Total payment fraud losses in the UK reached £1.28 billion in 2025, a stark reminder that your checkout is often the most vulnerable part of your business. Finding a secure online payment gateway for ecommerce isn’t just about technical compliance. It’s about protecting your revenue and building genuine trust with every customer. You’ve likely felt the frustration of abandoned carts caused by clunky checkouts, or the stress of seeing your funds held for days on end by traditional, distant providers.

We believe in a no-nonsense approach to finance that prioritises the merchant. You deserve a partner that offers clarity instead of corporate jargon and hidden fees. This guide will help you master the technical and security essentials required to protect your business whilst providing a seamless checkout experience for your UK customers. We’ll show you how to turn your payment setup into a competitive advantage.

We’ll examine the requirements of PCI DSS v4.0.1 and the July 2026 Mastercard data mandate. You’ll also discover how to secure next-day access to your sales revenue and achieve transaction rates that actually support your growth. It’s time to move from frustration toward a state of informed confidence.

Key Takeaways

- Understand why your digital “handshake” is the key to reducing basket abandonment and building lasting trust with your UK customer base.

- Learn how to navigate the latest PCI-DSS v4.0.1 requirements and 3D Secure 2.0 to protect your business from rising fraud.

- Discover why next-day funding is a critical feature for maintaining healthy cash flow compared to the slow settlement times of major aggregators.

- Master the essentials of choosing a secure online payment gateway for ecommerce that offers transparent pricing and integrates with your card machines.

- Demystify the complex journey of a transaction from the moment a customer clicks “Pay Now” to the final settlement in your account.

Why a Secure Online Payment Gateway is Critical for Your UK Ecommerce Growth

Think of your gateway as the digital “handshake” between your website and the global banking network. It is the precise moment where trust is either solidified or broken. Implementing a secure online payment gateway for ecommerce is no longer just a technical tick-box exercise. It is a fundamental requirement for survival in a market where 76% of UK consumers now prioritise data security when choosing an online merchant. If that handshake feels weak or suspicious, your customers will simply walk away.

There is a direct correlation between visible security markers and reduced basket abandonment. British shoppers are savvy; they look for reassurance before entering their card details. When a checkout looks professional and displays recognised security protocols, friction disappears. Conversely, the cost of insecurity is absolute. A single data breach can end a small UK business overnight. Beyond the immediate financial penalties, the loss of reputation is often impossible to recover. With UK payment fraud losses reaching £1.28 billion in 2025, your gateway acts as your first and strongest line of defence.

The goal for 2026 is a “frictionless” secure checkout. Security should never be a hurdle that slows down a legitimate purchase. Modern gateways use background authentication to verify users without forcing them through endless pop-up windows. This balance keeps your revenue safe whilst ensuring the user journey remains fast and intuitive.

The Role of the Gateway in the Payment Ecosystem

Confusion often exists between a gateway and a merchant account. Your gateway is the messenger that carries transaction data. The merchant account is the destination where your funds are held before being settled into your business bank account. You need both to accept card payments online in the UK. To understand the technical journey, it helps to research How Payment Gateways Work as a secure relay. This system doesn’t just move data; it protects you from fraudulent chargebacks by verifying the legitimacy of every request in real-time.

Building Customer Trust in 2026

Trust is built through familiarity and technical excellence. Standards like 3D Secure 2.0, including “Verified by Visa” and “Mastercard ID Check”, are now the expected norm for British shoppers. These tools provide an extra layer of protection that reduces your liability for fraud. Localised payment methods also play a vital role in conversion. A secure online payment gateway for ecommerce should feel local to the shopper, offering the currencies and card types they use every day. A payment gateway is a secure bridge for encrypted transaction data. By ensuring this bridge is robust, you provide the stability your business needs to grow.

Behind the Scenes: How Payment Gateways Secure Every Transaction

When your customer clicks “Pay Now”, a complex sequence of events triggers in less than a second. This millisecond journey is the difference between a successful sale and a potential security breach. A secure online payment gateway for ecommerce acts as the invisible orchestrator between your website, the card schemes, and the banking network. It ensures that sensitive data travels safely whilst filtering out malicious actors before they can impact your bottom line.

The process involves two primary financial institutions: the Acquiring Bank and the Issuing Bank. The Acquiring Bank is your business bank, responsible for receiving the funds. The Issuing Bank belongs to your customer and is the entity that approves or declines the transaction based on available funds and security checks. Between these two points, encryption serves as a protective tunnel. By using SSL/TLS protocols at the browser level, the gateway prevents “man-in-the-middle” attacks, where hackers attempt to intercept data as it moves through the internet.

The 5-Step Security Sequence

- Step 1: Data Capture and Encryption. Card details are immediately encrypted at the point of entry. This ensures your website never actually “sees” or stores the raw data.

- Step 2: Authentication. The system uses 3D Secure protocols to verify the cardholder’s identity, often through a mobile app notification or biometric check.

- Step 3: Authorisation. A request is sent through card schemes like Visa or Mastercard to the Issuing Bank to confirm the transaction is legitimate.

- Step 4: Fraud Scrubbing. The gateway applies advanced filters to check for suspicious patterns, such as high-risk IP addresses or unusual purchase behaviour.

- Step 5: Final Response. The gateway relays the approval or decline back to your checkout page to complete the user journey.

This rigorous verification and response phase happens instantly. If you are looking for a partner to manage this complexity with total transparency, our Online Payment Gateway is designed specifically for the needs of British merchants.

Tokenisation: The Future of Card Data Security

Tokenisation is a game-changer for modern ecommerce. It replaces sensitive card numbers with unique, non-sensitive “tokens”. If a hacker were to breach a database of tokens, the information would be useless to them. This technology significantly reduces your burden when adhering to PCI-DSS Security Standards. Because the actual card data stays with the processor, your compliance requirements are simplified.

Beyond security, tokenisation enables the seamless experiences customers now expect. It powers “one-click” checkouts and manages recurring subscriptions without requiring the customer to re-enter their details. This balance of safety and speed is what defines a truly effective secure online payment gateway for ecommerce in 2026. It allows you to focus on growth whilst the technical heavy lifting happens safely in the background.

Navigating Security Standards: PCI-DSS and 3D Secure 2.0

Security standards are often viewed as a burden; however, they are your best defence against the growing threat of cybercrime. For any merchant, a secure online payment gateway for ecommerce must adhere to the Payment Card Industry Data Security Standard (PCI-DSS). This is not a suggestion. It is a global requirement to ensure all companies that process, store, or transmit card information maintain a secure environment. If you fail to meet these standards, the consequences are significant.

The legal implications for non-compliance in the UK are severe. Beyond the risk of heavy fines from card schemes, you face the potential loss of your ability to process payments entirely. Most small businesses don’t have the resources to build a digital fortress. This is where a hosted payment page becomes invaluable. By redirecting your customers to a secure environment managed by your provider, you offload 99% of your security risk. Your servers never touch the sensitive data, which simplifies your life and protects your customers.

Understanding Your PCI Compliance Responsibilities

Compliance levels vary based on how you handle data. Most small ecommerce sites fall under SAQ A, which applies when you use a hosted page. If you store card data on your own servers, you face the much more rigorous SAQ D. We help our merchants navigate these requirements to avoid the monthly non-compliance fees that often catch business owners off guard. Choosing a Level 1 PCI Service Provider is non-negotiable. It ensures your partner meets the highest possible security audit standards.

The Evolution of 3D Secure

The original 3D Secure was a conversion killer. It forced customers to remember complex passwords, leading to abandoned carts. 3D Secure 2.0 (3DS2) has changed the game by using biometrics and app-based verification. This aligns with the requirements for Strong Customer Authentication (SCA) in the UK. It ensures that high-risk transactions are verified without ruining the user experience.

Customers today are more aware of secure online shopping practices than ever before. They expect a checkout that feels modern and safe. A major benefit of using 3DS2 is the liability shift. By successfully authenticating a transaction through 3DS2, the liability for fraudulent chargebacks shifts from the merchant to the bank. This provides an essential layer of financial protection for your business. Implementing a secure online payment gateway for ecommerce that supports these protocols isn’t just about safety. It is about building a resilient, trusted brand that prioritises customer security.

Choosing Your Provider: Beyond Just Transaction Rates

Choosing a secure online payment gateway for ecommerce involves looking past the flashy marketing of global aggregators. Many merchants fall into the trap of only comparing the headline transaction fee. Whilst a low percentage looks attractive on paper, it often masks inefficiencies that can cripple your daily operations. Large, multi-national payment platforms are popular for their quick setup. However, they often lack the localised support and flexible funding options that an independent UK provider can offer.

You must also be vigilant regarding hidden costs. It’s common to see extra charges for gateway access, PCI compliance, and monthly statements. These micro-fees quickly add up, eating into your margins. A transparent partner will lay these out clearly from the start. If you sell both online and in-person, ensure your gateway integrates with your EPOS Systems. Having a single view of your sales across all channels simplifies your accounting and inventory management.

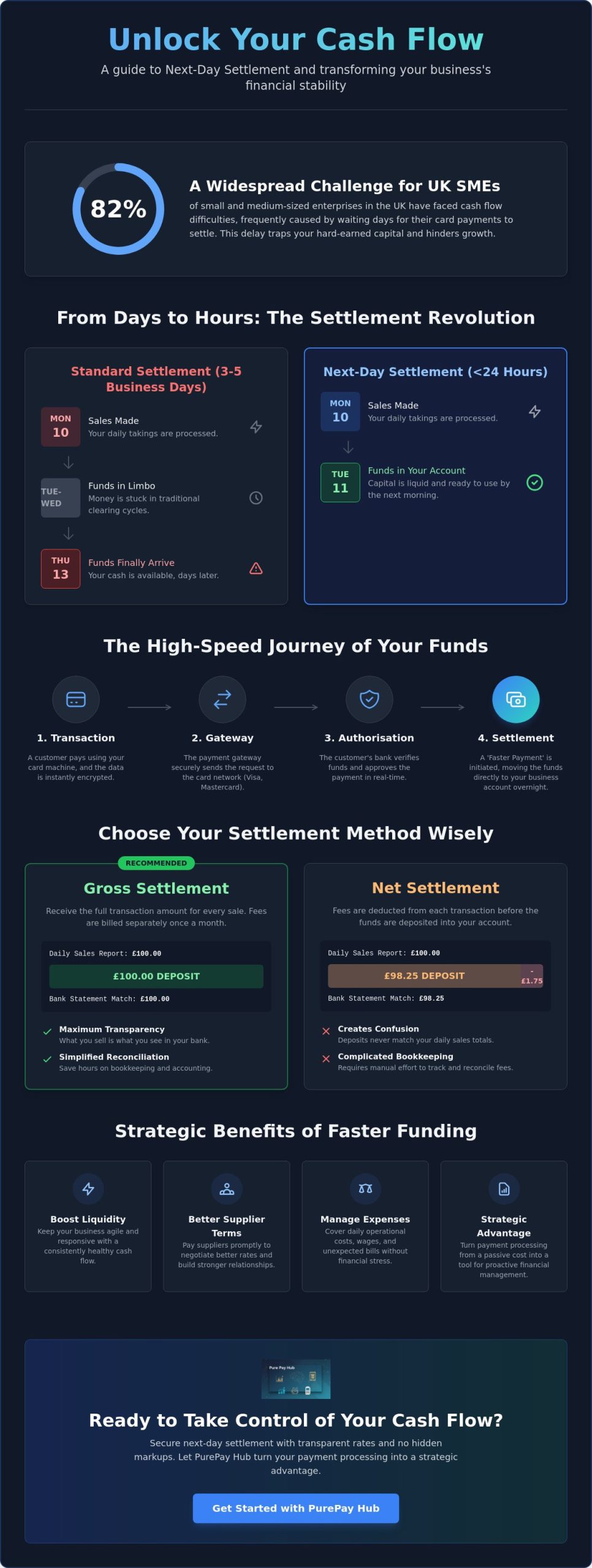

Settlement Speeds: Why 7 Days is Too Long

The funding gap is the silent killer of small business cash flow. This is the delay between a customer paying and the money actually landing in your bank account. Standard settlement windows can stretch to seven days or more. This delay makes it difficult to manage payroll, pay suppliers, or restock inventory. We believe you should have next-day access to your sales revenue. Accelerated settlement provides a significant competitive edge for UK SMEs, allowing you to reinvest your hard-earned cash immediately rather than waiting for a distant processor to release it.

Pricing Models: Interchange-Plus vs Flat Rate

Flat-rate pricing is simple but often expensive. If you pay a flat 1.75% on every transaction, you’re likely overpaying for debit card payments. Debit cards carry much lower processing costs than premium credit cards. Interchange-plus pricing is the no-nonsense alternative. It provides total transparency by separating the actual cost of the transaction from the processor’s markup. This ensures you only pay a fair margin on top of the base rates. PurePay Hub offers rates as low as 0.3% for debit and 0.5% for credit cards, reflecting our commitment to fair and honest pricing for the local merchant community. If you’re ready for a fairer deal, you can get a transparent quote today to see how much you could save.

A secure online payment gateway for ecommerce should be a tool for growth, not a source of frustration. By prioritising settlement speed and pricing transparency, you ensure your business remains agile and profitable in an increasingly competitive UK market.

PurePay Hub: Transparent, Secure, and Built for British Business

Traditional corporate processors often treat merchants like entries on a spreadsheet. They hide behind layers of jargon and opaque fee structures that make it impossible to know what you are actually paying. PurePay Hub was founded to disrupt this culture. We provide a no-nonsense alternative designed specifically for regional business owners who value honesty and integrity. We aren’t a distant financial institution. We are a fair partner committed to your growth.

One of the biggest frustrations for merchants is the lack of support when things go wrong. Most technical guides focus on the code, but they ignore the human reality of a gateway failure. When a transaction won’t process during your busiest hour, you don’t need a chatbot or a generic ticket number. You need a UK-based expert who understands your market and can provide immediate clarity. Our support team is disciplined and knowledgeable, ensuring you never feel abandoned by your technology. We’ve simplified the onboarding process, allowing most businesses to start taking payments within 24 to 48 hours.

The PurePay Hub Advantage for Ecommerce

Efficiency shouldn’t be complicated. Our secure online payment gateway for ecommerce integrates seamlessly with major platforms like Shopify, WooCommerce, and Magento. This ensures your technical transition is smooth and your checkout remains stable from day one. We also address the funding gap mentioned earlier by providing next-day funding as standard. This keeps your cash flow healthy and allows you to reinvest in your business without delay. You can track every penny through our centralised merchant dashboard, which offers transparent reporting untainted by hidden markups.

Supporting Your Growth with Business Cash Advances

Growth often requires capital, but traditional bank loans can be rigid and slow. We offer a Business Cash Advance as a flexible alternative for retailers. This facility provides capital based on your future card sales. Instead of fixed monthly payments, the advance is repaid as a small percentage of your daily takings. This means your repayments stay in sync with your actual revenue; if you have a quiet day, you pay back less. It is a fairer way to fund inventory or expansion without the stress of a traditional debt schedule.

Choosing a secure online payment gateway for ecommerce is about more than just security protocols. It is about finding a single partner that can handle your card machines, online payments, and growth capital with total transparency. If you are ready to move away from the opaque practices of traditional competitors, we are here to help. Organise your secure payment gateway with PurePay Hub today and experience a fairer way to take payments.

Secure Your Future with a Fairer Payment Partner

The landscape of digital payments in 2026 demands a balance between rigorous security and an effortless user experience. You now know that a secure online payment gateway for ecommerce is more than just a technical necessity. It’s the foundation of your customer’s trust and your business’s financial health. By prioritising Level 1 PCI security and embracing 3DS2 protocols, you protect your revenue whilst reducing friction at the checkout.

Don’t let slow settlement times or opaque fee structures hold your growth back. You deserve a partner that offers clarity and rewards your hard work with faster access to your funds. Transitioning to a system that puts the merchant first provides the stability you need to scale in the competitive UK market. It’s about moving from technical confusion to a state of total confidence.

Switch to a fairer, more secure payment gateway with PurePay Hub and benefit from debit card rates from 0.3%, next-day funding for UK merchants, and Level 1 PCI-compliant security. We’re ready to help you build a more resilient and profitable business today.

Frequently Asked Questions

What is the difference between a payment gateway and a payment processor?

A payment gateway is the digital “handshake” that encrypts transaction data at the point of sale. The processor is the back-end system that actually moves the money between the different banks involved. You need both to function, though many modern providers bundle these services together for simplicity. This integration helps you avoid the technical headache of managing multiple different contracts and connections.

How much does a secure online payment gateway cost in the UK?

Costs vary based on your transaction volume and the pricing model you choose. Most providers charge a percentage per transaction plus a small fixed fee. You should also look for monthly gateway fees or PCI compliance charges that might be hidden in the small print. A transparent provider will always show you these costs upfront to help you manage your business cash flow effectively.

Is my business too small to need a secure payment gateway?

No business is too small to prioritise security. Every merchant needs a secure online payment gateway for ecommerce regardless of their turnover. Fraudsters often target smaller sites because they assume the security measures are weaker. Protecting your customer data is a legal requirement in the UK and is essential for building a brand that shoppers can actually trust.

How long does it take to set up an online payment gateway?

Setting up a modern gateway typically takes between 24 and 48 hours. This includes the time needed for identity checks and linking the system to your website. Once your account is approved, integration is usually a simple process of installing a plugin or entering an API key. You can be taking payments and generating revenue almost immediately after your application is processed.

Can I use the same gateway for my physical shop and my online store?

Yes, you can use an integrated system to manage both your physical shop and your online store. This is often achieved through an EPOS system that synchronises your inventory and sales data in one centralised place. It simplifies your accounting significantly and provides a consistent experience for your customers, whether they are buying from you in person or through your website.

What happens if my payment gateway goes down?

If a gateway goes down, your website cannot accept payments, which leads to immediate revenue loss and frustrated customers. High-quality providers maintain multiple redundant servers to ensure maximum uptime. You should always choose a partner with a proven track record of stability. This ensures your business remains open for orders every hour of the day without technical interruptions.

Do I need a separate merchant account for my ecommerce gateway?

You do need a merchant account to receive funds, but it doesn’t always have to be a separate contract. Some providers offer a bundled service where the secure online payment gateway for ecommerce and the merchant account are provided as one package. This often makes the setup process much faster for new businesses and provides you with a single point of contact for support.

How does 3D Secure 2.0 affect my checkout conversion rate?

3D Secure 2.0 actually helps improve conversion rates by making the authentication process frictionless for the shopper. Unlike the old system that required complex passwords, 3DS2 uses biometrics and background data checks to verify the cardholder. This reduces basket abandonment whilst providing the high level of security your customers expect. It turns a potential hurdle into a smooth and reassuring experience.