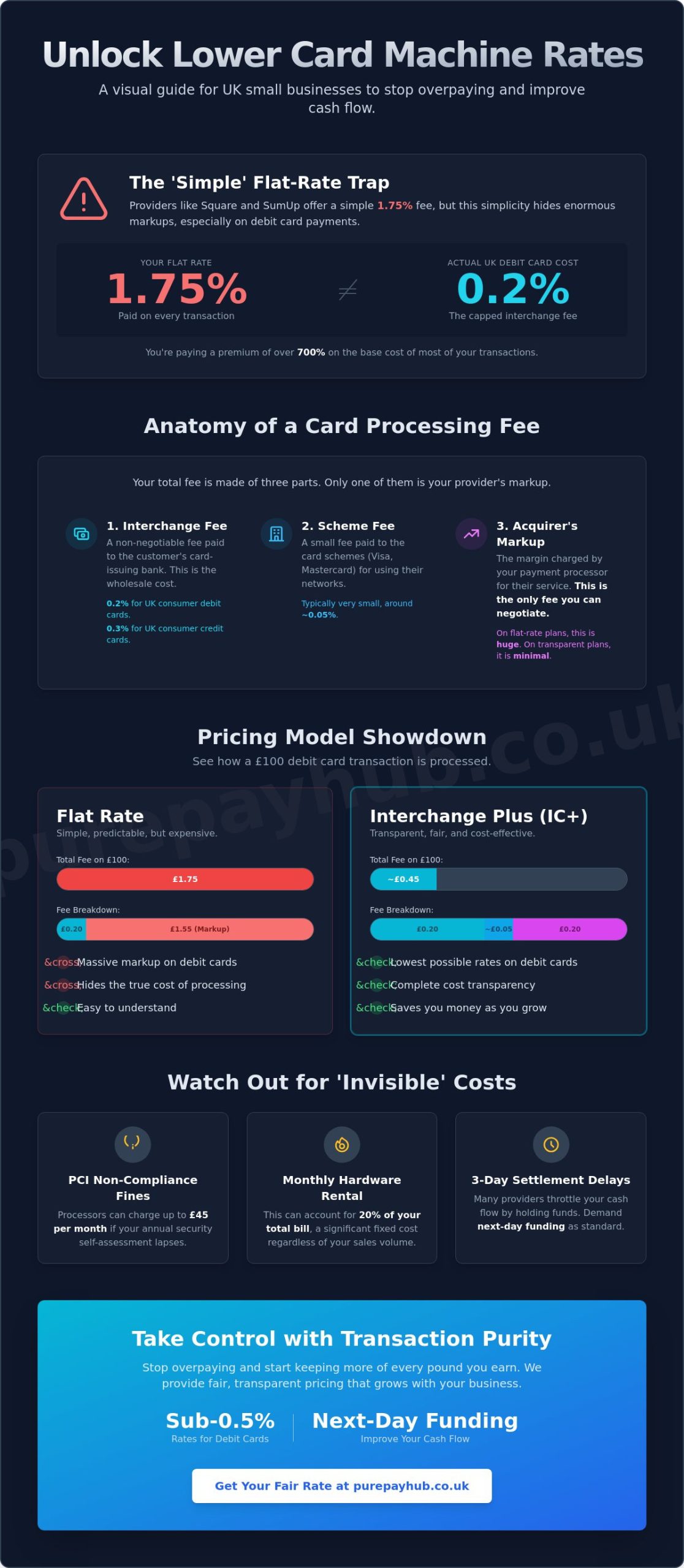

The “flat-rate” 1.75% fee you are currently paying might feel simple, but it is likely the most expensive way to run your shop or cafe. Whilst providers like Square and SumUp offer predictability, they often mask the reality that UK domestic debit card interchange fees are capped at a mere 0.2%. If you are hunting for the lowest card machine rates for small business UK, chasing a single headline figure is a trap that hides significant markups. You need a payment partner that prioritises transaction purity over padded margins.

We know you are tired of seeing your cash flow throttled by three-day settlement delays and confusing monthly statements. This guide promises to show you how to slash transaction costs to sub-0.5% for debit cards while securing the next-day funding your business requires. We will break down the 2026 market landscape, explain the impact of the latest PSD3 regulations, and reveal the most transparent providers available today. It is time to stop settling for opaque pricing and start keeping more of every pound you earn.

Key Takeaways

- Understand why the “lowest” rate is subjective and depends entirely on your specific turnover, average transaction value, and industry sector.

- Learn to decode your merchant statement by identifying the core interchange fee and spotting hidden markups that inflate your monthly costs.

- Discover why moving from a flat-rate fee to an Interchange Plus model is the most effective way to unlock the lowest card machine rates for small business UK.

- Follow a clear framework to audit your current payment setup and use your annual card turnover to negotiate a fairer, more transparent deal.

- Explore how transaction-based purity can provide your business with sub-0.5% rates and next-day funding to significantly improve your cash flow.

Understanding the UK Card Machine Market in 2026

Traditional high-street banks no longer hold a monopoly on how you take payments. In 2026, the UK merchant services market has matured into a competitive ecosystem where agility beats legacy. Most business owners are moving away from restrictive bank-led contracts toward specialised providers that treat payment processing as a central financial hub. Finding the lowest card machine rates for small business UK requires looking beyond the big bank logos and understanding how your specific trade impacts your bottom line.

A “low” rate is entirely subjective. For a high-volume coffee shop with a £5 average transaction value (ATV), a fixed fee might be a burden. Conversely, a luxury furniture retailer with a £2,000 ATV needs a different structure entirely. Your monthly turnover and transaction patterns dictate which pricing model is actually the cheapest. We believe your payment provider should act as a merchant’s ally, offering clarity instead of complexity through a transaction-based “Hub” approach that stabilises your finances.

The Evolution of Payment Processing for SMEs

We have moved past the era of clunky, tethered countertop units that restricted service to a single point. Today, UK SMEs favour portable and mobile-first solutions that integrate directly with their EPOS systems. With cash usage predicted to fall to just 4% by 2034, being “cashless” is no longer an option; it is the non-negotiable standard. We advocate for “Pure” processing, which ensures your transaction data is untainted by the legacy markups that traditional banks still try to enforce. This shift allows you to accept payments anywhere in your premises, matching the modern consumer’s expectation for speed and convenience.

Why Headline Rates Can Be Deceptive

Flashy marketing often hides an expensive reality. Many providers lure you in with “0% for 3 months” offers that eventually revert to punishingly high long-term percentages once the honeymoon period ends. It is vital to distinguish between a merchant account and a payment aggregator. While aggregators offer quick setup, they often lack the depth of a dedicated merchant account when it comes to volume-based discounts. You might start on a flat rate, but as your business grows, that simplicity becomes a tax on your success.

A critical component of your total cost is Interchange fees, which are the non-negotiable costs paid to the card issuer. To find the lowest card machine rates for small business UK, you must look at the total package, not just the teaser rate. The Merchant Service Charge is the core fee merchants must optimise to ensure they aren’t overpaying for the privilege of getting paid. By stripping away hidden markups, you can finally achieve the transparency your business deserves.

The Anatomy of Card Processing Fees: What “Lowest” Really Means

Understanding the true cost of taking payments requires looking past the headline percentage. To secure the lowest card machine rates for small business UK, you must dissect three specific pillars: transaction fees, hardware rental, and administrative charges. Most merchants focus solely on the transaction fee. Yet, monthly hardware rental and admin costs often represent 20% of the total bill for smaller enterprises. This complexity is often a deliberate choice by traditional providers to obscure their margins. PurePay Hub simplifies this by stripping away the jargon and focusing on transaction-based clarity.

Decoding the Interchange Fee

The interchange fee is the non-negotiable baseline of every transaction. It’s the fee paid to the customer’s bank. In the UK, domestic consumer debit cards are capped at 0.2% and credit cards at 0.3%. These rates are fixed by card schemes like Visa and Mastercard. However, these caps don’t apply to commercial or international cards. Following Brexit, cross-border fees for EEA cards rose significantly, with debit cards hitting 1.15% and credit cards reaching 1.5%. You can find more detail in this complete guide to credit card processing fees to see how these stack against your current statement.

The “Invisible” Costs: PCI Compliance and Admin

PCI DSS compliance is a mandatory security standard for everyone accepting card payments. Many providers charge a nominal monthly fee for this, but the real danger lies in “non-compliance” penalties. Some processors use these fines as a profit centre, charging up to £45 per month if your annual self-assessment isn’t updated. It’s a frustrating and unnecessary drain on your resources that many business owners overlook until the statement arrives.

Hardware rental is another area where costs can creep up. A portable card machine should include all software updates and technical support within the base price. You shouldn’t be charged extra for “gateway fees” or “statement fees” that provide no additional value. We promote “Pure” processing. This means we eliminate the murky “Hub” or “Platform” fees that other companies tack onto your statement. If you want a partner that acts as a transparent merchant ally, it starts with knowing exactly where every penny of your processing fee goes. By removing these hidden layers, you ensure your business keeps more of its hard-earned revenue.

Comparing Pricing Models: Flat Rate vs. Interchange Plus

Choosing between a flat-rate and an Interchange Plus (IC+) model is often the difference between a thriving margin and a struggling one. Flat-rate providers charge a single percentage, typically around 1.75%, regardless of the card type used. This simplicity comes at a high price. High-volume businesses on these plans are effectively subsidising the costs of smaller, riskier merchants. When you pay a flat fee, you are paying a premium for convenience that rarely reflects the actual cost of your specific transactions.

The Payment Systems Regulator market review highlights how complex fee structures can limit competition and transparency. Over a 12-month period, a typical SME processing £10,000 monthly on a 1.75% flat rate will spend £2,100 in transaction fees. Switching to an IC+ model could reduce this significantly, as it separates the non-negotiable interchange fee from the provider’s markup. This transparency is the only way to secure the lowest card machine rates for small business UK as you scale.

When is a Flat Rate Actually Better?

Flat rates are designed for micro-merchants. If your business processes under £2,000 per month, the predictability of a fixed fee is often worth the higher percentage. It suits seasonal sole traders or hobbyist businesses that need a simple “pay-as-you-go” structure without monthly commitments. However, this model quickly becomes a growth trap. As your turnover increases, that 1.75% starts to eat into your scaling margins, costing you hundreds of pounds more than a tailored merchant account would.

The Power of Interchange Plus (IC+) for Growing SMEs

Interchange Plus is the gold standard for professional merchant services. It offers total “Pure” transparency by showing you the exact cost of the transaction plus a small, fair margin. For instance, whilst a flat rate might charge you 1.75% for a domestic debit card payment, an IC+ model reveals the 0.2% capped interchange fee and adds a transparent markup. This can lead to an effective rate as low as 0.3% for debit transactions. PurePay Hub specialises in tailoring these rates to business volume. By moving away from the “one-size-fits-all” approach, you ensure your payment setup acts as a central Hub for growth rather than a drain on your resources.

How to Secure the Lowest Card Machine Rates for Your Business

Securing a better deal requires more than just a quick search; it demands a forensic look at your current statement. Many providers hide their true margins in a thicket of technical terms. To find the lowest card machine rates for small business UK, you must look beyond the headline percentage and evaluate the total cost of ownership. This involves auditing your existing fees, understanding your leverage, and avoiding long-term terminal rental traps that can cost your business thousands over a three-year contract.

Your annual Gross Transaction Value (GTV) is your biggest bargaining chip. If your turnover has grown by 20% or more since you last signed a contract, you are likely overpaying. Providers are eager for stable, growing businesses. You should use your actual processing data to demand a bespoke rate rather than accepting a generic off-the-shelf package. Always check for a Minimum Monthly Service Charge (MIRA). If your transaction volume drops during a quiet month, a high MIRA ensures the provider still gets paid, even if you don’t. We believe you should only pay for the value you receive.

Auditing Your Current Merchant Statement

The most important number on your statement isn’t the headline rate; it’s your Effective Rate. You calculate this by dividing your total monthly fees by your total turnover. It’s common to see a “headline” rate of 1.5% jump to an effective rate of 2.5% once you add in authorisation fees, which can range from 1p to 5p per tap. Check your statement for “Minimum Monthly Fees” and “PCI Non-Compliance” charges. These small, recurring amounts are designed to stay under the radar whilst padding the processor’s profits. Identifying these markups is the first step toward reclaiming your margin.

Switching Providers Without the Stress

The fear of downtime often keeps merchants trapped in bad contracts. However, the “Right to Switch” and modern onboarding processes have made the transition smoother than ever. Most exit fees can be offset by the savings you’ll make in the first three months with a fairer partner. The key is ensuring your new Merchant IDs (MIDs) are ready before you disconnect your old hardware. PurePay Hub offers quick onboarding to facilitate seamless transitions, acting as a supportive ally throughout the move. If you are ready to stop the drain on your profits, you can get a transparent fee audit today and see the difference transaction-based purity makes.

PurePay Hub: Transparent, Transaction-Based Payments for UK Growth

PurePay Hub isn’t just another payment processor. We act as your merchant’s ally by stripping away the complexity that traditional banks rely on to inflate their profits. By focusing on transaction-based purity, we offer starting rates of 0.3% for debit cards and 0.5% for credit cards. These figures represent some of the lowest card machine rates for small business UK currently available. We understand that a low rate is only half the battle. Your business also needs liquidity to thrive.

Whilst traditional banks might keep you waiting up to five working days for your own money, we provide next-day access to funds as standard. This ensures you can restock inventory or pay staff without the stress of delayed settlements. This integrated approach turns your payment terminal from a simple tool into a central Hub for financial stability. We provide the transparency you need to plan for the future with confidence and clarity.

Fairness and Clarity as Standard

We take a no-nonsense approach to fee structures. Unlike shared aggregators that often provide limited support and opaque pricing, we give you a dedicated merchant account tailored to your specific turnover. This direct relationship allows for greater flexibility and lower costs as you scale. If your business requires a boost for expansion, we also offer Business Cash Advances based on your card sales. This growth tool provides a fair alternative to traditional bank loans, with repayments that fluctuate naturally with your daily takings. You only pay back more when you are busy, and less when things are quiet.

Choosing Your Hardware: From Countertop to Mobile

Every UK business has unique requirements for its physical point of sale. We offer a range of solutions to fit your specific sector:

- Countertop Card Machines: Ideal for retail shops or pharmacies with a fixed till point and a stable internet connection.

- Portable Card Machines: Perfect for restaurants or cafes that need to take payments at the table via Wi-Fi or Bluetooth.

- Mobile Card Machines: A must-have for tradespeople or market stalls that require GPRS or 4G connectivity on the move.

Integrating these terminals with your EPOS system further reduces admin time and eliminates costly manual accounting errors. It’s about more than just a machine; it’s about a partnership that supports your long-term growth. Get a transparent quote from PurePay Hub today and start keeping more of every transaction your business processes.

Take Control of Your Transaction Costs

Finding the lowest card machine rates for small business UK isn’t about luck; it’s about data and transparency. You’ve seen how auditing your monthly statements can uncover hidden authorisation fees and why the common flat-rate model often acts as a growth tax on your success. By switching to a transaction-based model, you reclaim the margin that traditional banks have quietly siphoned away for years. It is time to treat your payment processing as a strategic asset rather than a fixed expense that drains your monthly revenue.

PurePay Hub provides the clarity you need to scale with confidence. We offer debit rates starting from 0.3% and ensure your cash flow remains healthy with next-day funding available as standard. You won’t find any hidden markups or murky fee structures here. We act as your merchant ally, providing the honest partnership your business deserves to thrive in a competitive market. Secure your lowest card machine rate with PurePay Hub today and keep more of your hard-earned revenue. Your business deserves a fair deal.

Frequently Asked Questions

What is the average card machine rate for a small business in the UK?

The average flat rate for a UK small business is 1.75% per transaction. However, this figure is often much higher than the actual cost of processing, as domestic debit interchange is capped at 0.2%. If you process over £2,000 monthly, you should move away from averages and seek the lowest card machine rates for small business UK through an Interchange Plus model.

Is it cheaper to buy or rent a card machine for my business?

Choosing between buying or renting depends on your monthly turnover and need for technical support. Buying a terminal upfront for around £19 plus VAT removes monthly rental costs, which suits micro-merchants or seasonal traders. For established SMEs, renting a professional portable card machine ensures you receive essential software updates and 24/7 technical support without a large initial capital outlay.

How do I avoid high exit fees when switching card machine providers?

You can avoid high exit fees by prioritising providers that offer rolling monthly contracts or shorter 12-month terms. Always scrutinise the “Term” section of your agreement before signing. If you are already trapped, some new providers might offer to cover a portion of your exit costs to help you switch to a fairer, more transparent processing model.

What is the difference between a transaction fee and a merchant service charge?

A transaction fee is typically a fixed cost in pence for each tap or dip of a card. The Merchant Service Charge (MSC) is the percentage fee applied to the total value of the sale. To find the lowest card machine rates for small business UK, you must look at the combined total of both these figures on your monthly statement.

Can I get a card machine with no monthly fees as a sole trader?

Sole traders can access card machines with no monthly fees through payment aggregators. These providers don’t charge for the Hub or platform access, but they compensate for this with much higher transaction percentages, often 1.75% or more. It’s a trade-off between fixed monthly costs and the variable cost of every sale you make.

What happens if my business doesn’t meet the minimum monthly transaction volume?

If your business fails to meet a specific transaction threshold, you may be charged a Minimum Monthly Service Charge (MIRA). This fee ensures the provider covers their overheads even during your quietest months. It’s usually a fixed amount, such as £10 or £15, which is only billed if your total transaction fees for that month fall below that level.

How long does it take for card payments to reach my UK bank account?

Card payments typically reach UK bank accounts within one to three working days. Whilst traditional banks and older processors often lean toward the longer end of this scale, modern fintech partners prioritise your cash flow. PurePay Hub offers next-day access to funds to ensure your business remains liquid and ready for daily operational expenses.

Are there extra charges for accepting Apple Pay or Google Pay?

There are no additional fees specifically for accepting Apple Pay or Google Pay on your terminal. These digital wallet payments are processed as standard contactless transactions using the underlying card’s domestic or international rate. They are a secure, high-speed way to take payments that 85% of UK consumers now prefer over cash.