Retailers who switch to unified commerce platforms see an average revenue increase of 9.5 per cent, according to data from ConnectPOS. If your current setup feels more like a weight than a wing, you aren’t alone. Many business owners spend hours on manual end-of-day reconciliation whilst high transaction fees eat into their margins. Building a solid business case for a new POS system is the first step toward stopping this drain on your resources. It’s time to stop viewing your payment setup as a simple cost and start seeing it as a strategic engine for growth.

We understand that upgrading feels like a daunting task, especially with the April 2027 expiry of older PCI PTS POI v5 devices fast approaching. You want clarity and fairness, not more corporate jargon. This guide will help you justify an upgrade by quantifying real efficiency gains and identifying hidden revenue streams. We will show you how to lower merchant service charges, automate your accounting integration, and speed up customer throughput. By the end of this article, you’ll have a clear, data-driven plan to modernise your business and reclaim your time.

Key Takeaways

- Identify the “friction tax” of slow processing and how manual reconciliation errors lead to avoidable revenue leakage.

- Learn how to draft a persuasive business case for a new POS system by focusing on efficiency, security, and long-term growth.

- Understand the impact of integrated payments on customer throughput and how automated accounting saves hours of administrative work.

- Quantify the direct financial benefits of switching, from reduced transaction fees to unlocking hidden revenue streams.

- Discover the advantage of transparent, no-nonsense fee structures that prioritise your business’s bottom line over hidden markups.

The Hidden Cost of Inaction: Why Your Current System is Costing You Money

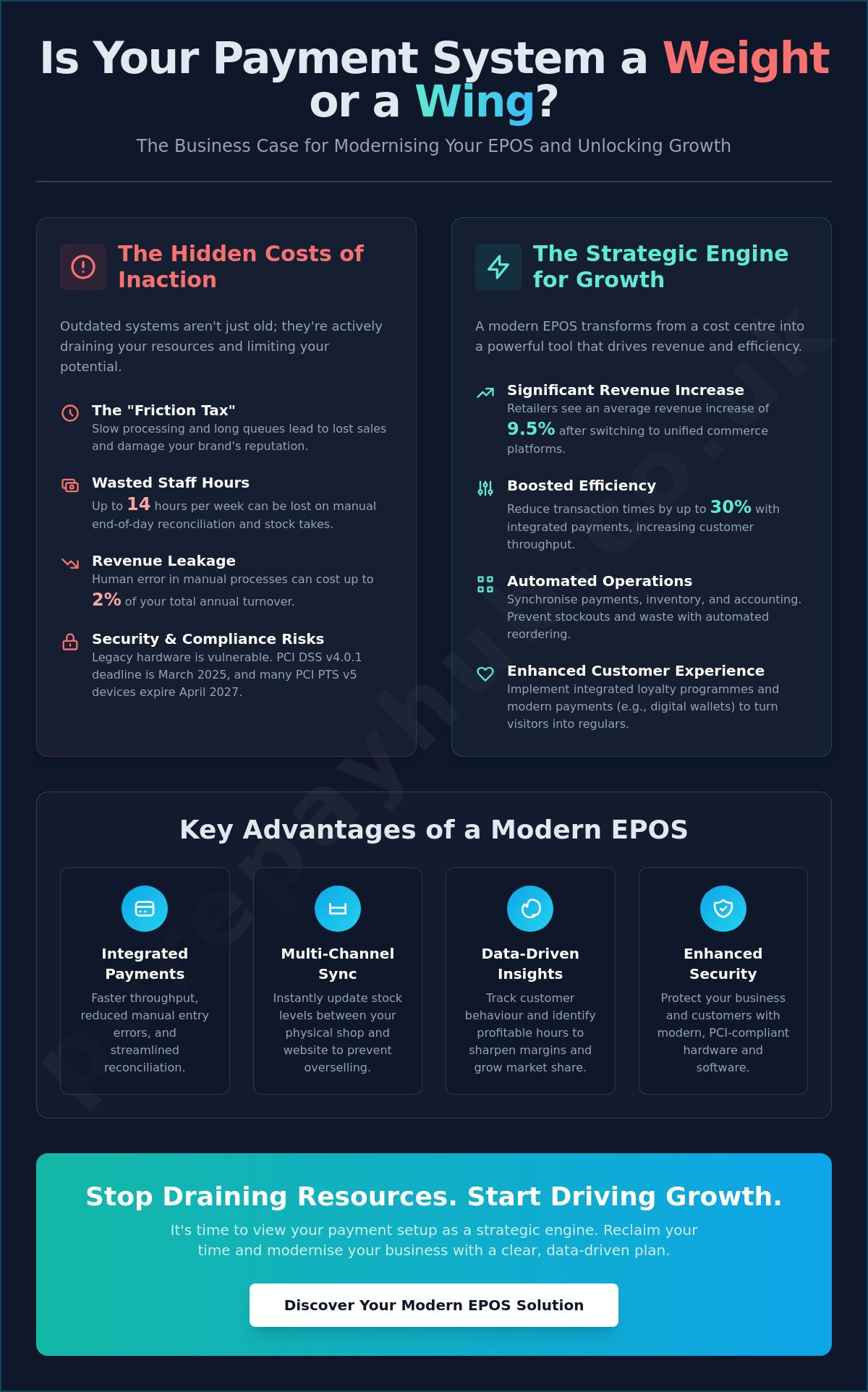

Staying with an outdated payment setup isn’t the safe or frugal choice. It’s often the most expensive path a merchant can take. Many regional business owners view a hardware upgrade as a pure expense, but this perspective ignores the daily financial leak caused by legacy tech. When you begin building a business case for new POS system adoption, you must first account for the “friction tax.” This is the invisible cost of slow processing speeds. If a customer sees a long queue caused by a sluggish card reader, they often walk away. That isn’t just a lost sale; it’s a permanent dent in your brand’s reputation.

To understand the full scope of the problem, we must look at what a POS system is in a modern context. It is no longer just a digital till; it’s the central engine of your business operations. Relying on older setups means you’re missing out on vital, real-time data. Without these insights, you cannot track customer behaviour or identify your most profitable trading hours. You are effectively flying blind whilst your competitors use data to sharpen their margins and steal your market share.

Quantifying Manual Labour and Human Error

Manual stock takes and end-of-day reports are massive drains on your resources. If your staff spend two hours every evening reconciling paper receipts and spreadsheets, that equates to fourteen hours of wages wasted every single week. Human error is inevitable in these manual processes, leading to “ghost inventory” where your records show items that aren’t actually on the shelf. This leads to missed sales opportunities and frustrated buyers. Industry data suggests that the cost of manual reconciliation often accounts for as much as 2 per cent of a merchant’s total annual turnover.

The Risk of Legacy Hardware Failure

System crashes during peak Saturday trade are a disaster for your brand. Patching old software is a temporary fix that often costs more in technician hours than a full upgrade. It also leaves your business vulnerable to security breaches. With PCI DSS v4.0.1 requirements becoming mandatory as of March 31, 2025, and many PCI PTS POI v5 devices set to expire on April 30, 2027, staying put is a significant regulatory risk. Legacy terminals also lack support for modern payment methods like digital wallets, which alienates a growing demographic of shoppers who no longer carry physical cards.

Strategic Advantages: How Modern EPOS Systems Drive Business Growth

A modern EPOS is far more than a digital cash drawer. It acts as a centralised hub that synchronises your payments, inventory, and staff management into one cohesive unit. When you develop a business case for new POS system investment, you’re looking at a shift from reactive management to proactive growth. Integrated payments are a core part of this transition. By removing the need for manual entry on a card terminal, businesses can reduce transaction times by up to 30 per cent. This speed doesn’t just please customers; it directly impacts your bottom line by increasing the volume of sales you can handle during your busiest hours.

For retailers and hospitality venues, multi-channel synchronisation is no longer optional. It ensures that a sale made on your website instantly updates the stock levels in your physical shop. This prevents the embarrassment of overselling and allows for more aggressive, accurate promotion strategies based on real-time data. If you’re ready to see how these efficiencies look in practice, exploring modern EPOS Systems is a logical next step for your growth strategy.

Inventory Mastery and Waste Reduction

Automated reordering is a game-changer for maintaining healthy cash flow. It prevents the twin traps of stockouts and overstocking by triggering orders only when needed. In the hospitality sector, ingredient-level tracking is essential to reduce food waste and protect margins. The many benefits of a new POS become clear when you can instantly identify your most and least profitable lines. This allows you to cut dead stock and double down on the products your customers actually want.

Enhancing Customer Experience and Loyalty

Integrated loyalty programmes turn one-off visitors into regulars. By capturing transaction data at the point of sale, you can create personalised marketing campaigns that resonate with your local community. Mobile POS and “pay at table” features also significantly reduce queues, allowing your staff to spend more time on service and less time tethered to a fixed counter. This improved experience is a key pillar in any business case for new POS system adoption, as retailers with unified commerce platforms see a 9.5 per cent increase in revenue on average according to data from ConnectPOS.

Calculating the ROI: Quantifying the Value of an Upgrade

Numbers don’t lie. Proving the value of an upgrade requires looking beyond the initial setup cost and examining the long-term impact on your overheads. You need a clear business case for new POS system adoption that speaks the language of profit and loss. When you quantify the direct savings and the potential for revenue uplift, the decision to modernise often moves from a “maybe” to a “must.”

Transaction Fee Optimisation

Legacy high-street banks often rely on your inertia. They keep you on outdated fee structures that include hidden markups and complex monthly rentals. Switching to an independent provider often reveals immediate savings. A reduction of just 0.5 per cent in your transaction fees can translate into thousands of pounds in annual profit for a busy merchant. This isn’t just about the rate; it’s about liquidity. Next-day funding ensures your takings are in your account when you need them, rather than being held by a distant bank for three to five working days. This immediate access to cash allows you to pay suppliers promptly and manage your stock more effectively.

Operational Efficiency Gains

Time is your most valuable asset. An intuitive interface reduces staff training time from days to hours. This is crucial for businesses with high staff turnover or seasonal peaks. You should also consider the financial benefit of tighter system permissions. By controlling who can issue refunds or void transactions, you significantly reduce “shrinkage” and internal errors. Automated reporting is the final piece of the puzzle. It typically saves senior management between five and ten hours per week by eliminating manual spreadsheet updates and data entry.

Manual data entry is a silent profit killer. Integrating your EPOS with accounting software like Xero or QuickBooks eliminates hours of administrative drudgery. If your manager reclaims five hours a week from bookkeeping, that is over 250 hours a year redirected toward high-value tasks like staff development or customer engagement. This efficiency is a cornerstone of a robust business case for new POS system investment.

Higher throughput is a direct result of faster service. If your team can process transactions 30 per cent faster, you can serve more customers during peak periods without increasing your headcount. In a restaurant setting, this often leads to an extra table turnover per evening. Finally, don’t ignore the tax side. Capital allowances often mean you can deduct the full cost of your hardware from your taxable profits in the first year, significantly reducing the net cost of your upgrade.

Building the Business Case: Aligning Stakeholders and Operations

A successful business case for new POS system adoption starts with a compelling executive summary. You must move beyond technical specifications and focus on three core pillars: Efficiency, Security, and Growth. Decision-makers need to see that this isn’t just a hardware swap. It is a strategic move to protect margins and scale the business. Start by auditing your current system’s performance. Record your average transaction times, the frequency of system freezes, and the hours spent on manual data entry each week. These baseline figures turn vague frustrations into hard data that justifies the investment.

Mapping the solution involves directly connecting new features to your specific pain points. If your main issue is slow service during the Friday rush, highlight how integrated payments and mobile terminals remove bottlenecks. When you present a clear link between a feature and a financial gain, the argument for change becomes undeniable. If you are ready to start this transition with a partner who values transparency, you can view our range of EPOS Systems to see how modern hardware fits your specific operational needs.

Addressing Stakeholder Objections

The most common hurdle is the “if it isn’t broken, don’t fix it” mentality. You can counter this by pointing to the upcoming April 2027 expiry of legacy payment devices and the mandatory PCI DSS v4.0.1 requirements. A system that “works” but leaves you open to fines or crashes is, by definition, broken. Many stakeholders also fear the complexity of data migration. Modern cloud platforms have made this process remarkably simple, allowing you to move your product lists and customer data with minimal manual input. For businesses prioritising liquidity, hardware rental models offer a low-risk alternative to upfront purchases, keeping your cash flow steady whilst you upgrade.

The Implementation Roadmap

Setting realistic expectations is vital for maintaining staff morale. A structured roadmap should include five distinct phases: Audit, Selection, Testing, Training, and Go-Live. To ensure zero lost sales, consider a “parallel run” where you test the new setup during quiet hours before fully switching over. This prevents the chaos of learning a new system whilst a queue of customers waits. Training should be hands-on and concise; modern interfaces are designed to be as intuitive as a smartphone, which naturally reduces the learning curve. Finally, ensure you have access to 24/7 technical support during the first 30 days to handle any teething issues with confidence.

The PurePay Hub Advantage: Simplifying Your Payment Infrastructure

Choosing the right partner is the final step in solidifying your business case for new POS system adoption. At PurePay Hub, we strip away the complexity and hidden markups that define the traditional banking sector. Our commitment is simple: we provide transparent, professional payment solutions designed specifically for the UK merchant community. We don’t believe in corporate jargon or opaque fee structures. Instead, we offer a “no-nonsense” approach that ensures you know exactly what you are paying for and why.

Efficiency starts with fair pricing. We offer UK-leading rates, with Debit transactions starting from 0.3 per cent and Credit from 0.5 per cent. When combined with our next-day funding, these rates provide a significant boost to your daily liquidity. Waiting for your money to clear is a thing of the past. We ensure your takings are available to re-invest in stock or staff when you need them most. This reliability acts as a stabilising force for your finances, allowing you to plan for growth with absolute confidence.

Tailored Solutions for UK Merchants

Every business has unique requirements. Whether you need a Countertop Card Machine for a fixed till point or a Portable Card Machine for table service, our hardware range is built for the rigours of daily trade. For those seeking a fully integrated experience, our EPOS Systems provide the centralised control we discussed earlier in this guide. We also offer a Business Cash Advance feature, providing a flexible way to fund expansion or refurbishments without the rigid constraints of traditional bank loans. Onboarding is designed to be stress-free, and we work closely with SMEs to ensure a smooth switch that avoids the typical exit fee headaches.

A Partnership Built on Trust

We position ourselves as a fair partner rather than a distant financial institution. This means you aren’t just another account number in a database. Every merchant we support has access to a dedicated account manager who understands the local business landscape. If you encounter a technical hurdle, our UK-based assistance team is ready to provide immediate, clear resolutions. We value discipline and integrity, ensuring that our support continues long after the initial sale is complete. Our goal is to act as your supportive business ally, helping you navigate the evolving world of payments with clarity and ease.

Modernising your infrastructure is an investment in your future. If you are ready to stop the revenue leakage caused by legacy tech and start enjoying fairer rates, we are here to help. Build your business case with a transparent quote from PurePay Hub and take the first step toward a more profitable, efficient operation today.

Modernise Your Business with Confidence

Building a robust business case for new POS system adoption is about more than just hardware; it’s about reclaiming your time and protecting your margins. We’ve detailed how quantifying the “friction tax” of slow processing and automating manual reconciliation can turn a cost centre into a growth engine. With the 2027 hardware deadlines fast approaching, staying with legacy tech is no longer the frugal choice. It’s a risk to your brand and your bottom line.

At PurePay Hub, we believe in fairness and clarity. We provide debit rates from 0.3% and ensure you have next-day access to your funds. There are no hidden markups or confusing corporate jargon here. We act as your supportive partner, helping you simplify your infrastructure so you can focus on your customers. You don’t have to navigate these changes alone. Take control of your financial future by making an informed choice today.

Get a transparent POS and payment quote for your business

Frequently Asked Questions

How long does it typically take to see an ROI on a new POS system?

You can typically expect a return on investment within 18 to 24 months. For high-volume merchants, the timeline is often shorter because the immediate reduction in transaction fees and administrative labour provides instant relief to your cash flow. This makes the business case for new POS system adoption particularly strong for businesses looking to scale quickly and reduce their daily overheads.

What are the essential features I should look for in a modern EPOS?

Look for a system that offers real-time inventory tracking, integrated payment processing, and automated reporting. A modern EPOS should act as a centralised hub for your operations, allowing you to manage staff and stock across multiple locations or online channels from a single interface. These features reduce manual errors and help you make data-driven decisions that protect your profit margins whilst improving the customer experience.

Can I keep my current merchant account when upgrading my POS hardware?

Whilst it is sometimes technically possible, we generally recommend switching to a provider that offers integrated processing. Using a separate, distant merchant account often results in higher fees and slower funding times. By moving to a unified setup, you benefit from a single point of contact for support and a more transparent fee structure that is untainted by hidden banking markups.

How does a new POS system help with PCI compliance?

New POS systems significantly simplify your compliance journey by using advanced encryption and tokenisation. This ensures that sensitive card data never actually enters your local network, which reduces the scope of your annual PCI DSS assessment. Modern terminals are also updated automatically to meet the latest security standards, ensuring you remain compliant with mandatory requirements like PCI DSS v4.0.1 without constant manual oversight.

Is it better to lease or buy POS hardware upfront?

Buying your hardware upfront is usually the most cost-effective option over a three-year period. However, leasing is an excellent alternative for businesses that prefer to preserve their cash flow for stock or expansion. We offer flexible models that allow you to access the latest EPOS Systems without a heavy initial capital outlay, making the transition manageable and predictable for regional SMEs.

What happens to my data if the internet goes down during service?

Most modern systems include an “offline mode” that allows you to continue processing transactions even if your internet connection fails. Your sales data is stored securely on the device and automatically synchronises with the cloud once your connection is restored. This prevents lost sales and ensures your business remains operational during peak hours, providing a stabilizing force for your finances regardless of technical glitches.

How do integrated payments differ from using a standalone card machine?

Integrated payments allow your POS hardware and card machine to communicate directly, eliminating the need for manual data entry. This reduces human error and speeds up the checkout process significantly. In contrast, a standalone machine requires your staff to type in the amount twice, which increases the risk of mistakes and slows down your service, ultimately leading to longer queues and customer frustration.

Will a new POS system integrate with my existing accounting software?

Yes, a modern EPOS will seamlessly integrate with leading accounting platforms like Xero or QuickBooks. This connection automates your daily sales sync and bank reconciliation, saving senior management several hours of administrative work each week. It is a vital component of any business case for new POS system investment, as it provides an accurate, real-time view of your financial health without the need for manual spreadsheets.

Leave a Reply