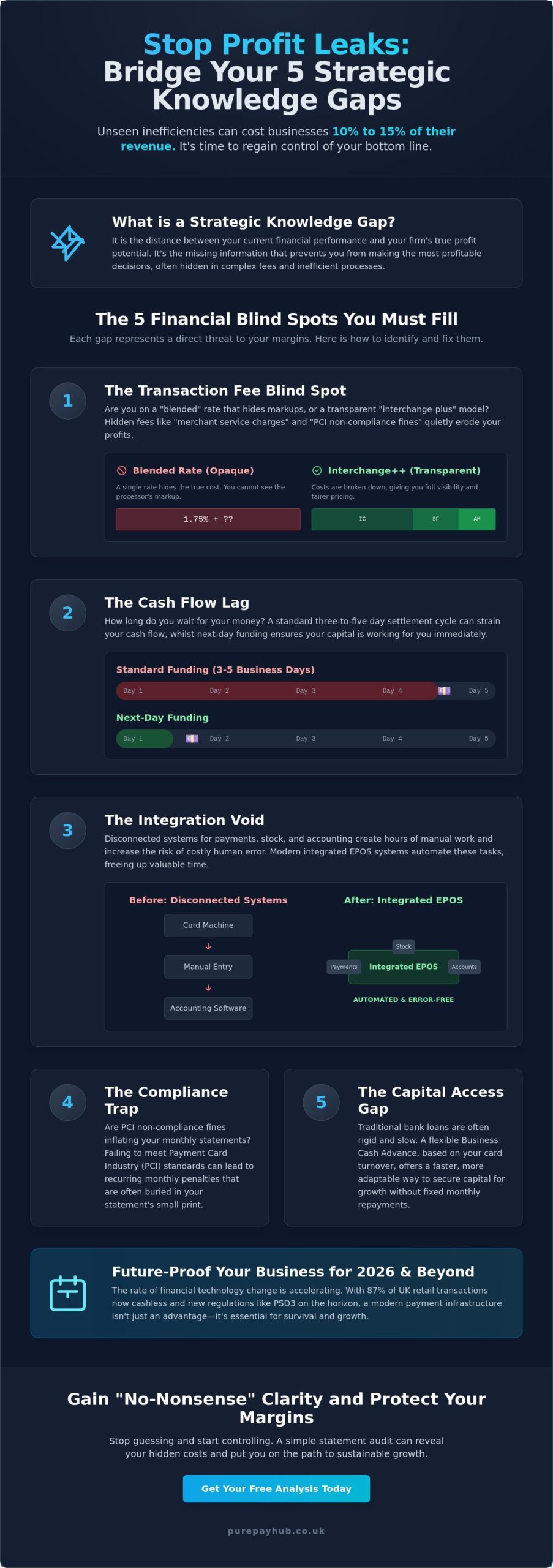

Businesses that lack clear visibility into their profit margins by product or customer can lose approximately 10% to 15% of their revenue. It’s a staggering figure, yet many regional business owners still struggle with opaque financial terminology and rising operational costs that feel out of their control. You might often feel like your competitors have access to better rates or more advanced tools. Here are 5 strategic knowledge gaps you can fill to stop the profit leaks and regain control over your bottom line.

We understand the frustration of seeing your hard-earned margins squeezed by hidden markups and complex fee structures. It’s exhausting to manage daily operations whilst wondering if your payment infrastructure is actually working against you. PurePay Hub is here to act as your supportive business ally, showing you how to identify these critical blind spots to protect your margins and accelerate your business growth. We will explore clear, actionable areas for improvement, from mastering your transaction data to preparing for 2026 payment regulations, ensuring your cash flow remains steady and your overheads stay low. By the end of this guide, you will have a transparent roadmap to move from financial uncertainty toward a state of informed confidence.

Key Takeaways

- Understand that a strategic knowledge gap is the distance between your current financial performance and your business’s actual profit potential.

- Here are 5 strategic knowledge gaps you can fill to protect your margins, focusing on invisible fee structures and cash flow inefficiencies.

- Learn how to conduct a rigorous Statement Audit to identify hidden costs and evaluate your Funding Velocity to ensure quicker access to your capital.

- Discover how modern payment infrastructure, such as integrated EPOS Systems, can automate manual processes and reclaim lost time.

- Find out how to align with a supportive partner to gain the “no-nonsense” clarity required for long-term, sustainable business growth.

What is a Strategic Knowledge Gap in a Business Context?

In simple terms, a strategic knowledge gap represents the distance between your company’s current financial performance and its true profit potential. Whilst many owners focus on increasing sales, they often overlook the internal inefficiencies that quietly drain their bank accounts. What is a Strategic Knowledge Gap in a Business Context? It is essentially the missing information that prevents you from making the most profitable decisions for your firm’s future. Here are 5 strategic knowledge gaps you can fill to transform your business from a reactive operation into a proactive market leader.

These gaps often remain invisible because you’re busy with the daily grind of serving customers and managing staff. Traditional banking institutions often thrive on this lack of clarity, using complex jargon to hide the true cost of their services. It’s vital to distinguish between “soft skill” gaps, like leadership styles, and “strategic financial” gaps that directly impact your margins. A soft skill gap might slow down a meeting; a financial knowledge gap can cost you thousands in unnecessary transaction fees every single month.

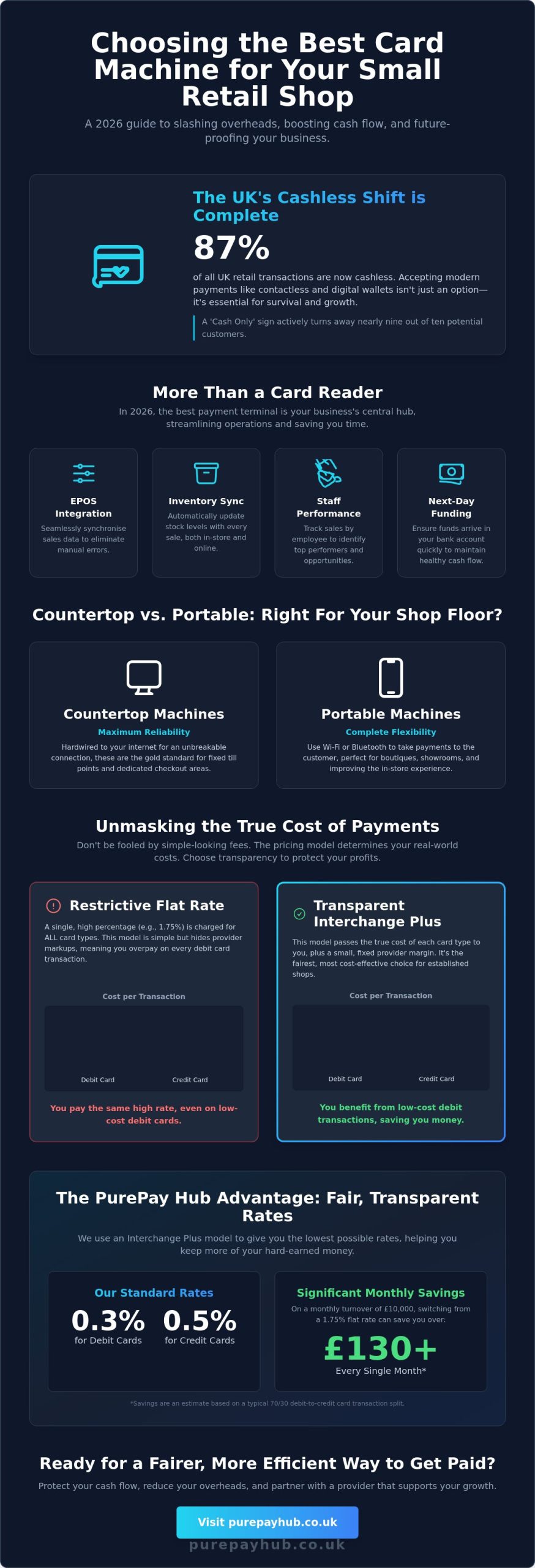

As of June 2026, the “half-life” of financial technology knowledge is shorter than ever. With 87% of UK retail transactions now being cashless, what worked in 2024 is likely obsolete today. New regulations like PSD3 and the mandatory shift to structured payment addresses mean that yesterday’s “good enough” setup is now a liability. Staying stagnant isn’t just a choice; it’s a risk to your business’s survival.

The Cost of “Not Knowing” in the UK Market

Unaddressed knowledge gaps lead to a significant loss of competitiveness amongst UK SMEs. When you don’t understand the true mechanics of your overheads, you cannot price your services effectively or negotiate better terms with suppliers. Honesty in auditing your own level of expertise is the first step toward building better vendor partnerships. A strategic knowledge gap is a measurable barrier to revenue growth.

Why Traditional “Team Training” Isn’t the Only Answer

Not every gap requires a classroom or a seminar. In the modern fintech world, some gaps are best filled by better systems rather than just more training. We call this “systemic knowledge,” where your hardware, such as advanced EPOS Systems, does the heavy lifting for you. This creates a bridge between your internal expertise and external strategic awareness, allowing you to focus on growth whilst your infrastructure manages the technicalities of payment processing and cash flow security.

The 5 Strategic Knowledge Gaps You Must Fill to Scale

Scaling a business isn’t just about hiring more people or increasing your marketing budget. It’s about fixing the leaks in your bucket before you pour more water in. Here are 5 strategic knowledge gaps you can fill to ensure your infrastructure supports your growth rather than hindering it. These aren’t HR issues; they are financial blind spots that directly affect your bottom line. Learning How to Identify Your Business’s Financial Blind Spots often starts with looking at your outgoing payments and incoming settlements.

- The Transaction Fee Blind Spot: Understanding if you are on a “blended” rate or an “interchange-plus” model.

- The Cash Flow Lag: Knowing how next-day funding compares to standard three-to-five day cycles.

- The Integration Void: Recognising the cost of non-integrated systems in terms of staff labour and manual entry errors.

- The Compliance Trap: Identifying the impact of PCI non-compliance fines that quietly inflate your monthly statements.

- The Capital Access Gap: Differentiating between rigid bank loans and flexible Business Cash Advances.

Deep Dive: The Transaction Fee Blind Spot

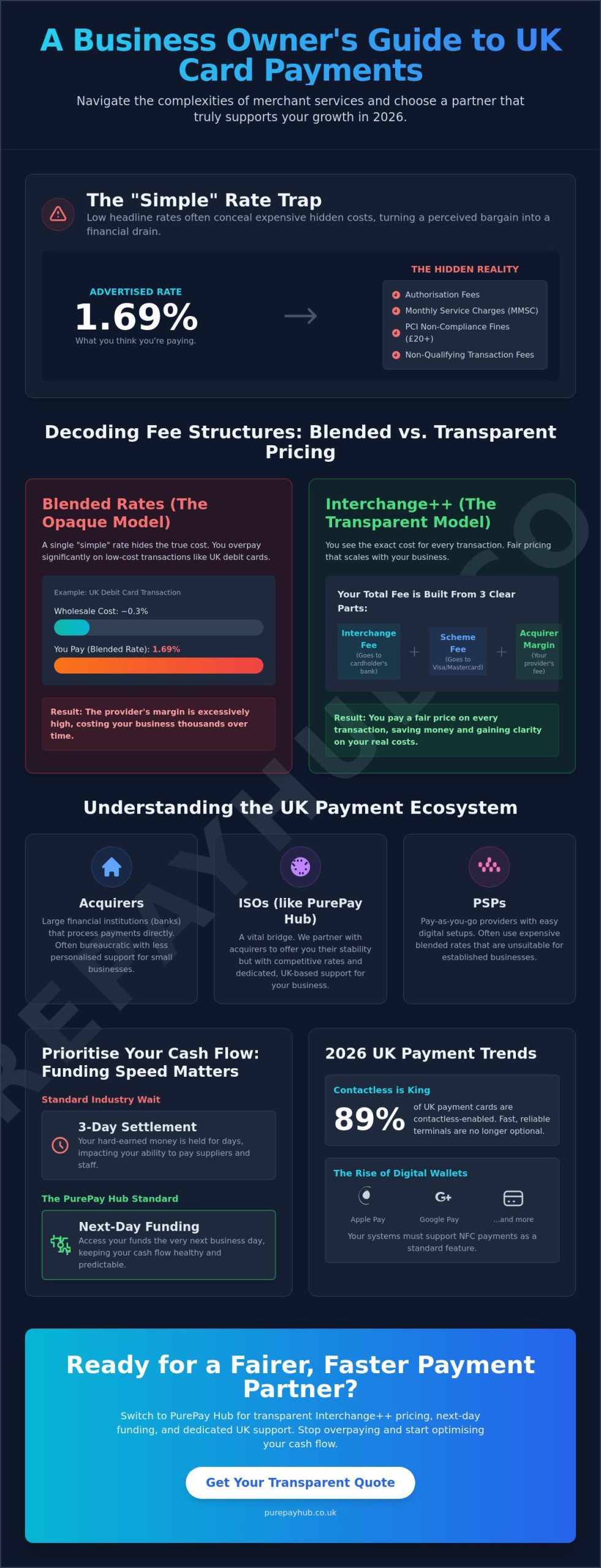

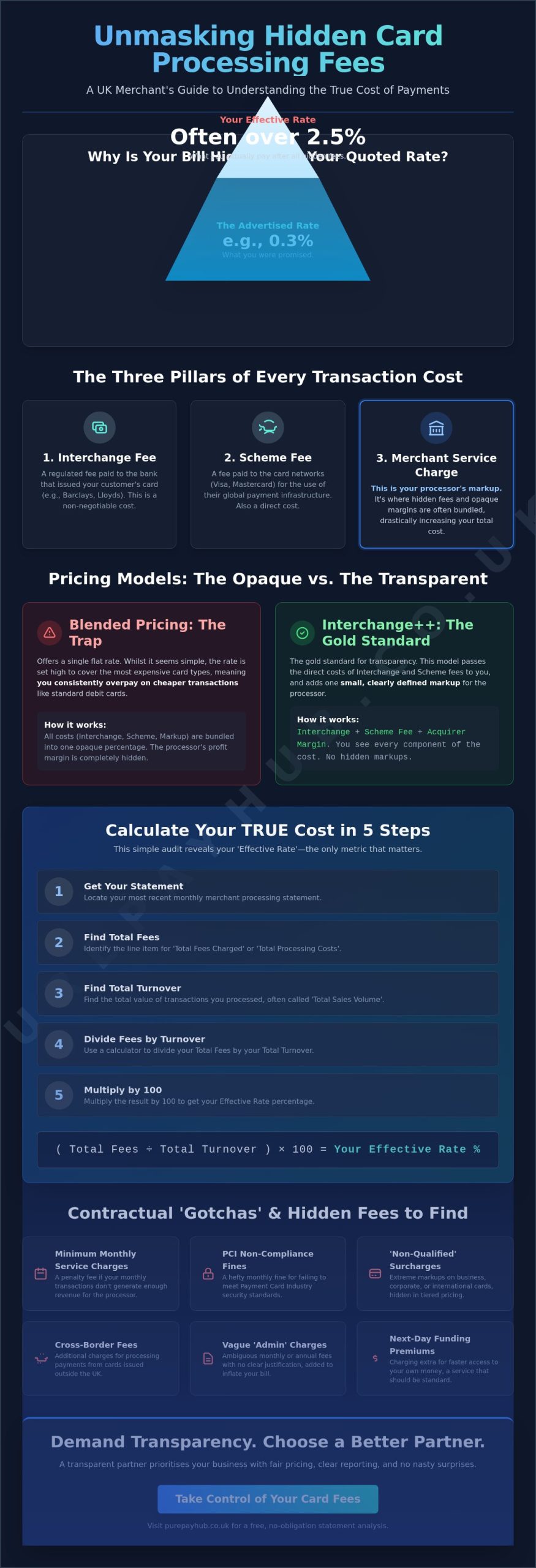

Hidden markups are the enemy of profit. A headline rate of 0.3% for debit cards sounds excellent. However, this can be undermined by “merchant service charges” and “minimum monthly fees” tucked away in the small print. Transparent pricing is a strategic advantage because it allows you to forecast your costs with total precision. To find the truth, grab your latest statement and look for these items:

- PCI Non-Compliance fees (usually around £30 per month).

- Minimum Monthly Service Charge (MMSC).

- Authorisation fees hidden inside a “blended” rate.

Deep Dive: The Integration Void

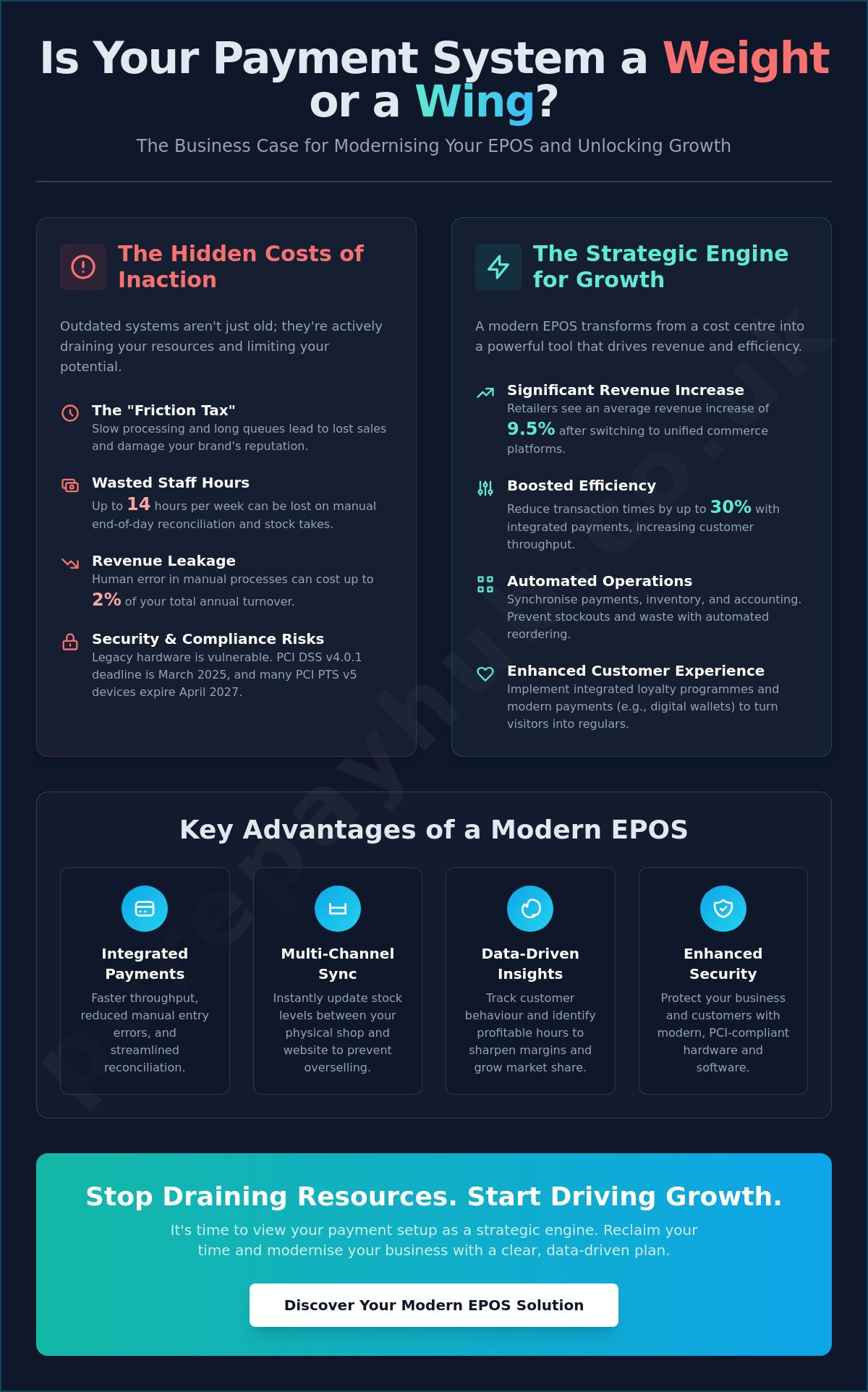

In a busy UK hospitality environment, manual entry is a recipe for disaster. It leads to “leakage” where staff enter the wrong amount or forget to record a sale entirely. Integrated EPOS Systems ensure your till and card terminal speak the same language. This setup reduces errors and speeds up the checkout process. It turns a clunky manual task into a seamless experience for both your team and your customers. Filling this gap doesn’t just save money; it saves time and reduces staff stress during peak hours. When your hardware does the thinking, your team can focus on service.

How to Identify Your Business’s Financial Blind Spots

Identification is the first step toward recovery. You can’t fix what you haven’t measured. Here are 5 strategic knowledge gaps you can fill by starting with a rigorous look at your current financial setup. Most business owners avoid their merchant statements because they’re intentionally designed to be confusing. It’s time to cut through the noise and look at the hard data. You need to know exactly where your money is going before it ever reaches your business account.

Start with a Statement Audit. Open your last three statements and look past the headline rate. Are you paying “minimum monthly service charges” or “non-compliance fees”? These are often avoidable costs that traditional banks hope you won’t notice. Next, evaluate your Funding Velocity. Check your bank records to see how long it takes for your card takings to clear. If your money takes three to five days to arrive, your provider is holding onto your capital whilst you wait to pay suppliers. In 2026, next-day funding should be your baseline for healthy cash flow management.

Assess your Hardware Friction by observing your staff during peak hours. Do they have to restart the terminal frequently? Does the battery on your Portable Card Machine die mid-shift? This friction costs you customer goodwill and reduces your total turnover. Finally, review your Compliance Health. If you see a £30 “PCI fee” on your statement every month, you’re paying a fine for a gap in your paperwork. It’s a simple fix that puts money back in your pocket immediately without requiring a single extra sale.

The 10-Minute Financial Health Check

Clarity beats corporate jargon every time. You can organise your financial priorities by looking at your costs objectively. Compare your current credit card processing rate, which might be as high as 1.5%, against the 0.5% industry standard for credit cards. If there’s a 1% difference, you’re essentially giving away a portion of your margin for no reason. This check isn’t about being an accountant; it’s about being a disciplined owner who values transparency and fairness.

Analysing Customer Behaviour and Payment Preferences

Your customers’ habits have changed rapidly over the last two years. If you don’t offer Payment Links for remote orders or Virtual Terminals for phone payments, you’re creating a barrier to sale. Failing to support favourite methods like NFC or digital wallets is a significant knowledge gap that directly affects your conversion rates. Modern customers expect a frictionless checkout experience that matches their digital lifestyle. Meeting these expectations is a strategic necessity. If your current setup doesn’t support these tools, you’re likely losing sales to competitors who have already modernised their payment infrastructure.

Closing the Gap: Implementing Modern Payment Infrastructure

Technology isn’t just a tool; it’s a bridge. Some industry voices suggest that closing skills gaps is an impossible task that requires years of intensive training. We disagree. Here are 5 strategic knowledge gaps you can fill simply by upgrading the infrastructure that handles your daily transactions. By moving from manual entry to automated systems, you eliminate the human error that leads to financial blind spots. Modern fintech solutions allow your hardware to do the heavy lifting, ensuring your data remains accurate and your margins stay protected.

Cash flow is the lifeblood of any UK business. If you are currently waiting several days for your funds to clear, you have a systemic gap in your liquidity that is entirely avoidable. Switching to a provider that offers next-day access to funds solves this problem instantly. It allows you to pay suppliers promptly and manage your stock levels with greater agility. This isn’t just a convenience; it is a strategic move that keeps your capital working for you rather than sitting in a bank’s clearing system.

Expansion also requires mobility. Portable Card Machines and Mobile Card Machines allow your staff to take payments at the table, on the shop floor, or even on the road. This expands your service area without the need for fixed, expensive infrastructure. It turns every customer interaction into a potential point of sale, ensuring you never miss a transaction due to technical limitations.

The Power of Integrated EPOS Systems

Integrated systems centre all your business data in one place. In the retail and hospitality sectors, this means your inventory levels, staff performance, and sales data are always in sync. You no longer need to guess which products are your most profitable or which hours are your busiest. This efficiency gain allows you to make decisions based on real-time facts rather than gut feeling. Next-day funding should be a standard expectation in this environment. It’s a foundational requirement for any modern, competitive business that values its time as much as its profit.

Leveraging Business Cash Advances for Growth

Traditional high-street bank loans often come with murky structures and rigid monthly repayments. This can be dangerous for seasonal businesses that experience fluctuating turnover. A Business Cash Advance offers a fairer, more transparent alternative. You receive unsecured capital up-front and repay it through a fixed percentage of your daily card sales. This means if you have a quiet day, your repayment is naturally smaller. It’s a disciplined way to bridge seasonal gaps or fund a new project without the stress of fixed debt obligations hanging over your head.

Ready to modernise your setup? Get started with PurePay Hub today to fill your strategic gaps with transparent, reliable payment solutions.

How PurePay Hub Bridges Your Strategic Knowledge Gaps

PurePay Hub acts as the bridge between your current financial frustration and future clarity. We provide the no-nonsense partnership that regional business owners have been missing for far too long. Identifying a problem is the first step, but solving it requires the right tools and a partner who advocates for your success. Here are 5 strategic knowledge gaps you can fill by aligning with a provider that values transparency as much as you do. We aim to move you from a state of uncertainty to being fully operational with a modern setup within a matter of days.

Our approach centres on fairness and discipline. We believe that a 0.3% debit rate and a 0.5% credit rate should be the benchmark for a “filled” fee gap. Unlike traditional institutions that hide behind complex terminology, we prioritise your bottom line. We also provide dedicated merchant account management to ensure your business stays on top of PCI compliance. This active support prevents those avoidable monthly fines from creeping back into your statements, allowing you to focus on growth whilst we manage the technicalities of security.

The transition process is designed for speed and simplicity because we know you don’t have weeks to wait for new hardware. Our onboarding is streamlined to get your new EPOS Systems or card terminals running quickly. Once you are live, our team takes over the heavy lifting of compliance and transaction routing. This provides a stabilising force for your finances, turning your payment infrastructure into a reliable engine for development rather than a source of stress.

Transparent Rates, No Hidden Markups

Trust is built through honesty and clear communication. PurePay Hub is proud to be untainted by hidden markups, providing you with monthly reporting statements that actually make sense to a busy owner. We break down every transaction so you can see your true costs without the corporate jargon. This level of clarity allows you to reclaim your margins and reinvest in your firm’s future. Organise a free statement audit with PurePay Hub today to see exactly where your current provider is letting you down.

Your Partner in National Business Growth

We position ourselves as a supportive ally rather than a distant financial institution. Whether you need a Countertop Card Machine for a fixed till point or a Mobile Card Machine for taking payments on the move, we have the hardware to suit your specific business model. Our goal is to provide the steady promise of better, fairer service that helps you scale with confidence. Explore our card machine solutions and close your knowledge gaps to start your journey toward informed financial confidence today.

Secure Your Business Future with Financial Clarity

Identifying blind spots is only the first step toward reclaiming your profit. You now understand how a rigorous Statement Audit reveals hidden markups and how integrated EPOS systems prevent costly manual errors. Here are 5 strategic knowledge gaps you can fill to ensure your margins remain protected whilst your competitors struggle with outdated, opaque fee structures. By prioritising transparency and modern infrastructure, you turn your payment setup from a necessary cost into a powerful growth engine.

It’s time to stop the profit leaks and demand a fairer deal for your business. Switch to PurePay Hub and start saving on your card processing fees today. You’ll benefit from debit card rates starting from 0.3%, next-day access to funds, and the no-nonsense transparent pricing your firm deserves. Taking control of your financial data is the most impactful move you can make for your business this year. We’re ready to help you build a more profitable, dependable future.

Frequently Asked Questions

What exactly is a strategic knowledge gap in a small business?

It is the measurable difference between your current operational performance and your maximum profit potential. In a payment context, it’s often a lack of awareness regarding hidden processing costs or inefficient cash flow cycles that drain your margins. Here are 5 strategic knowledge gaps you can fill to bridge this distance and ensure your infrastructure supports your scaling ambitions rather than hindering them.

How can I tell if I am paying too much for my card machine processing?

You should compare your total monthly fees against your total card turnover to calculate your “effective rate”. If this percentage is significantly higher than the headline rates you were originally promised, you are likely being hit by hidden markups or minimum monthly charges. A honest statement audit is the only way to uncover these discrepancies and identify exactly where your current provider is overcharging for their services.

Can an EPOS system really help me make better strategic decisions?

Yes, because it centralises your sales, inventory, and staff data into a single source of truth. Instead of guessing your busiest hours or most profitable products, you can use real-time reporting to optimise your stock levels and staff rotas. This shift from gut feeling to data-driven management allows you to respond to market changes with informed confidence rather than reactive panic during peak periods.

Is a business cash advance better than a traditional bank loan?

It is often a fairer choice for businesses with fluctuating turnover because repayments are linked directly to your daily card sales. Unlike a bank loan with fixed monthly instalments, a Business Cash Advance adjusts to your performance; you pay less during quiet periods and more when business is booming. This flexible structure protects your liquidity without the need for traditional property-based collateral or rigid repayment schedules.

How long does it take to switch providers and get next-day funding?

The transition process is designed to be swift, typically taking just a few working days from your initial application to being fully operational. Once your account is set up and your new hardware arrives, next-day funding becomes your standard settlement cycle. This immediate improvement in your funding velocity ensures your capital is available for reinvestment almost as soon as a sale is made, keeping your cash flow steady.

What are the most common hidden fees in merchant service contracts?

You should look for “minimum monthly service charges”, “authorisation fees”, and “PCI non-compliance fines” on your statements. These costs are frequently omitted from the initial sales pitch but appear once you’ve signed the contract. Here are 5 strategic knowledge gaps you can fill by learning to identify these murky structures and switching to a provider that prioritises transparent, no-nonsense pricing models for every merchant.

How does PCI compliance affect my monthly business costs?

Failing to maintain compliance can result in a monthly fine appearing on your merchant statement, which is an avoidable overhead that quietly drains your profits. Whilst this fee is common amongst traditional providers, it’s often a sign of a lack of support. Dedicated merchant account management helps you stay compliant, ensuring you only pay for the services you actually use rather than penalties for incomplete or outdated paperwork.