The lowest headline rate on a card machine often ends up being the most expensive mistake a UK business can make. You’ve likely noticed that a “simple” flat rate rarely stays simple whilst hidden markups and non-qualifying fees clutter your monthly statement. It’s an industry built on complexity, and when you try to compare card payment providers UK, the lack of clarity often feels intentional. You want to focus on serving your community, not decoding why your hard-earned revenue is tied up for days.

We agree that you deserve better than opaque contracts and slow access to your own funds. This 2026 guide provides a transparent, data-driven framework to help you identify providers that actually prioritise your cash flow. We’ll show you how to move beyond basic percentages to find genuine Interchange++ pricing and reliable next-day funding. By examining the impact of the 2026 PSR cross-border fee caps and seeing how the PurePay Hub standard of transparency compares to traditional providers, you’ll gain the clarity needed to choose a partner that supports your growth.

Key Takeaways

- Understand the critical differences between acquirers, ISOs, and PSPs to ensure you partner with a provider that offers direct stability and support.

- Decode complex fee structures to avoid the blended rate trap and switch to transparent Interchange++ pricing that reveals your true transaction costs.

- Apply our data-driven framework to compare card payment providers UK based on your specific monthly turnover and average transaction value.

- Learn how to prioritise your cash flow by identifying providers that offer next-day funding rather than the standard three-day wait.

- Discover how PurePay Hub acts as a stabilising force for your finances through honest pricing on portable card machines and integrated EPOS systems.

Navigating the UK Card Payment Market in 2026

The days of simply plugging in a bulky terminal and waiting for a dial-up connection are over. British retail now runs on integrated ecosystems where hardware and software speak the same language. If you want to compare card payment providers UK, you must first understand that you aren’t just buying a machine; you’re choosing a financial partner. The market has shifted toward “softPOS” technologies and mobile-first solutions that allow merchants to accept payments on smartphones. This evolution makes the choice of provider more critical than ever for your daily cash flow.

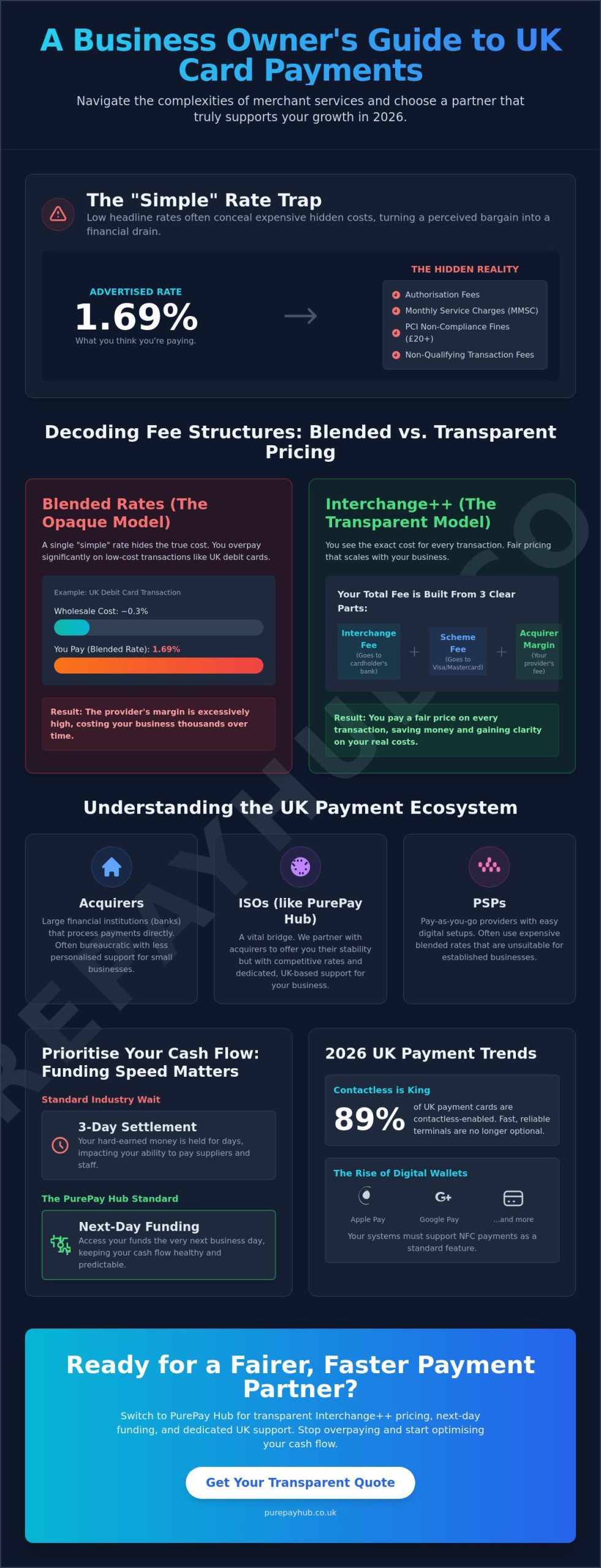

You’ll encounter three main types of players in this space. Acquirers are the massive financial institutions that actually process the money. Payment Service Providers (PSPs) offer quick, digital-only setups that are often easy to start but expensive as you grow. Then there are Independent Sales Organisations (ISOs). These entities provide the personalised service and competitive rates that big banks often ignore. Every transaction you process involves an Interchange fee, which is the baseline cost set by card schemes. A transparent provider will show you these costs clearly rather than hiding them behind a flat, “blended” rate.

The UK market is uniquely demanding. According to UK Finance data from March 2026, 89% of UK payment cards are now contactless-enabled. Consumers expect to tap and go in seconds. Meeting this demand requires hardware that is both fast and compliant with the latest PCI-DSS security regulations. Failure to keep up doesn’t just mean lost sales; it can lead to heavy non-compliance penalties that drain your revenue.

The Role of an ISO in the UK Ecosystem

ISOs like PurePay Hub act as a vital bridge between small businesses and the rigid bureaucracy of big banks. We take the raw processing power of major acquirers and refine it into a service that actually works for a local business owner. Because we handle high volumes across many merchants, we can often negotiate better rates than a single business going direct to a bank. You get the stability of a major financial institution paired with the dedicated, UK-based support of a partner who knows your name. It’s a way to bypass corporate jargon and get straight to the fair pricing your business deserves.

Current Payment Trends: Contactless and Digital Wallets

Digital wallets have moved from a novelty to a necessity. Apple Pay and Google Pay now dominate consumer behaviour, especially amongst younger demographics. Your Countertop Card Machine or Portable Card Machine must support Near Field Communication (NFC) as a standard feature. Looking ahead, Open Banking and QR code payments are beginning to gain traction. These methods allow customers to pay directly from their bank accounts, potentially offering even lower fees for merchants in the future. Staying ahead of these trends ensures your business remains accessible to every type of shopper.

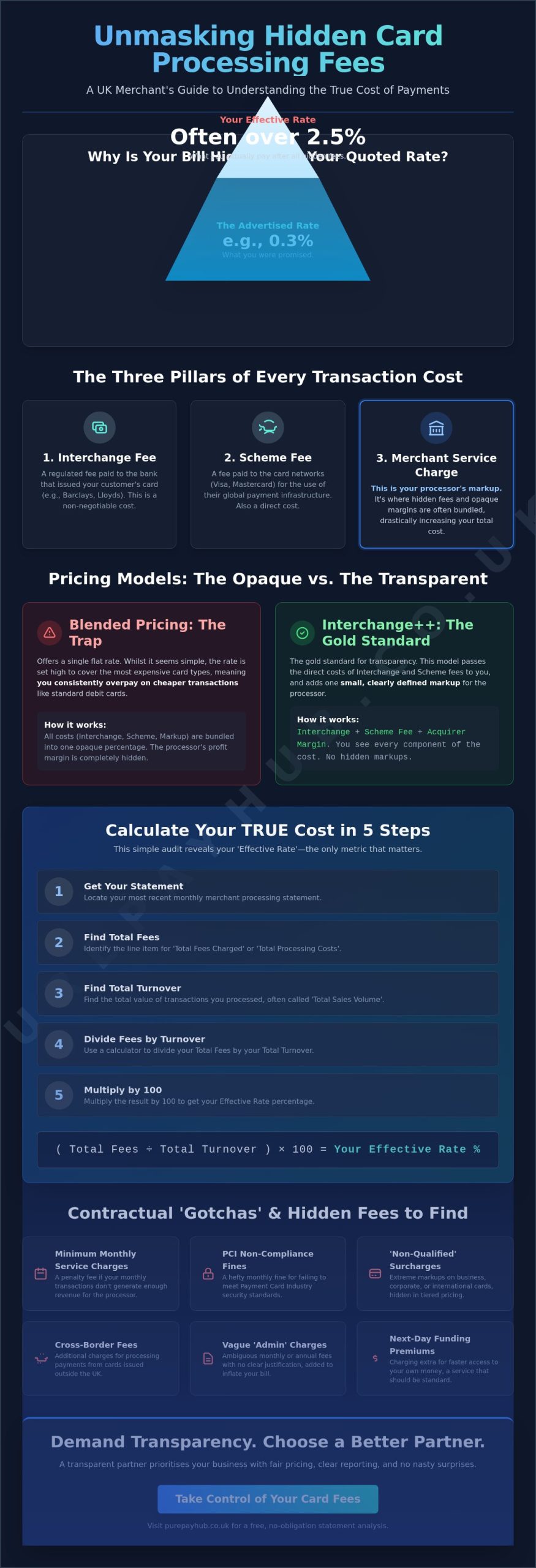

Decoding Fee Structures: Interchange++ vs. Blended Rates

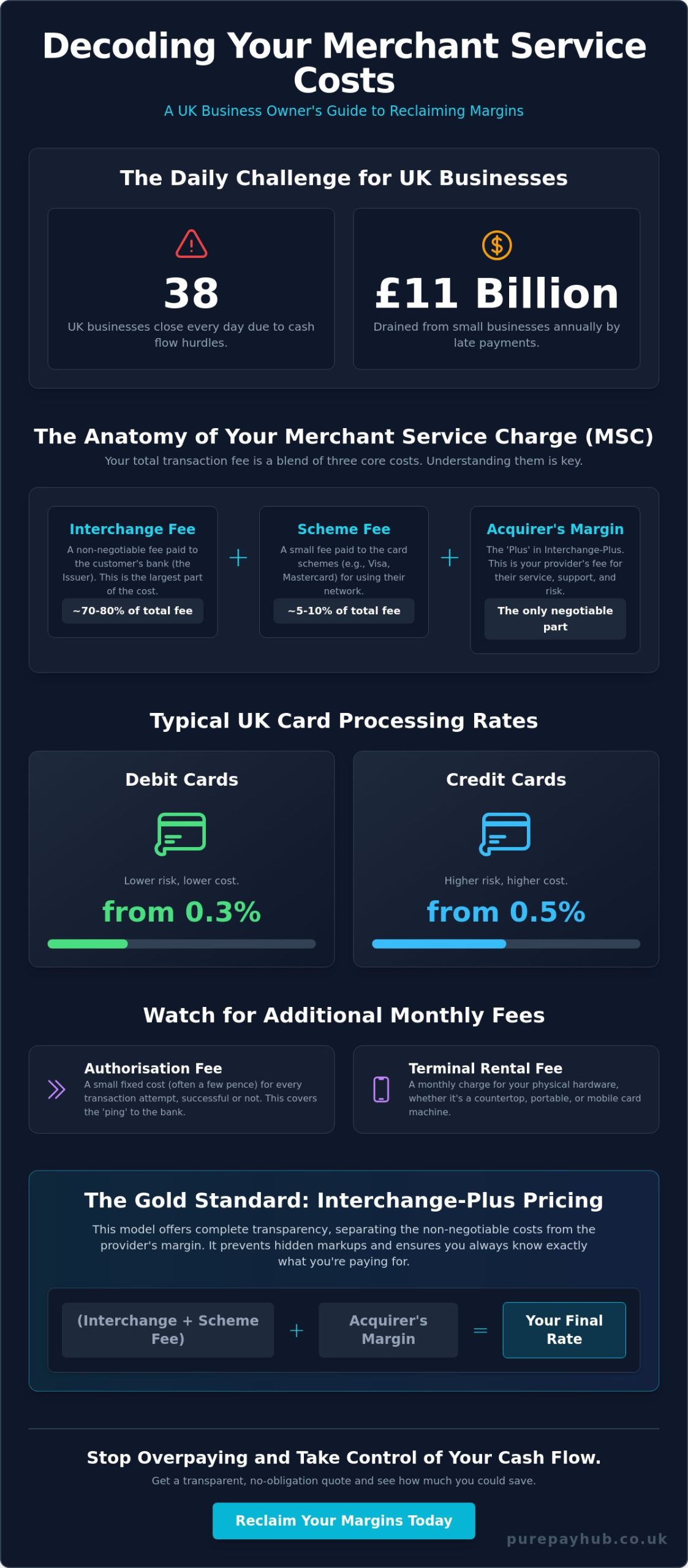

Headline rates are often smoke and mirrors in the merchant services industry. To truly compare card payment providers UK, you must look at what’s under the bonnet. Every transaction fee is a cocktail of three distinct ingredients. First is the interchange fee, which is the wholesale cost paid to the card-issuing bank. Second is the scheme fee, which goes to networks like Visa or Mastercard. Finally, there’s the acquirer margin, which is the only part your provider actually keeps as profit. The Payment Systems Regulator (PSR) oversees these structures to keep the market competitive, yet many providers still find ways to mask their true margins behind “simple” pricing.

Beyond the basic percentage, you must watch for hidden extras that drain your daily revenue. Many providers sneak in authorisation fees for every transaction attempt, regardless of whether it’s successful. You might also encounter a Minimum Monthly Service Charge (MMSC) if your turnover dips during a quiet month. Perhaps the most frustrating are PCI non-compliance fines, which can add £20 or £30 to your bill simply for missing a paperwork deadline. Choosing a partner that offers a transparent merchant account ensures these murky costs don’t eat into your hard-earned profits.

Why Blended Rates Can Cost You Thousands

Pay-as-you-go (PAYG) providers favour blended rates because they’re easy to market. You pay a flat 1.5% to 1.75% regardless of the card type used. This sounds convenient, but it’s often a trap for established businesses. Most domestic debit card transactions have a wholesale cost far below 0.5%. By charging you a flat 1.5%, the provider pockets the massive difference as pure profit. They use your high-volume debit sales to subsidise expensive premium or corporate cards that your customers might only use occasionally. Blended rates prioritise simplicity over actual cost efficiency.

The Transparency of Interchange++

Interchange++ is the gold standard for honest merchant services. This model separates the three cost components on your monthly statement, passing the wholesale savings directly to your business. You pay the exact interchange and scheme fees plus a small, fixed margin. This level of clarity is why growing UK businesses prefer this model for long-term stability. Reading your statement becomes a straightforward task because you can see exactly where every penny goes. You won’t find yourself paying an inflated “one-size-fits-all” margin that doesn’t reflect your actual transaction behaviour.

Provider Comparison: PAYG vs. Traditional Merchant Accounts

Deciding between a Pay-As-You-Go (PAYG) provider and a traditional merchant account is a major step for any British business. PAYG models appeal to seasonal traders or those with infrequent sales because they lack monthly overheads. However, they charge a premium for this lack of commitment. To compare card payment providers UK effectively, you have to look past the instant setup and assess the true cost of convenience. Once your sales volume stabilises, the high flat rates of basic readers often become a significant drain on your margins.

Traditional merchant accounts represent the professional standard for businesses processing over £5,000 each month. These accounts provide much lower transaction rates and more durable hardware, such as a Countertop Card Machine or a Portable Card Machine. While they involve a monthly fee, the savings on every tap and insert usually far outweigh the fixed cost. These professional setups offer seamless connectivity with your EPOS Systems and accounting software; this keeps your back-office tasks as streamlined as your customer service. You gain a level of operational stability that basic app-based readers simply cannot match.

The Tipping Point: When to Switch from PAYG

The transition to a managed merchant account usually makes sense at the £5,000 monthly turnover mark. At this level, the flat 1.75% fee common with app-based readers begins to undercut your growth. A managed account gives you access to wholesale rates that reflect your specific business profile. Additionally, PAYG hardware often struggles with the processing speed and battery life required in a high-pressure hospitality or retail setting. We’ve helped local shops cut their total processing costs by 40% by moving to a transparent account that rewards their success rather than penalising their volume.

Hardware Options: Countertop, Portable, and Mobile

Your hardware should match your service style. Selecting the right tool ensures a smooth customer experience and reliable uptime:

- Countertop Card Machine: The fixed retail workhorse. It stays at the till and uses a stable internet connection for total reliability.

- Portable Card Machine: Uses Bluetooth or Wi-Fi to reach customers. It’s the favourite for tableside service in cafes and restaurants.

- Mobile Card Machine: Uses GPRS or 4G networks via a roaming SIM. It’s vital for couriers, tradespeople, and outdoor events across the UK.

Modern hardware does more than process payments. It acts as a stabilising force by syncing directly with your digital records. This connectivity removes manual errors and provides a real-time view of your daily revenue, allowing you to make informed decisions about your business growth.

The Decision Framework: How to Choose Your Provider

Choosing a partner shouldn’t feel like a gamble. You need a logical sequence to compare card payment providers UK and find a fit that actually works for your specific business model. It’s easy to get distracted by shiny hardware, but the true value lies in the operational details that impact your daily life. Use this five-step framework to filter out the noise and identify a provider that acts as a genuine business ally.

Start by auditing your current monthly volume and average transaction value. This data is your strongest negotiating tool. High-volume merchants require the transparency of Interchange++ to keep costs low, whilst those with a lower turnover might focus on minimising monthly rental fees. Next, check for hardware compatibility. If you use integrated EPOS Systems, your new Countertop Card Machine or Portable Card Machine must talk to your software without friction. Finally, review the quality of technical support. Many low-cost providers outsource their helpdesks to distant call centres. When your terminal stops working during a busy lunch service, you need reliable, UK-based support that understands the local market and can provide immediate resolutions.

- Audit your data: Know your monthly card turnover and average transaction size before you start negotiations.

- Evaluate settlement times: Determine if your cash flow can handle a three-day wait or if next-day funding is a necessity.

- Check compatibility: Ensure your payment gateway or physical terminal integrates with your current accounting and sales software.

- Scrutinise the contract: Look for short terms and avoid auto-renewal clauses that lock you in for years.

- Test the support: Prioritise providers with dedicated UK-based teams that offer direct assistance when things go wrong.

Settlement Speed: The Overlooked Metric

Traditional banking often leaves you waiting. The difference between T+1 (next-day) and T+3 (three-day) settlement can be the difference between paying a supplier on time or missing a deadline. Accessing your funds quickly is essential for maintaining a healthy cash flow. PurePay Hub facilitates faster access to your hard-earned revenue, ensuring your bank balance reflects your actual sales. Don’t let a provider hold your money hostage when modern technology allows for rapid transfers.

Contract Terms and Exit Strategies

The merchant services industry is notorious for 36-month “auto-renewal” traps that make switching nearly impossible. Scrutinise every exit clause and look for a Service Level Agreement (SLA) that guarantees high uptime and clear service standards. We recommend that merchants always request a no-obligation quote before signing any long-term agreement. Request a transparent quote for your business here.

PurePay Hub: Transparent Payments and Next-Day Funding

Finding a provider that respects your bottom line shouldn’t be a struggle. We built PurePay Hub to offer a direct alternative to the murky pricing structures used by traditional banks. When you compare card payment providers UK, you’ll find that many hide their true margins behind complex jargon. We take a different path. Our commitment to transparency ensures you see exactly what you pay for. There are no hidden markups or unexpected fees to derail your financial planning. Our identity is built on being untainted by the opaque practices that frustrate so many business owners.

Cash flow is the lifeblood of your business. Waiting three to five days for your revenue to settle is a frustration you don’t need. We provide next-day funding as a standard feature, acting as a stabilising force for your finances. Our onboarding process is designed for speed and efficiency. We aim to get your business set up and accepting payments in days rather than weeks. Whether you need a Countertop Card Machine for your shop or a Virtual Terminal for remote sales, we provide the tools to keep your revenue moving without delay.

Fair Rates for UK Small Businesses

We believe in fairness. Our Interchange++ pricing model passes wholesale savings directly to you. We offer competitive rates with debit cards starting from 0.3% and credit cards from 0.5%. These rates are tailored to your specific sector, ensuring you aren’t subsidising other industries with higher risk profiles. Your security is also a priority. Every system we provide is fully PCI-compliant and backed by 24/7 monitoring to protect your data and your customers. Our portable card machines are designed for maximum retail efficiency, allowing you to take the till to the customer without compromising on speed or reliability.

A Partner in Your Growth

We do more than just process transactions. We act as a supportive ally for your long-term development. If you need capital to expand, our Business Cash Advance provides a flexible alternative to traditional loans. Your repayments are linked directly to your card turnover; this means you pay back more when business is brisk and less during quieter periods. Our systems offer seamless EPOS integration for hospitality and retail environments, connecting your sales data with your inventory management. It is time to move away from impersonal banking and join a partnership built on clarity. Organise a transparent quote with PurePay Hub today.

Take Control of Your Merchant Services

The landscape of UK merchant services is evolving fast. You’ve seen why the “one-size-fits-all” approach of blended rates often traps growing businesses in unnecessary costs. True transparency comes from an Interchange++ model that separates wholesale costs from provider margins. It’s also clear that you shouldn’t have to wait three days to access your own hard-earned revenue. When you compare card payment providers UK, prioritise partners who offer next-day funding and dedicated UK-based support. This ensures your operations remain resilient and your cash flow stays healthy.

PurePay Hub acts as a stabilising force for your finances. We don’t believe in opaque bureaucracy or hidden markups. Instead, we offer a direct partnership built on honesty and efficiency. With debit rates from 0.3% and credit rates from 0.5%, we provide the clarity you need to scale with confidence. Don’t let slow funding or complex fee structures hold your business back any longer. You deserve a partner that values your time as much as your revenue.

Compare your current rates and save with PurePay Hub

We’re here to help you build a more profitable and predictable future for your business.

Frequently Asked Questions

How much are typical card machine fees for UK small businesses?

Typical fees consist of an interchange fee, scheme fee, and an acquirer margin. For established UK businesses, debit card rates often start from 0.3% and credit cards from 0.5% when using a transparent pricing model. You should also look for authorisation fees and Minimum Monthly Service Charges (MMSC) on your statement. These costs vary based on your sector and monthly card turnover. Always ask for a full breakdown to avoid hidden markups.

What is the difference between a card reader and a merchant account?

A card reader is the physical hardware used to tap or insert a card, whilst a merchant account is the digital facility where funds are held before being settled into your bank. Many Pay-As-You-Go providers combine these into a single service with a flat rate. Professional providers separate them to offer more transparent pricing. Having a dedicated merchant account often allows you to access lower rates as your business volume grows.

Can I get a card machine with next-day funding?

Yes, you can get a card machine with next-day funding to improve your business cash flow. Whilst many traditional banks still take three to five working days to settle funds, modern providers prioritise faster access to your revenue. This service ensures your bank balance reflects your actual sales almost immediately. It acts as a stabilising force for your finances, allowing you to pay suppliers and staff without unnecessary delays.

Are there card payment providers with no monthly fees?

Card payment providers with no monthly fees do exist, but they usually charge higher transaction rates to compensate. These models are ideal for seasonal traders or micro-businesses with low turnover. However, once you process more than £5,000 monthly, the “free” account often becomes more expensive than a professional one with a small monthly rental. It’s essential to compare card payment providers UK based on your total cost of ownership.

How long does it take to switch card payment providers?

Switching card payment providers typically takes between three to ten working days. The process involves a standard credit check and an application for a new merchant account. Once approved, your new hardware, such as a Portable Card Machine, is dispatched via courier for immediate use. Most modern providers handle the heavy lifting of the transition, ensuring your service remains active so you never miss a sale during the move.

What information do I need to provide to compare card payment quotes?

To get an accurate quote, you need to provide your annual card turnover, average transaction value, and your current merchant statements. These documents allow a provider to see exactly what you’re currently paying in interchange and scheme fees. Providing this data ensures the new quote is tailored to your specific business profile. It also helps identify hidden markups that you can eliminate to save money on your processing costs.

Is it cheaper to buy or rent a card machine terminal?

Buying a terminal upfront is often cheaper for micro-businesses, but renting is the preferred choice for established retailers. Rental models usually include inclusive software updates, hardware replacements, and technical support. This means you won’t be stuck with an obsolete Countertop Card Machine if security regulations change. Renting also spreads the cost, keeping your initial capital free for other areas of business development and growth.

What is PCI compliance and why am I being charged for it?

PCI compliance is a mandatory security standard that ensures you’re protecting your customers’ sensitive card data. Providers charge for this to cover the costs of secure processing environments and regular security monitoring. It’s a vital part of maintaining trust in the UK payment ecosystem. If you don’t complete your annual compliance self-assessment, you may be hit with non-compliance fines that significantly increase your monthly bill.