What if a single 15-digit number was the only thing standing between your business and its next sale? For many UK business owners, the search for clarity on how to get a merchant ID number UK often leads to more confusion than confidence. It’s frustrating to face the distinction between your business bank account and a dedicated merchant account, especially when you’re also navigating the 2026 regulations that require payment providers to give a full 90 days’ notice for account closures.

We believe that securing your Merchant ID (MID) should be a transparent partnership, not a bureaucratic hurdle. This guide provides a clear roadmap to approval, helping you navigate the KYC process with ease and understand how to minimise your transaction fees effectively. You’ll discover exactly how to secure your MID and start accepting card payments through reliable tools like a portable card machine or an online payment gateway, all whilst keeping your costs predictable and fair.

Key Takeaways

- Understand that a Merchant ID is your business’s unique digital address, essential for ensuring customer payments reach your account safely and accurately.

- Master the application process for how to get a merchant ID number UK by gathering the correct documentation to bypass common KYC hurdles and speed up approval.

- Learn the difference between an MID and a Terminal ID (TID) to effectively manage multiple card machines or locations under one business entity.

- Prioritise providers that offer next-day funding and transparent fee structures to protect your cash flow in the current economic climate.

- Discover how to streamline your setup with PurePay Hub to start accepting payments within days whilst benefiting from highly competitive transaction rates.

What is a Merchant ID (MID) and Why is it Essential for Your UK Business?

A Merchant ID (MID) is more than just a string of numbers. It is the unique 15-digit numerical code that identifies your business to the entire payment processing network. Without an MID, your business cannot legally process credit or debit card transactions. It acts as a digital address, ensuring that every penny spent by a customer reaches your specific business rather than vanishing into the financial ether. While many new owners feel overwhelmed by the technicalities, understanding how to get a merchant ID number UK is essential for moving beyond cash-only operations.

Your MID is distinct from your standard business bank account. They work in tandem, but they serve different masters. Your bank account is where you manage your overheads and payroll; your MID is the identifier that allows you to interact with the global card networks. It is a fundamental requirement for any business that wants to scale and provide the modern payment options that customers now expect as standard.

How the Merchant ID Functions in the Payment Cycle

The moment a customer taps their card on your portable card machine, a high-speed verification process begins. Your MID routes the authorisation request through the payment gateway to the customer’s bank. It tells the system exactly who is requesting the funds and where they should eventually land. The acquiring bank, which is the institution that processes your card payments, uses this unique ID to recognise your business entity instantly. This system is also vital for maintaining security and PCI compliance. By tethering every transaction to a specific MID, banks can monitor for unusual behaviour and protect your business from fraudulent chargebacks.

The Difference Between a Merchant Account and an MID

Clarity is vital here. Think of your merchant account as a secure vault where your transaction funds are held temporarily before being settled into your business bank account. The MID is the key that opens that vault. You might only have one merchant account, but you could require multiple MIDs if you manage different business arms or use various channels like an online payment gateway alongside physical countertop card machines. The MID is the critical link between the customer’s card and your bank balance. Securing this identifier is a non-negotiable step for any modern retailer or service provider in the UK. When you look into how to get a merchant ID number UK, you are essentially applying for the right to be recognised by the global financial system.

How to Apply for a Merchant ID Number in the UK: A Step-by-Step Guide

Applying for an MID is a structured process. It isn’t a simple sign-up. You’re entering a formal financial partnership. Preparation is your best tool for success. If you want to know how to get a merchant ID number UK without the usual stress, you must gather your data first. You generally have two main routes. Traditional high-street banks offer familiarity but often come with rigid, long-term contracts. Independent Sales Organisations (ISOs) usually provide more flexibility and faster onboarding for local business owners. Once you choose your path, the ‘Know Your Customer’ (KYC) phase begins. This is where underwriters verify your identity and assess the health of your business.

Essential Documentation for UK Merchants

Underwriters need to see exactly who they’re doing business with. This isn’t just bureaucracy; it’s a legal requirement in 2026. You’ll need to provide:

- Proof of identity: A valid Passport or Driving Licence for all directors and shareholders with a significant stake.

- Business evidence: Recent utility bills in the business name, VAT registration details, or your latest Companies House filings.

- Financial history: Typically, you’ll need 3 to 6 months of previous processing statements if you’re switching providers. New startups should provide recent business bank statements.

Having these documents ready prevents the frustrating “back-and-forth” that often delays trading. If you’re looking for a partner that values clarity, you can explore our straightforward onboarding process to get started quickly.

Navigating the Risk Assessment Process

The risk assessment is where most applications stall. Underwriters assess the likelihood of your business facing high levels of chargebacks or financial instability. Certain sectors, such as travel, events, or gambling, are often flagged as high risk. If your business falls into these categories, you can mitigate concerns by providing a clear business plan and evidence of strong cash reserves. Your personal credit score also plays a role. It acts as a barometer for your financial discipline. To ensure a smooth approval, present a transparent business model. Clearly explain your delivery timeframes. Shorter gaps between a customer paying and receiving their goods represent lower risk to the bank. A disciplined approach to your application shows underwriters that you’re a reliable partner, leading to faster approval and better rates.

Merchant ID vs. Terminal ID: Clearing Up the Confusion for Multi-Site Businesses

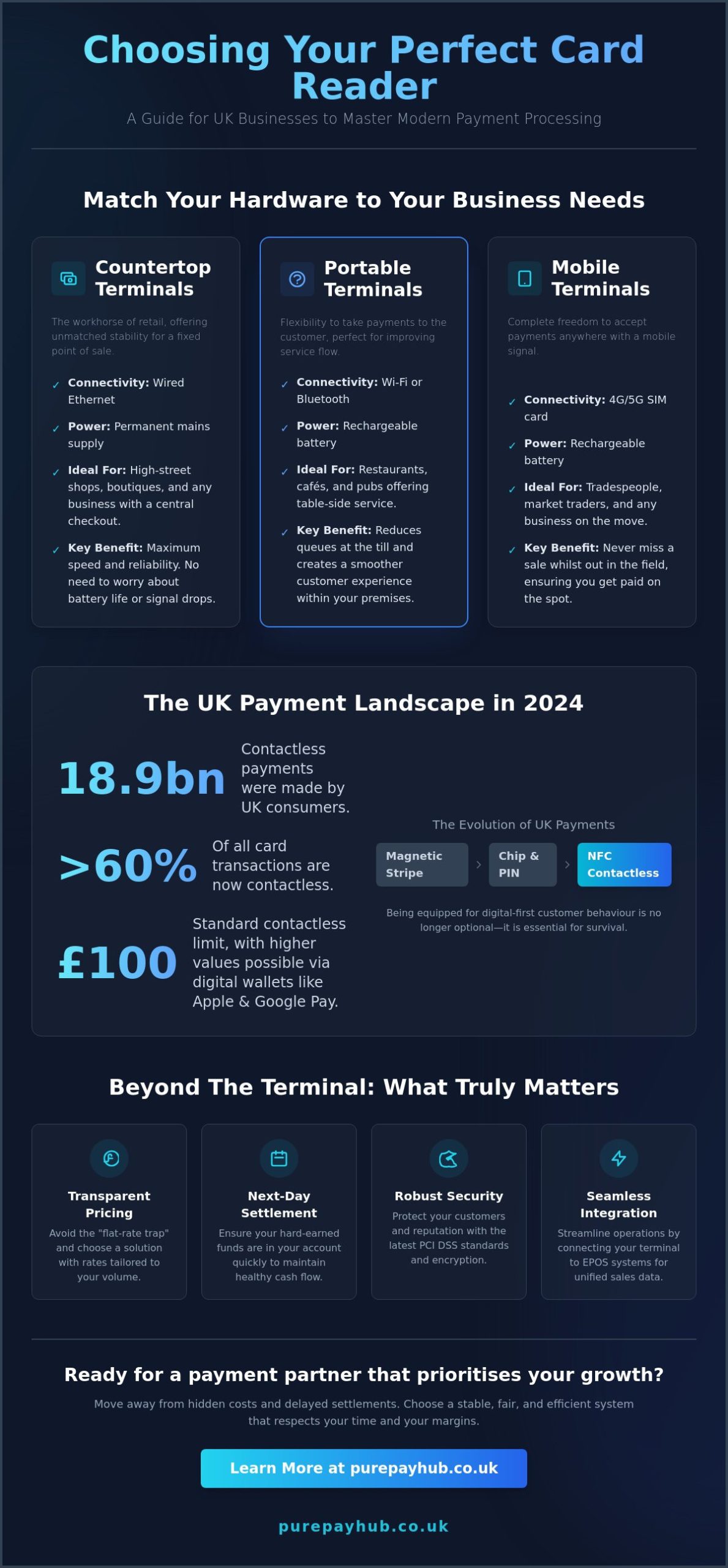

Many business owners feel a sense of relief once they understand how to get a merchant ID number UK, but that clarity often vanishes when they see additional codes on their bank statements. The most common source of confusion is the relationship between your Merchant ID (MID) and your Terminal ID (TID). While your MID identifies your business entity to the banking network, the TID identifies the specific piece of hardware used for the transaction. If you operate a busy cafe with three countertop card machines, you’ll have one MID but three distinct TIDs. This structure allows the banking system to track exactly which device initiated a payment.

This distinction isn’t just technical; it’s a powerful tool for your accounting. TIDs allow you to track performance at the per-device level. You can see exactly which till or which mobile card machine is processing the most volume. Keeping these numbers organised is crucial for reconciling your daily sales. When your end-of-day report shows a discrepancy, your TIDs act as a map to find exactly where the error occurred. It prevents the headache of searching through hundreds of transactions across multiple sites to find one missing entry.

When Do You Need Multiple MIDs?

While one MID usually suffices for most, certain growth milestones require more. If you’re operating different brands under one limited company structure, separate MIDs keep your branding consistent on customer bank statements. You should also separate your online payment gateway sales from your physical retail transactions. This helps you monitor different risk profiles and transaction rates more effectively. Additionally, if you’re expanding amongst various international regions, managing sales in different currencies often necessitates a dedicated MID for each territory to keep your tax reporting clean and your currency conversion costs transparent.

Troubleshooting ID Issues

Sometimes, a card machine might stop communicating with your MID. This often happens after a software update or a change in network settings. In these cases, your provider may need to re-map the TID to your account. If your business undergoes a significant change, such as a shift in legal status or a new trading name, you must update your MID details immediately. Failing to do so can lead to frozen funds while the bank verifies the new information. Whilst the MID identifies who is being paid, the TID identifies where the payment happened.

Key Criteria for Choosing Your Merchant Account Provider in 2026

Selecting a partner for your payment processing is a decision that impacts your daily operations and long-term profitability. Your choice matters. While you may have already researched how to get a merchant ID number UK, the provider you choose to issue that ID is just as critical. In 2026, the market is crowded with options, but few offer the transparency that local businesses deserve. You must look beyond the headline transaction rates. While debit charges of 0.3% and credit charges of 0.5% are common benchmarks, the total cost of ownership often includes hidden layers that can erode your margins.

Funding speed has become a non-negotiable factor for UK SMEs. In a high-inflation environment, waiting three to five working days for your funds to clear is no longer acceptable. Your business needs liquidity to respond to market changes and manage overheads. Reliability also means having access to UK-based experts who understand the regional market, rather than being stuck in a loop with automated chatbots when you need urgent help. Consider these key factors during your evaluation:

- Contract flexibility: Avoid ‘lock-in’ periods that prevent you from switching as your business grows.

- Direct support: Ensure you can speak to a human expert when technical issues arise.

- Funding speed: Prioritise providers that offer next-day settlement as standard.

Understanding Fee Structures: Interchange++ vs. Blended

Transparency is the foundation of a fair partnership. Interchange++ is often the favourite choice for growing businesses because it breaks down exactly what the card schemes, the banks, and the processor are charging. This prevents providers from padding their margins with opaque “blended” rates. Be vigilant for hidden ‘admin’ or ‘PCI non-compliance’ fees in your monthly statement. These are often used by traditional banks to inflate costs. Your industry type will influence the rates you’re offered, so ensure your provider understands your specific sector’s risk profile.

Hardware and Software Integration

Your MID must work seamlessly across all your payment channels. Whether you’re using countertop card machines in a shop or portable card machines for table service, the integration should be flawless. For hospitality and retail, an integrated EPOS system is vital for maintaining efficiency and reducing manual entry errors. In the current climate, next-day funding should be your primary priority when evaluating any provider. If you’re ready for a fairer way to trade, you can get a transparent quote from PurePay Hub and secure your MID today.

Secure Your UK Merchant ID with PurePay Hub: Transparent, Quick, and Reliable

Securing your payment processing shouldn’t feel like a battle against hidden terms and conditions. If you’ve been searching for how to get a merchant ID number UK, you’ve likely encountered the opaque practices of traditional banks. PurePay Hub was built to disrupt that cycle. We offer a no-nonsense onboarding process designed to get you trading within days, not weeks. We understand that for a local business, time isn’t just money; it’s the ability to serve your community without delay.

Our approach is founded on the principle of fair partnership. We provide some of the UK’s most competitive transaction rates, with debit processing at 0.3% and credit cards at 0.5%. These aren’t just introductory offers. They represent our commitment to transparency. We also provide next-day funding as standard. This ensures your cash flow remains healthy and predictable, allowing you to reinvest in your growth immediately rather than waiting for funds to clear. You’ll work with human-led support experts who treat you as a partner, not just another MID number in a database.

The PurePay Hub Advantage for SMEs

Small and medium-sized enterprises often face the brunt of complex fee structures. We’ve eliminated that frustration. With us, there are no hidden markups or confusing monthly charges; what you see is exactly what you pay. We provide specialised solutions for retail, hospitality, and service-based businesses across the UK. Whether you need a countertop card machine for a fixed till point or a portable card machine for table service, our hardware integrates effortlessly with your new MID. This seamless connection ensures that every transaction is recorded accurately and settled swiftly amongst your various business locations.

Start Your Application Today

Your journey to better payment processing starts with a streamlined digital application. We’ve removed the paperwork burden, creating a process that respects your busy schedule. Our team provides expert guidance through the PCI compliance maze, helping you avoid unnecessary fines and keep your customer data secure. We believe that clarity is the highest form of professional service. If you’re ready to move away from the skepticism of traditional finance and toward a reliable business ally, we’re here to help.

Get your transparent quote and start your MID application with PurePay Hub today. Experience the difference of a payment partner that prioritises your success and values your time whilst delivering the reliability your business requires.

Take Control of Your Business Payments Today

Securing your Merchant ID is the final hurdle to unlocking your business’s full potential. You now understand that while an MID identifies your entity, your Terminal IDs track the performance of individual card machines. Mastering how to get a merchant ID number UK requires preparation, but it shouldn’t be an overwhelming task. By gathering your documents early and choosing a partner that prioritises transparency, you can avoid the common pitfalls of the KYC process and start trading with confidence.

Your business deserves a payment structure that supports growth rather than hindering it. PurePay Hub provides the stability and clarity you need. We offer debit card rates starting from 0.3% and ensure that next-day funding comes as standard for all UK merchants. Our UK-based independent support team is always available to help you navigate technical challenges without the frustration of automated queues. We believe in straight-talking and fair service for every regional business owner.

Stop settling for opaque fee structures and delayed settlements. Get your ‘no-nonsense’ merchant service quote from PurePay Hub and join a community of business owners who value fairness. We’re ready to help you start your journey toward a more reliable financial future.

Frequently Asked Questions

How long does it take to get a merchant ID in the UK?

It typically takes between three to five working days to secure your MID. This timeline depends on the complexity of your business and the speed of the provider’s underwriting team. Whilst some digital-first providers offer near-instant setup, traditional high-street banks may take several weeks to complete their full risk assessment and credit checks.

Can I get a merchant ID without a business bank account?

No, you cannot secure an MID without a dedicated business bank account. Acquiring banks require a professional account to settle your funds and verify your business’s legal standing. This separation ensures your personal finances remain distinct from your commercial transactions, which is a key requirement for financial transparency and tax reporting in the UK.

What documents are needed for a UK merchant account application?

You will need to provide proof of identity for all directors, such as a passport or driving licence, and proof of your business address. Most providers also require three to six months of business bank statements and evidence of your commercial registration, such as Companies House filings or VAT details. Having these organised is the fastest way to understand how to get a merchant ID number UK.

Is a merchant ID the same as a VAT registration number?

No, these are entirely different identifiers used for different purposes. Your Merchant ID (MID) is a 15-digit code used by the payment network to route funds to your account. Your VAT registration number is issued by HMRC for tax collection purposes. Whilst both are essential for a compliant business, they are not interchangeable in any financial system.

Why has my merchant ID application been declined by a bank?

Applications are often declined due to a high-risk business model, a poor personal credit score, or insufficient documentation. Banks may also reject applicants who have a history of high chargeback rates or operate in sectors prone to fraud. If you face a decline, it is best to seek a provider that specialises in your specific industry or offers more flexible underwriting criteria.

Do sole traders need a separate merchant ID for card payments?

Yes, sole traders require their own MID to process card transactions legally. Even if you don’t operate as a limited company, you still need a unique identifier to connect your card machine or online gateway to your bank account. This ensures that every payment you receive is correctly attributed to your trading name for accounting and security purposes.

Can I use the same MID for my physical shop and my website?

You can use the same MID, but many providers recommend using separate IDs for physical and online sales. This is because card-present retail transactions have a lower risk profile than online e-commerce payments. Separating them allows you to track performance more accurately and often results in lower transaction fees for your in-person sales.

How much does it cost to maintain a merchant ID number monthly?

Maintenance costs vary significantly depending on your provider and monthly turnover. Monthly fees typically range from £0 to £40, whilst some providers also charge for PCI compliance and statement access. It’s essential to look for a transparent fee structure that avoids hidden markups, ensuring your monthly costs remain predictable as your business grows.