Why should your business be forced to pay the same fixed loan instalment during a quiet Tuesday in February as it does during the peak December rush? Most UK merchants find that traditional bank lending is far too rigid for the modern market. If you are looking for a more flexible alternative, a business cash advance based on card sales offers a financial solution that actually mirrors your daily turnover. You already know the stress of complex applications and the fear of high fixed costs during slow trading months. We are here to change that dynamic with a fairer approach to funding.

In this guide, you will discover how to secure unsecured capital within 72 hours through a process built on transparency and speed. We will explain how to access a repayment structure that breathes with your sales volume, ensuring your repayments always match your actual cash flow. We will also break down our clear fee structure, giving you the clarity needed to invest in stock, repairs, or growth with complete confidence. It is time to move away from the frustration of high-street banks and toward a partnership that supports your business through every peak and trough.

Key Takeaways

- Learn how a business cash advance based on card sales provides an unsecured injection of capital that moves in sync with your daily turnover.

- Discover the “breathing” repayment model where you pay back more on busy days and less during quiet periods, protecting your vital cash flow.

- Understand the no-nonsense application process that requires minimal documentation and rewards established UK merchants with fast, flexible funding.

- Identify the most effective revenue-generating ways to use your capital, from securing seasonal stock to investing in essential equipment upgrades.

- See how integrating your funding with PurePay Hub’s countertop card machines creates a transparent and seamless partnership for business growth.

What is a Business Cash Advance Based on Card Sales?

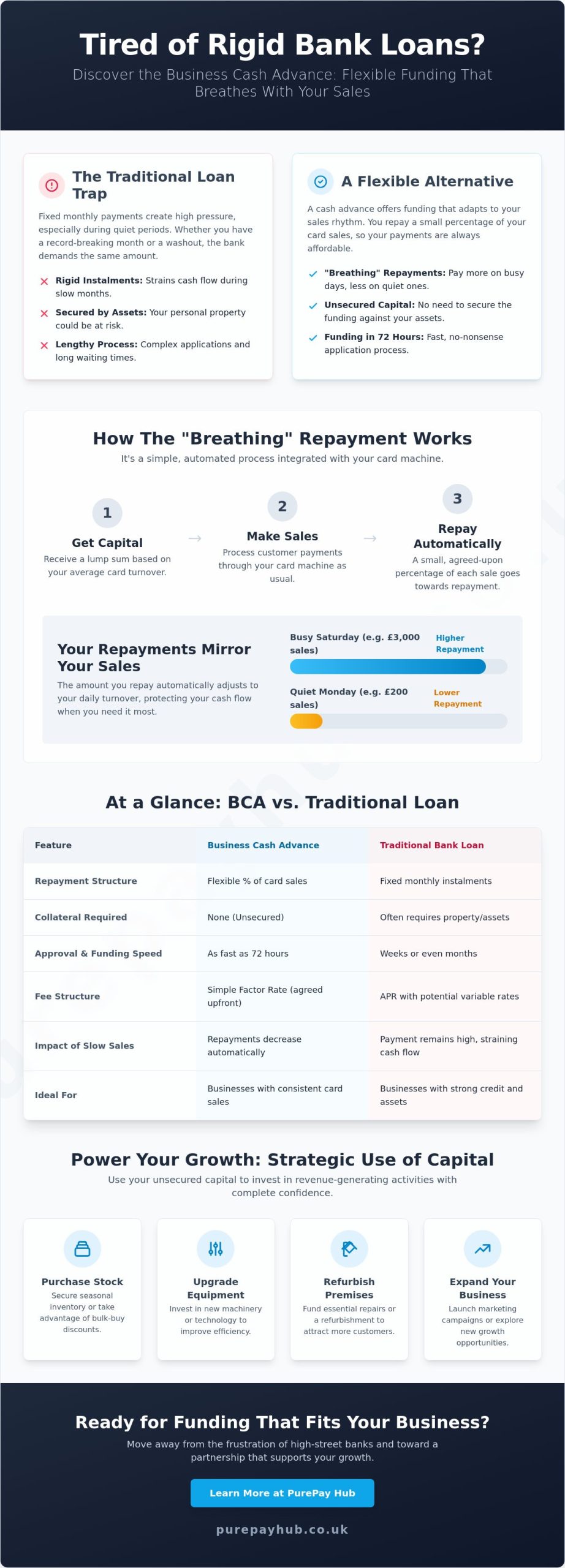

A business cash advance based on card sales provides a flexible alternative to restrictive bank funding. It’s an unsecured injection of capital built entirely on your future credit and debit card turnover. Instead of a bank manager demanding a charge over your property, this model looks at your terminal’s performance. You receive a lump sum upfront, and you pay it back as a small percentage of every card transaction you process.

This funding isn’t a loan in the legal sense. It is technically a “purchase of future sales” where a provider buys a portion of your future revenue at a discount. Because it isn’t a debt instrument, you won’t face fixed terms, APRs, or monthly standing orders that drain your account during quiet weeks. If your sales drop, your repayments drop too. To understand the broader context of this financial product, you can read more about What is a Merchant Cash Advance? to see how it differs from traditional lending.

At PurePay Hub, we prioritize transparency through our “Pure” advantage. We believe merchants deserve a partnership based on honesty rather than hidden administrative markups. You get a clear quote from the start, ensuring the total cost is visible before you commit. We’ve removed the complex fee structures that often make business finance feel like a trap.

The Core Difference: BCA vs. Traditional Business Loans

Traditional bank loans are rigid. They require fixed monthly payments regardless of whether you’ve had a record-breaking month or a total washout. A business cash advance based on card sales is different because it’s inherently flexible. Since there’s no physical collateral like property or equipment required, your personal assets stay protected. The Factor Rate is the fixed multiplier applied to your advance amount that determines the total sum you will repay.

Who is this Funding Model For?

This model is built for high-volume card businesses. If you run a busy cafe, a retail shop, or an e-commerce site, your card turnover is your strongest asset. Seasonal businesses particularly favour this approach. During the winter “off-season,” a pub might see a 40% dip in takings, and a BCA automatically adjusts to ensure repayments don’t stifle cash flow. This funding is designed for UK-registered businesses that can demonstrate at least 3 to 6 months of consistent trading history.

How the “Breathing” Repayment Mechanism Works

Traditional bank loans are rigid. They demand the same payment every month, regardless of whether your till is ringing or silent. A business cash advance based on card sales operates on a fundamentally different principle. We call it the “breathing” mechanism. Instead of a fixed monthly sum, you repay a small, agreed percentage of your daily credit and debit card takings.

This system mirrors the natural rhythm of your business. If you have a quiet Monday with only £200 in card takings, your repayment is proportionally small. When a busy Saturday brings in a surge of £3,000 in sales, you pay back more. This flexibility protects your cash flow during seasonal dips or unexpected quiet patches. Because the percentage is fixed, you always know exactly what portion of every sale is being diverted. There are no fixed deadlines and no late fees. The advance is settled only when you make a sale, which removes the pressure of a ticking clock.

The Role of Your Card Machine

The entire process is automated through your existing payment setup. A processor like PurePay Hub facilitates the split of funds at the moment of transaction. There’s no need for manual bank transfers or the old-fashioned hassle of writing cheques. This seamless integration ensures that your focus remains on operations, not debt management. It provides a pure, hands-off experience that allows you to grow without the administrative burden of traditional financing. You don’t have to remember to move money or worry about missing a payment date.

Understanding the Factor Rate

Clarity is vital for any UK merchant. Unlike traditional loans with fluctuating interest rates, a cash advance uses a fixed factor rate. This is a simple multiplier that determines the total cost of the funding from the start. It’s a transparent way to see exactly what you owe without hidden surprises. This straightforward approach is often cited in any Guide for Businesses Needing Funding as a key advantage for small enterprises that value certainty.

Consider a hypothetical example. If you secure an advance of £10,000 at a factor rate of 1.2, your total repayment amount is exactly £12,000. It doesn’t matter if it takes six months or ten months to reach that total; the cost remains the same. You won’t find yourself trapped by compounding interest or penalty charges for taking longer to pay during a slow season. This certainty helps you plan your budget with confidence. You’re in control of the pace, and the total cost is locked in from day one.

Eligibility and the No-Nonsense Application Process

Securing a business cash advance based on card sales is designed to be a painless experience. Traditional banks often demand years of audited accounts and thick stacks of paperwork; we prefer a transparent, modern approach that respects your time. To qualify, your business must be based in the UK and have at least three months of trading history. Most lenders look for a minimum monthly card turnover of £2,500. This low barrier makes capital accessible to a vast majority of small businesses that might otherwise struggle with high-street lenders.

Understanding how a merchant cash advance works helps you see why the documentation requirements are so light. You won’t need to produce complex business plans or five-year projections. Instead, you usually only need to provide your last three months of merchant statements. Digital onboarding ensures the entire process is “Pure” and efficient, allowing for approval in as little as 24 to 48 hours. Your personal credit score doesn’t tell the whole story here. Lenders focus on the health and consistency of your sales rather than just a single credit number.

Step-by-Step: From Quote to Capital

- Step 1: You share basic business details and your recent card processing volume through a secure online portal.

- Step 2: You receive a transparent quote. This shows the total advance amount and the factor rate, ensuring there are no hidden surprises.

- Step 3: Once you’re happy, you sign the digital contract. The lender performs a final verification of your merchant accounts and the funds are typically transferred within one working day.

Why Approvals are Higher than Traditional Loans

Lenders in this space prioritise real-time sales data over historical balance sheets. They don’t get hung up on what happened two years ago; they care about the “pulse” of your business today. A consistent flow of card sales serves as the primary security for the funder, which significantly reduces their risk. This shift in focus means that even businesses with less-than-perfect credit can still qualify. If your turnover is strong and your daily transactions are steady, you’re a viable candidate for a business cash advance based on card sales. It’s a fairer way to assess a modern UK business, moving away from the rigid and often exclusionary criteria used by old-fashioned financial institutions.

Strategic Growth: When to Use Your Cash Advance

A business cash advance based on card sales isn’t a life support machine for a failing model. It’s high-octane fuel for growth. You shouldn’t use this capital to pay off long-term structural debt or cover basic rent arrears. Instead, think of it as a tactical tool. The most effective use of these funds involves revenue-generating activities that offer a clear return on investment. This includes purchasing extra stock for peak seasons, launching a targeted marketing campaign, or upgrading kitchen equipment to increase table turnover. These investments pay for themselves by driving more customers through your door. For those in the health and supplement sectors, this funding could even help you discover Simplepack Ltd and their specialist contract packing services to help you scale your product lines efficiently.

Because there’s no fixed monthly burden, your daily operational cash flow remains protected. You aren’t forced to find a specific sum when the till is quiet. This flexibility ensures your business stays agile. You can focus on expansion without the constant worry of a looming bank deadline. It’s about using capital to create more capital, rather than just filling a hole.

Managing Seasonal Fluctuations

Seasonality is the biggest challenge for UK retail and hospitality. A seaside cafe in Cornwall might see a 70% drop in footfall during January, while a London toy shop prepares for a 300% surge in December. A business cash advance based on card sales provides the peace of mind needed to bridge these gaps. You can stock up on inventory in October without draining your reserves. Repayments automatically scale down when sales are lean, ensuring you don’t feel the squeeze during a quiet week. This model is a favourite amongst hospitality and retail sectors because it mirrors the natural rhythm of their trade.

The Opportunity Cost of Waiting

In business, speed is often more profitable than a low interest rate. Imagine a supplier offers a 20% discount on a bulk order, but the deal expires in 48 hours. Traditional bank loans often take weeks to approve. By the time the funds arrive, the opportunity has vanished. The cost of missing that discount is often far higher than the fixed cost of the advance. Access to capital is often more valuable than the cost of the capital itself. Quick funding allows you to react to market shifts faster than your competitors, securing better margins and exclusive stock before anyone else.

Ready to fuel your next growth phase? Explore our transparent funding options.

The PurePay Hub Advantage: Transparent Merchant Funding

At PurePay Hub, we believe you deserve better than the opaque practices often found in traditional lending. We’ve built our reputation as a merchant’s ally by stripping away the complexity that clouds UK business finance. Our approach is defined by “Purity.” This means no hidden fees and no confusing jargon. We view a business cash advance based on card sales as a strategic partnership for your growth, not a weight of debt to carry. It’s a tool designed to help you seize opportunities without the stress of fixed monthly repayments.

Traditional finance often feels like a maze; we’ve cleared the path. By focusing on your actual card takings, we provide a funding solution that breathes with your business. When you’re busy, you pay back more. During quieter weeks, the repayment amount drops automatically. This flexibility ensures your cash flow remains healthy, allowing you to focus on what you do best: running your business.

Next-Day Access and Integrated Systems

Managing your finances is simpler when your processing and funding live under one roof. Our Countertop Card Machines integrate directly with the funding process, creating a seamless loop for your cash flow. You’ll benefit from next-day access to your daily takings alongside your cash advance. This unified system lets you track every transaction and repayment through a single, clear reporting interface. You won’t have to log into multiple portals or cross-reference different bank statements. By centralising your financial tools, you gain a level of control that fragmented systems can’t offer. You’ll spend less time on admin and more time serving your customers.

Getting Your Personalised Quote

Every UK business has its own rhythm, and we don’t believe in one-size-fits-all finance. Your factor rate is tailored to your specific card volume and trading history. We look at the health of your business rather than just a credit score. Our UK-based team is here to walk you through your offer, ensuring you understand every detail before moving forward. We’re here to support your next big step, whether that’s a kitchen refit, a stock expansion, or a new marketing campaign. Transparency isn’t just a buzzword for us; it’s our standard. A business cash advance based on card sales should be easy to understand and even easier to manage. Apply for your transparent business cash advance today and experience a fairer, more honest way to fund your future.

Take Control of Your Business Growth Today

Traditional bank loans often feel like a heavy burden during quiet trading periods. A business cash advance based on card sales removes that pressure by aligning repayments with your actual daily takings. You get the capital you need today without the stress of fixed monthly commitments or hidden late fees. It’s a transparent way to fund new equipment, stock, or renovations whilst keeping your cash flow healthy and predictable.

At PurePay Hub, we prioritise straightforward funding for UK merchants. We offer debit card charges starting from 0.3% and provide approval in as little as 24 hours. There aren’t any rigid schedules here; if your sales slow down, your repayments slow down too. This breathing mechanism ensures you stay in control of your finances without the fear of penalties. We’re here to act as your ally, providing the pure clarity you deserve in a complex financial world.

Secure your flexible business cash advance with PurePay Hub and start scaling your operations with confidence. We’re ready to help your business reach its full potential.

Frequently Asked Questions

Is a business cash advance based on card sales a loan?

No, a business cash advance based on card sales isn’t a traditional loan. It’s the purchase of your future credit and debit card revenue at a discounted rate. Unlike a bank loan with fixed monthly instalments, this arrangement moves in harmony with your turnover. You only pay back a small percentage of what you earn, keeping your cash flow pure and predictable.

How much can my business typically borrow through a merchant cash advance?

Most UK merchants can access funding between £2,500 and £500,000. Lenders typically offer an amount equal to 100% or 150% of your average monthly card turnover. If your boutique or cafe processes £20,000 a month in card payments, you could qualify for £20,000 to £30,000 in upfront funding to support your growth.

Will a cash advance affect my ability to get other business finance?

It’s unlikely to stop you from securing other finance. Because a cash advance is a commercial transaction rather than a traditional debt, it doesn’t always appear on your credit report in the same way a bank loan does. This flexibility helps you maintain a healthy financial profile while you grow, acting as a supportive partnership rather than a restrictive burden. If you’re also looking into personal borrowing options like car financing, you can check out I Need Cash for more information on their range of credit products.

What happens if I have a day with zero card sales?

If you don’t make a sale, you don’t make a payment. This is the core benefit of a business cash advance based on card sales. On a quiet Monday with zero transactions, the lender takes nothing. You only repay when your customers pay you, which removes the stress of fixed deadlines during seasonal lulls or slow trading periods.

Are there any hidden fees or “non-utilisation” charges?

Transparent providers don’t use hidden “non-utilisation” fees or surprise costs. You agree to a single, fixed cost upfront known as a factor rate. There are no compound interest charges or late payment penalties. This no-nonsense approach ensures what you see at the start is exactly what you’ll pay back over time, with no nasty surprises in the small print.

Can I pay off the cash advance early to save on costs?

You can settle the balance early, but it won’t typically reduce the total cost. Since you pay a fixed fee rather than accruing interest, the amount stays the same regardless of how quickly you repay. This clarity ensures you know your total commitment from day one, allowing you to plan your business finances with absolute certainty.

What is the minimum monthly card turnover required for a BCA?

Most providers require a minimum average turnover of £2,500 per month from card sales. You also need to have been trading for at least 3 to 6 months. This baseline ensures your business has a consistent enough history to support the repayment structure through your card terminal without affecting your daily operations.

How long does the application process take from start to finish?

The process is remarkably fast, often taking between 24 and 48 hours from application to funding. You’ll need to provide your last 3 months of merchant statements to get started. Once approved, the funds are usually transferred to your business bank account within 24 hours, providing the quick capital you need to seize new opportunities.