A 2026 study by money.co.uk found that only 46% of UK small business owners truly understand the fees they pay for their payment hardware. It’s a startling figure that highlights just how opaque the industry has become. If you’re trying to pin down the cost of renting a card machine UK, you’ve likely encountered a wall of jargon and hidden “statement fees” that make budgeting feel like guesswork.

We believe you deserve clear, predictable overheads and transaction rates that respect your profit margins. It’s exhausting to deal with long-term contracts and PCI compliance fines that feel designed to catch you out. This guide provides a transparent breakdown of monthly rental structures, transaction fees, and the specific charges that often stay hidden. We’ll help you calculate your true monthly spend so you can secure next-day access to your funds and keep your business moving with confidence.

Key Takeaways

- Understand the 2026 shift toward smart terminals and how integrated EPOS hardware can streamline your daily business operations.

- Learn how to calculate the true monthly cost of renting a card machine UK by separating fixed hardware leases from variable transaction rates.

- Compare the total cost of ownership between renting and buying to ensure your hardware never becomes obsolete or a drain on profit.

- Identify and eliminate “stealth” fees such as minimum monthly service charges and PCI compliance fines to protect your cash flow.

- Discover a transparent approach to payment processing where debit rates from 0.3% help you keep more of every sale.

Understanding Card Machine Rental in the UK Market

Renting a Payment terminal is a service-led agreement. It isn’t just about the physical box on your counter. You’re paying for a comprehensive package that includes the hardware, ongoing technical support, and critical software updates. Whilst a purchased reader might fail and leave you stranded, a rented unit includes a maintenance guarantee. If the tech breaks, the provider replaces it. This reliability is a core factor when calculating the true cost of renting a card machine UK. Most agreements in the current market span between 12 and 36 months, offering a stable framework for your business planning.

Why UK Businesses Prefer Rental Over Purchase

Many merchants choose rental to avoid large upfront costs. This preserves your capital for stock or marketing. You gain access to professional-grade hardware like a Countertop Card Machine or a Portable Card Machine without a heavy initial hit to your bank balance. Centralised updates are another win. Your provider pushes software changes automatically. This ensures your business stays compliant with the latest security standards without you needing to lift a finger. It’s about peace of mind. By removing the burden of hardware ownership, you can focus on growth instead of troubleshooting.

- Zero upfront capital: Better cash flow management for growing businesses.

- Automatic updates: PCI compliance is handled centrally by the provider.

- Hardware access: Use high-spec Mobile Card Machines without high purchase prices.

The 2026 Landscape: Smart Terminals and Connectivity

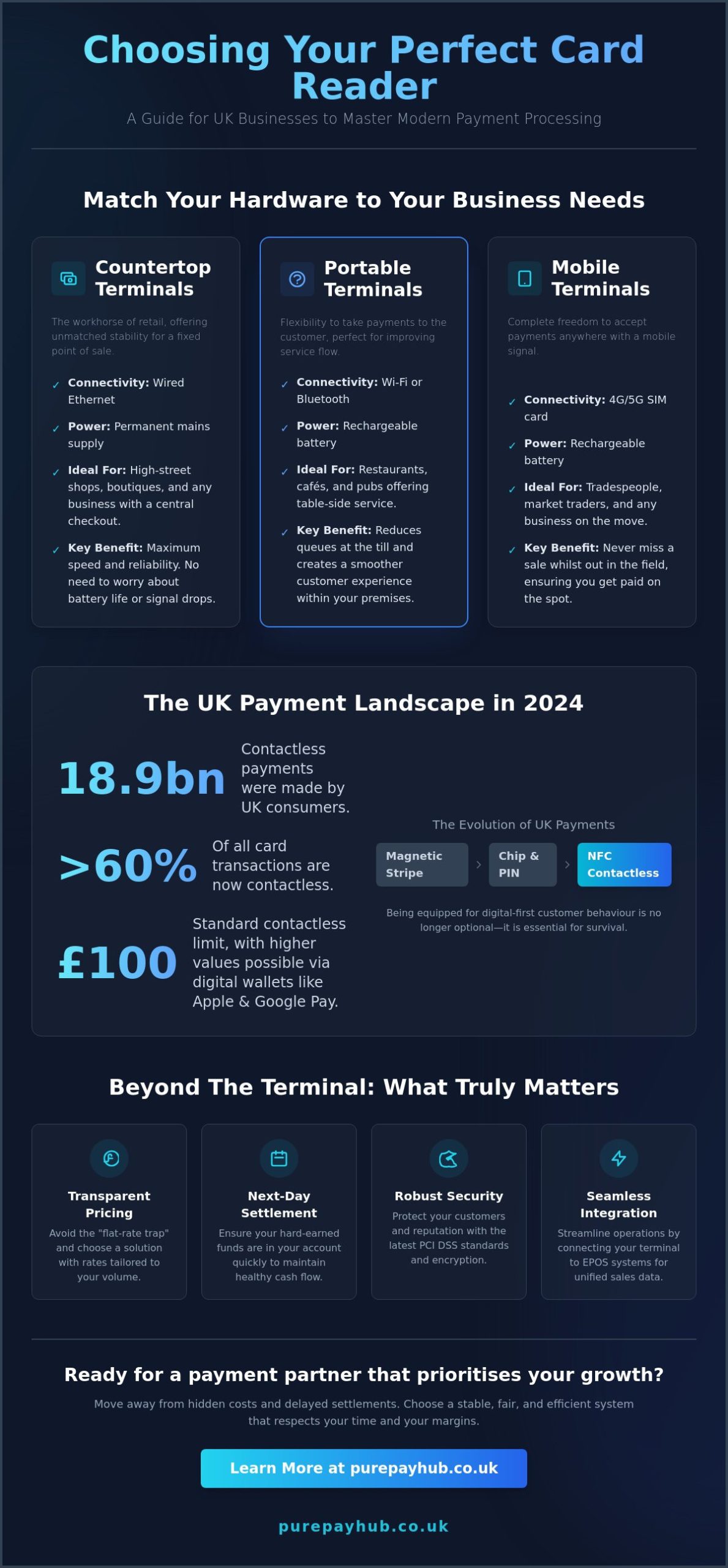

The market has moved far beyond simple chip-and-pin. In 2026, smart terminals are the standard. These devices integrate directly with your EPOS Systems to sync sales data in real time. Connectivity is faster than ever. New hardware utilises 5G and Wi-Fi 6 to ensure checkouts are instant, matching modern customer behaviour. Speed matters. Nobody wants to wait for a spinning wheel whilst a payment processes. When you evaluate the cost of renting a card machine UK, you’re investing in this future-proof infrastructure.

We’re also seeing a shift toward environmental responsibility. Modern rental agreements often feature eco-certified hardware and paperless receipt options. These small changes help your business meet local sustainability expectations whilst reducing waste. Integration with digital wallets like Apple Pay and Google Pay is now a baseline requirement. It’s a partnership that keeps your payment technology current whilst you focus on serving your customers.

Breaking Down the Monthly Cost: Rental vs Transaction Fees

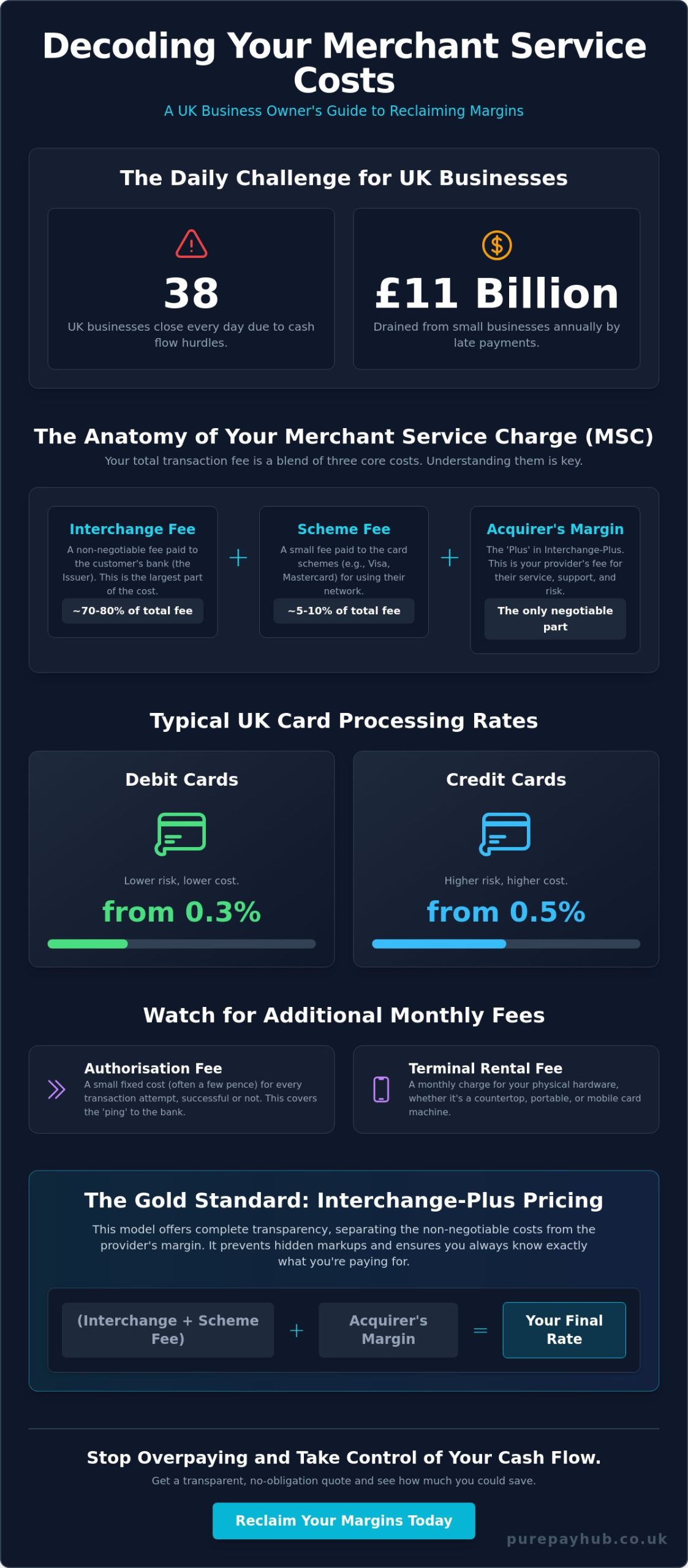

Understanding the cost of renting a card machine UK requires looking at two separate but connected pillars. The first is your hardware lease. This is a fixed monthly payment that stays the same regardless of your sales volume. The second is your transaction processing fee. This fluctuates based on your monthly turnover. Together, they form your Total Cost of Ownership (TCO). Many providers also include a Merchant Account Management fee. This covers the administrative cost of keeping your account secure and active. It’s a standard industry practice, but the price can vary significantly between providers.

The Hardware Lease: What Are You Paying For?

Think of this as the subscription fee for your physical kit. Whether you choose a Countertop Card Machine for a fixed till point or a Portable Card Machine for table service, the monthly fee provides a predictable baseline for your budget. This isn’t just a payment for the plastic and wires. It covers essential services that keep your business running. This includes professional technical support, rapid replacement units if your hardware fails, and constant security monitoring. Basic readers often come with lower monthly fees, but they lack the depth of integrated EPOS-ready terminals. These smarter units sync directly with your sales software, which reduces human error and saves hours of manual reconciliation every week.

Transaction-Based Processing Fees Explained

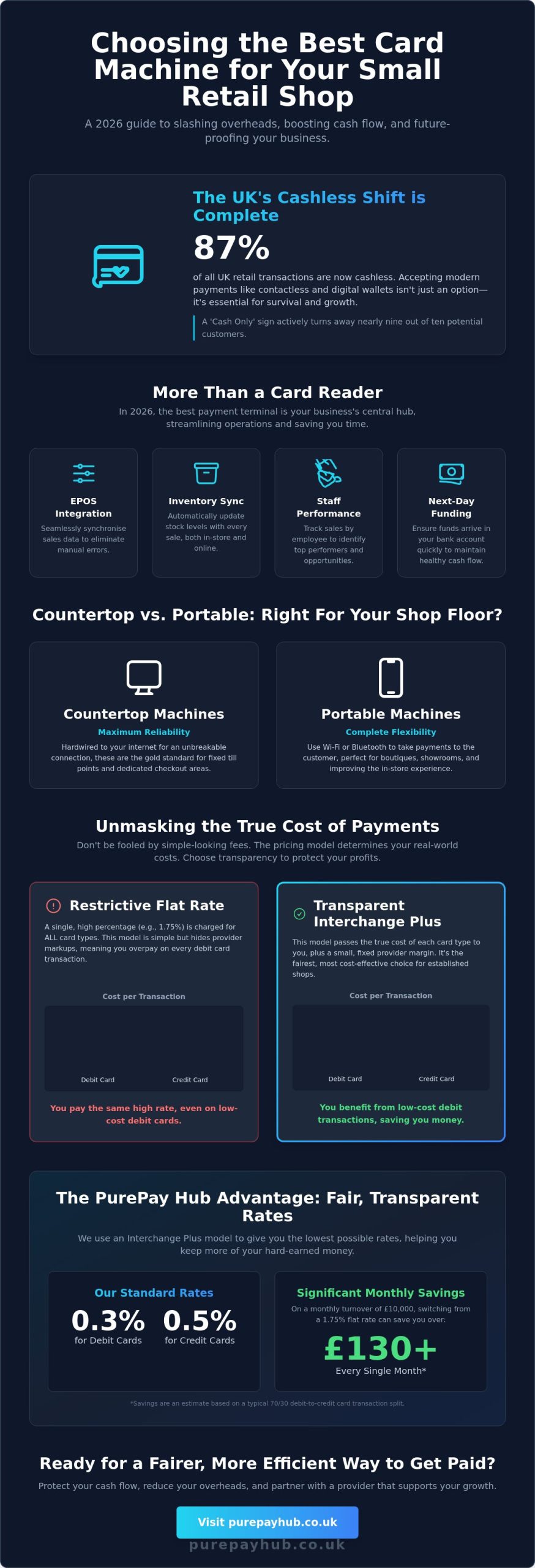

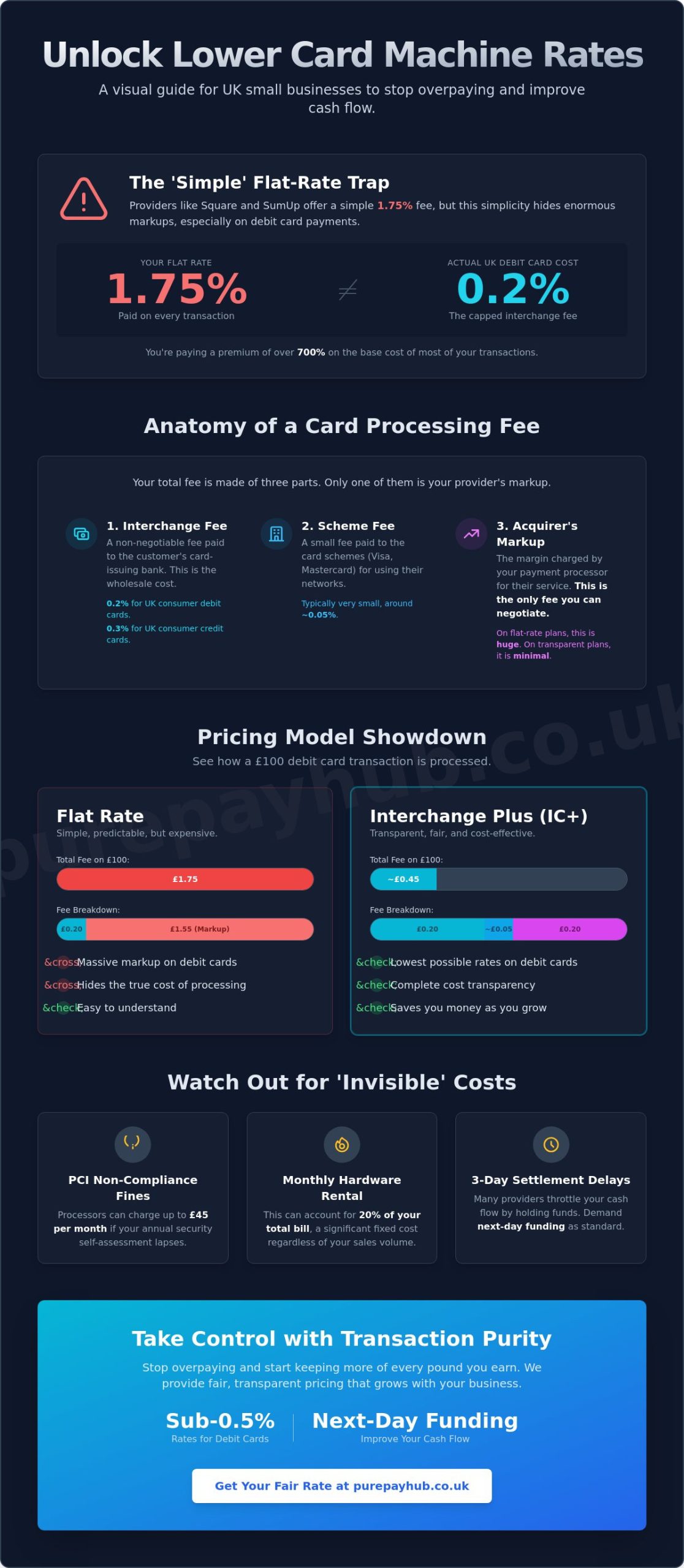

This is where the financial detail becomes critical. Rates are typically split based on the card type used. For example, you might see debit card charges at 0.3% whilst credit card fees sit at 0.5%. These rates are built from interchange fees and merchant service charges. The Payment Systems Regulator market review has highlighted how these fee structures impact UK merchants. It’s a complex area where transparency is often lacking.

Your business volume plays a massive role here. High-volume retailers often have the leverage to negotiate lower percentage rates. Whilst “fixed-rate” models marketed by some fintech companies look simple, they can actually be more expensive once you reach a certain turnover. A variable model that scales with your business is often the more professional choice for established shops. If you want to see how these pillars work together for your specific turnover, you can request a transparent fee breakdown to see exactly what you’ll pay each month. Balancing these two costs effectively is the secret to protecting your profit margins whilst maintaining a modern checkout behaviour.

Renting vs Buying: A Total Cost of Ownership Comparison

Choosing between owning your hardware and leasing it requires a long-term view. A simple price tag on a reader doesn’t tell the whole story. When you calculate the cost of renting a card machine UK over a three-year period, the numbers often flip in favour of the rental model for established businesses. Ownership carries an invisible burden of obsolescence. If you buy a device today, you’re stuck with that technology until it dies or you pay to replace it. Renters don’t have this worry. Their providers swap out ageing units for modern, 5G-ready hardware as standard. This ensures your checkout process remains fast and efficient without further investment.

Downtime is the silent profit killer. If your owned reader fails during a busy Saturday service, your revenue stops instantly. You’ll spend hours on hold with a generic tech support line or wait days for a new delivery. A rental agreement acts as an insurance policy. It includes a support contract that ensures hardware is replaced rapidly, often by the next business day. This protection of your cash flow is a value that purchase-only models simply can’t match. When you’re processing high volumes, the reliability of a managed service outweighs the one-off saving of a cheap reader.

Admin time also has a tangible financial value. Managing PCI compliance manually is a tedious, complex task for any owner. Rental providers handle the bulk of this centrally. They ensure your system remains secure and compliant without constant manual intervention. This reduces the risk of expensive non-compliance fines and frees you up to focus on your customers. For businesses with a monthly card turnover above £8,000, the lower transaction rates offered in rental contracts typically make this the most cost-effective path over the long term.

When Buying Makes Sense

Buying a basic reader is often the right choice for micro-businesses or seasonal traders. If you only trade at Christmas markets or summer festivals, a monthly rental fee might sit idle for half the year. Sole traders who don’t require integrated EPOS Systems or advanced reporting can benefit from the low entry price of a simple mobile reader. It’s a low-commitment way to start taking payments, provided you don’t mind slightly higher transaction fees on every sale.

The Strategic Advantage of Renting

For growing businesses, renting offers unmatched scalability. You can easily add more Portable Card Machines to your fleet as your team expands or your premises grow. There’s also a significant tax advantage. Rental payments are typically fully deductible as a business expense, which simplifies your accounting. You gain peace of mind with 24/7 technical support and the knowledge that your cost of renting a card machine UK covers every eventuality, from hardware failure to software security updates.

Avoiding the Fine Print: Hidden Costs in Rental Contracts

The headline price on a quote rarely tells the whole story. When you calculate the true cost of renting a card machine UK, you must look past the hardware lease and transaction rates. Many traditional providers bury “stealth” fees in the fine print that can quickly erode your profit margins. Statement fees are a classic example. These are monthly charges just to receive a digital summary of your own sales data. Exit fees and auto-renewal clauses are even more restrictive. If you don’t cancel your agreement within a narrow window, your 18-month contract might reset for another full term without your consent. It’s a practice designed to trap you in long-term cycles.

Chargeback fees and refund charges also impact your monthly spend. Every time a customer disputes a payment or you process a return, the provider may charge an administrative fee. Whilst these are sometimes unavoidable, they should be clearly defined from day one. You also need to watch for “authorised” vs “unauthorised” fee structures. These can lead to unexpected markups on certain card types that weren’t clearly explained during the initial sales pitch. If you’re tired of decoding complex bills, you can get a transparent quote today to see how we eliminate these hidden markups.

The PCI Compliance Trap

PCI Non-Compliance fines are perhaps the most avoidable hidden cost on your bill. If you haven’t completed your annual security assessment, providers often slap a fee on your statement. These fines can reach £30 or more every single month. A supportive partner won’t just fine you. They will help you organise your business and guide you through the Self-Assessment Questionnaire (SAQ) to ensure your terminal security is standard across all your sites. This proactive approach saves you hundreds of pounds a year whilst keeping your customer data safe.

Minimum Monthly Service Charges (MMSC)

Minimum Monthly Service Charges (MMSC) act as a safety net for the provider, not for you. This fee works by setting a floor for your transaction processing. If your transaction fees don’t reach a set threshold, you pay the difference to the provider. This matters immensely for seasonal businesses or those with fluctuating trade. If you have a quiet month in January, you’re essentially paying for transactions you never made. When assessing the cost of renting a card machine UK, always look for providers with fair or zero MMSC structures to protect your cash flow during slower periods.

PurePay Hub: Transparent Terminal Rental for UK Merchants

PurePay Hub provides a standard of quality that traditional banks often miss. We understand that the cost of renting a card machine UK shouldn’t be a mystery. Our approach is built on professional advocacy for the local merchant. We offer competitive rates that respect your margins. Debit card processing starts from 0.3% and credit cards from 0.5%. This clarity allows you to budget with precision. You won’t find any hidden markups here.

Our range covers every operational need. You can choose a Countertop Card Machine for busy retail points or mobile solutions for trading on the move. We also provide integrated EPOS Systems that sync your sales and stock data effortlessly. A critical advantage of our service is next-day access to your funds. Whilst some providers hold onto your money for days, we ensure your cash flow remains healthy. It’s your money. You should have it when you need it. This speed acts as a stabilising force for your business finances.

A Partnership Built on Transparency

We’ve built our reputation on eliminating hidden markups. This has made our service a favourite amongst UK SMEs who are tired of murky fee structures. The onboarding process is disciplined and efficient. We aim to get your business set up and taking payments within days, not weeks. Beyond hardware, we act as a supportive ally for your future development. This includes access to a Business Cash Advance. It’s a flexible way to fund growth based on your future card sales. We position ourselves as a fair partner rather than a distant financial institution.

Next Steps for Your Business

Every business is unique. A generic price list won’t reflect your specific transaction volume or card mix. We recommend a personalised review of your current merchant statements. This allows us to identify exactly where you are overpaying. We can then provide a tailored quote that reflects your actual trading behaviour. This ensures the cost of renting a card machine UK remains as low as possible for your specific circumstances. We value straight-talking and efficiency above all else.

Stop guessing about your overheads. You can Get a transparent card machine rental quote from PurePay Hub today. Our team is ready to provide the straight-talking advice you need to manage your payments effectively. Let’s build a partnership that prioritises your profit and provides the clarity you deserve.

Take Control of Your Payment Overheads

Effective business management requires more than a working terminal. It demands a partnership built on honesty. We have explored how hardware reliability and the absence of hidden stealth fees are the true markers of a sustainable agreement. By choosing a model that scales with your turnover, you ensure that your checkout technology remains a tool for growth rather than a drain on your margins. Understanding the cost of renting a card machine UK allows you to move past the confusion of traditional banking and into a state of informed confidence.

You shouldn’t have to wait for your own money or decode complex monthly statements. We provide a no-nonsense approach that prioritises your cash flow and rewards your hard work. With debit rates starting from 0.3% and next-day funding as standard, you can focus on serving your community whilst we handle the technicalities. It’s time to demand better from your payment provider. Switch to a fairer payment partner with PurePay Hub and experience the clarity of a truly transparent service. Your business deserves a partner that values integrity as much as you do.

Frequently Asked Questions

How much does it typically cost to rent a card machine in the UK?

Typical terminal rental in the UK costs between £10 and £40 per month. This price varies based on the hardware type and the length of your contract. For example, a basic Countertop Card Machine usually sits at the lower end of the scale. A feature-rich Portable Card Machine with 4G connectivity will naturally command a higher monthly fee to cover the advanced technology.

Are there any hidden fees I should look out for in a rental contract?

Watch for statement fees, minimum monthly service charges (MMSC), and exit fees. These are common hidden costs that aren’t always mentioned in the initial sales pitch. You should also check for PCI non-compliance fines. These can reach £30 per month if you don’t complete your annual security tasks. Some providers also charge extra for till rolls or processing customer refunds.

Can I rent a card machine for a short-term event or pop-up shop?

Short-term rental is possible for pop-up shops and seasonal events. Whilst standard contracts are longer, some providers offer rolling monthly agreements or specific event hire. Be aware that the daily or monthly rate for these flexible options is often higher than a traditional 18-month lease. It is a practical solution for businesses that don’t need a permanent payment till point.

What is the difference between a rental fee and a transaction fee?

A rental fee is a fixed monthly payment for your hardware, whilst a transaction fee is a variable percentage of each sale. The total cost of renting a card machine UK involves balancing these two figures. Renters often pay a monthly fee to access lower transaction rates. This approach typically saves money as your monthly sales volume grows over time.

Is it better to rent or buy a card machine for a small business?

Renting is usually better for businesses with a monthly card turnover exceeding £8,000. At this level, the lower transaction rates of 0.75% to 1.5% found in rental contracts outweigh the monthly hardware fee. For micro-businesses with lower volumes, buying a reader outright with a flat 1.75% rate can be more cost-effective over a three-year period.

How long are the typical contract terms for card machine hire?

Most UK rental contracts last for 12 to 18 months. Some providers offer longer terms of up to five years to lower the monthly hardware cost. You must check for auto-renewal clauses. These can automatically extend your commitment if you don’t provide notice within a specific timeframe. Always ensure you understand the notice period required to exit the agreement.

What happens if my rented card machine stops working?

Your agreement should include technical support and rapid hardware replacement as part of the service. If your device fails, most rental providers will send a new unit by the next business day. This protection is included in your monthly fee. It prevents the lost revenue that occurs when a purchased reader breaks and the owner has no immediate support or replacement.

Do rental costs include PCI compliance management?

Many providers include compliance assistance, but you are still responsible for completing the necessary assessments. The cost of renting a card machine UK can escalate if you are hit with non-compliance fines. These charges are avoidable if you work with a partner who helps you organise your security documentation and guides you through the self-assessment questionnaire correctly.