not just visible. You win by being the easiest choice in your community.

Identifying the gaps in your current strategy

Take a moment to audit your customer touchpoints. Every time a customer has to wait too long or deal with a confusing process, you lose a bit of their trust. This friction is expensive. It negates your active marketing spend by turning a potential advocate into a frustrated lead. 2. The “Invisible Marketing” Gap is the missed opportunity to turn routine operations into brand builders. If your card machine is slow or your booking system is complex, you’re widening that gap. Closing it starts with making your backend operations your most effective sales tool. True growth happens when your service speaks for itself.

The Psychology of Stealth: Why background efforts win

Why do some brands feel like a natural part of our lives whilst others feel like a constant interruption? The answer lies in the psychology of stealth. When a business operates smoothly in the background, it respects the customer’s time and mental energy. This is the most effective way to bridge 2. The “Invisible Marketing” Gap. Instead of bombarding people with messages, you focus on the quality of the interaction itself. This approach wins because it aligns with how our brains actually work. You don’t need a loud voice when your actions are consistent and reliable.

Cognitive fluency is the ease with which we process information. When a process is simple and fast, we perceive it as more truthful and reliable. A fast payment gateway or a responsive countertop card machine isn’t just a utility. It’s a psychological trigger that says, “This business is professional.” Complicated systems do the opposite. They create friction that drives customers away, regardless of how good your marketing campaign was. By making the path of least resistance your standard operating procedure, you secure your status as a favourite brand in the customer’s mind.

Cognitive Fluency and the path of least resistance

The human brain is wired to seek simplicity. Complicated systems, like a multi-step checkout or a glitchy card machine, trigger “psychological reactance.” This is the feeling of being restricted or frustrated, which often leads to customers abandoning their purchase. A smooth, fast checkout does more than just complete a sale; it reinforces your authority. When the process is familiar and fast, customers feel in control. This sense of ease is what brings people back time and again without you needing to spend a penny on new adverts.

Building trust through consistent background presence

Trust isn’t always built through large gestures. Often, trust is built in the quiet moments between transactions. Automated reminders or status updates keep the customer informed without being intrusive. These background efforts reduce anxiety and show you’re organised. Payments and checkouts are often overlooked yet crucial touchpoints in this journey. If these moments are handled with speed and transparency, your brand authority grows naturally. Using “invisible” data to personalise these interactions makes the customer feel seen, rather than just managed.

Operational speed is a direct signal of competence. If you can process a transaction or answer a query instantly, you project an image of authority. This leads to organic advocacy. Customers who have a frictionless experience are more likely to recommend you to others. They become your marketing team without you ever having to pay for a testimonial. If you want to turn your operations into a silent growth engine, consider how modern EPOS systems can help you automate these crucial background tasks whilst you focus on serving your community.

Bridging the Gap: The payment experience as marketing

Whilst many business owners focus their energy on social media campaigns or local flyers, they often overlook the most critical touchpoint in the building. The card machine is the final brand ambassador your customer interacts with. If that interaction is slow or awkward, it leaves a lasting negative impression. A seamless transaction is the most direct way to close 2. The “Invisible Marketing” Gap. It ensures that the positive feeling of the purchase isn’t ruined by a frustrating checkout process. You’ve worked hard to win the sale; don’t let a clunky terminal lose the customer’s future loyalty.

Modern payment technology like NFC (Near Field Communication) and integrated EPOS systems do more than just process money. They reduce “buyer’s remorse” by making the transaction happen in the blink of an eye. The faster the payment, the less time there is for doubt to creep in. This isn’t about tricking the customer. It’s about respecting their time and maintaining the momentum of a positive experience. Professionalism is also reinforced through digital Payment Links and branded receipts. These tools keep your name in front of the customer long after they’ve left the premises, reinforcing your brand identity without an active sales pitch.

The Countertop Card Machine: More than just a terminal

A sleek, fast Countertop Card Machine signals that your business is legitimate and modern. It tells the customer that you value their convenience. By accepting all payment types, including Apple Pay and Google Pay, you show brand inclusivity. You aren’t just taking their money; you’re providing a service that fits their lifestyle. You can also use payment data to identify your most loyal customers. This allows you to offer “invisible” rewards, such as a surprise discount on their next visit, without needing a complex loyalty card scheme. It’s a simple way to make people feel valued.

Integrated EPOS systems: The heart of invisible operations

For hospitality and retail businesses, efficiency is everything. Integrated EPOS systems ensure that your front-of-house “talks” directly to the kitchen or stockroom. This reduces wait times and prevents errors that could damage your reputation. When your systems are integrated, your staff don’t have to spend their time on manual data entry or running back and forth to check stock. They can stay focused on the customer. This operational excellence is a form of marketing that builds trust through consistent, high-quality service. It turns a routine transaction into a professional experience that customers will want to repeat. You win by being the business that just works.

Implementing Invisible Strategies in your SME

Closing the gap between what you promise in your adverts and what you deliver at the till requires a structured plan. You can’t fix every operational hurdle at once. Instead, you must systematically replace manual, “loud” efforts with quiet, automated systems. This is the most practical way to bridge 2. The “Invisible Marketing” Gap. It turns your daily operations into a self-sustaining growth engine that doesn’t rely on your constant manual intervention. You win by being the business that is simply easier to deal with.

The first step is to map your customer journey from discovery to post-purchase. Identify the friction points where active effort is currently needed. Are you manually chasing payments? Are customers waiting for an old terminal to dial out? These moments are where “invisible” systems should take over. Upgrading your hardware to support modern expectations is essential. Whether it’s a portable card machine for tableside service or a mobile card machine for trade work, speed is your best marketing tool. Finally, you must monitor “invisible” metrics like transaction speed and repeat visit rates. These figures provide a clearer picture of your brand health than any social media metric.

Automating the post-purchase loop

The relationship shouldn’t end the moment the receipt is printed. You can set up “invisible” review requests that trigger automatically after a successful card payment. This builds your online reputation whilst you focus on the next customer. For service-based businesses, using a virtual terminal ensures that your invoicing is professional and arrives on time. You can also use payment links in follow-up emails for subtle upselling. It’s a low-pressure way to encourage repeat business without the customer feeling pestered. It keeps your brand in their mind through utility rather than interruption.

Maintaining PCI compliance as a trust signal

Security is the ultimate form of invisible marketing. When your payment systems work perfectly, no one notices the complex encryption happening in the background. This builds a vital foundation of safety. Customers feel confident returning to a business where their financial data is handled with integrity. PurePay Hub manages the complexity of PCI compliance for you, which removes a significant administrative burden from your shoulders. You can find more detail on staying protected in The Merchant’s Guide to PCI Compliance. When security is seamless, trust becomes a permanent part of your brand identity.

If you’re ready to stop chasing leads and start building a brand that sells itself, view our range of smart card machines to find the right fit for your business.

PurePay Hub: Your partner in invisible growth

Every successful business needs a quiet engine running in the background. At PurePay Hub, we position ourselves as that engine for UK SMEs. We understand that your focus should remain on your customers and your craft, not on the technicalities of financial processing. By providing reliable, “no-nonsense” technology, we help you bridge 2. The “Invisible Marketing” Gap. You don’t need a loud payment provider; you need a fair partner that ensures every transaction reinforces your brand’s professionalism. We act as a stabilizing force for your finances so you can grow with confidence.

Our approach is built on the principles of honesty and integrity. We offer competitive rates, such as 0.3% for debit transactions, with absolutely no hidden markups. This transparency allows you to maintain a healthy cash flow without the stress of unexpected costs. Next-day funding ensures your capital is available when you need it, supporting the invisible health of your daily operations. Whether you utilize our integrated EPOS systems or our portable card machines, you gain the flexibility to serve your community wherever they are. We provide the tools; you provide the excellence.

Transparent fees for a clearer business focus

Clarity is the foundation of trust. We break down our rates to ensure you know exactly what you are paying for every sale. Our promise is to provide the lowest card machine rates for small business UK merchants whilst maintaining a high standard of service. By eliminating the murky fee structures used by traditional competitors, we allow you to reinvest your savings back into your business. You deserve a partnership that is untainted by corporate jargon or complex contracts. Our goal is to help you stay focused on what matters most: your growth.

Support that works in the background

Our commitment to your success goes beyond just processing payments. We offer quick onboarding and dependable technical support to ensure your systems never skip a beat. If you need capital for a new project, a business cash advance can provide the necessary funds based on your future card sales. This is support that works with you, not against you. We handle the complexities of the backend so your brand remains a symbol of reliability in the eyes of your customers. Trust is built through consistency, and we are here to provide that steady presence for your business.

Ready to close the gap? Explore our card machine solutions today.

Transform Your Operations into Your Greatest Advocate

Growing a business doesn’t require a louder voice; it requires a smoother system. By focusing on the customer experience at the point of sale, you bridge 2. The “Invisible Marketing” Gap. This strategy turns every routine transaction into a quiet endorsement of your brand’s quality and reliability. You’ve seen how frictionless payments and automated follow-ups build long-term loyalty without the constant drain of expensive advertising campaigns. Operational excellence is the most honest way to prove your value to your local community.

It’s time to let your backend systems do the heavy lifting for you. We provide the tools to make your business growth feel effortless and professional. With debit rates starting from 0.3% and next-day access to funds, your cash flow stays as healthy as your reputation. Our next-generation integrated EPOS systems ensure your team can focus on serving people rather than managing paperwork. Switch to PurePay Hub for transparent, high-speed card processing and start building a brand that speaks for itself. You have the vision; we provide the steady technology to support it.

Frequently Asked Questions

What exactly is invisible marketing for a small business?

Invisible marketing is the practice of using operational excellence and seamless customer experiences to build brand loyalty without overt advertising. For a small business, this means making every interaction so smooth that the customer feels valued and respected. It addresses 2. The “Invisible Marketing” Gap by turning necessary tasks, like processing a payment, into positive touchpoints. This builds trust quietly and effectively through consistent reliability.

How do card machines contribute to my marketing strategy?

A card machine is the final touchpoint in a physical store and acts as a vital brand ambassador. Using a fast, modern Countertop Card Machine signals that your business is professional and values the customer’s time. It reduces friction at the most sensitive part of the journey. Accepting modern methods like Apple Pay shows you are inclusive and technologically capable. This leaves a lasting positive impression that encourages repeat visits.

Can automation really replace a marketing department for an SME?

Automation doesn’t replace the need for a strategy, but it handles the repetitive tasks that drain your time. Background systems can manage review requests, digital receipts, and loyalty rewards automatically. This allows a small business owner to maintain a consistent brand presence without hiring a full team. It ensures that your background efforts are working 24/7 whilst you focus on your core service and community.

Is invisible marketing ethical for UK businesses?

Yes, because it is based on improving the customer experience rather than using trickery. Invisible marketing is about removing hurdles and becoming more efficient for the benefit of the buyer. It relies on transparency and reliability to win trust over time. By providing a better service through smoother operations, you are being a fair partner to your customers. It’s a principled approach that respects the consumer’s desire for simplicity.

How much do integrated EPOS systems cost to run?

Costs for integrated EPOS systems vary depending on your business size and specific requirements. You should check with providers for tailored quotes that suit your particular industry and volume. These systems often save money in the long run by reducing manual errors and improving stock management. We prioritise clarity in our fee structures to ensure you aren’t surprised by hidden costs. We focus on providing value through operational efficiency.

How can I measure the ROI of background marketing efforts?

You can measure the return on investment by tracking specific operational metrics rather than just clicks. Look at your repeat customer rate, average transaction speed, and the number of organic reviews you receive. These data points indicate how well your background systems are closing 2. The “Invisible Marketing” Gap. If customers return more frequently and leave positive feedback without being prompted, your strategy is working effectively to build long-term value.

What is the difference between stealth marketing and invisible marketing?

Stealth marketing often involves hidden advertisements or paid influencers who don’t disclose their relationship with a brand. Invisible marketing is different because it focuses on the quality of the actual service provided. It isn’t about hiding a sales pitch; it’s about making the service so good that the pitch isn’t necessary. One relies on secrecy to influence, whilst the other relies on operational excellence and customer respect to earn loyalty.

How does next-day funding help my business growth?

Next-day funding keeps your cash flow healthy and predictable. It ensures that the money you’ve earned is available almost immediately to pay suppliers or invest in new stock. This stability allows you to respond quickly to local opportunities without waiting for traditional banking cycles to complete. It’s a quiet form of support that keeps your business moving forward without financial bottlenecks. Reliable cash flow is the foundation of any growing brand.