Did you know that over half of UK small business loan applications are currently rejected by major banks? It’s a discouraging reality for any owner trying to scale. When you do secure a traditional loan, you’re often stuck with rigid repayments that don’t account for seasonal dips or quiet weeks. We know that fixed monthly costs create unnecessary stress. A business cash advance for small business UK offers a fairer, more transparent way to bridge the gap.

You deserve a financial partner that understands your daily challenges. You’ll discover how to secure flexible, revenue-linked capital to grow without the weight of fixed monthly bills. This guide covers everything from quick access to working capital to why this model keeps your personal assets safe. We’ll explain how to turn your future card sales into immediate growth, ensuring your repayments always mirror your actual daily turnover.

Key Takeaways

- Understand how a business cash advance for small business UK works by linking repayments to your daily card sales, ensuring you only pay back when you are making money.

- Learn why this flexible funding model is often accessible within 48 hours, bypassing the lengthy and complex application processes of traditional high-street banks.

- Discover the peace of mind that comes with unsecured capital, allowing you to grow your business without putting personal or commercial assets at risk.

- Identify the straightforward eligibility requirements, focusing on your recent turnover and trading history rather than just a traditional credit score.

- See how PurePay Hub simplifies the process by integrating funding directly with your existing payment systems for automated, stress-free management.

Navigating Small Business Cash Flow Challenges in the UK

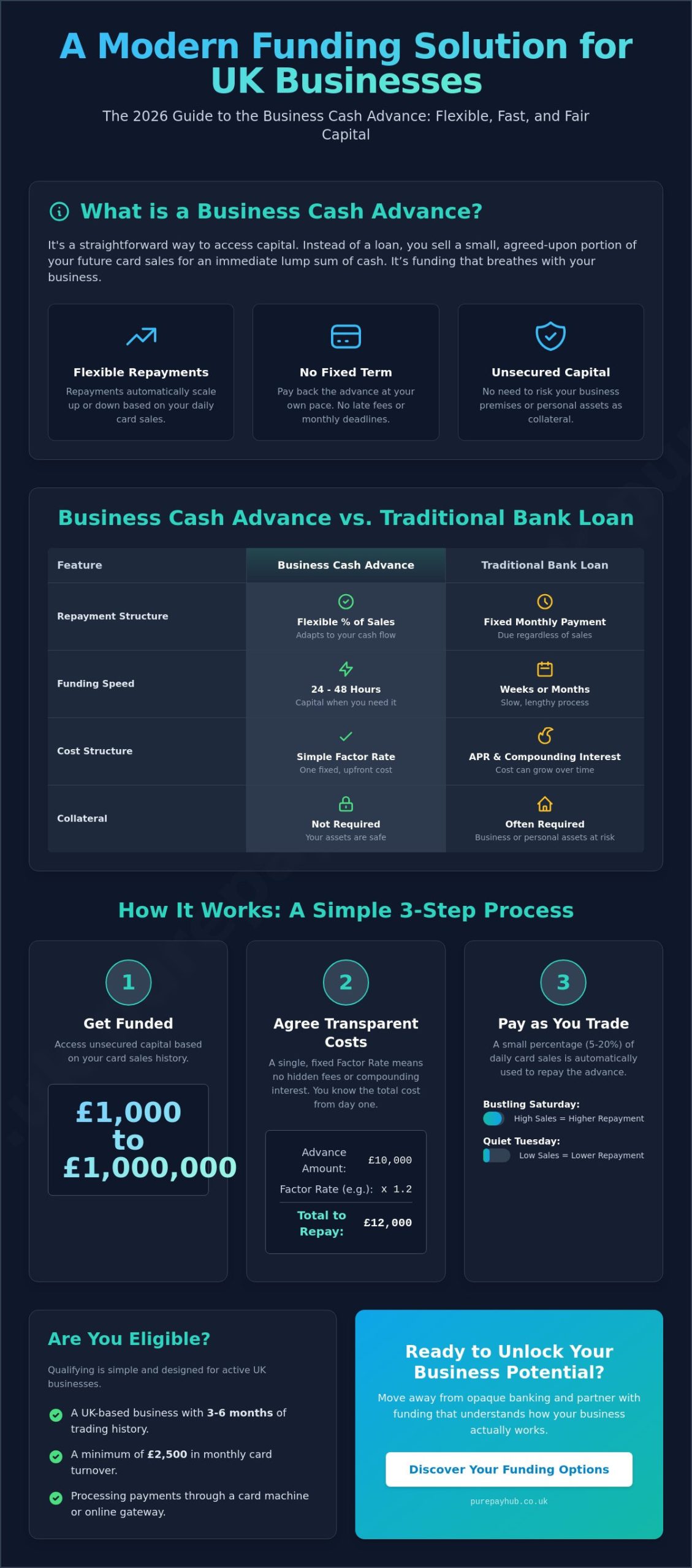

Running a local shop or a seaside cafe in Britain means living by the rhythm of the seasons. You might see a surge in turnover during the summer holidays, only to face a quiet stretch once the school term starts. This volatility is a natural part of the business cycle, but it often clashes with the rigid expectations of traditional lenders. High-street banks typically operate on a one-size-fits-all model. They provide a lump sum and demand a fixed monthly repayment, regardless of whether your till was ringing or silent that week. It’s a system built for stability, not the reality of independent trade.

This mismatch creates a “funding gap”. It’s the moment when your ambition for growth outpaces your available working capital. According to industry data from 2023, the success rate for SME loan applications at major banks dropped to just 45 per cent. Conventional banking is often too slow and too restrictive to help. Whilst-you-wait funding models, such as a What is a Merchant Cash Advance?, offer a modern alternative. They prioritise speed and adaptability over lengthy paperwork and fixed schedules. A business cash advance for small business UK bridges this gap by aligning your repayments with your actual sales.

The Burden of Fixed Monthly Repayments

Fixed repayments can quickly drain your cash reserves during quiet trading periods. If revenue doesn’t meet your projected targets, the pressure to find that monthly instalment becomes a major source of stress. It’s a significant risk of default that many owners simply can’t afford. This is why more UK SMEs are moving away from rigid financial structures. They want a partner that shares the risk. When your sales are lower, your repayments should be too. It’s a fairer way to manage debt without compromising your daily operations or staff wages.

Capitalising on Immediate Business Opportunities

Business doesn’t wait for a bank’s committee to meet. Sometimes you need to move fast. Securing a bulk-buy discount from a supplier can significantly improve your margins, but only if you have the cash ready. A business cash advance for small business UK provides that agility. It allows you to fund emergency repairs to vital equipment, like your countertop card machines or shop fittings, without disrupting your cash flow. You can also use this capital to invest in targeted marketing during peak UK shopping seasons, like the lead-up to Christmas or bank holiday weekends. This ensures you’re always ready to capture demand when it arrives.

What is a Business Cash Advance? Revenue-Based Funding Explained

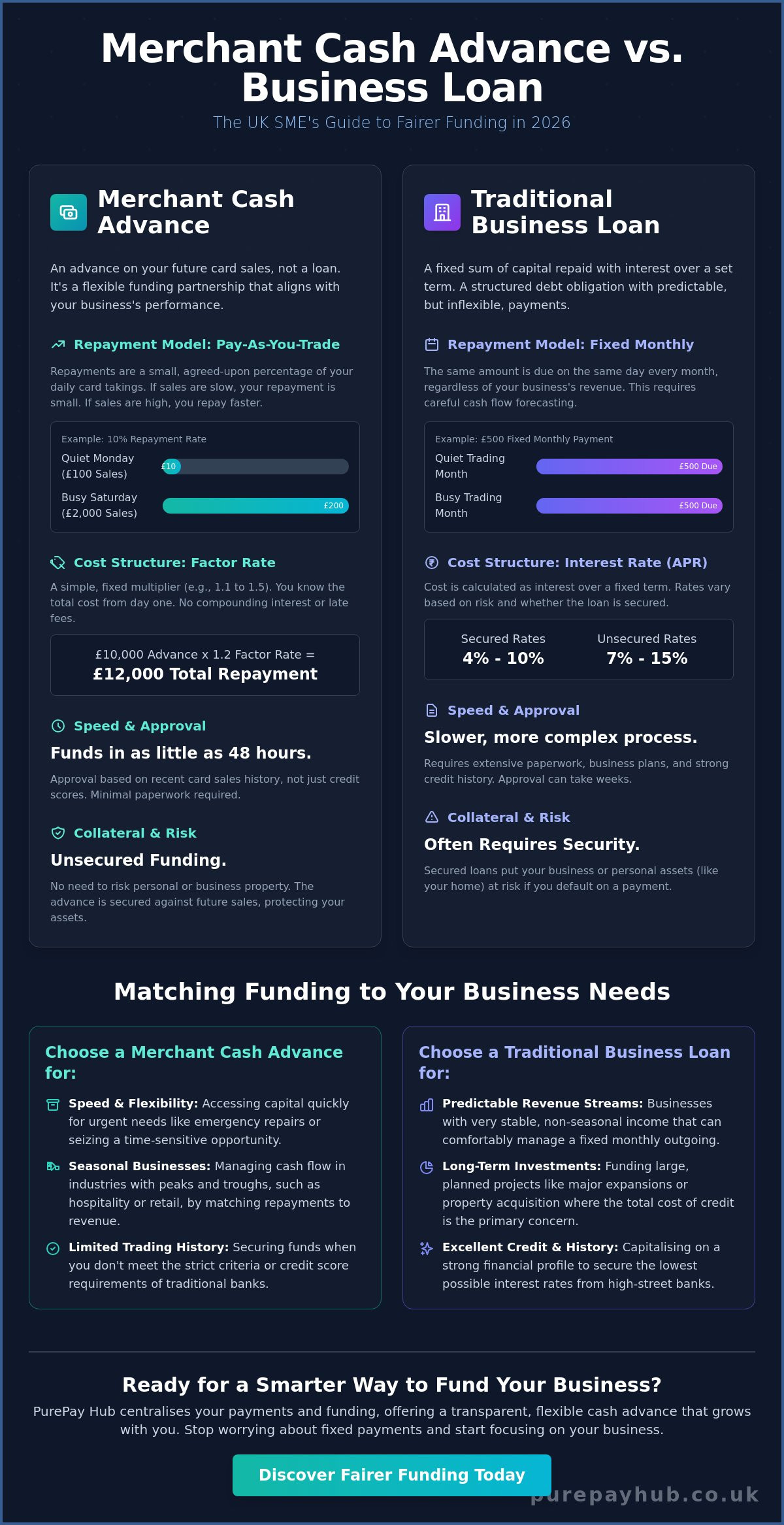

A business cash advance for small business UK is an unsecured capital injection based on future card takings. Unlike a traditional bank loan, this isn’t money you “borrow” in the conventional sense. It is technically a purchase of your future credit and debit card sales. A provider gives you a lump sum upfront, and in exchange, they buy a specific portion of your future revenue at a fixed cost. This distinction is vital because it changes how the funding is regulated and how you manage it daily.

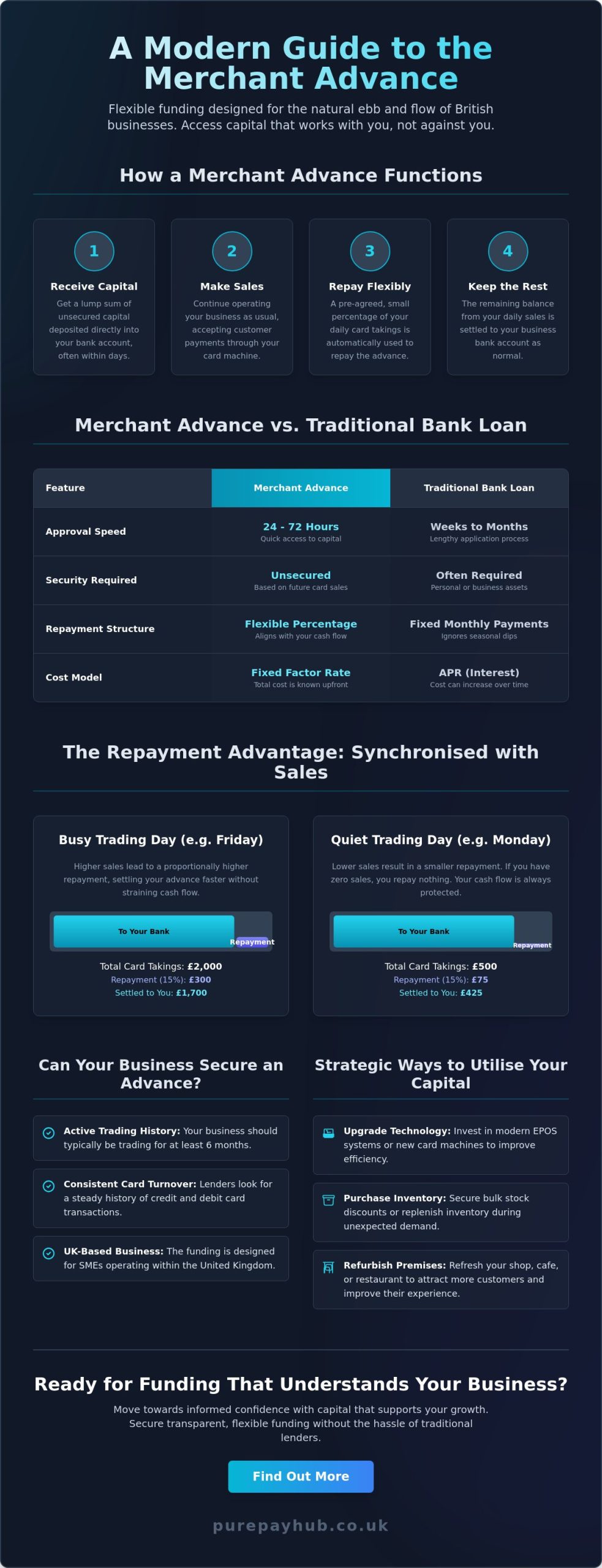

The entire process is managed through your merchant account, which serves as the automated hub for the transaction. There’s no need to set up standing orders or worry about missing a deadline. Your card terminal communicates directly with the provider to facilitate the repayment. This level of integration is supported by industry bodies like The British Merchant Cash Advance Association, which helps maintain high standards of transparency across the UK’s alternative finance sector.

Understanding the Factor Rate vs APR

One of the biggest hurdles in traditional finance is the complexity of interest rates. Banks often use an Annual Percentage Rate (APR), which can be difficult to calculate when compound interest and monthly fees are added. A business cash advance for small business UK uses a factor rate instead. This is a simple multiplier applied to the advance amount. If you take an advance of £10,000 at a factor rate of 1.2, your total repayment is £12,000. You won’t face fluctuating interest or late payment penalties. This no-nonsense approach ensures you know exactly what the funding costs before you spend a single penny.

The Repayment Mechanism: Pay as You Earn

The “sweep” method is the engine behind this funding’s flexibility. Rather than a fixed monthly bill, a small percentage of your daily card sales is diverted to clear the balance. This percentage usually stays between 10 per cent and 30 per cent of your daily takings. The beauty of this system lies in its responsiveness to your trading volume. On a quiet Tuesday, you pay back very little. If you have a day with zero card sales, your repayments simply stop until the next customer taps their card. This ensures your working capital isn’t choked during slow weeks, allowing you to maintain a healthy cash flow whilst clearing the balance. You can check your eligibility for this type of funding through PurePay Hub’s business cash advance service.

Business Cash Advance vs. Traditional Loans: Which Suits Your SME?

Choosing between a high-street bank and alternative finance is a pivotal decision for any merchant. Traditional loans are often slow. They require mounds of paperwork and can take weeks, or even months, to process. In contrast, a business cash advance for small business UK is designed for speed. You can often access funds within 24 to 48 hours of approval. This agility is essential when you need to settle a VAT bill or grab a time-sensitive stock opportunity. Traditional lenders lean heavily on your credit score and years of audited accounts. A cash advance looks at the health of your current trading instead. If you have a consistent history of card takings over the last 3 to 6 months, you are likely to qualify. It is a more inclusive way to fund a modern business.

| Criteria | Business Cash Advance | Traditional Bank Loan |

|---|---|---|

| Speed of Funding | 24 to 48 hours | 3 to 6 weeks |

| Security Required | Unsecured (No assets) | Secured (Property/Assets) |

| Repayment Structure | Flexible (Linked to sales) | Fixed monthly amount |

| Approval Basis | Card sales history | Credit score and accounts |

| Cost Type | Fixed factor rate | Variable or fixed APR |

Fixed vs. Flexible Repayment Models

Imagine a quiet month where footfall drops due to local roadworks or poor weather. With a bank loan, you still owe the same fixed amount. This creates a massive cash flow squeeze. The business cash advance for small business UK model removes this stress. Because it is revenue-linked, your repayments shrink during quiet times. There’s a significant psychological benefit to revenue-aligned debt. You don’t have to worry about defaulting during a seasonal dip because the system adjusts to your performance automatically. It keeps your business stable whilst you focus on bringing customers back through the door.

Security, Collateral, and Personal Risk

Most bank loans for SMEs are “secured”. This means you must pledge collateral, often your home or commercial property. If things go wrong, your personal assets are at risk. A cash advance is fundamentally different. It is an unsecured product. You aren’t putting your house on the line to get the capital you need. This protects your personal future and allows you to make smarter funding choices without the fear of losing everything. It is about empowering you to grow on your own terms, keeping your personal life separate from your business liabilities.

Eligibility and Application: Preparing Your Business for Funding

Securing a business cash advance for small business UK is a refreshingly direct process. Unlike the rigid gatekeeping of high-street banks, this funding model focuses on your current momentum. Most providers require a minimum monthly card turnover of between £2,500 and £5,000 to qualify. You also need a consistent trading history, typically spanning at least 3 to 6 months. This ensures your business has a proven track record of card transactions that can support the repayment structure. Eligibility is primarily based on card sales volume rather than just a credit score.

One major advantage of this approach is the use of “soft search” credit checks. Traditional loan applications often leave a permanent mark on your credit report. This can negatively impact your score, especially if you apply to multiple lenders in a short period. A soft search allows providers to assess your suitability without affecting your credit rating at all. It is a transparent and risk-free way to explore your options. Your merchant service statements act as the primary evidence of your ability to repay, providing a clear picture of your daily takings and customer behaviour.

The Application Checklist

To ensure a smooth approval, you should have your documentation ready. You will typically need your last three to six months of merchant account statements to demonstrate your turnover. You also need proof of business identity and valid UK bank account details where the funds will be deposited. When presenting your turnover, ensure it is accurate and reflects your average monthly performance. This clarity helps providers offer you the best possible factor rate. It reduces the perceived risk and proves your business is a stable partner for development.

Timing Your Advance for Maximum Impact

Strategic timing is key to making the most of your capital. Many UK merchants apply for funding just before peak seasons, such as the Christmas rush or the summer holiday period. This allows them to stock up on inventory or hire extra staff when demand is highest. You might also consider an advance before a planned renovation or to replace aging equipment. However, it is vital to avoid over-leveraging. Only take what your future sales can comfortably support. Planning your funding around these cycles ensures the capital drives real growth rather than just covering existing gaps. Ready to take the next step? You can apply for a business cash advance through PurePay Hub and get a decision quickly.

Securing Flexible Capital with PurePay Hub Merchant Services

PurePay Hub approaches finance differently. We don’t view funding as a separate, distant service. Instead, we integrate the business cash advance for small business UK directly into our payment ecosystem. This centralised approach means your funding is perfectly aligned with your card processing. Whether you use our Countertop Card Machine, Portable Card Machine, or Mobile Card Machine, your hardware becomes a gateway to flexible capital. We understand that waiting weeks for a bank’s decision isn’t an option for a busy merchant. That’s why we offer next-day funding for our partners, ensuring you have the liquidity to act when opportunities arise.

Our commitment to transparency is absolute. We’ve built our reputation on a no-nonsense approach that avoids the murky fee structures of traditional competitors. You won’t find hidden markups or complex corporate jargon here. We position ourselves as a fair partner to regional business owners, providing the clarity you need to manage your finances with confidence. Transitioning from a standard merchant to a funded partner is a seamless journey designed to support your long-term development. We act as a stabilising force, helping you turn daily turnover into a tool for sustainable growth.

Transparent Processing and Integrated Funding

There is a massive advantage in having your payment processor and funding facilitator under one roof. It removes the friction often found when dealing with multiple third parties. Our low transaction rates, starting at 0.3 per cent for debit cards, ensure you keep more of your hard-earned profit. Because the system is integrated, your reporting is simplified. You can track your daily sales and your advance repayments in one single, clear dashboard. This level of visibility prevents the confusion that often leads to cash flow stress, providing a clear path for your business’s finances.

Getting Started with PurePay Hub

Joining PurePay Hub is a straightforward process that prioritises your time. Our onboarding is fast, often taking just 10 to 15 minutes, with terminals delivered within 48 hours. If you’re already trading, switching to us is just as simple. You’ll gain access to our dedicated, UK-based support team who are ready to answer any questions about your funding or your hardware. We don’t hide behind automated bots or distant call centres. We are local experts committed to your success. If you’re ready to secure the capital your business needs to scale, you can Enquire about a Business Cash Advance with PurePay Hub today.

Elevating Your Business with Flexible Funding

Traditional banking often leaves UK merchants feeling constrained by rigid terms and slow processes. You’ve seen how revenue-linked capital offers a fairer alternative, aligning your repayments with your actual daily sales. By choosing a business cash advance for small business UK, you protect your personal assets whilst gaining the agility to invest in stock or equipment exactly when you need it. It is a modern solution designed for the unique rhythms of the British high street, ensuring you never pay more than you can afford during quieter trading periods.

PurePay Hub is here to simplify your growth journey with a commitment to total transparency. We provide next-day access to funds and debit card rates starting from 0.3 per cent; all supported by our dedicated UK-based expert team. We believe in straight-talking finance without the hidden markups or complex jargon that often complicates business development. Ready to transform your future card sales into immediate, usable working capital? Apply for a transparent Business Cash Advance today and take the next step with confidence. Your business has the potential to scale, and we are ready to provide the flexible tools to make it happen.

Frequently Asked Questions

What is the maximum amount I can borrow through a business cash advance?

The amount you can secure is typically based on your average monthly card turnover. Most providers offer between 100 per cent and 200 per cent of your typical monthly sales volume. This ensures the advance remains manageable for your specific business size. If your average monthly takings are £10,000, you might access a lump sum up to £20,000 depending on your trading history and risk profile.

How long does it take for the funds to reach my UK business bank account?

Funds can reach your account in as little as 24 to 48 hours following approval. The digital application process is designed for speed; bypassing the weeks of manual checks required by traditional lenders. Once you have submitted your merchant statements and passed the soft search, the capital injection is processed quickly. This makes a business cash advance for small business UK an ideal choice for urgent stock needs or emergency repairs.

Can I get a business cash advance if I have a poor credit history?

Yes, you can still qualify even if you don’t have a perfect credit score. Providers prioritise your recent card sales and trading consistency over historical credit data. Because the funding is unsecured and linked to your future revenue, your ability to generate daily sales is the most important factor. This inclusive approach helps many independent merchants who have been unfairly turned away by high-street banks.

Do I have to switch my card machine provider to get a cash advance?

You don’t always have to switch; however, using an integrated provider like PurePay Hub simplifies the entire process. When your card machine and funding are aligned, repayments are automated through your daily takings without any manual intervention. If you are currently with another provider, switching to our countertop or portable machines can often unlock better transaction rates alongside your funding.

Is there an interest rate or APR associated with a business cash advance?

No, these products do not use interest rates or an Annual Percentage Rate (APR). Instead, you pay a fixed cost determined by a factor rate; which is agreed upon at the start. This means you’ll know exactly how much you will pay back from day one. There are no compound interest charges or late payment fees; ensuring total transparency for your business’s financial planning.

What happens to my repayments if my card machine is broken or I am on holiday?

Your repayments automatically pause or slow down if you aren’t processing card sales. Since the “sweep” mechanism takes a pre-agreed percentage of each transaction, zero sales means zero repayments. This provides a natural safety net during holiday closures or equipment downtime. You won’t face the stress of a fixed monthly bill whilst your till is silent; allowing you to focus on getting back to trade.

Are there any restrictions on how I use the cash advancement?

There are generally no restrictions on how you utilise the capital within your business. You can use a business cash advance for small business UK to settle tax bills, purchase seasonal stock, or invest in new marketing campaigns. Whether you need to upgrade your EPOS systems or fund a shop renovation; the choice is entirely yours. We provide the capital, and you provide the expertise to grow.

Can start-up businesses in the UK apply for a merchant cash advance?

Brand new start-ups usually need to establish a short trading history before they can apply. Most providers require at least 3 to 6 months of consistent card processing data to assess your average turnover. Once you have this baseline of sales, you can apply for funding to help scale your operations. It is an excellent secondary step for businesses that have moved past the initial launch phase.