Why is your card processing bill so much higher than the percentage rate you signed up for? It’s a question we hear from local merchants every week. You likely chose your provider based on a competitive headline rate, yet your monthly statement remains a confusing maze of unexpected admin charges and compliance fees. These hidden fees card processing UK businesses face are often a deliberate tactic to mask the true cost of service.

We agree that reconciling your accounts shouldn’t feel like a full-time job. With the Payment Systems Regulator currently focusing on tackling high card fees through 2026 and 2027, there has never been a better time to demand transparency. This guide uncovers the opaque charges eroding your margins and explains how to calculate your effective rate, which is the only metric that truly matters. We will provide a checklist to compare providers fairly and show you how to secure next-day funding without the hidden premiums that often trap growing businesses.

Key Takeaways

- Learn how to decode your monthly merchant statement to identify charges that weren’t mentioned in your initial sales proposal.

- Master a simple five-step audit to calculate your ‘Effective Rate’ and see exactly what your processing truly costs.

- Identify common contractual traps like Minimum Monthly Service Charges and PCI non-compliance fines that drain your monthly margins.

- Uncover the reality of hidden fees card processing UK providers often bury within complex tiered pricing structures.

- Discover how a transparent partnership prioritises your business with next-day funding and clear, punchy reporting.

The Reality of Card Processing Fees in the UK

Hidden fees aren’t just a minor annoyance. They are a direct hit to your bottom line. In the UK merchant services market, hidden fees are any costs that weren’t explicitly highlighted in your initial sales proposal or headline rate. You might sign a contract based on a low percentage, only to find your monthly statement littered with unexpected admin or compliance line items. Despite the Payment Systems Regulator focusing on fee transparency through 2026 and 2027, the industry remains intentionally opaque. This complexity makes it difficult for local business owners to reconcile their accounts or compare providers fairly.

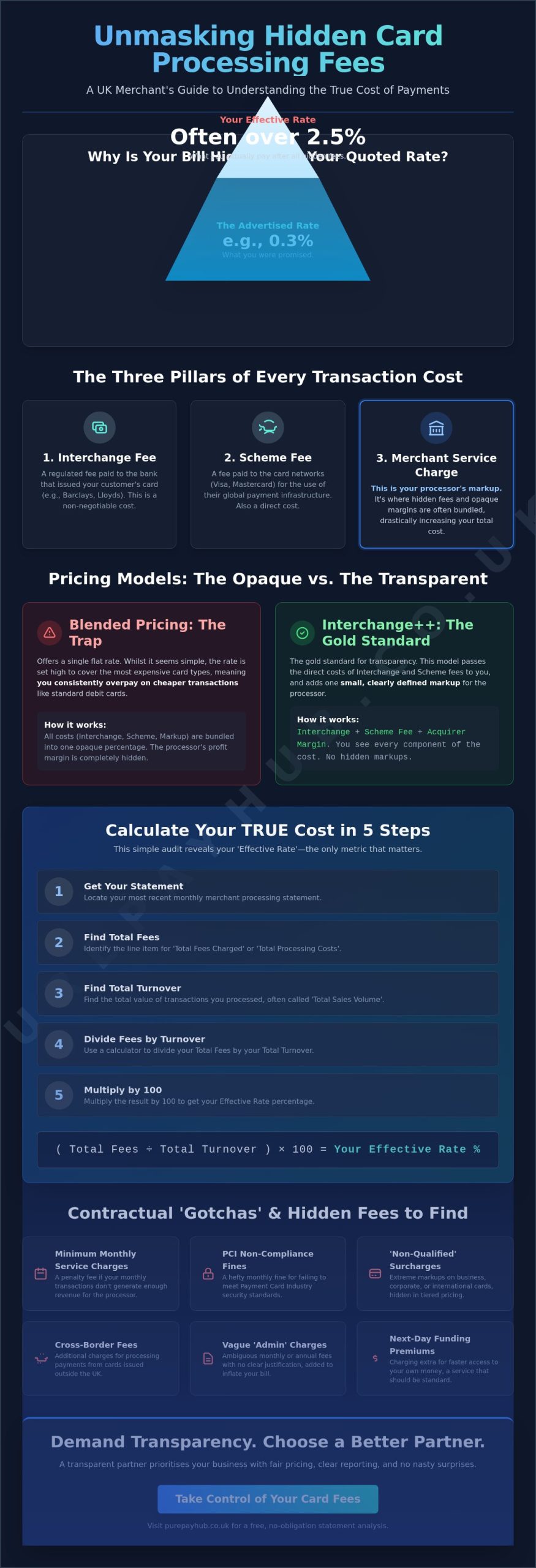

The gap between what you are promised and what you actually pay can be staggering. A headline rate of 0.3% sounds like a bargain, but it rarely represents the final cost. When you factor in various markups, that figure can easily climb toward a 2.5% effective rate for an SME. Understanding these hidden fees card processing UK providers often use is the first step toward reclaiming your margins. It requires looking past the marketing and into the mechanics of how payments are actually priced.

The Three Pillars of Payment Costs

Every transaction you process consists of three distinct cost components. The first is the Interchange fee. This is a regulated fee paid to the bank that issued your customer’s card. The second is the scheme fee, which Visa and Mastercard charge for the use of their global networks. The third pillar is the Merchant Service Charge (MSC). This is the processor’s cut. While interchange and scheme fees are relatively fixed, the MSC is where hidden margins often live. Many providers bundle these together to hide exactly how much they are taking for themselves.

Why ‘Cheap’ Rates Can Be Expensive

Low headline rates are frequently used as bait to trap busy merchants. A provider might quote you a tiny percentage that only applies to domestic consumer debit cards. They often omit the much higher rates for commercial, corporate, or international cards. These transactions can carry markups that are three or four times higher than the quoted rate.

This “bait and switch” tactic relies on you not checking your “Effective Rate”—the total cost divided by your total turnover. If you don’t monitor this metric, you won’t see how cross-border fees or monthly “minimum service” charges are eroding your annual profits. A transparent partner should provide a clear breakdown of these costs from day one, ensuring you don’t get a nasty surprise when your first statement arrives.

Decoding the Merchant Statement: Identifying Common Markups

Reading your monthly merchant statement shouldn’t require a finance degree. Most providers design these documents to be intentionally confusing. They bury the most expensive charges in the fine print. To find the hidden fees card processing UK providers often tuck away, you need to look past the summary page. The real story is told in the transaction breakdown. Your statement is more than just a bill. It is a map of where your provider is prioritising their profit over your partnership.

The Tiered Pricing Trap

Many UK merchants are on tiered pricing models without realising it. This model groups transactions into “Qualified”, “Mid-Qualified”, and “Non-Qualified” categories. Qualified rates apply to standard consumer debit cards. Mid-Qualified usually covers cards that are manually keyed in. Non-Qualified is the catch-all for corporate, international, and premium reward cards.

Processors often hide their highest margins in the Non-Qualified tier. Since these transactions are more complex, providers assume you won’t question a higher rate. If you see a large portion of your turnover falling into the Non-Qualified category, you are likely overpaying. Common triggers for these higher tiers include:

- Business or corporate credit cards.

- International cards from outside the UK or EU.

- Transactions where the card wasn’t physically present, such as phone orders.

Interchange++ vs. Blended Pricing

Blended pricing is a common model for small businesses. It offers a single flat rate for all transactions. Whilst this sounds simple, it usually includes a significant safety margin for the provider. They set the rate high enough to cover the most expensive cards. This means you pay a premium on every standard debit transaction to protect the processor’s margin. It is a model built on convenience rather than cost-efficiency.

Interchange++ is the gold standard for transparency. It breaks the cost into three distinct parts: the interchange fee, the scheme fee, and the acquirer margin. This model ensures you only pay the exact cost of the transaction plus a fixed fee for the processor. It prevents providers from padding scheme fees or hiding extra markups. If you want a partner that prioritises this level of clarity, you might want to explore a fairer way to manage your payments.

Look closely at the “Scheme Fees” section of your statement. Some providers add a small markup to the fees set by Visa and Mastercard. Because these are technical costs, most merchants assume they are fixed. A transparent statement will show these costs as pass-through charges with no added padding. If your provider won’t show you the exact breakdown of these three components, they are likely hiding something. Demand a statement that treats you like a business partner, not a source of easy profit.

Contractual ‘Gotchas’ and Opaque Monthly Charges

Transaction rates are only half the story. To truly understand the hidden fees card processing UK merchants face, you must look at your fixed monthly costs. Many providers lure you in with low percentages but claw that money back through contractual gotchas. These charges apply regardless of your sales volume. They turn a seemingly fair deal into a heavy financial burden that is difficult to reconcile at the end of the month.

The Minimum Monthly Service Charge (MMSC) is one of the most common traps. If your total transaction fees don’t reach a set threshold, the provider charges you the difference. You are essentially paying a penalty for doing too little business. It is a fee for a service you never actually used. For seasonal businesses or those just starting out, this can make your effective rate skyrocket during quiet periods.

Administrative and Compliance Fees

PCI DSS Management fees are often presented as a necessary security service. In reality, they are frequently just a high-margin line item. Whilst data security is vital, many providers charge non-compliance fines that typically exceed £10 per month. Some processors make the compliance paperwork intentionally difficult so they can keep collecting these penalties. You might also find statement fees on your bill. There is a distinct irony in paying a monthly fee just for the right to see how many other fees you have been charged. High-volume retailers should also watch for authorisation fees. These small per-click costs apply to every transaction attempt and can quickly add up amongst hundreds of daily sales.

The Hardware Lease Loophole

Hardware leases are a major red flag in the merchant services industry. A 48-month lease for a Countertop Card Machine or a Portable Card Machine might seem affordable at first. However, the total cost of ownership over four years often ends up being triple the price of buying the unit outright. These leases are usually managed by third-party finance companies, making them nearly impossible to cancel even if you close your business.

You should also be wary of maintenance and support fees bundled into these leases. Often, these charges provide very little actual value. If your terminal breaks, you may still find yourself waiting days for a replacement despite paying a monthly support premium. Always check the exit fees and notice periods before signing. Trying to leave a bad deal can often cost thousands of pounds in remaining lease payments and contract buy-out fees. A transparent partner will offer flexible terms that don’t rely on trapping you in a four-year hardware loop.

How to Audit Your Processing Costs in 5 Steps

Taking control of your finances starts with a clear audit. You cannot fix what you cannot measure. Identifying hidden fees card processing UK businesses are subject to requires a methodical approach. By stripping away the sales jargon, you can see exactly how much of your hard-earned revenue is being siphoned off by your provider. Follow these five steps to uncover the truth about your merchant account.

- Step 1: Calculate your ‘Effective Rate’. Divide your total monthly card fees by your total monthly card turnover. This single percentage is the ultimate truth of your processing costs.

- Step 2: Isolate fixed monthly costs. Look for line items that appear every month regardless of your sales volume. This includes terminal hire, MMSC, and statement fees.

- Step 3: Review your ‘Card Mix’. Check your statement to see if you are being penalised for business, corporate, or international cards. These often carry massive hidden markups.

- Step 4: Target compliance and admin fees. Identify PCI non-compliance fines or “security” fees. If you are compliant, these should not exist on your bill.

- Step 5: Request a breakout quote. Ask a transparent provider for a side-by-side comparison. A fair partner will show you exactly where you can save money without hiding behind complex bundles.

Calculating Your True Effective Rate

Your effective rate is the only metric that bypasses marketing fluff. To find it, take your most recent monthly statement. Locate the total amount deducted for all card services and divide it by your total card sales for that period. For example, if you paid £150 in total fees on £10,000 of sales, your effective rate is 1.5%.

In 2026, a competitive effective rate for a UK business often sits between 0.4% and 1.7% for debit-heavy industries. If your rate is consistently above 2% or 3%, you are likely paying for services you don’t need or markups you didn’t agree to. This formula allows you to compare different providers on a level playing field, regardless of how they structure their individual transaction rates.

Negotiating with Your Current Provider

Once you have your data, it’s time to challenge your provider. Use direct language. Ask them why your “miscellaneous” or “admin” charges are so high. Specifically, ask them to switch your account to an Interchange++ pricing model. This model removes the “safety margin” that providers build into blended rates.

If they refuse to provide a clear breakdown, it is a sign that the partnership is no longer serving your business. Sometimes the long-term savings of a transparent deal far outweigh the one-off cost of an exit fee. You deserve a partner that treats your margins with respect. If you are ready for a clearer picture of your costs, you should request a breakout quote to see the difference transparency makes.

Choosing a Transparent Partner for Your UK Business

PurePay Hub doesn’t just provide technology. We act as a fair partner to regional business owners. Traditional providers often treat merchants as a source of passive income. They hide markups in complex tiered structures and obscure their true margins. We believe that transparency is the only way to build a dependable financial relationship. By eliminating the hidden fees card processing UK merchants typically endure, we help you keep more of your revenue where it belongs. Our role is to provide clarity in an industry that has long thrived on confusion.

Our approach focuses on directness. We offer a comprehensive suite of tools including Countertop Card Machines, Portable Card Machines, and Mobile Card Machines. Each device is backed by a commitment to honest pricing. Whether you use our EPOS Systems or our Online Payment Gateway, you receive punchy, clear reporting. You will always know exactly what you are paying and why. This level of detail ensures your accounts are always easy to reconcile.

The PurePay Hub Difference

Onboarding should be simple. We avoid the fine print that traps merchants in long-term, high-cost contracts. Our process is direct. It prioritises your business needs over corporate jargon. One of our core commitments is providing next-day access to funds. We understand that cash flow is the lifeblood of your operation. We don’t believe in holding onto your money to support our bank balance. You earned it; you should have it. Hardware costs are another area where we lead with honesty. We offer fair rental terms for our equipment without the 48-month lease traps discussed earlier. You get the equipment you need to take payments in person or via Payment Links without worrying about inflated ownership costs.

Taking the Next Step Toward Fairness

The journey to a fairer deal starts with an audit. Our experts provide a free, no-obligation review of your current merchant statement. We look for the “non-qualified” markups and the admin charges that erode your margins. We then show you a clear path to a more transparent model. This isn’t just about switching providers. It is about reclaiming the profit that your hard work generates.

Switching is a straightforward process. We handle the technicalities so you can focus on running your business. You deserve a payment partner that prioritises your growth and treats you with respect. If you are tired of the maze of monthly charges and opaque billing, it is time to take action. You can audit my merchant statement today to discover the true cost of your current processing and see how much your business could save with a transparent partner.

Reclaim Your Margins with Absolute Transparency

You’ve now uncovered how the hidden fees card processing UK providers often hide can quietly erode your hard-earned profits. By calculating your effective rate and auditing your monthly statement for fixed admin charges, you take the power back from opaque institutions. You don’t have to settle for confusing bundles or predatory lease terms that hold your business back. Reclaiming your revenue starts with the simple decision to demand total clarity.

A fair partnership is built on clarity and mutual respect. At PurePay Hub, we prioritise your success by offering debit card rates from 0.3% and next-day funding as standard. You shouldn’t have to wait for your money or guess what your bill will be at the end of the month. Our independent UK-based support team is here to ensure you always have a direct line to an expert who understands your local business needs. We focus on being a supportive ally rather than a distant financial firm.

It’s time to stop overpaying for complexity and start keeping more of every pound you earn. Take the first step toward a simpler, fairer financial future for your business by choosing a partner that values honesty as much as you do. You deserve a payment solution that works just as hard as you do.

Get a Transparent Quote from PurePay Hub Today

Frequently Asked Questions

What is a Minimum Monthly Service Charge (MMSC) in the UK?

A Minimum Monthly Service Charge is a baseline fee you pay if your monthly transaction volume is low. If your earned transaction fees don’t reach this set amount, the processor charges you the difference. It ensures the provider makes a profit even during quiet periods. You should check your statement for this charge if your business is seasonal or just starting out.

How can I tell if I am being overcharged for PCI compliance?

You are likely being overcharged if you see a “PCI Non-Compliance Fee” every month on your statement. These penalties usually cost more than £10 per month. A fair partner helps you complete your paperwork to remove these fines. If you are paying for “PCI Management” but still receiving penalties, your provider is profiting from your lack of support.

Are debit card fees always lower than credit card fees?

Consumer debit card fees are usually lower than credit card fees because they carry less risk and have lower regulated interchange caps. In the UK, consumer debit interchange is capped at 0.2% whilst consumer credit is 0.3%. However, commercial and international cards don’t follow these caps. These hidden fees card processing UK merchants often see can push credit costs much higher.

What is an ‘effective rate’ and why is it important for my business?

Your effective rate is the total cost of processing divided by your total monthly turnover. It is the most important metric because it reveals the true percentage you pay after all markups are added. It bypasses headline rates and sales jargon. Monitoring this number helps you understand if your current deal is actually as cheap as you were promised.

Can I switch card machine providers if I am still in a contract?

You can switch providers at any time, but you must first calculate your exit fees. Traditional contracts often have long notice periods or terminal lease buy-outs. Sometimes the monthly savings from a transparent partnership outweigh the one-off cost of leaving a bad deal. It’s best to have an expert audit your current contract before making the move.

Why does my statement show ‘non-qualified’ transactions?

Non-qualified transactions appear on your statement when a sale doesn’t meet the criteria for your lowest “qualified” rate. This usually happens with corporate cards, international cards, or manually keyed-in orders. These transactions carry higher markups that providers often hide in the fine print. Seeing many of these is a sign that your current pricing model isn’t built for your card mix.

What are authorisation fees and should I be paying them?

Authorisation fees are small charges applied every time your card machine requests approval from the customer’s bank. These “per-click” costs apply to every transaction attempt, even if it is declined. Whilst common, they can become a significant cost for high-volume retailers. You should ensure these fees are clearly stated in your initial quote to avoid surprises.

Is next-day funding usually an extra hidden cost?

Next-day funding is frequently sold as a premium service with an extra hidden cost. Many traditional providers hold your funds for three to five days to support their own bank balance. A transparent partner provides next-day access to your money as a standard feature. You shouldn’t have to pay a premium to access your own revenue quickly.