With cashless transactions accounting for over 85% of all UK payments as of October 2025, your choice of a self employed card machine UK is the most critical tool in your business kit. It is the difference between a seamless sale and a frustrated customer. Many sole traders still struggle with opaque fee structures that hide the true cost of doing business. You shouldn’t have to settle for clunky hardware or wait three days for your money to arrive.

We agree that your hard-earned margins deserve protection from unnecessary markups. This guide promises to show you exactly how to secure transaction rates below 1% and ensure next-day access to your funds. We provide a transparent breakdown of the best hardware for 2026. We compare everything from the £25 SumUp Air to high-performance portable units. You will learn how to simplify your payments through a reliable partnership that prioritises purity and clarity in every transaction.

Key Takeaways

- Maximise your sales potential by adapting to a UK landscape where cash transactions have dropped below 10% of total sales.

- Secure a self employed card machine UK with transparent, transaction-based rates starting from 0.3% to protect your business margins.

- Identify the ideal hardware for your specific setup, comparing the connectivity and durability of countertop, portable, and mobile terminals.

- Solve cash flow delays by choosing settlement options that provide next-day access to your funds instead of the standard multi-day wait.

- Eliminate hidden markups and “murky” fee structures by adopting a simplified, honest approach to your merchant service agreement.

Why a Self-Employed Card Machine is Essential in 2026

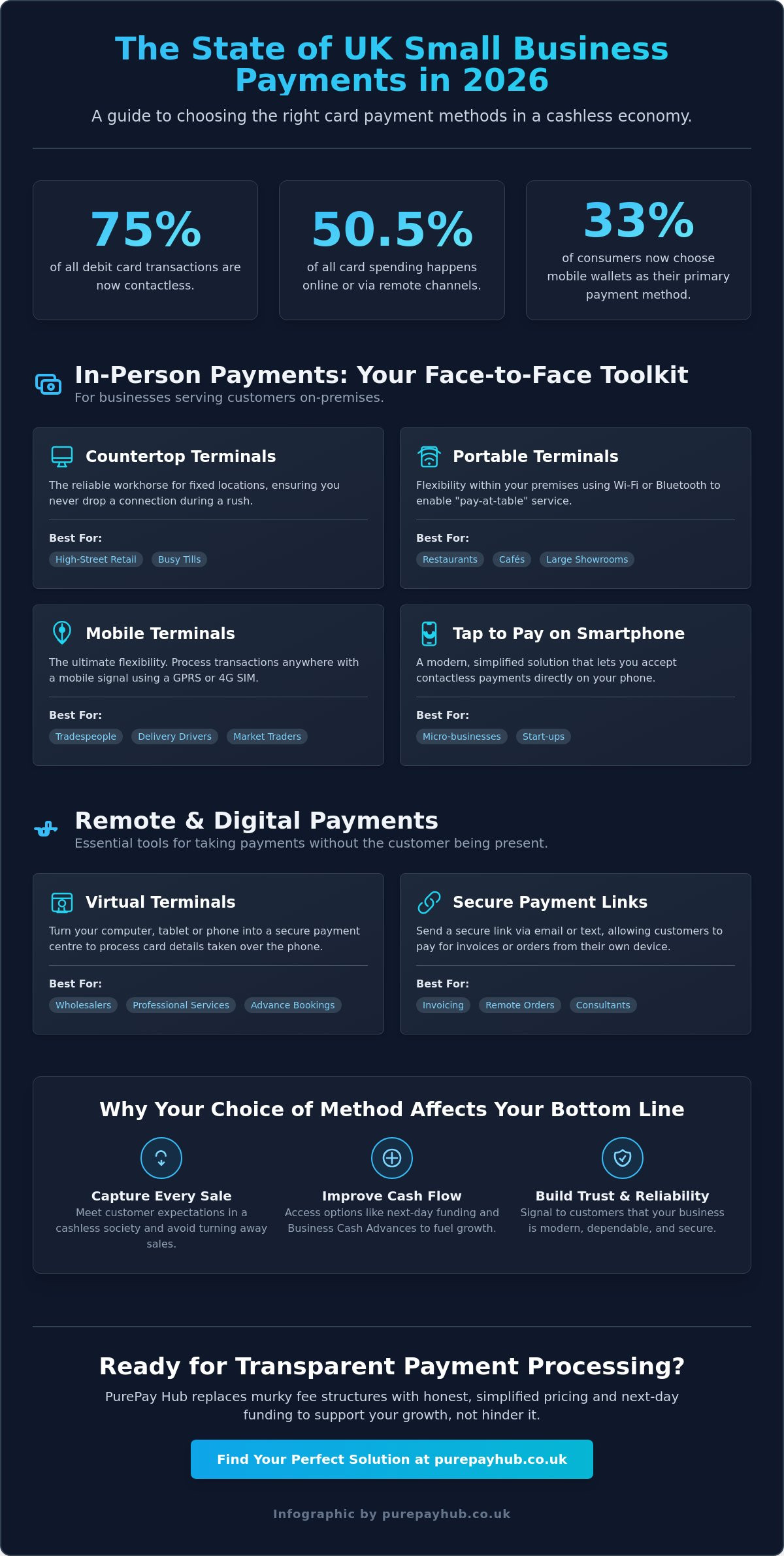

2026 has arrived; and for the UK’s 4.1 million sole traders, the ability to accept digital payments is no longer a luxury. It’s the baseline. A self employed card machine UK is the primary tool that ensures you never miss a sale. With cash transactions now accounting for less than 10% of total UK sales, relying on physical currency is a high-risk strategy that alienates the modern shopper. If you aren’t equipped to take card payments, you’re effectively closing your doors to nine out of ten potential customers.

Asking for a bank transfer or searching for a nearby ATM creates unnecessary friction. A dedicated payment terminal signals that your business is legitimate, modern, and ready to serve. Research consistently shows that British consumers spend more when they pay by card. It removes the “wallet ceiling” imposed by how much physical cash they happen to be carrying, allowing your average transaction value to grow naturally. Professionalism matters in a competitive market; and nothing says “established business” like a sleek, reliable payment process.

The Shift from Cash to Contactless

Digital wallets like Apple Pay and Google Pay have moved from being alternative methods to the standard. In 2026, “Tap to Pay” is the instinctive behaviour for the majority of UK shoppers, especially in urban centres. If your business doesn’t facilitate this, you’re creating a barrier to entry. The modern card machine is a gateway to financial inclusion for SMEs. It allows even the smallest micro-business to compete on a level playing field with high-street giants by providing the same seamless checkout experience.

Benefits Beyond Simple Payment Acceptance

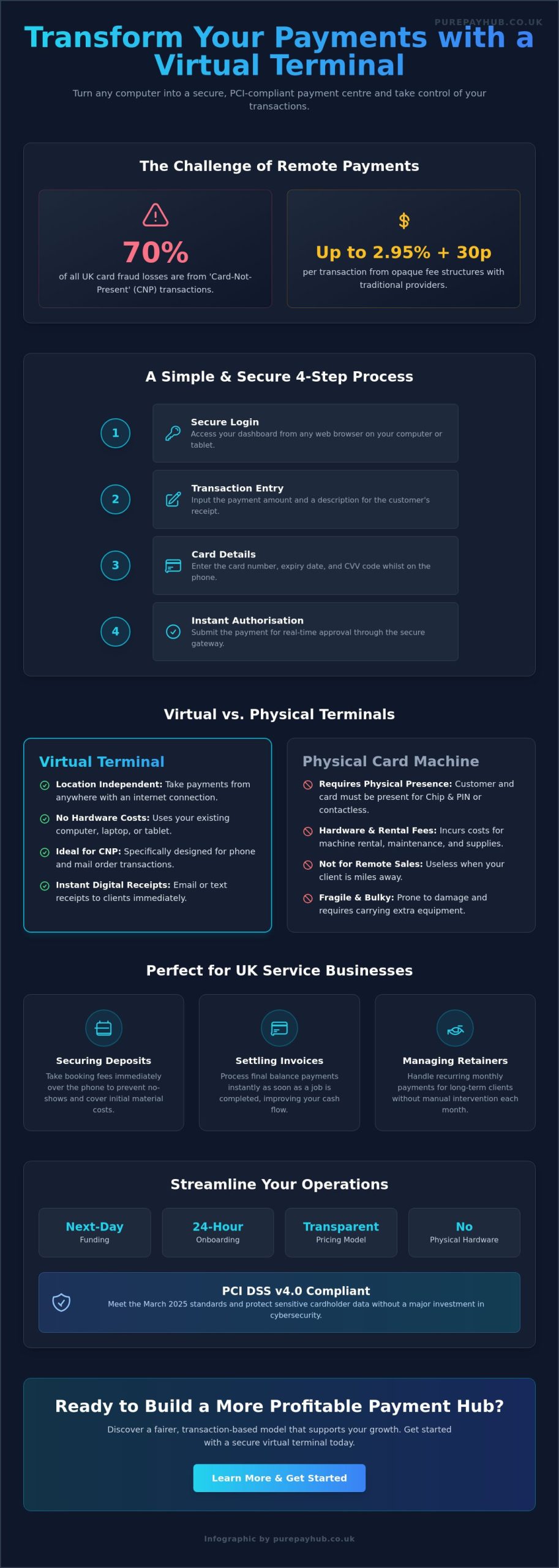

Accepting card payments does more than just move money. It simplifies your entire back-office operation. Integration with accounting software makes Making Tax Digital (MTD) compliance straightforward rather than a quarterly headache. You spend less time counting coins and making trips to the bank; this reduces the physical risk of carrying cash and the time-cost of manual reconciliation. Many modern machines now support payment links and virtual terminals too. This means you can take secure payments whilst away from your primary place of work. It is perfect for tradespeople or consultants who need to secure deposits or finalise invoices on the move without the delay of traditional banking.

Decoding Self-Employed Card Machine Costs: Pure vs Murky Fees

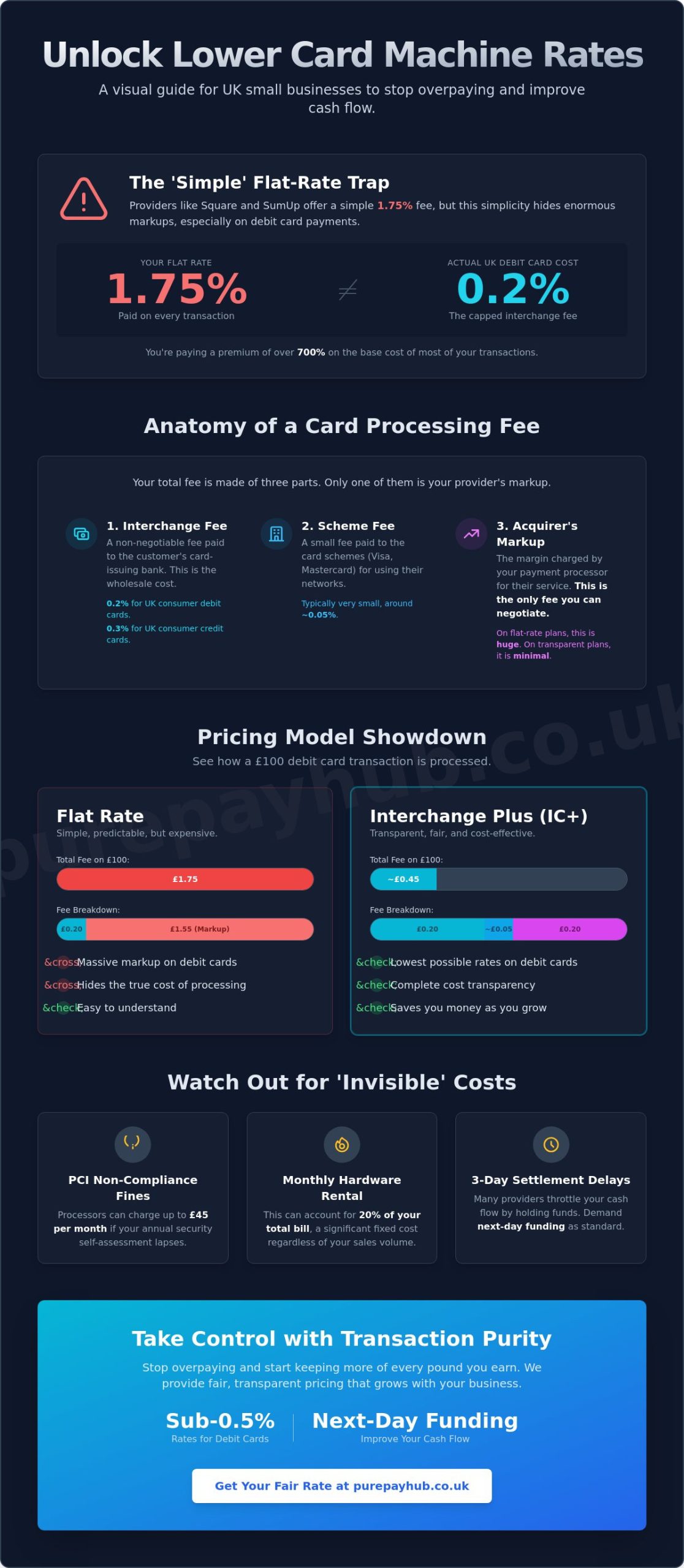

Understanding the true cost of a self employed card machine UK requires looking past the flashy hardware. Most providers hide their profits behind a single, flat percentage. This “murky” model is easy to understand but expensive to scale. To protect your margins, you must understand the three core pillars of payment costs. These dictate what actually leaves your bank account every month. Transparency is the only way to ensure you aren’t overpaying for the simple act of accepting money.

Every transaction fee consists of several layers. A fair provider will break these down for you, rather than bundling them into a high, flat rate. These components typically include:

- Interchange Fees: The non-negotiable cost paid to the customer’s bank.

- Merchant Service Charge (MSC): The fee your provider charges to process the payment.

- Terminal Rental: The monthly cost for the physical hardware and support.

- PCI Compliance: A small fee, usually between £4 and £6, to ensure your data security meets industry standards.

According to recent UK payment trends, the shift towards digital payments has made fee transparency a top priority for small businesses. Beware of “hidden” costs like non-compliance fines. If you don’t complete your annual security questionnaire, some providers will charge you £20 or more every month. A reliable partner helps you avoid these penalties through clear communication and support.

The 0.3% Advantage: Transaction-Based Pricing

The “Pure” model uses transaction-based pricing. In the UK, interchange fees are capped at 0.3% for most debit cards and 0.5% for credit cards. If you pay a flat 1.75% rate, you are effectively giving away 1.45% of every sale in pure profit to your provider. Consider a sole trader with a £5,000 monthly turnover. At a 1.75% flat rate, you pay £87.50. With a transaction-based model, even including a £15 rental fee and small processing markups, your total cost could drop to approximately £45. You can see how much you could save by switching to a model that prioritises your margins over provider profit.

Monthly Rental vs Outright Purchase

Renting your terminal is often the most efficient choice for established sole traders. It provides peace of mind; if the hardware fails, your provider replaces it immediately. Rental contracts also ensure you always have the latest software updates to stay compliant with UK regulations. From a tax perspective, monthly rental fees are a fully deductible business expense. While buying a basic mobile reader for £25 makes sense for very low-volume micro-businesses, the higher transaction rates on those devices quickly become a burden as your sales grow. Once you process more than £2,000 per month, the lower rates found in rental agreements far outweigh the initial hardware saving.

Choosing the Right Terminal for Your Business Type

Your hardware choice is a personal decision that dictates your daily workflow. You need a device that matches your pace and environment. A self employed card machine UK should never be a bottleneck during a busy shift. The right terminal ensures you stay connected; whether you’re behind a counter or at a customer’s front door. We categorise these devices into three primary types to help you find your perfect fit.

Countertop units are the traditional workhorses of the retail world. They plug directly into your power supply and use a fixed Ethernet or Wi-Fi connection. These are the most stable options for permanent shops. Portable units offer more freedom; they allow you to take the terminal to a customer within your premises. These typically rely on Wi-Fi or Bluetooth. For those who work on the road, mobile units are essential. They use internal SIM cards to connect to 4G or GPRS networks, ensuring you can take payments anywhere in the country with a mobile signal. You can explore our full range of Mobile & Portable Payment Solutions to see which technology suits your specific trade.

Connectivity is the backbone of your payment process. Ethernet remains the gold standard for reliability in fixed locations. However, if you’re mobile, 4G connectivity is superior to Bluetooth pairing with a smartphone. It eliminates the frustration of dropped connections and sync errors. Battery life is equally critical. If you’re a courier or a mobile hairdresser, a dead battery means lost revenue. Look for hardware that offers at least 8 hours of active use or 48 hours of standby time to get through your longest days without anxiety.

Mobile Card Machines for Tradespeople and Couriers

If you’re always on the move, you need a device that is both lightweight and rugged. Mobile terminals are designed to fit in a pocket or a tool bag. They use pre-installed SIM cards to provide a standalone connection, so you don’t have to rely on a customer’s Wi-Fi. For outdoor environments, durability is a priority; look for units with reinforced casing. If a customer isn’t physically present, you can use payment links as a secure backup. This allows you to send a simple URL via text or email, ensuring you get paid for deposits or remote call-outs without delay.

Portable and Countertop Units for Fixed Locations

Fixed locations like cafes or salons benefit from the speed of portable and countertop units. Portable devices are perfect for hospitality; they allow for “pay at table” service which improves table turnover. These units often feature integrated thermal printers for physical receipts, which many British customers still prefer for their records. Countertop units are ideal for high-volume retail centres where a stable, wired connection is available. They are built for speed and constant use, providing a central, stabilizing force for your checkout area.

Managing Cash Flow: Next-Day Funding and Advances

Cash flow is the ultimate metric of health for any UK sole trader. You can have a record-breaking day of sales; but if that money is trapped in a clearing cycle, your business is effectively at a standstill. This is why settlement speed is often the primary objection when choosing a self employed card machine UK. Standard processing times of three to five working days are an outdated relic of traditional banking. They don’t reflect the fast-paced reality of running a modern business in 2026.

Next-Day Funding changes the equation. It means that the sales you process today are sitting in your bank account by the next working day. This level of liquidity allows you to respond to opportunities in real-time. You don’t have to check your balance with anxiety before ordering new supplies or paying a supplier. We view our role as a central, stabilising force for your finances. By removing the wait, we turn your payment terminal into a high-speed engine for your business’s daily operations.

Why Settlement Speed Matters

Slow funding cycles do more than just cause stress; they actively limit your ability to scale. If you are a tradesperson waiting for a large invoice to clear before you can purchase materials for the next job, you are losing billable hours. PurePay Hub prioritises rapid access to funds because we understand that time is money for a merchant. We ensure that your card machine remains a bridge to your next success rather than a barrier to entry. Your hardware should facilitate your growth, not act as a financial bottleneck.

Flexible Funding via Your Card Sales

Beyond daily settlements, your card turnover can unlock significant growth capital. A Business Cash Advance is a flexible, modern alternative to a rigid bank loan. Unlike traditional lending, there are no fixed monthly repayments that stay the same regardless of your income. Instead, you repay a set percentage of your daily card sales. This model is inherently fair; you pay back more during your peak seasons and less during the quieter months. It aligns perfectly with the natural ebb and flow of self-employed life.

This is unsecured capital. It doesn’t require bricks-and-mortar collateral, making it an accessible option for self-employed professionals who don’t own commercial property. It is a partnership based on your actual performance rather than a credit score from a distant institution. You can learn more about our Business Cash Advance Based on Card Sales to see how this flexible funding can support your next project without the stress of fixed debt.

Why PurePay Hub is the Best Partner for the Self-Employed

Choosing a self employed card machine UK is about more than just hardware. It is about finding an ally who values your margins as much as you do. We built PurePay Hub on a “Pure” philosophy. This means we provide transaction-based pricing without the hidden markups that often plague the industry. We don’t believe in corporate jargon; we believe in clarity. Our goal is to act as a central, stabilising force for your business finances, allowing you to focus on growth while we handle the technicalities of every “tap” and “swipe”.

Our service adapts to your specific needs. Whether you require a countertop unit for a fixed shop or a mobile terminal for trade on the road, our hardware range is designed for reliability. We prioritise honesty in our partnerships. You won’t find yourself trapped in a murky contract with escalating fees. Instead, you get a simplified model that scales with your success. By choosing us, you are choosing a modern fintech partner that understands the individual pressure of being a sole trader in the UK today.

The PurePay Hub Onboarding Experience

We know that your time is your most valuable asset. The process of getting a Merchant ID and setting up your first terminal shouldn’t take weeks. We have refined our onboarding to be fast and intuitive. Once you apply, we move quickly to get you approved and your hardware dispatched. You won’t be left to struggle with complex manuals either. Our dedicated UK support team is always available to ensure your first sale goes through without a hitch. We provide the technical backbone so you never have to worry about a Sale Failed message during a busy shift.

Switch to PurePay Hub today for fairer, faster payments

Commitment to the UK Merchant Community

Our approach is shaped by the latest UK standards. On April 21, 2026, the UK government announced new measures to modernise payment services regulation. We have already integrated these digital frameworks into our systems to ensure you stay ahead of the curve. You also benefit from updated protection; we provide at least 90 days’ notice for any service changes, which is a significant improvement over the previous 60-day industry standard. This commitment to transparency is matched by our focus on security. Every system we provide is fully PCI-compliant, giving you and your customers total peace of mind during every transaction.

Get your bespoke quote for a self-employed card machine

Secure Your Margins and Simplify Your Payments

Running a business as a sole trader in 2026 demands efficiency and absolute clarity. You have seen how the right self employed card machine UK turns every transaction into a growth opportunity. By moving away from murky flat-rate fees and adopting a transaction-based model, you keep more of your hard-earned profit. Speed matters just as much as cost. Next-day access to your funds ensures your cash flow remains fluid; this allows you to pay suppliers and manage stock without the standard three-day delay.

The choice of hardware, from mobile terminals for traders on the move to stable countertop units, should always match your specific workflow. We believe in providing a pure, honest partnership that eliminates the stress of hidden markups and technical failures. You deserve a payment partner that acts as a reliable hub for your growth. It is time to stop overpaying for the simple act of accepting money and start protecting your margins with a fairer system.

Join the thousands of UK merchants using PurePay Hub for transparent processing and benefit from debit rates starting from 0.3% and next-day funding with no hidden monthly markups. Your business is ready for the next level; we are here to help you reach it.

Frequently Asked Questions

Is it better to buy or rent a card machine when self-employed?

Renting is the superior choice for established sole traders who prioritise reliability and support. When you rent, your provider handles software updates and replaces faulty hardware immediately. This ensures your self employed card machine UK never becomes a point of failure. Buying a basic reader outright makes sense for micro-businesses with very low turnover; but the higher transaction fees on those devices quickly erode any initial hardware savings.

How much are the average transaction fees for a sole trader in the UK?

Average fees vary significantly depending on your pricing model. Most flat-rate providers charge approximately 1.75% per transaction regardless of the card type used. In contrast; a transaction-based model allows you to pay closer to the actual interchange rates. These are currently capped at 0.3% for most UK debit cards and 0.5% for credit cards. Choosing a transparent model can reduce your total processing costs by over 50%.

Can I take card payments without a physical machine?

You can accept payments remotely using a Virtual Terminal or Payment Links. A Virtual Terminal allows you to type card details into a secure web browser whilst speaking to a customer over the phone. Payment Links are even simpler; you send a secure URL via text or email. These digital tools are perfect for consultants or tradespeople who need to take deposits before arriving on-site.

What is a merchant account and do I need one if I am self-employed?

A merchant account is a dedicated holding area where funds are checked and authorised before being sent to your bank. You definitely need one to accept card payments. Modern providers usually bundle this into your service agreement; so you don’t have to apply for one separately at a high-street bank. It acts as the essential bridge between your customer’s card and your business bank account.

How long does it take for card payments to reach my bank account?

Standard settlement times in the UK typically range from three to five working days. However; many modern providers now offer Next-Day Funding as a standard or premium feature. This speed is vital for managing your daily cash flow and paying suppliers on time. If you process a sale on Monday; the funds should be available in your account by Tuesday morning.

What happens if my card machine loses Wi-Fi connection during a sale?

High-quality mobile and portable machines automatically switch to a GPRS or 4G backup signal if the Wi-Fi fails. This ensures your self employed card machine UK stays online even in areas with poor internet. Some devices also offer an “offline mode” that stores the transaction data securely. The payment then processes once the connection is restored; so you never have to turn a customer away.

Are there any hidden costs like PCI compliance fees I should know about?

You should be aware of PCI compliance fees and potential non-compliance fines. Most providers charge a small monthly fee, usually between £4 and £6, to manage your data security certification. If you fail to complete your annual security profile; you may be hit with a non-compliance fine of £20 or more every month. Transparent providers will help you navigate this process to avoid these unnecessary penalties.

Can I use a personal bank account for my card machine sales?

Some entry-level providers allow you to link a personal account; but most dedicated merchant services require a business bank account. Using a business account is best practice for tax purposes and Making Tax Digital (MTD) compliance. It keeps your professional earnings separate from your personal spending. Most UK banks also have terms and conditions that prohibit using personal accounts for business activities.