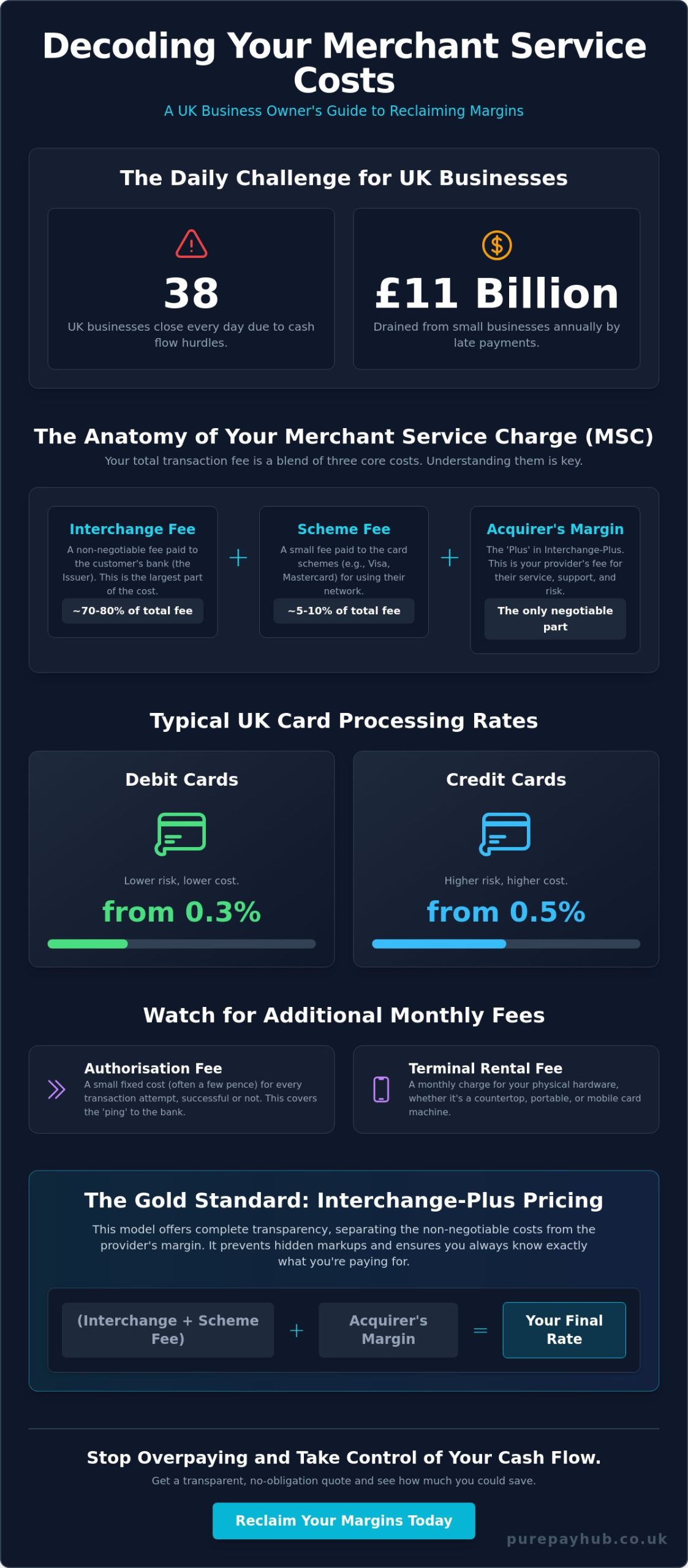

Thirty-eight UK businesses close every single day because of cash flow hurdles and the £11 billion drain of late payments. You likely feel that your monthly statement is a puzzle designed to be unsolvable. It’s frustrating to watch Interchange and MMSC fees eat into your hard-earned margins whilst you wait days for funds to settle. You deserve a partner that prioritises your growth over hidden markups. This guide provides merchant services explained UK business owners can use to reclaim their margins, stripping away the complexity to help you secure lower transaction rates and faster access to your capital.

We’ll explore the 2026 regulatory shifts, from the Commercial Payments Bill to the latest PCI DSS v4.0.1 standards, ensuring you have the clarity needed to make informed decisions for your business. Whether you’re looking for portable card machines or integrated EPOS systems, it’s time to turn your payment processing from a source of stress into a reliable engine for your cash flow. We’ve built this guide to move you from confusion to confident control, focusing on the transparency your business deserves.

Key Takeaways

- Understand the three core pillars of payment processing—merchant accounts, gateways, and terminals—to build a stable financial foundation.

- Learn to decode your monthly statement with our merchant services explained UK guide, helping you distinguish between debit and credit rates to lower your costs.

- Identify the most efficient hardware for your business, whether you require fixed countertop card machines or portable units for flexible service.

- Discover how a Business Cash Advance provides a flexible alternative to traditional bank loans by using your card turnover to secure growth capital.

- Master the stress-free process of switching providers by auditing hidden fees and requesting quotes that directly target your highest expense areas.

What are Merchant Services? Defining the UK Payment Ecosystem

Understanding the UK payment landscape starts with a foundational question: What are merchant services? In simple terms, it’s the ecosystem of hardware, software, and financial accounts that enables your business to accept card payments. It’s the invisible machinery that turns a customer’s plastic card or mobile wallet into settled funds in your bank account. This merchant services explained UK guide identifies three essential pillars that keep your business running smoothly.

- The Merchant Account: A specialised financial account where funds from card sales are held before being transferred to your business bank account.

- The Payment Gateway: The secure software bridge that authorises the transfer of data between your point of sale and the banks.

- The Card Terminal: The physical hardware, such as a countertop card machine or portable unit, used to process transactions in person.

Your standard business bank account isn’t designed to handle card transactions directly. It lacks the necessary infrastructure to communicate with card schemes like Visa or Mastercard. Instead, you require a Merchant ID (MID). Think of the MID as your unique digital fingerprint in the financial world. It ensures every penny processed is correctly attributed to your business and nobody else’s, providing a vital layer of security and accountability.

The Difference Between an Acquirer and an Issuer

Every card payment involves a conversation between two banks. The Issuer is the customer’s bank, which provides their credit or debit card. The Acquirer is your bank, the entity providing your merchant services. When a customer taps their card, the Acquirer asks the Issuer for permission to take the money. These two entities collaborate to authorise a transaction in seconds. They check for sufficient funds and ensure the card hasn’t been reported stolen. Your Acquiring Bank is your most vital partner. They take the risk of processing your sales and ensure the money eventually reaches your pocket.

Merchant Accounts vs. Business Bank Accounts

It’s helpful to view a merchant account as a holding pen for your authorised card funds. Money doesn’t jump instantly from a customer’s wallet to your business bank account. It sits in this holding pen whilst the banks perform essential security checks. Risk assessment happens at the merchant account level rather than at your high-street bank. This is because the merchant account provider assumes the liability for potential refunds or disputes. When you search for merchant services explained UK, you’ll find that the distinction between these accounts is the most critical factor for your settlement speed. PurePay Hub streamlines this connection, acting as a stabilising force that facilitates next-day access to funds to help you maintain a healthy cash flow.

Decoding the Costs: How UK Merchant Service Fees are Calculated

Deciphering a monthly statement often feels like solving a riddle without a key. The Merchant Service Charge (MSC) is the most significant figure you’ll encounter. It’s the core percentage taken from every transaction you process. In the UK, these rates aren’t uniform. Debit card rates typically start from 0.3%, whilst credit card rates usually begin from 0.5% because of the higher risk and processing costs involved. Understanding these baselines is the first step in ensuring you aren’t overpaying for your processing.

The UK Payment Systems Regulator (PSR) monitors the industry to ensure fairness, yet many providers still bury extra costs in the fine print. Beyond the transaction percentage, you’ll likely see a fixed authorisation fee. This is a small cost, often just a few pence, for every “ping” to the bank to confirm a customer has sufficient funds. You also need to account for physical hardware. Whether you use a countertop card machine or a mobile unit, monthly rental fees cover the cost of the terminal and the software updates required to keep it secure.

Interchange-Plus Pricing Explained

Transparency is the only way to truly understand your bill. Interchange-Plus pricing is the gold standard for clarity. The “Interchange” element is a non-negotiable fee set by card schemes like Visa and Mastercard. It’s paid to the customer’s bank. The “Plus” element is where your provider adds their specific margin for service and support. This model prevents providers from hiding massive markups behind a single, “blended” rate. When you have merchant services explained UK style, you’ll see that knowing exactly what the provider earns helps you negotiate a fairer deal.

PCI Compliance and Avoiding Non-Compliance Fines

Security isn’t just about protecting data; it’s about protecting your profits. The Payment Card Industry Data Security Standard (PCI DSS) is a mandatory set of rules for any SME handling card data. Many business owners ignore the paperwork, only to find “non-compliance fees” draining their accounts every month. These fines can range from £10 to £50 per month, which adds up to a significant annual loss. Choosing a partner that offers active PCI compliance monitoring turns a complex chore into a simple, automated process. If you’re tired of seeing unexpected charges on your statement, you can request a transparent quote that identifies exactly where you can save.

Choosing Your Hardware: Countertop, Portable, and EPOS Systems

The physical hardware you choose defines your customer’s final impression of your brand. It’s the moment a sale becomes a success. In this merchant services explained UK guide, we focus on matching hardware to your specific daily workflow. Choosing the right setup is a core part of having Merchant services tailored to your specific operations, ensuring you don’t pay for features you’ll never use.

- Countertop Card Machines: These are the workhorses for fixed retail locations. They connect via Ethernet or a phone line, providing maximum stability for high-volume till points. They don’t rely on batteries, making them the most reliable choice for a busy boutique or cafe.

- Portable and Mobile Units: Hospitality venues benefit from portable units using Bluetooth or Wi-Fi for “at-the-table” service. Mobile card machines use GPRS or 4G, making them ideal for tradespeople, delivery drivers, or market traders working on-the-go across the UK.

- Payment Links: You don’t always need a physical card to get paid. You can send a secure link via SMS or email to get paid instantly for invoices, deposits, or remote bookings.

Hardware isn’t just about swiping cards; it’s about how your business moves. A retail shop has different needs than a mobile plumber. Modern merchant services explained UK business owners can trust should always highlight that hardware must solve a problem, not create one. Whether you’re at a fixed counter or on the road, your equipment should be a silent, reliable partner in every transaction.

Integrated EPOS Systems for Hospitality and Retail

Modern businesses need their systems to talk to each other. An EPOS (Electronic Point of Sale) system isn’t just a digital till; it’s the brain of your business. Seamless integration means the price on the till automatically appears on the card machine. This reduces human error at the checkout, such as typing in the wrong amount. It also allows for real-time inventory management. You’ll know exactly what’s in stock and which items are your bestsellers through detailed sales reporting, helping you make smarter stock-buying decisions.

Virtual Terminals and Online Gateways

If you take orders over the phone, a Virtual Terminal is essential. It transforms your computer or tablet into a secure payment terminal. You can accept Mail Order and Telephone Order (MOTO) payments safely without needing physical hardware. This is particularly useful for wholesalers or service-based businesses. For those selling online, an Online Payment Gateway ensures your digital checkout experience matches your in-store professionalism. It provides a consistent, secure journey for every customer, ensuring their data is protected whilst your funds are processed efficiently.

Beyond Processing: Using Merchant Services to Support Cash Flow

Merchant services are often viewed as a cost centre. However, for a savvy SME, they act as a vital lever for growth. A core feature of modern merchant services explained UK providers offer is the Business Cash Advance. This is unsecured capital. It isn’t based on your asset wealth or a rigid credit score in the traditional sense. Instead, it’s based on your future card turnover. This makes funding accessible to businesses that might be rejected by a high-street bank. It removes the need for personal guarantees or putting your home at risk, which is a common barrier for many regional business owners.

The repayment model is where the real value lies. It’s a “pay-as-you-earn” system. You pay back a fixed percentage of your daily card sales. This means your repayments are always perfectly in sync with your income. If you have a slow Tuesday, you pay back less. If you have a busy Saturday, you pay back more. This flexibility is a lifesaver for seasonal businesses, such as coastal cafes or holiday rentals, during quieter trading periods. It ensures that your debt never outpaces your ability to pay, providing a stabilizing force for your finances.

Next-Day Funding: The Importance of Settlement Speed

Waiting for your money is a silent killer of small businesses. A 3-5 day settlement delay prevents you from restocking or paying staff on time. Healthy cash flow requires your funds to move as fast as your sales. You should look for a provider that offers next-day access to your capital. This removes the “weekend lag” where Friday’s takings don’t appear until the following Wednesday. Faster settlement keeps your business agile and responsive, ensuring your hard-earned money stays in your business rather than sitting in a holding pen.

Applying for a Business Cash Advance

Getting started is more straightforward than a bank loan application. Eligibility is typically based on just 3-6 months of card trading history. There are no fixed monthly repayments to worry about, which significantly reduces financial stress. Whether you need to fund a renovation, purchase bulk stock to prepare for a peak season, or handle emergency repairs, this capital is designed to work with your business cycle. It’s a partnership that prioritises your survival and expansion.

If you need a cash injection to take your business to the next level, apply for a Business Cash Advance today to see how much you could secure based on your card turnover.

How to Switch Merchant Service Providers Without the Stress

Many SMEs feel trapped by complex contracts and the fear of high exit penalties. It’s a common frustration. However, staying with a provider that drains your margins is often more expensive than the cost of leaving. This merchant services explained UK guide focuses on making the transition seamless, ensuring your business never misses a sale during the move. Your first step is a thorough audit of your current statement. Identify your contract end date and look closely for a Minimum Monthly Service Charge (MMSC) or hidden admin fees. These are the primary areas where you can secure immediate savings.

Requesting a competitive quote should be a targeted exercise. Don’t just look at the headline rate. Ask how a new provider will handle your specific pain points, such as slow settlement or high credit card fees. If you are still in contract, some modern providers offer support to help you manage exit fees. The goal is to move toward a partnership that prioritises your cash flow. Once you decide to switch, the onboarding process is designed to be quick. Modern systems ensure your new hardware arrives and is ready to use before your old contract even expires, preventing any downtime at the till.

The Onboarding Roadmap for UK SMEs

Moving your processing shouldn’t be a hurdle. The process follows three logical steps to get you up and running without stress.

- Step 1: Application. You’ll submit digital documents for a quick approval process. This usually takes just a few days.

- Step 2: Hardware Delivery. You receive your new countertop or portable card machine. Each unit is pre-configured for your business so you can test it immediately.

- Step 3: Integration and Training. If you’re using an EPOS system, this is where the software syncs. You can then briefly train your staff on any new features to ensure a smooth first day of trading.

Mastering Your Monthly Statements

You shouldn’t need an accounting degree to understand your own bill. A transparent merchant statement should clearly separate your Merchant Service Charge from your hardware hire. Look out for “junk fees” such as statement fees or excessive PCI non-compliance penalties that weren’t clearly explained at the start. If your statement is a wall of jargon, it’s a sign that your provider isn’t acting as a true partner. Clarity is the foundation of trust in this industry. You deserve to know exactly where every penny of your transaction fee is going. If you’re ready for a fairer approach to your payments, Get a transparent quote from PurePay Hub today and take back control of your business margins.

Secure Your Business Future with Transparent Payments

You now have the tools to navigate the UK payment landscape with confidence. We’ve covered everything from decoding complex Interchange-Plus pricing to choosing the right portable hardware for your team. This merchant services explained UK guide shows that you don’t have to accept hidden fees or slow settlement as the status quo. By auditing your statements and understanding your Merchant ID, you can protect your margins and ensure your cash flow remains stable.

It’s time to partner with a provider that values your growth as much as you do. We offer debit rates from 0.3% and credit rates from 0.5%, ensuring your costs stay low whilst your efficiency stays high. With next-day access to funds and dedicated, no-nonsense UK support, you can focus on running your business instead of chasing your money. Switch to PurePay Hub for transparent rates and next-day funding and experience a fairer way to get paid. Your business deserves a partner that treats you with the integrity you’ve worked hard to build. We look forward to supporting your next stage of growth.

Frequently Asked Questions

What are merchant services in simple terms?

Merchant services are the essential tools and financial accounts required to accept credit and debit card payments from your customers. This includes the physical card machines you use in-store, the secure online payment gateway for your website, and the merchant account that holds funds before they reach your business bank. It’s the complete machinery that turns a customer’s tap or click into settled capital for your business.

How much do merchant services cost for a UK small business?

Costs are generally split into transaction fees, monthly hardware rental, and compliance charges. You’ll typically pay a small percentage of every sale, with debit cards usually being cheaper to process than credit cards. Some providers also charge a fixed authorisation fee for every transaction. Having merchant services explained UK business owners can trust means looking for transparent, Interchange-Plus pricing to avoid hidden markups on your monthly bill.

How do I get a merchant account for my business?

You can obtain a merchant account by applying through a specialist payment provider. You’ll need to provide basic business information, proof of your UK trading address, and details of your expected transaction volumes. The provider performs a risk assessment to ensure your business model is stable. Once approved, your account acts as a secure holding pen for your authorised funds before they are settled into your business bank account.

What is the difference between a payment gateway and a merchant account?

A payment gateway is the secure software that captures and sends card data to the banks for authorisation. It acts as the digital bridge for your transactions. In contrast, a merchant account is the financial holding pen where funds sit whilst they are verified. You need both to process card payments successfully; the gateway handles the data transfer, whilst the account handles the actual money.

Can I take card payments without a card machine?

Yes, you can accept payments remotely using a Virtual Terminal or Payment Links. A Virtual Terminal turns your computer or tablet into a secure checkout for taking orders over the phone. Payment Links allow you to send a secure URL to your customer via SMS or email. These methods are ideal for service-based businesses or wholesalers who don’t require physical, face-to-face card readers to operate.

How long does it take for card payments to reach my bank account?

Settlement times vary between providers, but standard processing usually takes between one and three working days. Some providers now offer next-day access to funds to help improve your cash flow. It’s important to check if your provider processes payments over the weekend, as this can often lead to a “weekend lag” where Friday’s sales don’t arrive until the following week.

Are merchant services secure for my customers?

Modern merchant services are highly secure and must adhere to the Payment Card Industry Data Security Standard (PCI DSS). This ensures that every transaction is encrypted and sensitive customer data is never stored on your own devices. By using a compliant payment gateway and secure card machines, you protect your business from fraud and give your customers the confidence to spend with you safely.

What is a Merchant ID (MID) and why do I need one?

A Merchant ID (MID) is a unique identifier that distinguishes your business within the global payment ecosystem. You need one to ensure that the funds from your card sales are correctly routed to your specific merchant account. It acts as your digital financial fingerprint, allowing banks to track your transactions, manage your settlements, and provide you with accurate sales reporting for your business.

Leave a Reply