Did you know that contactless payments reached a staggering 19.2 billion transactions in the UK last year? As of March 2026, UK Finance reports that 76% of all debit card payments are now tap-and-go. If you want to accept Apple Pay on card machine UK terminals, you aren’t just following a trend; you’re building a Pure security layer for your business. You likely feel the weight of opaque fee structures from traditional banks and worry about the technical glitches that often strike during peak trading hours.

We understand that the shift toward mobile wallets can feel complex, especially with the FCA’s March 2026 removal of the mandatory £100 contactless limit. This guide cuts through the corporate jargon to show you exactly how to integrate Apple Pay whilst securing the lowest transaction-based rates. You will discover how to speed up your checkouts, protect your revenue from fraudulent chargebacks, and navigate the latest 2026 pricing from providers like SumUp and Square. It’s time to bring clarity and honesty back to your payment processing hub.

Key Takeaways

- Learn how tokenisation and biometric verification provide a superior security layer against fraud compared to traditional 4-digit PINs.

- Discover how to choose the perfect hardware to accept Apple Pay on card machine UK terminals, whether you require fixed countertop units or portable Wi-Fi devices.

- Understand the “Pure” advantage of transaction-based pricing, featuring 0.3% debit and 0.5% credit rates to help you avoid hidden merchant service charges.

- Gain insight into why digital wallets have become the primary payment method for UK shoppers in 2026 and how this trend boosts your checkout speed.

- Follow our straightforward guide to conducting a rate review, allowing you to identify unfair markups and switch to a more transparent payment partner.

What is Apple Pay and why is it essential for UK businesses in 2026?

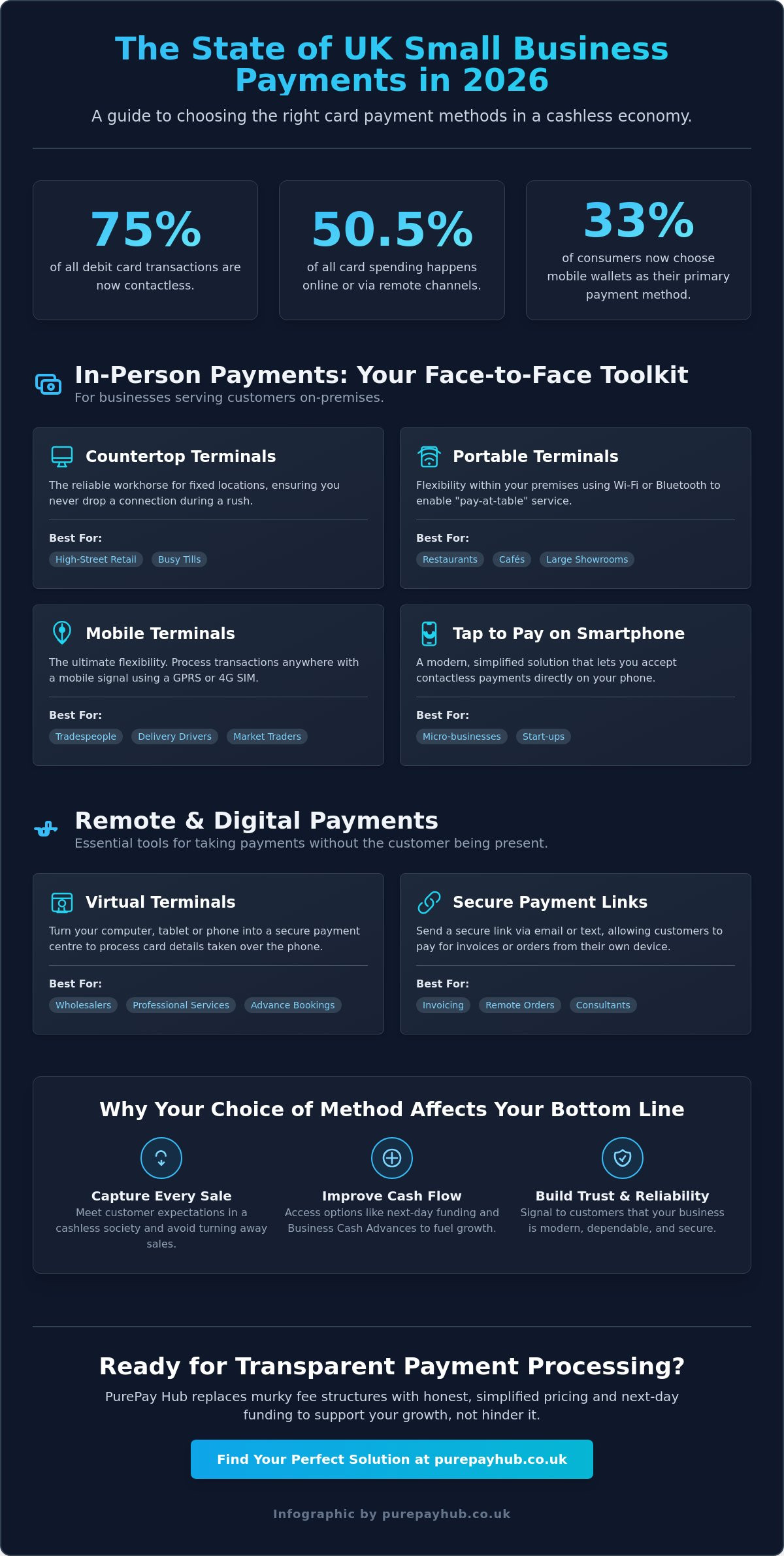

Understanding What is Apple Pay is the first step toward modernising your checkout. It’s a mobile payment service that uses Near Field Communication (NFC) to allow secure, contactless transactions via iPhone and Apple Watch. To accept Apple Pay on card machine UK terminals is no longer a luxury for niche retailers. It’s a fundamental expectation for every merchant. By May 2026, the shift in consumer behaviour is undeniable. Digital wallets have officially overtaken physical plastic cards amongst UK shoppers as the preferred way to pay.

According to UK Finance data from March 2026, contactless payments now account for 76% of all debit card transactions. Consumers don’t want to fumble for a physical wallet or remember a four-digit code. They want to tap and go. At PurePay Hub, we see mobile wallet acceptance as a baseline requirement for business credibility. If you don’t support these methods, you’re telling your customers that your business is stuck in the past. We help you bridge that gap with transparent, transaction-based tools that keep your cash flow moving.

There’s also a common myth regarding the “Contactless Limit” that needs debunking. Whilst the FCA removed the mandatory £100 cap on March 19, 2026, many traditional banks still enforce this limit for physical cards to mitigate risk. Apple Pay is different. Because it uses biometric verification, such as FaceID or TouchID, it allows your customers to authorise high-value transactions well over £100. This makes it a powerful tool for luxury retail, electronics, and hospitality businesses where average transaction values often exceed the standard contactless ceiling.

The evolution of UK payment behaviour

The UK’s transition toward a cashless society has moved at a record pace over the last three years. Gen Z and Millennial customers are particularly decisive about where they spend their money. Research shows these demographics will often abandon a basket or leave a restaurant if mobile payment options aren’t available. They value friction-free speed. Features like “Express Mode” have also transformed quick-service retail and transport. This allows customers to accept Apple Pay on card machine UK readers without even waking their device or using biometrics, making the queue move faster than ever before.

NFC technology: The silent engine of your checkout

NFC technology operates on a specific 13.56 MHz frequency to create a secure, wireless connection. It’s the technical “handshake” that powers every tap. Near Field Communication (NFC) is the short-range wireless link between a device and a card machine. This modern standard is significantly more reliable than the magnetic stripes or early chip-and-pin systems used in previous decades. It reduces physical wear on your hardware and ensures a more stable connection during your busiest trading periods. By using NFC, you ensure that every transaction is processed with the highest level of technical precision and speed.

How Apple Pay security protects your business

Security is often discussed from the customer’s perspective, but for a merchant, it’s about protecting your bottom line. When you choose to accept Apple Pay on card machine UK terminals, you are implementing a security layer that physical cards simply cannot match. Digital wallets move the risk away from your shop floor and onto the encrypted infrastructure of the card issuer. This shift provides a level of “Pure” protection that helps you avoid the stress of fraudulent activity and administrative headaches.

The primary mechanism here is tokenisation. When a customer taps their device, your card machine never actually “sees” or stores the real 16-digit card number. Instead, Apple replaces sensitive data with a unique Device Account Number. You can read more about this on the Official Apple Pay UK page. If your business systems were ever compromised, there would be no sensitive card data for hackers to steal. This drastically reduces the impact of potential data breaches on your business reputation.

Understanding Tokenisation

Tokenisation ensures that transaction data is both secure and transparent. By using a one-time security code for every payment, Apple Pay prevents the replay of transaction data. Your terminal handles the “token” whilst the actual financial details remain isolated. This setup simplifies your annual PCI DSS compliance reporting. Since you aren’t storing raw cardholder data, your security obligations are significantly lighter, allowing you to focus on serving your customers.

Biometrics vs. PIN: A security comparison

A four-digit PIN can be overlooked or stolen. Biometric verification through FaceID or TouchID cannot. These credentials are stored in a “Secure Enclave” on the user’s iPhone or Apple Watch, meaning the data never leaves the device. This makes “friendly fraud”, where a customer falsely claims they didn’t authorise a purchase, much harder to commit. For a merchant, this extra security layer leads to fewer disputed transactions and lower costs.

This leads to the “Merchant Liability Shift,” a crucial benefit that many providers fail to explain. Because Apple Pay transactions are verified with biometrics, they meet the requirements for Strong Customer Authentication (SCA). In most cases, this shifts the liability for fraudulent transactions from you, the merchant, back to the card issuer. You are no longer the one left out of pocket if a payment is disputed. To secure your revenue with the latest hardware, you might want to explore our range of secure card machines designed for the UK market.

Choosing the right card machine to accept Apple Pay

While some tech companies suggest you can run a professional business entirely from a smartphone, experienced UK merchants know that dedicated hardware is the backbone of reliability. To accept Apple Pay on card machine UK terminals, you need hardware that is robust, fast, and pre-configured for the latest NFC updates. Choosing the wrong device can lead to connection drops during peak trading, which frustrates your customers and stalls your cash flow. We believe in providing hardware that acts as a stabilising force for your business finances.

There are three primary categories of hardware to consider for your shop floor or mobile service:

- Countertop Card Machines: These are the gold standard for fixed retail points and busy reception desks. They use a wired Ethernet connection, ensuring maximum uptime and transaction speed.

- Portable Card Machines: Essential for hospitality, these devices use Wi-Fi or Bluetooth to take the payment directly to the customer’s table.

- Mobile Card Machines: Built for tradespeople and mobile retailers, these units use roaming GPRS or 4G SIM cards to process payments anywhere in the UK.

Hardware for the hospitality sector

In a busy restaurant or cafe, every second counts toward your table turnover. Portable units allow your staff to provide tableside service, which significantly reduces “wait-to-pay” times for your guests. When your card machine is integrated with your EPOS system, Apple Pay sales sync automatically with your kitchen and inventory. This eliminates manual entry errors and ensures your books are always accurate. We recommend specific, robust portable units that can withstand the high-traffic environment of a professional bar or bistro. Customers can easily learn How to set up Apple Pay on their own devices, but it is your hardware that ensures the “tap” is successful every time.

Retail and service-based solutions

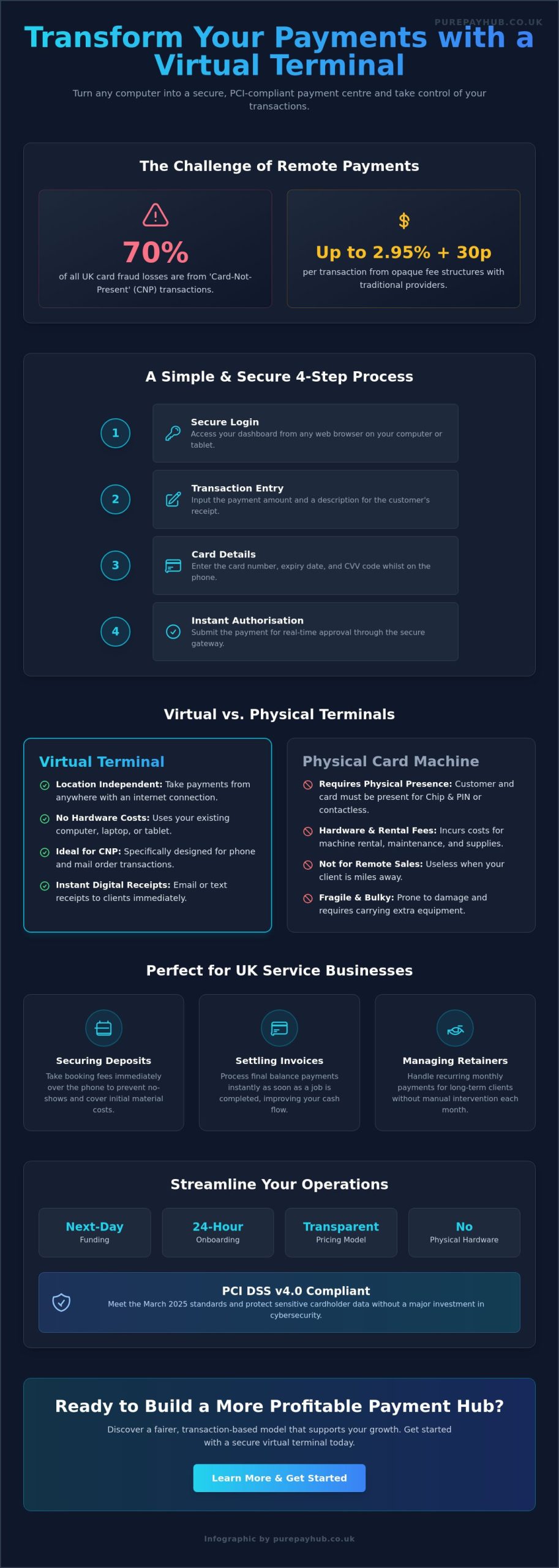

For shopfronts, countertop reliability remains unbeatable. A wired connection avoids the signal interference issues that can sometimes plague wireless networks in crowded shopping centres. If you operate a service-based business without a physical storefront, you can still accept Apple Pay on card machine UK systems via digital alternatives. Virtual Terminals and Payment Links allow you to send a secure request to your customer, which they can then settle using Apple Pay on their own device. This is a “Pure” way to handle remote billing without the need for physical contact. Whether you use a physical countertop unit or a digital link, a clear display is vital. Informative prompts build customer confidence and ensure the transaction is completed quickly and honestly.

Optimising your transaction costs and cash flow

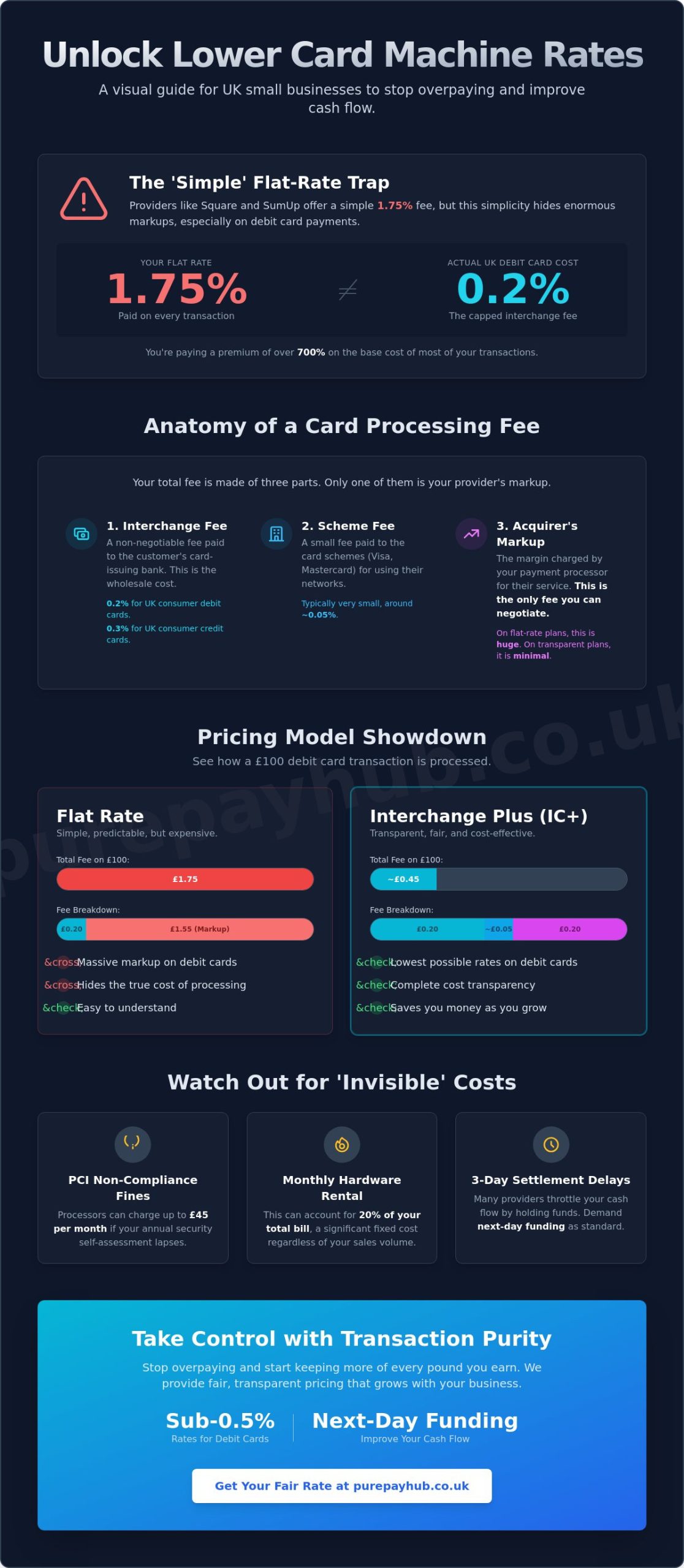

You shouldn’t be penalised for your success. When you accept Apple Pay on card machine UK setups, you want to see that money in your bank account, not swallowed by opaque fee structures. Traditional aggregators often lure small businesses with the promise of “simple” flat rates. However, for established UK merchants, these flat fees often hide a significant markup that drains your monthly revenue. Choosing a partner that prioritises purity in their pricing ensures you keep more of every pound you earn.

The Merchant Service Charge (MSC) is the core fee you pay for every transaction. It’s usually split between debit and credit rates. Because Apple Pay transactions are processed at the same rate as standard contactless payments, you can significantly lower your overheads by moving away from flat-fee models. We also help you avoid common traps like monthly minimum service charges, PCI non-compliance fines, and unnecessary statement fees that traditional banks often slip into their contracts.

The true cost of “Simple” flat rates

Let’s look at the numbers. While a flat rate of 1.75% from providers like Square or Zettle seems convenient, it doesn’t reflect the actual cost of processing for a growing business. Most UK debit card transactions have a much lower interchange cost. By switching to a transaction-based model, you reward your own growth. Here is how a £1,000 transaction compares:

- Aggregator Flat Rate (1.75%): £17.50 fee

- PurePay Hub Debit Rate (0.3%): £3.00 fee

- Your Monthly Saving: £14.50 per £1,000 processed

This transparency is what we call “Pure” processing. Seasonal businesses especially benefit from this structure because you aren’t tied down by fixed monthly costs during quieter trading months. You only pay for what you process, ensuring your costs always align with your actual income.

Accelerating your access to capital

Speed of payment is just as vital as the cost. Waiting 3-5 working days for your funds to clear is an outdated banking practice that harms your cash flow. We provide next-day funding, ensuring your Apple Pay takings are available to use almost immediately. This liquidity allows you to restock inventory or pay staff without delay, keeping your business agile.

If you’re looking to scale, your digital sales history is a powerful asset. Through our Business Cash Advance service, you can secure unsecured growth capital based on your future card takings. Everything is managed through the central “Hub,” giving you real-time reporting to monitor your finances with total clarity. If you’re ready to stop overpaying and start growing, get a transparent quote for your card processing today.

How to switch and start accepting Apple Pay today

Switching your payment provider doesn’t have to be a source of stress. We’ve simplified the transition to ensure you can accept Apple Pay on card machine UK terminals without the technical headaches or hidden costs of traditional banking. Our goal is to move you from frustration to informed confidence. By following a clear, four-step path, you can modernise your checkout whilst protecting your hard-earned revenue.

- Step 1: Conduct a rate review. Send us your recent merchant statements. We will identify every hidden markup and show you exactly how much you can save by switching to our transaction-based model.

- Step 2: Select your “Pure” hardware. Whether you need a fixed Countertop unit for a reception desk or a Portable device for tableside service, choose the hardware that fits your specific workflow.

- Step 3: Complete digital onboarding. Our UK-based support team handles the heavy lifting. We guide you through the setup process to ensure your account is verified and ready for action.

- Step 4: Plug in and play. Your new card machine arrives pre-configured for Apple Pay. There’s no complex coding required. You simply connect to your network and start trading.

The PurePay Hub onboarding experience

We act as your dedicated “Merchant Ally” throughout the entire process. Our team understands that peak trading hours are not the time for technical glitches. That’s why we ensure your hardware is fully tested before it reaches your door. Training your staff is also straightforward. Because Apple Pay transactions are authenticated on the customer’s device, your team only needs to enter the amount and prompt the tap. If a rare issue does occur, our UK-based experts are just a phone call away. You don’t have to navigate an automated menu to find a human who understands your business needs.

Ready to modernise your checkout?

The benefits of a modern payment hub are clear. You gain faster checkout speeds, superior biometric security, and significant cost savings on every transaction. Many merchants worry about exit fees from their current provider. We can often help you navigate these costs to make the switch as smooth as possible. Don’t let opaque contracts hold your business back from the future of payments. It is time to embrace a fairer, more transparent way of working. Organise a transparent rate review and upgrade your card machine today.

Secure your growth with a fairer payment partnership

The shift toward a digital-first economy is now complete. Since 76% of all UK debit transactions are now contactless, your ability to accept Apple Pay on card machine UK terminals is the key to maintaining customer trust in 2026. You’ve seen how biometric verification shifts liability away from your business and how dedicated hardware ensures reliability during your busiest hours. It’s time to move past the opaque fee structures and high flat-rates that have held local merchants back for too long.

Choosing a Pure approach means choosing total clarity for your finances. We provide debit card rates from 0.3% and credit from 0.5%, alongside next-day funding as standard to keep your cash flow moving. There are no hidden markups or confusing statement fees; just honest, transaction-based processing designed for your specific needs. Switch to a PurePay Hub card machine and accept Apple Pay with rates from 0.3% today. We’re ready to act as your merchant ally and help you build a more profitable, secure future.

Frequently Asked Questions

Does it cost more for a business to accept Apple Pay than a standard card?

No, merchants aren’t charged any additional fees by Apple for accepting these payments. Every transaction is processed at the same rate as a standard contactless card payment. If you use a transparent, transaction-based pricing model, you’ll benefit from the same fair rates you receive for physical debit and credit cards.

Is there a limit on how much a customer can pay with Apple Pay in the UK?

There is no fixed transaction limit for Apple Pay in the UK. Unlike physical cards, which often still adhere to a £100 cap despite the March 2026 FCA regulation changes, Apple Pay uses biometric authentication. Face ID and Touch ID allow customers to authorise high-value purchases securely, which is a major advantage for luxury retail and hospitality sectors.

Do I need a specific type of merchant account to accept Apple Pay?

You don’t need a specialised account to accept Apple Pay on card machine UK terminals. A standard merchant account paired with NFC-enabled hardware is all that’s required. Most modern payment hubs include this capability as a baseline feature to ensure you can meet the expectations of the 76% of UK shoppers who prefer contactless methods.

How long does it take for Apple Pay funds to reach my business bank account?

Settlement times depend entirely on your merchant service provider. Whilst traditional banks may still take 3-5 working days to clear funds, we offer next-day funding as standard for all UK merchants. This ensures that your digital takings are available to support your business growth almost immediately after the transaction is completed.

Will Apple Pay work on my old card machine if it already does contactless?

Yes, if your current machine is NFC-compatible and already accepts contactless cards, it should support Apple Pay. However, older hardware might lack the processing speed or latest security updates required for seamless high-value transactions. Upgrading to a modern, robust unit ensures your checkout remains fast and dependable during peak trading periods.

What should I do if an Apple Pay transaction is declined?

You should treat a declined Apple Pay transaction exactly like a failed physical card payment. First, ensure the customer has a valid card selected in their digital wallet and a stable data connection. If the terminal continues to decline the tap, ask the customer to use a physical card or an alternative payment method to complete the sale.

Can I accept Apple Pay for phone or mail-order transactions?

You cannot accept Apple Pay on card machine UK terminals directly over a phone call because the customer’s device must be physically near the NFC reader. To accept it remotely, you should use Payment Links. This allows you to send a secure URL to the customer, who can then settle the invoice using Apple Pay on their own device.

Is Apple Pay safer for my business than physical chip-and-pin cards?

Yes, Apple Pay is significantly more secure due to tokenisation and biometric verification. Because your card machine never stores the actual card numbers, the risk of a data breach is virtually eliminated. These transactions also meet Strong Customer Authentication (SCA) requirements, which shifts the liability for fraudulent chargebacks away from your business and back to the card issuer.