How much time did you spend this week chasing a bank transfer that was “definitely sent” or waiting for a cheque to clear? It’s a common frustration for professionals who still rely on manual payments or basic apps. A 2026 study by money.co.uk found that only 46% of UK SMEs with card machines fully understand their fees. You shouldn’t have to be a financial expert to get paid fairly for your hard work. Finding the right card machine for tradesmen UK means moving past high transaction fees on small jobs and the constant worry of a signal dropping out when you’re on-site.

We believe your payment setup should be a tool for growth, not a source of stress. This guide shows you how to eliminate “cash-only” limitations and secure your earnings instantly at the end of every job. You’ll discover how to access lower rates than standard pay-as-you-go readers and ensure your money is in the bank by the next morning. We’ll break down the latest 2026 hardware options, from portable terminals to mobile readers, so you can build a reliable cash flow that supports your trade business.

Key Takeaways

- Meeting the “contactless expectation” helps you secure payments instantly and reduces the security risks of carrying large amounts of cash in your van.

- Compare mobile and portable terminals to find the right connection type for your work environment, whether you need 4G connectivity for remote sites or Wi-Fi for a workshop.

- Learn how to avoid the “flat-rate trap” by choosing a card machine for tradesmen UK that offers transparent Merchant Service Charges instead of high fixed fees.

- Follow a simple checklist to prepare your trade credentials for a quick setup, ensuring you can take professional on-site payments without delay.

- Discover how switching to a dedicated merchant partner can provide faster settlement times and lower rates that respect your hard-earned profit margins.

Beyond “Cash Only”: Why UK Tradesmen are Switching to Card Machines

Cash is no longer king on the British doorstep. In 2026, most homeowners don’t keep enough physical currency to cover even a basic call-out fee, let alone a full boiler service or electrical rewire. If you tell a customer you’re “cash only,” you’re creating a hurdle that many won’t bother to jump. Choosing a reliable card machine for tradesmen UK removes this friction. It ensures you can accept payment the moment the job is finished, rather than sending your customer on a late-night hunt for an ATM.

Security is another major driver for this shift. Carrying large amounts of cash in a van makes you a target. It’s a liability that creates unnecessary stress during your workday. Digital payments move money directly from the customer’s account to yours, bypassing the physical risks entirely. Beyond safety, a professional payment terminal builds immediate credibility. It signals that you’re a legitimate, modern business. This trust is vital when you’re working in a new client’s home for the first time.

The Death of the Bank Transfer Lag

We’ve all heard the phrase, “I’ll pay it tonight, I promise.” Too often, that promise turns into days of chasing unpaid invoices and sending awkward reminder texts. This lag kills your business cash flow. When you take a card payment on-site, the transaction is settled before you even pack your tools away. There is also a distinct psychological shift at play. Customers are statistically more likely to approve small extras or additional repairs when they can pay by card; the friction of setting up a new bank transfer often stops those “while you’re here” jobs from happening. You’ll also spend far fewer hours on a Sunday evening reconciling your bank statements against your job list.

VAT and Tax Compliance Simplified

Staying on top of your books is easier when every job creates its own digital footprint. As Making Tax Digital (MTD) requirements become more stringent, having an organised digital record of every transaction is a massive advantage. You can send automatic digital receipts to your customers via email or SMS, which provides a better experience for them and a cleaner paper trail for your accountant. Modern card machines integrate directly with your accounting software to save you up to three hours of admin every single week. This automation reduces the risk of manual entry errors and ensures your VAT returns are based on accurate, real-time data.

Portable vs. Mobile: Choosing the Right Terminal for the Job

Picking the right hardware is about more than just aesthetics. For a busy plumber or electrician, a card machine for tradesmen UK needs to be as rugged as a cordless drill. You have two main choices: portable and mobile. A Portable Card Machine relies on Wi-Fi. It’s excellent if you have a workshop or if your customers are happy for you to jump on their home network. However, a Mobile Card Machine is the true workhorse for on-site visits. These devices come with built-in SIM cards, allowing you to process payments via 4G or GPRS from a driveway, a building site, or the side of the road.

Battery life is a non-negotiable factor. You need a terminal that lasts a full 10-hour shift without needing to sit on a charging cradle. There’s nothing more unprofessional than a dead battery just as a client reaches for their wallet. Durability matters just as much. Your terminal will live in a dusty van, sit on workbenches, and occasionally get knocked over. Professional-grade hardware is built to withstand these environments, unlike consumer-level tablets or flimsy plastic readers that often fail under pressure.

The Connectivity Checklist

Connectivity issues are the biggest cause of payment frustration. While Wi-Fi is fast, it’s often unreliable at the far end of a garden or in a basement. GPRS and 4G provide a more stable alternative in rural postcodes. We recommend looking for devices with roaming SIM cards. These automatically switch to the strongest available network, whether that’s EE, Vodafone, or O2. This “stand-alone” advantage is why we advise against phone-tethered apps. You don’t want to be faffing with Bluetooth pairing or draining your phone battery when you could be moving to the next job.

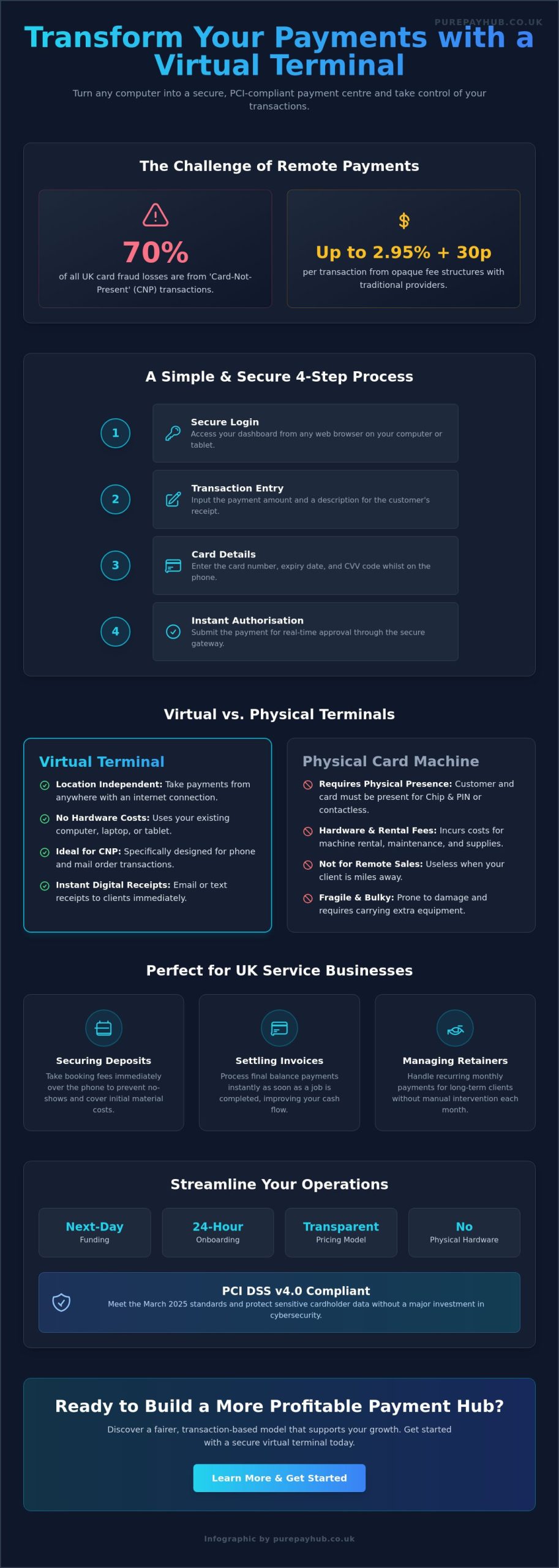

Payment Links and Virtual Terminals

Not every payment happens face-to-face. A Virtual Terminal allows you to take secure deposits over the phone before you even load the van. This reduces the risk of no-shows and secures your time. For jobs where you can’t access the property, you can send secure Payment Links via SMS. The customer clicks, pays, and you receive an instant notification. This is also useful for setting up recurring card payments for maintenance contracts or service plans. If you are looking for a setup that handles both on-site and remote payments, exploring a Mobile Card Machine is a smart first step.

Demystifying the Cost: Transaction Rates vs. Monthly Rentals

Many businesses fall into the “flat-rate trap” when they first start out. It feels safe to have no monthly costs, but this convenience comes at a premium. If your turnover is consistent, a 1.75% transaction fee is simply too high. For an established business, a dedicated card machine for tradesmen UK with a merchant account is usually the more profitable path. Merchant Service Charges (MSC) represent the core cost of processing any UK card payment. These rates often sit between 0.3% and 0.5% for debit cards. When you add a small monthly rental fee for a professional terminal, your total monthly spend often drops significantly compared to flat-rate apps.

Interchange fees shouldn’t be a mystery amongst traders. This is the fee paid to the customer’s bank for every transaction. Transparent providers pass these through clearly rather than bundling them into a high, opaque flat rate. Paying for hardware rental ensures you have a reliable device and access to these lower processing rates that respect your profit margins. It’s a stabilizing force for your finances that provides clarity instead of confusion.

Optimising your overheads doesn’t stop at transaction fees; managing your vehicle’s daily expenses is just as crucial. For instance, Fleetmaxx Solutions provides a way to compare fuel management solutions, helping you keep your refuelling costs under control while you move between jobs.

Calculating Your Break-Even Point

Let’s look at the numbers. If you process £5,000 a month at a 1.75% flat rate, you pay £87.50. With a merchant rate of 0.4% plus a £20 rental fee, your cost is only £40. That is a saving of £47.50 every single month. Pay-as-you-go models are fine for hobbyists or those with very low volumes. Professional tradespeople need predictable, lower costs to protect their margins. Be wary of “Next Day Funding” claims in flat-rate apps; they often charge extra for this service, whereas merchant accounts frequently include it as standard.

Fairness and Transparency in Fee Structures

Clarity is key when reviewing any payment contract. You should look for a no-nonsense approach with reasonable contract lengths and clear exit fees. Some providers hide “PCI Non-Compliance” fees in the small print. These are avoidable charges if you complete a simple annual security profile. Security also involves understanding your responsibilities when handling fraudulent payments and disputes. A fair partner acts as a supportive ally, helping you navigate these issues without adding hidden markups to your bill. This transparency builds the trust necessary for a long-term business partnership.

Setting Up for Success: A Checklist for On-Site Payments

Getting your card machine for tradesmen UK operational is a straightforward process if you have your paperwork in order. You’ll typically need to provide proof of your business address and a recent business bank account statement. This verification process is a mark of a professional merchant setup. It ensures your funds are handled securely and transparently. Unlike the instant sign-up apps mentioned earlier, this step secures the lower rates that protect your profit margins.

Once your hardware arrives, decide on your primary connection. If you’ve opted for a SIM-based mobile machine, check the signal strength in your van before heading to your first job. We always recommend performing a small test transaction of £1.00. This confirms the link between your terminal and your bank account is active. It’s better to find a signal dead-spot now than when you’re standing in front of a client with your tools packed away.

Don’t keep your new capability a secret. Add “All Major Cards Accepted” stickers to your van and include the logos on your flyers. This small change often leads to more bookings from customers who prefer the security of card payments over bank transfers. It signals that you’re a modern, reliable professional who values customer convenience.

Managing Your Cash Flow

Cash flow is the lifeblood of any trade business. Setting up Next-Day Funding ensures your material budget stays healthy. It allows you to pay for supplies for tomorrow’s job using today’s earnings. You can also use built-in transaction reports to track which jobs are most profitable over time. Many tradespeople use these reports to organise their tax set-aside automatically. This removes the stress of a surprise bill from HMRC at the end of the quarter.

The Business Cash Advance Advantage

Your card turnover creates a valuable digital history. This record can act as a credit score for a Business Cash Advance. Unlike a traditional bank loan, this unsecured capital is based on your future card sales. It’s a flexible way to fund new tools or a van upgrade without the rigid monthly repayments of a bank. You simply pay back a small percentage of each card transaction as you earn. This makes it a supportive tool that works with your seasonal fluctuations rather than against them. If you’re ready to grow, you can apply for a Business Cash Advance to take your trade to the next level.

PurePay Hub: Transparent Payment Solutions for the Modern Trade

Choosing a card machine for tradesmen UK shouldn’t feel like a gamble. We built PurePay Hub to be the fair partner you’ve been looking for. Our “no-nonsense” approach means you get technical precision without the corporate jargon. While many providers hide markups in complex fee structures, we prioritise clarity. You deserve to keep more of your hard-earned money. That is why our debit card charges start from just 0.3%. This is a significant shift from the high flat rates that often drain the profits of regional businesses.

Next-day access to funds comes as standard with our service. We know your business doesn’t stop; your cash flow shouldn’t either. Whether you need to restock materials or cover a van repair, having your takings in your account by the next morning is a stabilising force. If you ever run into a hitch, our dedicated UK support team is here to help. We understand the local merchant community because we are part of it. You won’t be left hanging by a distant financial institution when you’re in the middle of a job.

Tailored Terminals for the Road

Our mobile units are designed specifically for the professional who lives and works out of a van. These are not flimsy gadgets. They are robust, professional-grade tools. Each Mobile Card Machine features integrated systems that connect your on-site payments directly with your back-office reports. This automation eliminates hours of manual data entry. If you encounter a signal issue or a technical question whilst on a job, our support team provides immediate, calm advocacy to get you back to work. We focus on efficiency so you can focus on your trade.

Partnering for Growth

We view ourselves as a supportive business ally rather than just a service provider. As your turnover grows, our solutions scale with you. This partnership includes access to a Business Cash Advance to bridge the gap between large-scale projects. It provides the capital you need for growth without the rigid constraints of traditional bank lending. We are committed to transparency and honesty in every transaction. If you are ready to see how much you could save with PurePay Hub, our team is standing by to help you make the switch.

Secure Your Business Future Today

The shift toward digital payments is a necessity for any modern professional. By choosing a dedicated card machine for tradesmen UK, you eliminate the stress of chasing bank transfers and the security risks of carrying large amounts of cash in your van. You now understand how mobile terminals provide the essential connectivity needed for rural jobs and why merchant accounts offer a more sustainable fee structure than basic, flat-rate apps. It’s about protecting your margins whilst providing the convenience your customers expect in 2026.

PurePay Hub acts as your supportive business ally. We offer debit rates starting from 0.3% and provide next-day funding as standard to keep your material budget healthy. Our no-nonsense approach ensures you always have clarity regarding your costs with no hidden markups to cloud your books. We believe in providing the tools you need to grow without the administrative headaches of traditional banking. Switch to PurePay Hub for lower rates and next-day funding and take the first step toward a more reliable cash flow. Your trade deserves a payment partner that works as hard as you do every single day.

Frequently Asked Questions

Do I need a separate business bank account to use a card machine?

You will need a dedicated business bank account to clear funds through a professional merchant service. Most providers require this to verify your trade status and keep your professional income separate from personal spending. Having a separate account also simplifies your VAT and tax reporting whilst ensuring your business remains compliant with UK financial regulations.

What is the cheapest card machine for a sole trader in the UK?

The cheapest option depends on your monthly turnover rather than just the upfront cost of the hardware. Whilst a pay-as-you-go reader has a low initial price, high transaction fees can eat into your profits as your business grows. For established professionals, a card machine for tradesmen UK with a lower merchant service charge often results in the lowest total cost.

Can I take card payments if there is no Wi-Fi at the job site?

You can certainly take payments without Wi-Fi by using a Mobile Card Machine equipped with a built-in SIM card. These devices connect to 4G or GPRS networks to process transactions from driveways, gardens, or building sites. This ensures you never have to ask a customer for their Wi-Fi password or worry about signal dead-zones inside a property.

How long does it take for the money to reach my account?

Most modern payment providers offer next-day funding as standard to help you manage your material budget. Some services even provide instant settlement, moving the funds into your account within seconds of the transaction. You should check your specific contract terms to ensure your cash flow remains steady and predictable for your next project.

Are there any hidden fees like PCI compliance that I should worry about?

PCI compliance is a mandatory security standard, but you shouldn’t be surprised by non-compliance fees. These charges are easily avoided by completing a simple annual security profile to prove your business handles data safely. Transparent partners will guide you through this process to ensure you aren’t hit with unnecessary costs on your monthly statement.

Can I take payments over the phone with a mobile card machine?

You can take phone payments using a Virtual Terminal or by sending a secure Payment Link to the customer’s mobile. This is ideal for taking deposits before you arrive on-site or for settling invoices after you’ve left the property. It provides a professional alternative to manual card entry and keeps your transaction history organised in one place.

Is it better to buy a card reader or rent a professional terminal?

Renting a professional terminal is often the better choice for full-time tradespeople who need reliability and lower rates. Whilst buying a basic reader is fine for occasional jobs, a rented terminal usually comes with better technical support and much lower transaction fees. This setup respects your profit margins and provides a more dependable tool for daily use.

What happens if the card machine breaks whilst I am at a customer’s house?

If your hardware fails whilst you are on-site, you can use a backup method like a Payment Link sent via SMS. This allows the customer to pay securely on their own device whilst you pack up your tools. Professional merchant partners also provide rapid technical support and replacement services to ensure your business stays operational with minimal downtime.