Most UK business owners are effectively paying a “confusion tax” every time a customer taps their card. If your merchant statements feel like they are written in a secret code, you are likely overpaying for your processing. Learning how to negotiate lower card processing fees isn’t just about asking for a discount; it’s about reclaiming your margins from opaque billing and hidden PCI non-compliance fines. You deserve to know exactly where every penny of your hard-earned revenue is going.

We understand the frustration of feeling trapped in long-term contracts with escalating rates. It’s exhausting to manage a business whilst worrying about whether your provider is being honest with you. This guide will help you master the art of auditing your merchant statements and provide the exact tactics you need to slash your costs. We’ll explore the latest 2026 interchange caps, identify which markups are actually negotiable, and show you how to secure a transparent, lower effective rate for your business.

Key Takeaways

- Identify your ‘Effective Rate’ to strip away the confusion of complex merchant statements and see your true processing costs.

- Master how to negotiate lower card processing fees by learning to distinguish between fixed interchange caps and flexible provider markups.

- Spot the common ‘red flags’ that drain your revenue, including hidden PCI non-compliance fines and deceptive teaser rates that hide massive markups.

- Follow a disciplined five-step roadmap to audit your data and benchmark your current rates against fair, independent providers.

- Understand why legacy bank ‘rate matching’ is often a temporary fix and how to secure a transparent partnership with modern hardware.

Understanding the Anatomy of Your Merchant Statement

Your merchant statement is often designed to be difficult to read. This isn’t by accident. Traditional providers frequently hide their margins behind a wall of acronyms and complex tables. If you want to learn how to negotiate lower card processing fees, you must first understand what you are actually paying for. Most statements are a layer cake of fixed costs and flexible markups. By the time you finish this section, you will know exactly which layers you can trim away.

In 2026, statements look slightly different due to the recent Visa and Mastercard antitrust settlements. These changes have introduced a 0.10% reduction in average interchange rates. Whilst this sounds like a win for merchants, many providers have simply absorbed this saving into their own margins. You need to verify that these reductions are being passed on to you rather than lining your processor’s pockets.

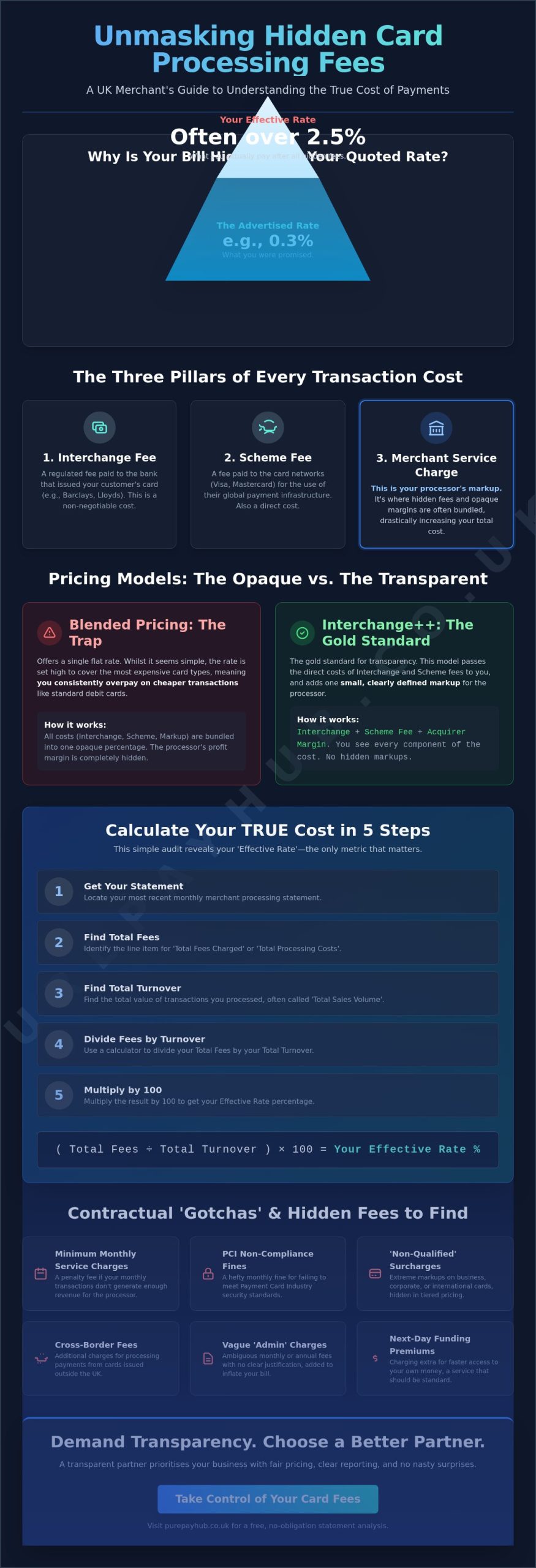

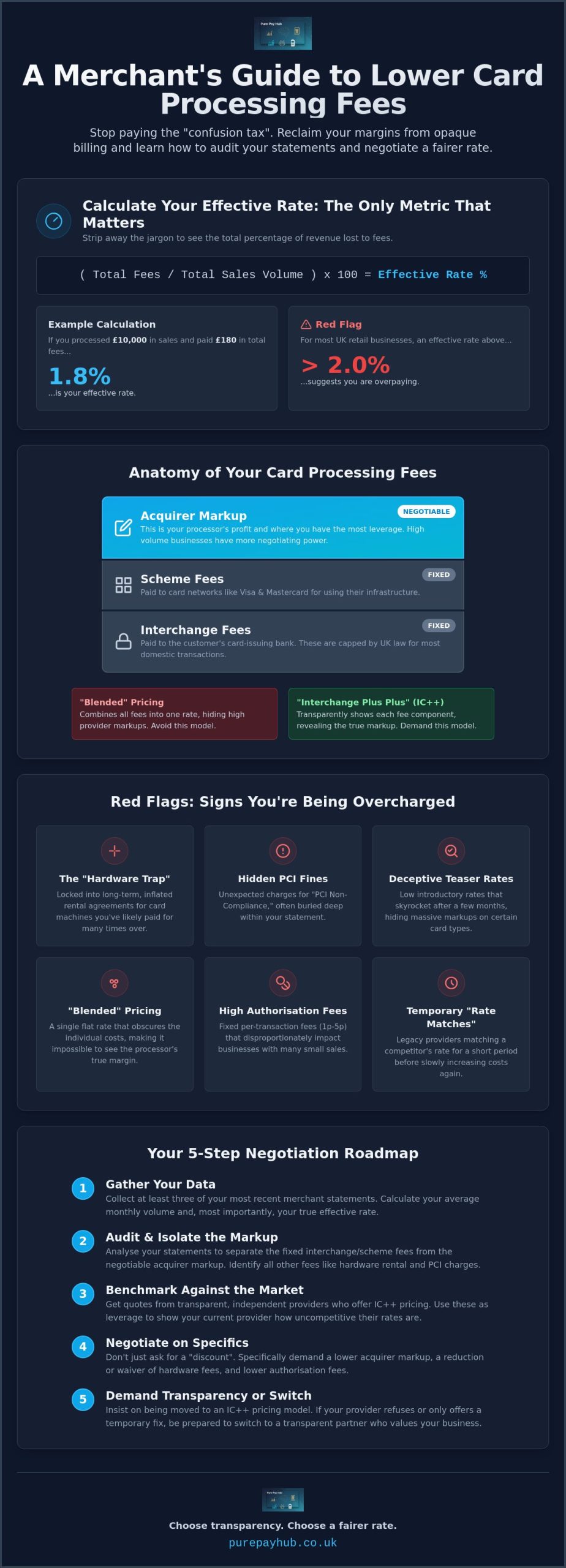

Calculating Your Effective Rate

The effective rate is the only metric that truly matters for your bottom line. It strips away the jargon and shows you the total percentage of your revenue lost to fees. To find it, use this simple formula: (Total Fees / Total Sales Volume) x 100. For example, if you processed £10,000 in sales and paid £180 in total fees, your effective rate is 1.8%. To help you with these calculations, you can check out LyrxPay for a detailed merchant audit checklist.

An effective rate above 2% is a red flag for most UK retail businesses and suggests you are likely overpaying for your merchant services. When performing this calculation, look closely at the “VAT on fees” line item. If your business is VAT-registered, you can often reclaim this cost; ignoring it means you are miscalculating your true overheads. PurePay Hub prioritises this level of clarity from day one, ensuring you never have to guess what you are paying.

Interchange vs. Scheme Fees

Every transaction includes non-negotiable costs. Interchange fees are paid to the card-issuing bank and are capped by law for most domestic transactions. Scheme fees are paid directly to Visa or Mastercard for the use of their networks. Since Brexit, cross-border transaction costs for EEA cards have risen, making it vital to check how your provider categorises these “pass-through” costs.

The third layer is the Acquirer Markup. This is the fee your provider charges for processing the payment and providing your countertop card machines or portable devices. This markup is the primary area where you have leverage. Understanding how to negotiate lower card processing fees relies on isolating this markup. If your provider uses a “Blended” pricing model, they are likely hiding a high markup behind a single, flat rate. Switching to an “Interchange Plus Plus” (IC++) model provides the transparency needed to see the raw costs versus the provider’s profit, making it much easier to demand a fairer deal.

Identifying Negotiable vs. Fixed Processing Costs

Not every line on your merchant statement is set in stone. When you are looking at how to negotiate lower card processing fees, you must separate the “untouchables” from the “negotiables”. Card networks like Visa and Mastercard set the interchange rates, which are largely fixed by UK regulation. Your Merchant Category Code (MCC) also dictates a baseline; a high-risk industry like travel will always have a higher starting point than a local grocer. However, almost everything else is up for discussion.

The “Hardware Trap” is a common drain on UK businesses. Many legacy providers lock you into long-term rental agreements for your countertop card machine or portable devices. These monthly fees are often inflated. If you have been with a provider for several years, you have likely already paid for the hardware many times over. Demand a reduction in rental costs or ask for the fees to be waived entirely as part of your renewal. Challenging these recurring costs is a quick win for your cash flow.

Authorisation fees are another area where small-ticket merchants are often penalised. These are flat fees, often ranging from 1p to 5p, charged on top of the percentage rate. If you run a coffee shop or a newsagent, these flat fees can significantly increase your effective rate. You should aim to negotiate these down to the lowest possible fraction, as they represent pure profit for the processor.

The Acquirer Markup: Your Primary Leverage

The acquirer markup is the slice of the pie your processor keeps for themselves. This is your biggest point of leverage. High-volume businesses have more room to squeeze this margin because the processor’s operational cost remains the same regardless of your turnover. Understanding how to get the lowest fees involves benchmarking this markup against industry standards. At PurePay Hub, we advocate for a transparent structure where markups on debit cards stay low, reflecting the lower risk and cost of those transactions compared to premium credit cards.

Ancillary Fees: The “Hidden” Negotiation Points

Beyond the headline percentage rates, “junk fees” often quietly erode your profits. Look for the Minimum Monthly Service Charge (MMSC). If your transaction volume is high enough, this should be waived entirely. Similarly, statement fees, portal fees, and vague “admin” charges are often legacy costs that modern providers have abolished. If you use a virtual terminal for phone payments, check the per-transaction authorisation fee. Everything from your portable card machine rental to your PCI management fee is a variable that can be challenged. Mastering these details is the secret to how to negotiate lower card processing fees effectively.

Spotting the Red Flags: Signs You Are Being Overcharged

Identifying overcharging requires a sharp eye for detail. Many providers rely on the fact that you are too busy running your business to scrutinise every line of your monthly statement. If you want to master how to negotiate lower card processing fees, you must first identify the “hidden” revenue streams your processor is using to inflate their margins. These aren’t always obvious percentage markups; often, they are disguised as administrative necessities or compliance requirements.

Teaser rates are a classic industry trap. A provider might offer a “0.1% debit rate” to get you through the door, but this headline figure is rarely the whole story. They often compensate for this low rate by applying massive markups to credit cards, business cards, or international transactions. You might also notice inconsistent billing, where your rates slowly creep upwards over several months without any formal notification. This “fee creep” is a clear sign that your provider prioritises their profit over your partnership.

Chargeback fees are another area of concern. Whilst processors do face risks with disputed transactions, an “admin fee” of £25 or £50 for a single chargeback is often excessive. If these costs far outweigh the actual risk or administrative effort involved, it’s time to challenge them. A fair partner should support you through disputes, not use them as an excuse to drain your account. Learning how to negotiate lower card processing fees effectively involves identifying these redundant charges before you even pick up the phone to your account manager.

The PCI Compliance Revenue Stream

The PCI non-compliance fine is perhaps the most frustrating “junk fee” in the industry. Many providers charge between £20 and £50 every single month simply because a merchant hasn’t completed their Self-Assessment Questionnaire (SAQ). This is essentially a tax on your lack of paperwork. You can stop these fines immediately by completing the simple online SAQ, which proves your business handles card data securely.

A transparent provider should help you achieve compliance rather than profiting from your failure to do so. Look for “PCI Management Fees” on your statement. If you are paying for “management” but still receiving “non-compliance fines,” you are being charged twice for the same service. PurePay Hub believes in advocacy; we help you stay compliant so you can keep more of your revenue.

The ‘Junk Fee’ Audit

Your audit should also look for markups on “Dues and Assessments.” These are fees paid to the card schemes, but some processors add a small, hidden margin on top of what Visa and Mastercard actually charge. You should also check for “Gateway Access Fees” that might overlap with your existing EPOS subscription, effectively charging you twice for the same digital bridge. Next-day funding should be a standard feature of a modern merchant account, not a premium add-on that costs extra.

The Negotiation Roadmap: 5 Steps to Lower Rates

Negotiation is a structured process, not a casual conversation. If you want to master how to negotiate lower card processing fees, you must approach your provider with data rather than just a complaint. Start by gathering three months of recent merchant statements. This evidence proves your sales volume and your history of “Good Standing.” It shows the provider exactly what they stand to lose if you walk away. A provider is far more likely to listen when you can demonstrate exactly how much revenue you are moving through their systems.

Benchmark these statements against independent ISOs like PurePay Hub. Independent providers often have lower overheads than legacy banks and can offer more competitive margins. Use your seasonal peaks as leverage; if your turnover doubles in December, use that volume to negotiate lower minimum monthly requirements for the quieter months. This approach ensures your costs remain manageable during your slower periods.

Preparing Your Benchmarking Data

When seeking a “Like-for-Like” quote from a competitor, keep your current rates private initially. Let the new provider offer their best deal based on your volume alone. If you reveal your current pricing too early, they may only offer a marginal improvement. Instead, wait for their quote, then use it as a weapon in your primary negotiation. This ensures you are seeing the true market value of your processing and prevents the competitor from simply “beating it by a penny.”

To streamline this benchmarking process and find the most competitive alternatives, you can discover PaySelect to compare and select the most suitable payment gateways and systems for your needs.

The Negotiation Script: What to Say

Don’t waste time with general customer service. Ask to speak directly with the “Retention Department” or the “Cancellations Team.” These staff members have the authority to override standard pricing models. Use specific phrases like “I am currently reviewing my business overheads” rather than making an immediate threat to leave. This keeps the tone professional and collaborative whilst signalling that you are a savvy operator.

If they offer to “match” a competitor’s rate, be cautious. A rate match is often a silent admission that they have been overcharging you for years. Ask for a comprehensive “Service Review” instead of just a “Rate Cut.” Demand that the new pricing includes modern hardware and a “No-Increase” guarantee for the next 12 to 24 months. If your provider refuses to be transparent, it’s time to switch to a fair partner who values your business from the start.

You can also leverage your future growth. If you are considering a Business Cash Advance to expand your premises or buy stock, mention this. Providers are more likely to offer better processing rates if they see the potential for a long-term, multi-service relationship. Always ensure the final agreement is delivered in writing before you agree to stay. Verbal promises rarely survive the next billing cycle.

When Negotiation Fails: Switching to a Transparent Partner

Negotiation doesn’t always lead to the result you deserve. If your bank offers to match a competitor’s quote, you should be wary. This “rate matching” is often a temporary tactical move to prevent you from leaving. It rarely addresses the underlying issue of “fee creep,” where new, obscure charges appear a few months later to recoup the lost margin. Independent providers offer a fairer alternative. They provide personalised service and modern hardware, like a portable card machine that actually works for your specific business layout.

The Switching Process Simplified

Many business owners stay with expensive providers because they fear the transition. It doesn’t have to be difficult. First, check your current “Exit Fees.” If you have been with a provider for several years, these can often be negotiated down or waived entirely by citing poor service or a lack of transparency. When moving, set up your new hardware in parallel. You can test your new countertop card machine whilst your old one is still active. This ensures there is zero downtime for your customers. Modern systems also offer seamless integration with your accounting software, ensuring your bookkeeping remains accurate throughout the switch.

Why Transparency Trumps ‘The Lowest Rate’

Chasing the absolute lowest rate can sometimes lead you back to a provider who uses teaser rates to hide markups. Real value lies in transparency. Clear, digital reporting allows you to see every transaction and its associated cost in real-time. This level of clarity acts as a stabilising force for your finances. Next-day access to funds is another critical factor. At PurePay Hub, next-day funding is a standard feature, not a premium extra. This improves your business’s agility, allowing you to reinvest your revenue immediately rather than waiting for a banking cycle to clear.

Learning how to negotiate lower card processing fees gives you the power to demand better. However, if your current provider refuses to move away from opaque billing, don’t be afraid to walk away. PurePay Hub positions itself as a long-term partner for your business growth, offering debit rates starting at 0.3% and credit from 0.5%. We prioritise honesty over corporate jargon. Our goal is to alleviate the stress of hidden costs, providing a dependable foundation for your regional business to thrive.

Take Control of Your Merchant Margins

Mastering how to negotiate lower card processing fees is about more than just chasing a cheaper rate; it’s about establishing a relationship built on transparency. You now have the tools to audit your statements, identify hidden non-compliance fines, and approach your provider with data-driven confidence. Your merchant category and sales volume are powerful leverage points. Use them to challenge markups and protect your revenue from “fee creep” or legacy bank tactics.

If your current provider refuses to offer the clarity you need, it’s time to choose a partner who values your business growth. PurePay Hub provides a fair alternative with debit rates starting from 0.3% and the essential benefit of next-day funding. Our expert UK-based support team is here to ensure you never feel lost in financial jargon again. You’ve worked hard to build your business; don’t let opaque fees quietly drain your success.

Get a transparent, no-obligation quote from PurePay Hub today and start keeping more of what you earn. Your bottom line deserves a fairer deal.

Frequently Asked Questions

Are card processing fees legally negotiable in the UK?

Yes, the acquirer markup portion of your fees is entirely negotiable in the UK. While interchange fees and scheme fees are set by card networks and regulators, the margin added by your processor is flexible. Understanding this distinction is the first step in learning how to negotiate lower card processing fees. You have the right to challenge any fee that isn’t a fixed, pass-through cost from the card networks.

What is a ‘good’ merchant service charge for a small business in 2026?

A competitive merchant service charge varies based on your industry and sales volume, but a total effective rate under 2% is a strong benchmark for most UK retailers. You should look for debit rates starting from 0.3% and credit from 0.5%. Avoid providers who offer a low headline rate only to inflate costs with hidden administrative charges or premium card markups elsewhere on your statement.

How often should I negotiate my card machine rates?

You should review and negotiate your rates every 12 to 18 months. This prevents “fee creep” from quietly eroding your margins over time. If your business experiences a significant increase in turnover, don’t wait for the annual review. Use your higher sales volume as immediate leverage to secure a better deal. Regular audits ensure your provider remains a fair partner as your business grows.

Can I negotiate my PCI compliance fees?

You can absolutely negotiate or eliminate PCI compliance costs. Non-compliance fines are optional charges that vanish once you complete your annual Self-Assessment Questionnaire (SAQ). If you are paying a “PCI Management Fee,” ask your provider what specific service they are performing. Transparent partners like PurePay Hub help you achieve compliance rather than using it as a way to generate extra revenue from your business.

Does my business volume affect my ability to negotiate?

Your total transaction volume is your greatest piece of leverage during negotiations. Processors have fixed operational costs; they are often willing to accept a smaller percentage markup on high-volume accounts to secure the business. Demonstrating consistent growth or seasonal peaks can help you squeeze the acquirer’s margin. This is a core tactic when learning how to negotiate lower card processing fees for an expanding business.

What happens if I want to switch providers but I’m in a contract?

Switching while in contract requires a careful review of your exit fees and notice periods. You can often negotiate with your current provider to waive these fees if you can prove they haven’t met service standards. Alternatively, some new providers may offer incentives to help offset the cost of leaving a legacy contract. Always get a full breakdown of any termination costs in writing before making a final decision.

Is it cheaper to have a blended rate or Interchange Plus Plus?

Interchange Plus Plus (IC++) is generally cheaper and far more transparent than a blended rate. Blended pricing simplifies your statement into a single flat rate, but this often hides a significant markup for the processor. IC++ breaks down every cost, allowing you to see the exact interchange fee and the provider’s margin. This transparency makes it much easier to identify where you are being overcharged.

Do online payment gateway fees follow the same negotiation rules?

Online payment gateway fees follow the same negotiation principles as physical card machines. The gateway provider’s markup and the per-transaction authorisation fees are both flexible. If you process a high volume of online sales, you should benchmark these costs against independent providers. Bundling your online gateway with your portable card machine services can also provide additional leverage to secure a lower overall rate.