Your “simple” card payment machine might be the single biggest drain on your business’s monthly bottom line. Many providers hide behind complex jargon while taking a hefty cut of every transaction you process. It’s frustrating to watch a significant percentage of every sale vanish into opaque fee structures, only to wait three to five days for the remaining funds to actually reach your bank account. You’ve worked hard to build your business; you shouldn’t have to settle for hardware that drops its Wi-Fi connection or settlement terms that stall your growth.

We believe in a fairer, more transparent approach to merchant services. This guide will show you exactly how to secure transaction rates below 1% and unlock next-day funding, ensuring your cash flow stays as healthy as your sales figures. We’ll explore the latest hardware options for 2026, from portable card machines to full EPOS systems, while breaking down the fee models that protect your margins. By the end of this guide, you’ll have a clear roadmap to choosing a reliable payment partner that treats your business as a priority rather than a policy number.

Key Takeaways

- Identify the specific hardware that suits your business model, from fixed countertop units to a portable card payment machine for flexible service.

- Learn how to look beyond headline rental costs to secure transaction rates below 1%, shielding your profits from high flat-rate fees.

- Discover how to end the wait for your funds by moving to a provider that offers next-day settlement as standard.

- Master the process of auditing your merchant statements to expose hidden markups and navigate existing contract notice periods.

- Understand why a transparent partnership is the best defence against the opaque pricing structures common in the traditional banking sector.

What is a Card Payment Machine and Why Does Your Choice Matter?

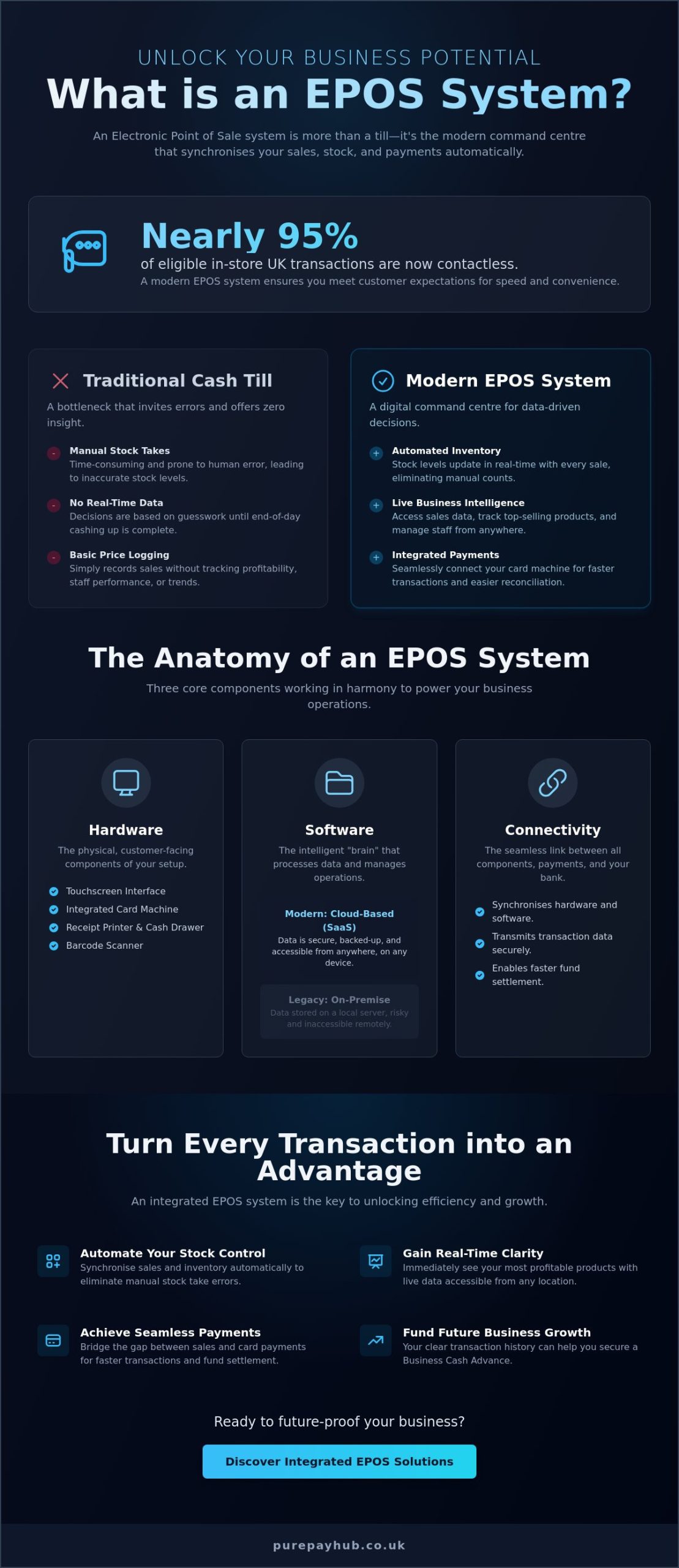

A card payment machine acts as the vital bridge between your customer’s bank account and your business balance. It’s the final, most critical link in your sales chain. Modern terminals are no longer simple card readers; they are sophisticated communication hubs. They securely process everything from traditional Chip & PIN to digital wallets like Apple Pay and Google Pay. To truly understand What is a Payment Terminal?, you must view it as a security gatekeeper that protects both your revenue and your customer’s sensitive data.

Your choice of hardware directly dictates your daily cash flow and annual profit margins. It isn’t just about the physical device on your counter. The wrong choice can result in funds being held for days or high percentage cuts on every sale that slowly erode your bottom line. The UK market has shifted significantly. We’ve moved from restrictive “rent-only” legacy models to flexible, high-tech ownership options. This shift empowers you to choose a partner that offers next-day funding and transparent rates, rather than being stuck with a distant financial institution that treats your business like a policy number.

The Shift from Cash to Contactless

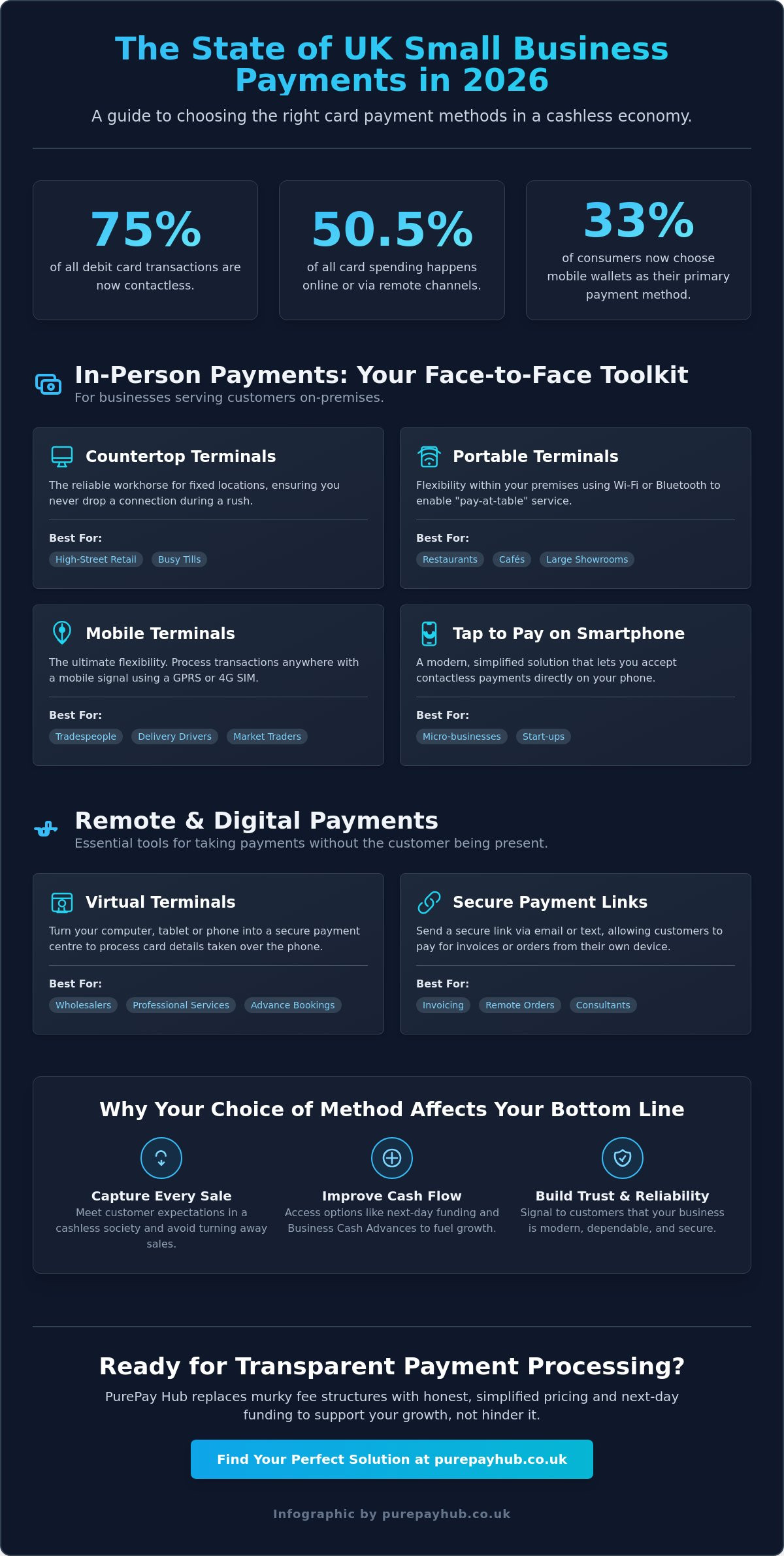

Consumer behaviour has changed permanently. The overwhelming majority of retail transactions in the UK are now card-based. “Tap to Pay” technology has removed the friction from spending, making it the preferred method for almost every demographic. Refusing card payments isn’t a viable option for a modern business. It creates a physical barrier that turns customers away. Accepting cards is about more than just convenience; it’s about legitimising your business in a digital-first economy and ensuring you never miss a sale because a customer isn’t carrying cash.

Types of Payment Technology in 2026

Selecting the right technology requires a focus on your specific operational needs. You shouldn’t pay for mobility if you don’t need it, but you shouldn’t be tethered to a desk if your business moves. Here are the primary categories for 2026:

- Traditional Countertop: These units use a fixed Ethernet connection for maximum reliability. They are the workhorses of retail centres and pharmacies where the till stays in one place and speed is paramount.

- Portable & Mobile: These use Bluetooth, Wi-Fi, or GPRS to offer total flexibility. They are the standard for table service or mobile trades, ensuring you can take payments anywhere whilst maintaining a secure connection.

- Smart Terminals: These Android-powered devices can manage inventory and sales data whilst processing payments. They bridge the gap between a simple card reader and a full EPOS system.

Hardware reliability is a major factor that many business owners overlook until it’s too late. A card payment machine that frequently drops its Wi-Fi connection causes queues, frustrated staff, and lost revenue. In a fast-paced environment, you need hardware that is as resilient as it is fast. Choosing a modern, well-supported terminal ensures your business stays online and your transactions clear without unnecessary delay.

Choosing the Right Hardware: Countertop, Portable, or Mobile?

Selecting the correct card payment machine is a decision that impacts your staff’s speed and your customer’s patience. It isn’t just about picking a sleek device; it’s about matching technology to your specific environment. Whether you operate a bustling high-street shop or a roaming food truck, your hardware must remain a silent, reliable partner in every sale. The right choice ensures that the transaction process is invisible to the customer but infallible for your business.

Countertop machines are the undisputed workhorses of retail and pharmacy centres. These units rely on a fixed Ethernet connection, which virtually eliminates the risk of terminal downtime during peak hours. When you have a queue of twenty people, you can’t afford for your Wi-Fi to flicker. These terminals integrate seamlessly with your existing cash drawer and receipt printer, creating a secure, centralised payment station that anchors your checkout process. A fairer approach to hardware ensures you aren’t overpaying for features you don’t use whilst maintaining this rock-solid reliability.

For those in hospitality, portable units are the standard. They allow you to take the till directly to the customer whilst maintaining a strong Wi-Fi connection within your premises. This mobility increases efficiency and often leads to higher tips, as the payment happens at the moment of peak satisfaction. When choosing the right credit card processing plan, consider how many roaming units you need to prevent bottlenecks at the bar during a busy Friday night shift.

If your business takes you on the road, mobile machines are the answer. These devices use built-in SIM cards to process payments anywhere in the UK with a mobile signal. They are perfect for delivery services or outdoor market stalls where traditional connectivity isn’t an option. For businesses looking for a complete solution, integrated EPOS systems combine payment processing with stock management into one clear interface, giving you a real-time view of your entire operation.

Best for Retail: Countertop Reliability

A fixed connection is the best defence against technical failure. In a retail setting, a countertop card payment machine provides a permanent, secure point of sale. Because these units don’t rely on battery power or fluctuating Wi-Fi signals, they offer the highest level of security and uptime. This stability is essential for high-volume environments where every second of downtime equals lost revenue. You can also organise your counter space more effectively by integrating these units directly with your legacy hardware.

Best for Hospitality: Portable and Roaming Units

In a restaurant or café, staff efficiency is tied to movement. Portable units allow servers to close tables without returning to a central station, which speeds up table turnover significantly. Modern portable units are designed with full-day shift usage in mind, featuring long battery lives that won’t fail during a lunch rush. Using multiple units allows you to spread the workload amongst your team, ensuring that customers never have to wait for the “only machine” to become available.

The True Cost of Card Processing: Beyond the Monthly Rental

Focusing solely on the monthly rental price of a card payment machine is a mistake that costs UK small businesses thousands of pounds every year. While a terminal might only cost between £15 and £30 per month, the real impact on your bottom line lies in the transaction rates and hidden service fees. Traditional providers often use these low headline costs to distract from high percentage cuts on every sale you process. You must look at the total cost of ownership to protect your margins and ensure your business remains profitable.

Your monthly statement consists of several layers. The most significant is the Merchant Service Charge (MSC). This includes the Interchange fee, which is a non-negotiable cost set by card schemes like Visa and Mastercard. On top of this, many providers add a substantial markup. Before you sign a payment processing contract, you should also check for “hidden” extras. These often include PCI compliance fees of £4 to £6, minimum monthly service charges (MMSC) that can reach £30, and steep exit fees if you decide to switch. These small additions quickly stack up, turning a “cheap” deal into a heavy financial burden.

The “Flat Rate” Trap vs. Merchant Accounts

Flat-rate providers often market a single transaction fee, typically around 1.75%, as a simple solution. Whilst this appears easy to understand, it’s often a trap for growing businesses. A flat rate subsidises high-risk or international cards by overcharging you on standard UK debit cards, which usually carry much lower underlying costs. If your business processes more than £2,000 per month, moving to a full merchant account is almost always more cost-effective. PurePay Hub operates on a more transparent model, with rates starting at 0.3% for debit and 0.5% for credit, allowing you to keep a much larger portion of your revenue.

Understanding Payout Speeds and Cash Flow

Cash flow is the lifeblood of any regional business. Many traditional banks still operate on a “3-5 day” settlement cycle. This delay is essentially an interest-free loan you’re giving to the processor whilst your own bills, stock orders, and payroll requirements wait. In 2026, next-day funding should be a non-negotiable requirement for your card payment machine. Accessing your funds within 24 hours allows you to reinvest in stock immediately and manage your liquidity with confidence. It removes the stress of “pending” balances and gives you a real-time view of your available capital.

How to Switch Providers and Set Up for Success

Switching your merchant services provider shouldn’t feel like a leap into the unknown. Whilst many companies focus on the ease of their own signup, they often ignore the logistical hurdles of leaving a restrictive contract. To ensure a smooth transition, you must first understand the true state of your current agreement. Start by auditing your last three months of merchant statements to identify hidden markups and unnecessary admin fees. This clarity allows you to compare your current costs against a more transparent model, ensuring your new card payment machine actually delivers the savings you expect.

Check your existing contract for notice periods or exit fee clauses before making any commitments. Under current UK regulations, contracts for card readers cannot exceed 18 months, but many traditional providers still bake in auto-renewal terms that can catch you off guard. If you find yourself facing a steep exit fee, speak to your prospective partner. Some modern providers are willing to discuss ways to offset these costs to facilitate your move to a fairer service. Once you’ve cleared the legal hurdles, select hardware that matches your specific business layout and customer flow. If you’re ready to leave opaque pricing behind, you can request a transparent quote for your business today.

Avoiding Exit Fees and Contract Traps

Negotiating a better deal involves more than just a lower transaction rate. You should prioritise “rolling contracts” over long-term commitments to maintain your business’s agility. A rolling monthly agreement proves that the provider is confident in their service; they don’t need to trap you to keep your custom. Always read the fine print of a card machine lease to ensure there are no hidden “end-of-term” charges or mandatory hardware insurance fees that you didn’t ask for. This discipline protects your future cash flow from unexpected shocks.

Setting Up Your New Terminal

Setting up your new hardware is a straightforward process if you follow a logical sequence. Whilst Wi-Fi offers flexibility, a hardwired Ethernet connection remains the most secure and stable option for fixed points of sale. Once connected, run a test transaction for a small amount to verify the link to your merchant account. This is also the time to set up staff logins and configure your digital terminal for tips, VAT, and custom receipt branding. Taking these steps before your first real customer arrives prevents any awkward delays at the till. Organise your transition by keeping your old terminal active until the new card payment machine is fully tested and live to avoid any downtime.

PurePay Hub: Transparent Payments for UK Businesses

PurePay Hub stands as a stabilising force for your business’s finances. In an industry often viewed with skepticism, we prioritise clarity over corporate jargon. We position ourselves as a fair partner to regional business owners rather than a distant financial institution. Our no-nonsense approach ensures that you understand every aspect of your merchant services, from the hardware on your counter to the final settlement in your bank account. By removing the stress of hidden costs, we allow you to focus on what matters most: serving your customers and growing your brand.

Reliability is the foundation of our service. Whether you need a single countertop card payment machine for a local pharmacy or a network of integrated EPOS systems for a busy retail centre, our solutions are designed to scale with your ambitions. We understand that technical issues can halt your sales, which is why our UK-based support team is always ready to resolve problems quickly. You won’t be passed amongst different departments or left waiting for days for a response. We treat your business as a priority, ensuring your payment processing remains a silent, efficient partner in your daily operations.

Beyond Payments: Business Cash Advances

We provide more than just a way to take payments. A Business Cash Advance offers a flexible way to access capital based on your future card sales. Unlike traditional loans with rigid monthly interest, repayments fluctuate naturally with your daily turnover. When your sales are high, you pay back more; when things are quieter, your repayments reduce accordingly. This model is perfect for funding renovations, purchasing new stock, or launching a marketing campaign without the pressure of fixed monthly overheads.

The PurePay Hub Advantage

The PurePay Hub identity is built on the steady promise of better, fairer service. We believe that your hard-earned money should be in your account as quickly as possible. Whilst many competitors hold onto your funds for several days, we provide next-day funding as standard. This immediate access to capital keeps your business moving and simplifies your cash flow management. Our pricing model is equally transparent, offering rates that protect your margins:

- Debit Cards: Rates starting at 0.3%

- Credit Cards: Rates starting at 0.5%

- Funding: Next-day settlement as standard

- Contracts: Flexible terms without hidden traps

Choosing a card payment machine shouldn’t involve navigating a sea of technicalities or worrying about surprise fees. We offer the technical precision you need framed by a commitment to simplicity. If you’re ready for a partnership that values honesty and integrity, Contact PurePay Hub today for a bespoke quote. Let’s work together to secure the fastest funding and the lowest transaction rates for your business.

Secure Your Business Future with Transparent Payments

Selecting a card payment machine is a strategic decision that directly affects your annual profitability. You now have the tools to distinguish between sleek marketing and genuine financial utility. By prioritising reliable hardware and avoiding the trap of expensive flat-rate fees, you ensure that more of every sale stays exactly where it belongs. A fair partnership is built on the foundation of clarity; your payment processor should be a silent, efficient ally rather than a source of financial stress.

PurePay Hub is here to act as your supportive business partner. We provide a disciplined approach to merchant services that eliminates the frustration of opaque costs and slow settlement cycles. Our partners benefit from debit card rates starting at 0.3% and next-day access to funds, all with a guarantee of no hidden markup fees. We focus on the technical precision of your payments so you can focus on the growth of your business.

Start saving on your transaction fees with PurePay Hub

Taking the step toward a more transparent provider is the smartest move you can make for your bottom line. We look forward to supporting your continued success and helping your business thrive in the modern economy.

Frequently Asked Questions

How much does a card payment machine cost per month in the UK?

Monthly rental for a card payment machine in the UK generally falls between £15 and £30. You should be aware that this headline figure is rarely the total cost. Most providers include additional service charges, PCI fees, and minimum monthly service charges that can double your expected bill. Always request a full breakdown of all recurring costs before committing to a specific terminal.

What is the cheapest way to take card payments for a small business?

The most cost-effective method depends entirely on your monthly turnover. For very low volumes, a flat-rate reader might seem attractive because there are no monthly fees. However, once you process more than £2,000 per month, the high transaction rates of flat-rate providers become a burden. Switching to a dedicated merchant account with rates below 1% will save you significantly more in the long run.

Can I get a card machine without a long-term contract?

You can certainly find providers that offer rolling monthly contracts. Whilst many traditional banks try to lock you into agreements lasting 18 months or longer, modern fintech partners prioritise flexibility. Choosing a rolling contract gives you the freedom to leave if the service doesn’t meet your expectations; this forces the provider to maintain high standards and fair pricing to keep your custom.

How long does it take for card payments to reach my bank account?

Settlement times vary significantly between providers. Traditional banking structures often take three to five working days to clear your funds. In 2026, you should look for next-day funding as a standard feature. Accessing your money within 24 hours provides the liquidity needed to manage stock levels and payroll without relying on expensive credit or overdrafts.

Do I need a specific merchant account to use a card machine?

A merchant account is essential for processing any transaction through a card payment machine. This account acts as a holding area where funds are verified before being settled into your business bank account. Whilst some providers bundle this into a single service, it remains a distinct financial requirement for accepting card payments legally and securely in the UK.

What happens if my business Wi-Fi goes down whilst taking a payment?

Most modern terminals include a mobile SIM card as a fallback for when your business Wi-Fi fails. These units automatically switch to 4G or GPRS networks to ensure you don’t lose sales during a local internet outage. If you operate in an area with poor connectivity, choosing a “roaming” SIM that connects to the strongest available network is a vital safeguard for your revenue.

Are there extra fees for accepting Apple Pay or Google Pay?

There are typically no additional transaction fees for accepting Apple Pay or Google Pay. These digital wallet payments are processed using the same contactless technology as a physical card. Because they use biometric authentication, they are often more secure; this can lead to fewer chargebacks and disputes for your business compared to traditional card-present sales.

How do I avoid PCI compliance fines on my monthly statement?

To avoid PCI compliance fines, you must complete your annual Self-Assessment Questionnaire (SAQ). Many businesses are charged “non-compliance fees” simply because they haven’t updated their details on the merchant portal. Ensure your hardware meets the latest PCI DSS 4.0 standards and maintain a regular schedule for security updates to keep these unnecessary costs off your monthly statement.