Imagine it’s a busy Saturday afternoon and your shop is full, but suddenly your terminal displays a “System Tamper” error. Within minutes, a queue forms and you’re forced to tape a “Cash Only” sign to your front door. It’s a nightmare scenario that costs you revenue and reputation. If your current provider is dragging their feet, you need an emergency card machine replacement to get your business back online before the next customer walks away.

We understand how frustrating it is to feel abandoned by legacy providers when your livelihood is on the line. With nearly 95% of in-store transactions now being contactless, being unable to take card payments is no longer a minor hiccup; it’s a total shutdown. You shouldn’t have to wait days for a resolution or navigate complex onboarding during a crisis. Business owners deserve a partner that acts with the same urgency they do.

This article will help you secure a rapid replacement terminal and keep your business trading whilst your main system is down. We’ll look at the quickest ways to restore your payments, the importance of modern hardware compatibility, and how a supportive partner can turn a technical disaster into a seamless transition.

Key Takeaways

- Learn the immediate troubleshooting steps to take when a terminal fails, from performing hard resets to verifying network-wide outages with your provider.

- Discover how to keep revenue flowing using a Virtual Terminal or Payment Links whilst your physical hardware is out of action.

- Understand the timeline for an emergency card machine replacement and why digital onboarding speed is the real bottleneck for most businesses.

- Identify the key contract features, such as swap-out warranties and UK-based support, that protect your business from future payment disruptions.

- Compare the slow response times of legacy banks against modern providers that prioritise rapid account activation and next-day hardware delivery.

Immediate Steps to Take When Your Card Machine Fails

When your card machine stops working, the clock starts ticking on your daily revenue. Don’t panic. Start with a hard reset. Power the unit down completely, wait thirty seconds, and restart. This simple step often clears temporary software glitches that stall transactions. If the screen remains blank or frozen, check your connectivity. Most modern hardware relies on stable Wi-Fi or a GPRS signal to communicate with the bank. A Payment terminal is a sophisticated piece of kit, but it’s only as good as the network it sits on. Ensure your router is functioning and that other devices can connect to the same network.

If the reset fails, call your provider immediately. You need to know if you’re facing a widespread network outage or a localised hardware failure. Ask the support agent for a specific error code. Documenting this code is vital. It speeds up the technical support process and proves you’ve done your due diligence. If they confirm the hardware is dead and cannot be fixed over the phone, you’re officially in the market for an emergency card machine replacement. Do not wait for a “call back” that might never come; insist on a clear timeline for a new unit.

Whilst you wait for a resolution, switch to a backup method. Don’t turn customers away with a “Cash Only” sign. If you have access to a Virtual Terminal or can generate Payment Links, use them. These tools allow you to process payments via a tablet or smartphone. They keep the queue moving while your main terminal is out of action. It’s about maintaining momentum and showing your customers that you’re prepared for technical hitches.

Troubleshooting Common Terminal Errors

“Tamper” alerts are the red flag of the payment world. They usually mean the internal security sensors have been tripped, often due to a drop or a power surge. This hardware is permanently compromised for security reasons and cannot be reset. Also, check the basics. Is the charging base faulty? Try a different cable to rule out power issues. For portable units, reseat the SIM card. A loose connection here can mimic a total system failure and is a quick fix that avoids an unnecessary emergency card machine replacement.

When to Declare a Hardware Emergency

Identify the point of no return early. If there’s visible physical damage or the software is stuck in a reboot loop, it’s time to act. Calculate your downtime. If your current provider quotes a seven-day lead time but you’re losing hundreds of pounds an hour, that’s a genuine hardware emergency. You need a partner who offers next-day dispatch to minimise the damage to your bottom line. Remember that just buying a generic reader from a local shop won’t work instantly. You need a provider who can handle the digital onboarding and account linking just as fast as the physical delivery.

Speed of Replacement: How Quickly Can You Get Back to Trading?

Speed is a relative term in the payments industry. For a legacy bank, “fast” might mean a replacement unit arriving in a week. For a local merchant losing sales, “fast” means tomorrow morning. When you’re searching for an emergency card machine replacement, you must distinguish between the delivery of the hardware and the activation of the service. A shiny new device sitting on your counter is just an expensive paperweight until the software is live and linked to your account. You need both the physical and digital tracks moving at the same pace to restore your cash flow.

Traditional high-street banks often struggle with this dual requirement. They rely on outdated logistics networks and manual approval processes that aren’t designed for a crisis. It’s common for these institutions to quote 7-10 working days for a replacement. In a modern retail environment, that delay is a disaster. You shouldn’t be penalised for hardware failure, yet slow support from a legacy provider does exactly that. Choosing a provider that treats your downtime with urgency is the only way to protect your bottom line.

Hardware Delivery Timelines in the UK

In the UK, the logistics of merchant services are well-established. Reliable providers use dedicated courier networks to ensure next-day delivery for countertop and portable machines. This is the baseline you should demand. If a provider cannot guarantee a 24-hour window, they aren’t equipped for emergency scenarios. Always verify that the replacement package is comprehensive. This includes the terminal, the correct power adapter, and the specific charging cradle for your model. Retail and hospitality businesses don’t have time to hunt for spare cables whilst customers are waiting to pay. A complete “plug-and-play” kit is essential for a smooth emergency card machine replacement.

The Onboarding Bottleneck

The digital onboarding process is the most common cause of extended downtime. Even with hardware in hand, you might be stuck waiting for background checks. To bypass this, choose a partner that uses automated verification systems for “Instant Activation”. You can play your part by keeping your business documentation organised and ready for upload. This includes your latest business bank statements and valid photo identification. Having these files ready allows a modern provider to verify your account in hours rather than days. At PurePay Hub, we’ve stripped away the unnecessary red tape. Our system is built for speed and transparency, ensuring your account is ready to process transactions the moment your hardware is unboxed. We believe that restoring your payments should be a simple, straight-talking process that gets you back to trading without the typical corporate run-around.

Accepting Payments Without a Physical Terminal

Waiting for your emergency card machine replacement to arrive doesn’t mean your business has to grind to a halt. You can bridge the gap between a hardware failure and the arrival of a new unit by using software-based payment tools. These interim solutions allow you to keep processing transactions without a physical terminal in your hand. They’re quick to set up and ensure that your customers aren’t met with a “Cash Only” sign. By diversifying how you accept money, you build a more resilient business that can survive technical hitches.

Most modern merchant accounts include access to digital payment methods as standard. If you’ve been relying solely on a countertop or portable unit, now is the time to explore your dashboard. These tools aren’t just for emergencies; they’re valuable additions to your trading arsenal. They offer flexibility for phone orders, off-site events, or simply managing a sudden surge in customers when your main system is under pressure.

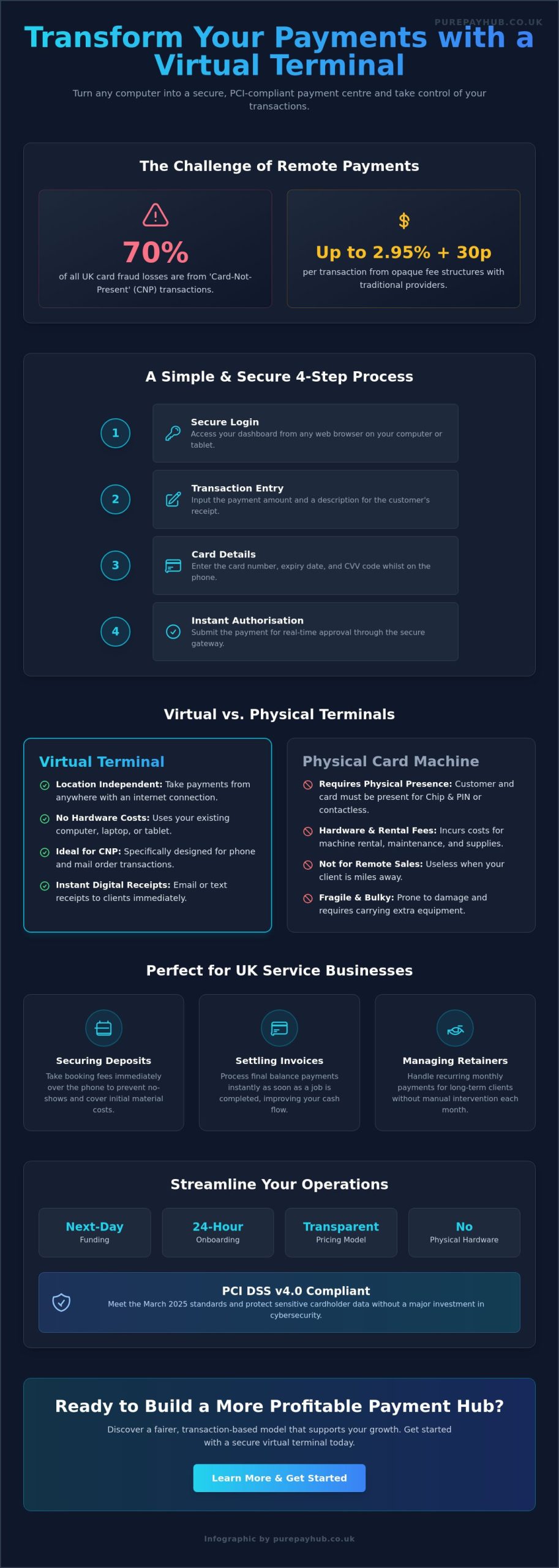

Virtual Terminals as a Backup Plan

A Virtual Terminal is a cloud-based checkout for manual entry. It allows you to turn any device with an internet connection into a secure payment point. You simply log in to your provider’s secure browser-based portal and type in the customer’s card details. This is particularly effective for taking deposits or processing orders over the phone. It’s a professional way to handle transactions whilst you wait for your emergency card machine replacement. Ideally, you should verify that this feature is activated on your account before a crisis occurs, as it provides an instant safety net for your revenue.

Payment Links for Socially Distanced Sales

Payment Links are another powerful tool for maintaining trade. You can create a unique URL for a specific transaction amount in seconds and send it to your customer via SMS, email, or even a QR code. The customer then pays on their own smartphone using their preferred method, such as Apple Pay or Google Pay. This keeps your queues moving and removes the need for physical contact with a terminal. You can track these link payments in real-time through your merchant dashboard, giving you total clarity on your cash flow even without a working card reader on your counter.

For mobile merchants, Tap-to-Pay technology can turn a standard smartphone into a temporary card reader. This allows you to accept contactless payments directly onto your phone. It’s a discreet and efficient way to trade during a hardware emergency. However, no matter which interim method you choose, you must ensure your solution remains PCI compliant. As of 2026, PCI DSS v4.0.1 is the sole active standard. Your provider should handle the heavy lifting of security, but you must remain disciplined about never storing sensitive card data on your own devices. Security shouldn’t be sacrificed for speed, even in a crisis.

Choosing a Provider That Minimises Future Downtime

Securing an emergency card machine replacement is a vital reactive step, but the ultimate goal is to ensure you never face a total blackout again. The reliability of your payment system depends heavily on the infrastructure of your provider. Many legacy banks offer hardware as an afterthought to their main banking services, which leads to slow support and outdated technology. You need a partner that treats payment processing as a mission-critical function. This means prioritising providers that offer “Swap-Out” warranties. Under these agreements, a new unit is dispatched the moment a fault is logged, rather than waiting for a technician to attempt a repair on-site.

Contract flexibility is another essential factor. Avoid being locked into long-term, restrictive agreements with providers that have already failed you during a crisis. If a company cannot meet its service-level agreements during an outage, you should have the freedom to move. A modern provider wins your loyalty through consistent performance and transparent fees, not through fine-print traps. Look for rolling monthly contracts or short-term commitments that keep the pressure on the provider to deliver excellent service every single day.

The Importance of UK-Based Support

When your machine fails on a busy Saturday night, you cannot afford to wait for a support centre in a different time zone to open. UK-based technical support is a non-negotiable requirement for regional merchants. You need to speak with someone who understands the local retail environment and the specific banking regulations that govern UK payments. Direct phone support is always superior to slow, ticket-based systems that leave you in the dark for hours. A quick conversation with an expert can often resolve a configuration issue in minutes, potentially saving you from needing a full emergency card machine replacement.

Technical Resilience in Modern Card Machines

Modern hardware should be built to withstand network failures. Look for multi-comms terminals that feature automatic roaming. These units can switch seamlessly between Wi-Fi and 4G signals if one connection drops out. This dual-path connectivity is essential for portable units used in busy restaurants or at outdoor events. Additionally, consider integrated EPOS systems that offer “offline caching”. These systems can securely store transaction data during a temporary internet outage and process them once the connection is restored. Auditing a provider’s historical uptime is a sensible step before you sign any lease; a dependable partner will be happy to share their reliability record.

If your current provider is letting you down, it is time to switch to a partner that values your business continuity. You can view our range of resilient card machines to find a solution that keeps your payments stable and your queues moving.

Switching to PurePay Hub for Reliable Payment Continuity

When your current system fails, you need more than just a new box on the counter. You need a partner that understands the high-stakes reality of a busy retail environment. At PurePay Hub, we’ve built our service around the needs of regional merchants who can’t afford to wait. We offer an emergency card machine replacement process that focuses on both physical speed and digital readiness. Our team ensures your hardware is dispatched for next-day delivery, but we don’t stop there. We also prioritise next-day funding. This ensures the money you earn today is in your bank account tomorrow, keeping your cash flow stable whilst you transition to a more reliable system.

Traditional banks often treat small business owners as a number in a long queue. We take a different approach. Our onboarding is designed to be punchy and efficient. You won’t be trapped in a cycle of endless paperwork or vague timelines. Instead, you’ll have direct access to account managers who understand that every hour without a terminal is an hour of lost revenue. We believe in straight-talking and fair partnership, ensuring you’re never left in the dark during a technical crisis.

Rapid Setup for UK Businesses

Our streamlined application process is specifically designed to get you back to work. We’ve removed the unnecessary hurdles that legacy institutions often put in your way. By using modern verification tools, we can approve your account in a fraction of the time it takes a traditional bank. PurePay Hub prioritises business continuity through fast-track approval. This means your digital account is often live and ready to process transactions before the courier even arrives with your new device. You get a direct line to experts who prioritise urgent requests, ensuring your emergency card machine replacement is handled with the gravity it deserves.

A Fairer Approach to Merchant Services

Transparency is the core of our identity. We’ve seen the murky fee structures and hidden markups used by legacy providers, and we’ve chosen a cleaner path. There are no opaque charges, even for urgent setups. We also include our Virtual Terminal and Payment Links as standard for every client. These tools act as your permanent safety net, allowing you to take payments over the phone or via SMS if your hardware ever fails again. If you need a capital injection to help your business grow, we also offer a business cash advance based on your card turnover. It’s a flexible way to fund development without the stress of fixed monthly repayments. Restore your payments today with PurePay Hub and experience a service built on honesty, efficiency, and reliability.

Secure Your Trading Future with Resilient Payments

A hardware failure is a stressful event, but it’s also an opportunity to build a more resilient business. By understanding the immediate steps to take and utilising interim tools like Payment Links, you can protect your revenue during a crisis. Ultimately, the impact of a technical fault depends on the agility of your provider. An emergency card machine replacement should be a swift, transparent process that prioritises your continuity over corporate bureaucracy.

You shouldn’t have to settle for slow support or hidden fees when your livelihood is on the line. We provide the stability your business needs with next-day delivery, UK-based expert support, and fair rates starting from 0.3% for debit cards. It’s time to move away from legacy systems that let you down when you need them most. Our goal is to replace frustration with informed confidence.

Get your business back on track with a reliable card machine from PurePay Hub. Take control of your payments today. Ensure you’re always ready to trade, no matter what happens to your hardware.

Frequently Asked Questions

How long does it take to get a replacement card machine?

A replacement typically arrives within 24 hours when you use a provider that offers next-day delivery. Legacy banks often take much longer, sometimes up to 10 working days, which can be devastating for your cash flow. You should always check if your contract includes a swap-out warranty to ensure the fastest possible dispatch. Modern providers prioritise hardware logistics to minimise your downtime.

Can I use my phone as a card machine while I wait for a replacement?

You can use your smartphone to accept payments by utilising Tap-to-Pay technology or generating Payment Links. These digital tools turn your mobile device into a temporary terminal, allowing you to process contactless transactions without physical hardware. It is an excellent way to maintain trading momentum whilst waiting for your emergency card machine replacement. Most modern accounts include these features as standard.

Do I have to pay for a replacement card terminal?

Whether you pay for a replacement depends on your specific merchant agreement and the cause of the failure. Most rental or lease plans include hardware support and free replacements for technical faults. However, if you purchased the machine outright or the damage is accidental, you may need to pay for a new unit. Always review your service-level agreement to see what coverage you have.

Will a replacement machine work with my existing merchant account?

A replacement machine will work with your existing account as long as it is supplied and configured by your current merchant service provider. You cannot simply buy a generic reader from a retail shop and link it to your old account instantly. The hardware must be mapped to your unique merchant ID by your provider’s technical team to ensure secure processing.

What is the fastest way to get a card reader for my business?

The fastest route is to partner with a modern fintech provider that offers next-day hardware delivery and rapid digital onboarding. Whilst some retail shops sell basic card readers over the counter, these still require account approval which can take several days. Choosing a partner that handles both the logistics and the verification in-house is the most efficient solution for a business in a hurry.

Is it possible to get a card machine with same-day activation?

Same-day activation is generally only possible for digital tools like Virtual Terminals and Payment Links. While physical hardware usually requires at least 24 hours for courier delivery, a modern provider can often approve your digital account within a few hours. This allows you to start taking phone or online payments on the very same day you apply for an emergency card machine replacement.

What should I do if my card machine is stolen?

You must contact your merchant service provider immediately to deactivate the terminal and prevent fraudulent use. Because card machines contain sensitive security keys, a stolen unit poses a significant risk to your business data. Once the old unit is blacklisted, your provider will help you secure a replacement and ensure your account remains PCI compliant during the transition.

Can I switch providers if my current terminal is broken?

You can switch providers at any time, and doing so is often the quickest way to escape poor service from a legacy bank. If your current provider is quoting long lead times or charging high fees for support, moving to a specialist can get you back to trading faster. Just ensure you check your existing contract for any notice periods or exit fees before making the move.