How much of your hard-earned Friday night profit is disappearing into opaque transaction fees before the weekend even starts? You likely know the frustration of thin margins being eaten away by hidden charges and the stress of system downtime during a peak dinner rush. It’s common to feel that your current setup, with its fragmented reporting between the till and the card machine, is holding your business back rather than helping it grow.

Choosing the right restaurant EPOS system UK for 2026 can change that by slashing transaction costs and finally uniting your front-of-house with the kitchen. We promise to show you how to select an integrated solution that provides next-day access to your funds, lowers your merchant service charges, and ensures your operations run seamlessly. This guide explores the latest hardware and software strategies to help you reclaim your margins whilst maintaining the transparency your business deserves. You’ll learn how to move from a state of frustration to one of informed confidence, ensuring your technology acts as a supportive partner in your success.

Key Takeaways

- Understand how to transition from a basic till to an integrated ecosystem that manages payments, staff, and stock from one central hub.

- Identify the essential features for a restaurant EPOS system UK, including floor plan customisation and Kitchen Display Systems that reduce order errors.

- Learn to calculate the Total Cost of Ownership by contrasting fixed hardware costs with variable merchant service charges to protect your margins.

- Discover the steps to ensure a seamless transition between providers without experiencing system downtime or losing a single night of trade.

- Leverage transparent transaction rates as low as 0.3% for debit and 0.5% for credit to turn every payment into a growth opportunity.

What is a Restaurant EPOS System and Why is it Critical in 2026?

A What is a Point of Sale (POS) system is no longer just a box for holding cash. In 2026, a restaurant EPOS system UK acts as the central nervous system of your entire hospitality business. It’s the point where every customer interaction, kitchen order, and stock adjustment meets. The days of simple, standalone tills are over. Modern owners have transitioned toward integrated ecosystems that manage payments, staff scheduling, and inventory in one place. This shift is critical because 2026 brings unique pressures. With rising operational costs and thin margins, you need real-time data synchronisation to make informed decisions. You aren’t just managing a till anymore; you’re optimising a digital business partner that works as hard as you do.

The Evolution of Hospitality Tech: From Tills to Ecosystems

Legacy setups often relied on standalone card machines that didn’t talk to the till. This created fragmented reporting and endless manual reconciliation. Modern EPOS systems remove this friction entirely. Because they’re cloud-based, you can monitor your restaurant’s performance from your phone whilst away from the site. This transparency is vital for spotting waste or staffing issues early. In a high-inflation economy, the speed of your cash flow is also paramount. Integrated systems provide next-day access to funds, ensuring your business stays liquid and ready for the next delivery. This reliability helps alleviate the stress that business owners feel regarding complex fee structures and delayed payments.

Why “Good Enough” is No Longer Enough for UK Restaurants

Consumer behaviour has changed rapidly. Statistics from early 2026 show that contactless payments now account for 92% of all hospitality transactions. If your system is slow or prone to downtime, you’re directly hurting your table turnover. A laggy interface during a peak Friday night doesn’t just frustrate staff; it costs you covers. Security is another non-negotiable factor. With PCI DSS v4.0.1 now being the sole supported standard as of 2025, using outdated tech risks monthly non-compliance fines. A modern restaurant EPOS system UK keeps you compliant automatically, protecting your reputation and your revenue. By prioritising clarity and efficiency, you ensure your technology supports your growth rather than acting as a bottleneck.

Essential Features Every UK Restaurant EPOS Must Have

The best systems don’t just process payments; they orchestrate the entire floor. A robust restaurant EPOS system UK provides a clear, customisable floor plan that acts as the foundation for your service speed. Your staff should be able to see, at a glance, which tables are waiting for drinks, which are mid-course, and which are ready for the bill. This visual clarity prevents bottlenecks and ensures no customer is left waiting during a frantic shift. Beyond the floor plan, your system must offer granular inventory tracking. With food prices remaining volatile in 2026, knowing your exact cost-per-dish is the only way to protect your margins. Every ingredient should be accounted for, from the premium steaks to the garnish.

Front-of-House Efficiency: Table Management and Mobile Ordering

Speed at the table is the heartbeat of a busy shift. By adopting restaurant industry technology trends like mobile tableside ordering, you eliminate the constant back-and-forth to a central terminal. Waitstaff can send orders directly to the kitchen the moment they are taken; this significantly reduces lead times and improves order accuracy. For weekend diners, split-billing features are no longer optional. Customers expect to pay for exactly what they had without a mathematical debate at the end of the night. These tools also allow you to build a database of your guests. Recognising a favourite customer’s previous order or dietary preference builds the kind of loyalty that keeps a local business thriving.

Back-of-House Control: Inventory and Kitchen Integration

Your kitchen is where your margins are won or lost. A Kitchen Display System (KDS) replaces messy paper tickets with clear, digital prompts that reduce errors and food waste. These screens ensure the kitchen team receives orders the second they are placed, keeping the rhythm of service steady. Integration with your inventory is equally vital. When a burger is sold, your system should automatically deduct a bun and a patty from your stock levels in real-time. Automated low-stock alerts prevent the awkwardness of a server having to tell a guest that a menu item is unavailable mid-service. This level of control allows you to run a leaner, more profitable operation. If you are looking to upgrade, choosing a modern EPOS system can help you centralise these complex tasks into one manageable dashboard.

Managing your team effectively requires more than just a paper rota. Modern systems include staff management tools that track individual performance and handle shift scheduling. You can see which servers are upselling effectively and which shifts require more support. By identifying these patterns, you can optimise your labour costs whilst ensuring your best staff are rewarded. This data-driven approach turns your EPOS from a simple tool into a strategic asset for your restaurant’s long-term growth.

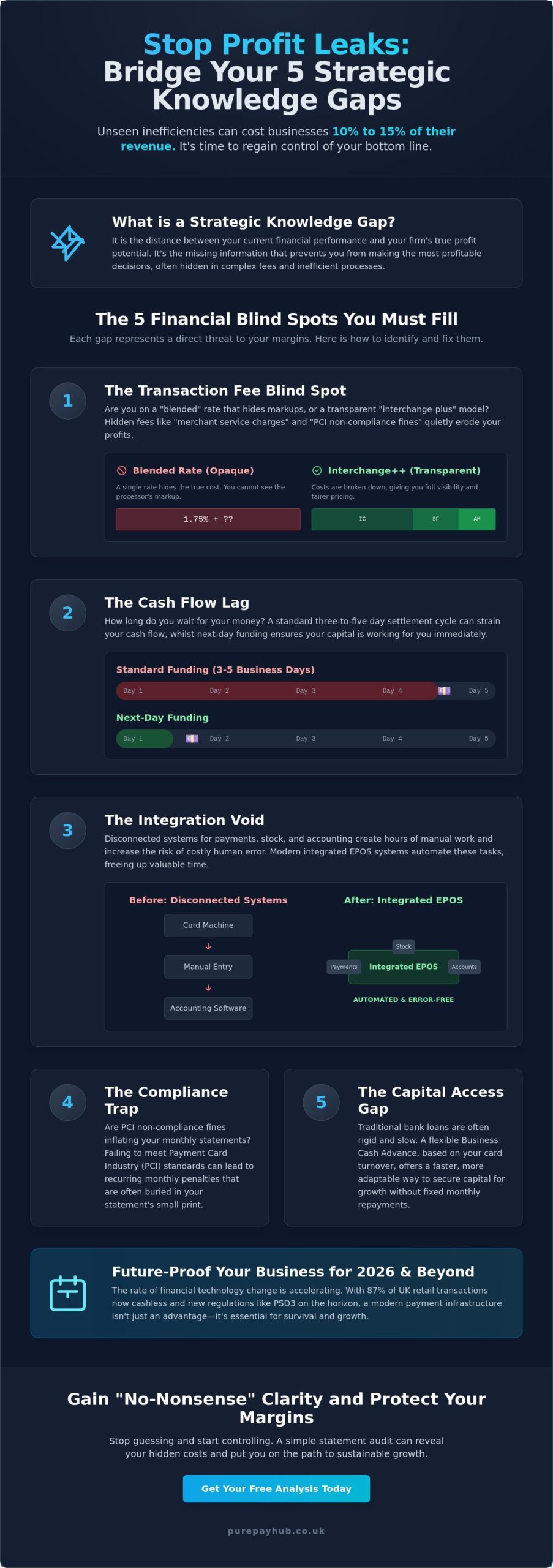

Calculating the Real Cost: Software Fees vs. Transaction Rates

Finding the most cost-effective restaurant EPOS system UK requires looking past the initial sales pitch. You must evaluate the Total Cost of Ownership (TCO) to understand how much money actually leaves your bank account each month. Many owners focus on the hardware price or the software subscription whilst ignoring the variable merchant service charges that follow. These transaction fees are often the largest expense in your technology stack. The effective rate is the true measure of payment processing costs; it represents your total monthly fees as a percentage of your total sales volume.

A transparent financial strategy balances fixed and variable costs. Fixed monthly hardware rentals provide predictability, but they shouldn’t be bundled with opaque processing terms. You need a partner that identifies every cost clearly, from the terminal lease to the per-transaction markup. This clarity helps you move from a state of frustration regarding hidden fees toward a state of informed confidence in your margins. Your technology should be a stabilizing force for your business finances, not a source of unexpected overheads.

The Trap of “Free” EPOS Software

Entry-level providers often lure business owners with the promise of “free” software. This is frequently a financial trap that punishes your success. These systems usually carry high transaction rates of 1.75% or more, which can cost a thriving restaurant thousands of pounds in unnecessary fees. For a restaurant with a £20,000 monthly turnover, a “free” system at a 1.5% rate costs you £300 a month. Conversely, a paid system with a £50 monthly fee and a 0.3% rate costs you only £110 in total. The “free” option is actually £190 more expensive every single month. You should also insist on next-day access to funds as a standard feature. In a fast-moving hospitality environment, waiting days for your own money is an outdated practice you don’t have to accept.

Understanding Merchant Service Charges (MSC)

Transparency in Merchant Service Charges (MSC) is the no-nonsense approach every owner should demand. You deserve to know exactly what you’re paying for debit and credit transactions. Fair rates, such as those from PurePay, typically start around 0.3% for debit cards and 0.5% for credit cards. These small differences in percentage points can save you enough to hire another staff member or upgrade your kitchen equipment over the course of a year. Avoid long-term contracts that hide annual fee increases or exit penalties. A supportive business ally won’t need to lock you in with complex legalese; they’ll keep your business through fair service and honest pricing. By prioritising these clear fee structures, you ensure your technology acts as a growth engine rather than a drain on your resources.

Organising a Seamless Transition to Your New System

Switching your restaurant EPOS system UK shouldn’t feel like a leap into the dark. It’s a strategic move. It requires a structured plan to avoid losing a single night of trade. Many owners worry about the administrative headache of setting up new technology during a busy season. The right partner makes this transition effortless by prioritising clarity over complexity. You need a system that stabilises your finances from day one. This transition follows a simple logic: identify the bottlenecks in your old setup and configure the new one to solve them. It’s about improvement, not just replacement.

Data Migration: Moving Your Menu and Stock

Moving your data is the perfect time for a digital spring clean. Audit your current menu before you start the import. Remove unpopular items that clutter your interface and slow down your servers. This ensures a clean import into your new setup. Crucially, you must map your VAT categories correctly. This keeps you compliant with HMRC and prevents accounting errors later. Generic global advice often ignores these UK-specific banking and tax requirements. A provider that offers dedicated technical support during this phase prevents costly mistakes. They help you bridge the gap between your old till and your new integrated ecosystem whilst ensuring your historical data remains accessible for year-end reporting.

Staff Buy-In: Training for Peak Performance

Your staff use the system during the frantic Saturday night rush. They need an interface that makes sense immediately. A punchy, intuitive design reduces the learning curve for new hires and seasoned veterans alike. Don’t go live without a mock service. Run a practice shift with your team to test the workflow. This builds the confidence your team needs to handle high-pressure situations without hesitation. Once live, use the granular reporting to reward your most efficient performers. You can see which staff members are upselling effectively or managing their tables with the most speed. This turns a technical change into a motivational tool for your entire team.

A successful transition relies on a partner who values your time and your margins. You deserve a system that is as disciplined and professional as your kitchen. By following a clear onboarding framework, you can upgrade your technology without the stress usually associated with new software. If you’re ready to leave behind opaque fees and fragmented reporting, you can switch to a more transparent EPOS system today and start reclaiming your hard-earned profits.

Why PurePay Hub is the Growth Engine for UK Restaurants

PurePay Hub acts as a stabilising force for your restaurant’s finances. In an industry often viewed with scepticism, we provide a transparent alternative to the opaque practices of traditional banks. Choosing our restaurant EPOS system UK means you aren’t just buying hardware; you’re entering a disciplined partnership. We offer 0.3% debit and 0.5% credit transaction rates to ensure your margins remain protected. This clear fee structure allows you to forecast your overheads with absolute certainty. Our goal is to alleviate the stress that business owners feel regarding hidden costs and complex markup models.

Integrated Payments and Next-Day Funding

Integrated payments remove the frustration of manual entry on card machines. When your till and your terminal speak the same language, human errors disappear. This efficiency is supported by our range of Countertop Card Machines and Portable Card Machines, designed to suit any restaurant layout. We believe in calm advocacy for our partners, which is why next-day access to your funds is a standard feature. You shouldn’t have to wait for your own money to arrive whilst your suppliers need paying. By prioritising your cash flow, we ensure your technology acts as a supportive ally rather than a bottleneck.

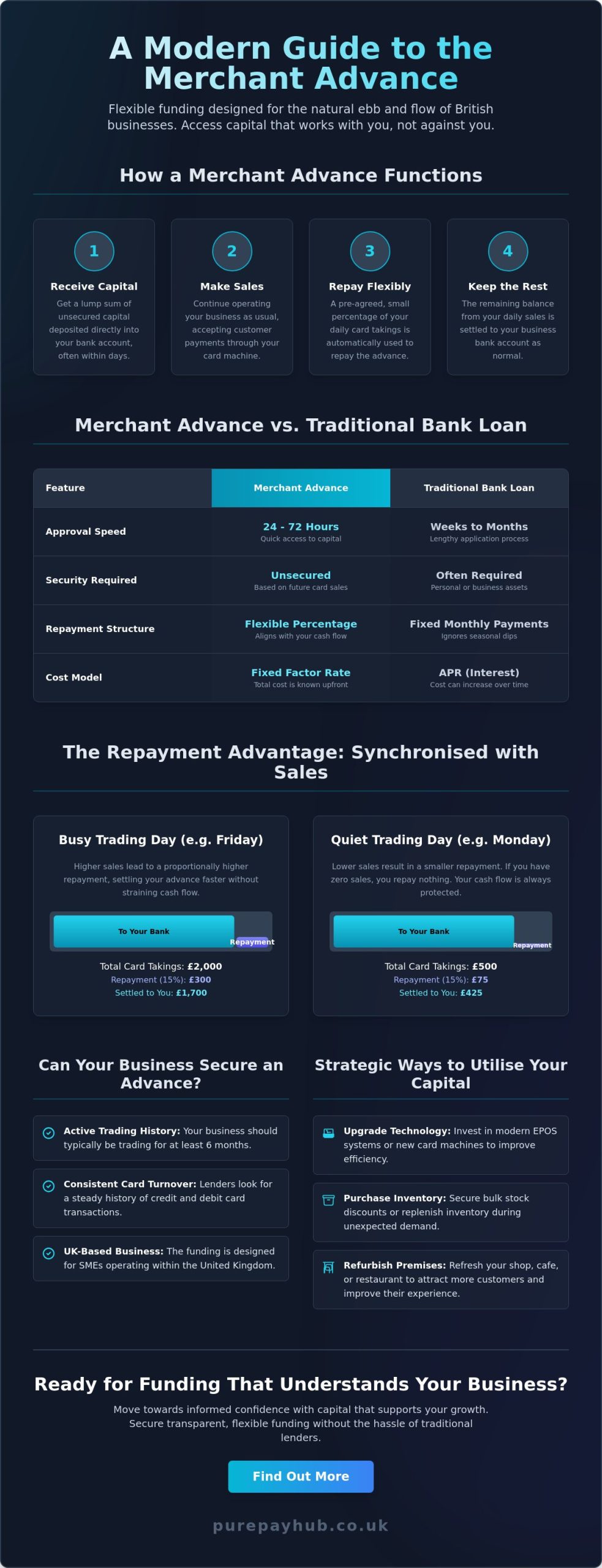

Unlocking Capital with Business Cash Advances

We understand that growth requires capital, but traditional bank loans are often too rigid for the hospitality sector. Our Business Cash Advance allows you to use your future card sales to secure unsecured capital today. This is a game-changer for owners planning refurbishments or kitchen upgrades. Unlike bank loans with fixed monthly repayments, this model follows a “pay-as-you-earn” structure. Your repayments are a small, agreed percentage of your daily card sales. If you have a quieter week, your repayments automatically reduce. It’s a flexible, no-nonsense way to fund your expansion without the pressure of traditional debt cycles.

Our focus remains on the individual business owner. We disdain hidden markups and corporate jargon, choosing instead to lead our partners toward a state of informed confidence. By centralising your payments, your reporting, and your funding, we help you lead your business with a clear head. You deserve a partner that values efficiency and straight-talking as much as you do. You can organise a transparent rate review with PurePay Hub today to discover how much your business could save.

Reclaiming Your Margins in 2026

The right technology should be a stabilising force for your finances, not a source of stress. You’ve seen how a modern restaurant EPOS system UK acts as a central nervous system, uniting your front-of-house with the kitchen whilst protecting your hard-earned margins. By looking past the trap of “free” software and focusing on transparent transaction rates, you can turn every payment into a growth opportunity. Whether you’re streamlining a single site or planning a multi-venue expansion, the path to a more profitable 2026 starts with clarity and integrated reporting.

We are here to act as your fair partner in an industry that often feels opaque. You deserve a setup that offers next-day funding as standard and provides no-nonsense, UK-based support when you need it most. It’s time to stop letting hidden fees eat into your success. We provide debit rates from 0.3% and credit rates from 0.5% to ensure you keep more of what you earn every single day.

Switch to PurePay Hub for 0.3% rates and integrated EPOS

Take the next step toward a more efficient, profitable future for your restaurant. Your success is our priority.

Frequently Asked Questions

How much does a typical restaurant EPOS system cost in the UK?

The total cost depends on your specific hardware needs and the number of terminals required for your floor plan. You will typically encounter a combination of upfront hardware costs for screens and printers; a monthly software subscription fee; and variable transaction rates. It is vital to look at the total cost of ownership rather than just the initial price tag to ensure your margins remain protected from hidden markups.

Can I keep my existing card machine when I switch EPOS providers?

You can technically use a standalone card machine, but you will lose the significant advantages of an integrated restaurant EPOS system UK. Integrated systems allow your till and terminal to communicate directly; this removes the need for manual data entry and prevents reconciliation errors at the end of a shift. Switching to a unified provider usually simplifies your reporting and results in faster access to your funds.

What is the difference between an EPOS system and a standard cash register?

A standard cash register is a passive tool for recording sales and storing cash; an EPOS system is an active partner that helps you optimise your entire business. It tracks inventory in real-time, manages staff rotas, and provides granular data on your most profitable dishes. Whilst a till only handles the final transaction, an EPOS system orchestrates everything from the initial order to the final kitchen prompt.

How long does it take to install a new restaurant EPOS system?

A standard installation usually takes between one and three days depending on the size of your venue and the complexity of your menu. This period includes the physical setup of your terminals and a dedicated training session to ensure your team is confident before the first live service. Choosing a partner that prioritises quick onboarding helps you transition between systems without losing a single night of trade.

Do I need a specific internet speed to run a cloud-based EPOS?

Stability is more important than raw speed; most cloud-based systems run perfectly on a standard fibre connection with speeds of 10-20Mbps. You should ensure your Wi-Fi coverage is consistent across your entire dining area to support portable card machines for tableside ordering. We recommend using a dedicated network for your business operations to keep your connection fast and secure during peak periods.

Is a business cash advance better than a traditional bank loan for my restaurant?

A business cash advance offers more flexibility for the hospitality sector because repayments are based on a small percentage of your daily card sales. This “pay-as-you-earn” model means you pay back less during quieter weeks, which protects your cash flow. Traditional bank loans require rigid monthly payments regardless of your turnover; this can create unnecessary financial pressure during the off-season or slower months.

What happens if my internet goes down during service?

Modern systems include an offline mode that allows you to continue taking orders and processing payments even if your connection drops. All data synchronises automatically once your internet is restored. This feature ensures that a temporary technical glitch doesn’t disrupt your service or lead to lost revenue during a busy Friday night rush. Your business remains operational and your data remains secure.

How does an integrated EPOS help with HMRC and VAT reporting?

An integrated restaurant EPOS system UK automatically maps every sale to the correct VAT category; this ensures your reporting is accurate and fully compliant with HMRC requirements. You can export clean, professional data directly into your accounting software, which saves hours of manual reconciliation for your bookkeeper. This level of transparency provides you with an effortless audit trail and total confidence in your financial records.