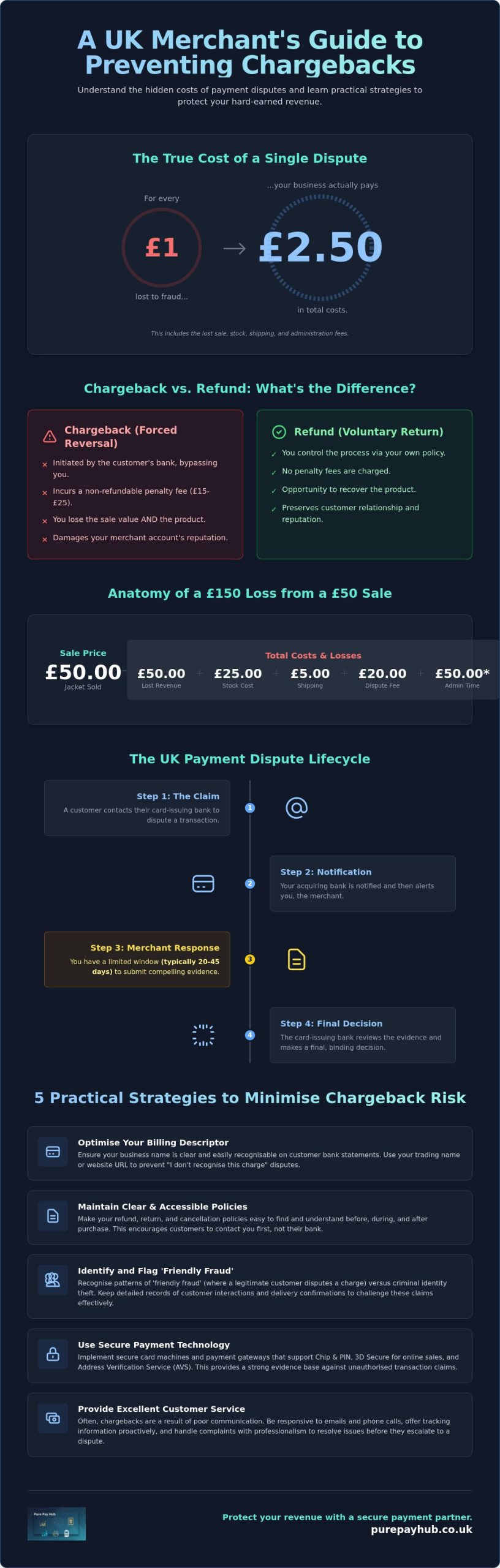

Did you know that for every £1 lost to fraud, the average UK merchant actually pays out £2.50 once administration fees and lost stock are tallied? It’s a staggering drain on your hard-earned revenue that goes far beyond the initial transaction. If you feel like the system is weighted against you, you’re certainly not alone. Losing both your product and the sale price to a dispute is incredibly frustrating, especially when it feels like a customer is simply bypassing your refund policy to claim their money back. You deserve a payment partner that helps you fight back against these hidden costs.

This guide explains exactly how to prevent chargebacks UK small businesses face in 2026. We’ll show you how to protect your bank account from ‘friendly fraud’ and secure your payment process with practical, no-nonsense strategies. We’ll explore how to upgrade your payment hardware, clarify the difference between refunds and disputes, and master the specific evidence required to win your case. By the end, you’ll have a clear roadmap to keep your chargeback ratio well below the 1.5% threshold and keep more of what you earn.

Key Takeaways

- Understand the true cost of disputes, which includes lost inventory, shipping expenses, and non-refundable bank fees.

- Optimise your billing descriptor to ensure your business name is easily recognisable on customer statements, reducing accidental disputes.

- Learn exactly how to prevent chargebacks UK merchants face by implementing clear, accessible refund and return policies.

- Identify the difference between criminal identity theft and ‘friendly fraud’ to better protect your revenue and stock.

- Discover how secure card machines and next-day funding can stabilise your cash flow whilst you manage payment disputes.

What is a Chargeback and Why is it Rising in the UK?

A chargeback is more than just a simple reversal of funds. It is a consumer protection mechanism that allows a cardholder to bypass the merchant and go straight to their bank to demand their money back. Essentially, what is a chargeback is a safety net designed to protect shoppers against fraud or businesses that fail to deliver. However, for a small business owner, it represents a significant operational hurdle that can disrupt your cash flow without warning.

In 2026, the UK landscape has shifted significantly for retailers and service providers. Recent data indicates that 1 in every 200 payments now results in a dispute. This rising trend makes learning how to prevent chargebacks UK businesses face an essential survival skill for anyone accepting card payments. Consumers are becoming more aware of their rights, but this awareness often leads to an increase in disputes that could have been resolved through simple communication.

You might wonder why a chargeback is considered more damaging than a standard refund. When you issue a refund, you remain in control of the process. You keep your processing reputation intact and avoid penalty fees. A chargeback is forced upon you by the bank. You lose the sale and the stock, but you’re also hit with a non-refundable administration fee. These fees often range from £15 to £25 per incident, regardless of whether you eventually win the dispute.

Chargebacks vs. Section 75: Knowing the Difference

UK merchants must distinguish between card scheme chargebacks and Section 75 of the Consumer Credit Act 1974. Section 75 is a legal requirement for credit card purchases between £100 and £30,000. It makes the card provider jointly liable with the retailer for any breach of contract or misrepresentation. Whilst chargebacks apply to both debit and credit cards and are governed by card network rules, Section 75 is a statutory right that provides shoppers with a much stronger legal footing. Understanding how to prevent chargebacks UK requires you to recognise that high-value credit card sales carry this additional layer of legal liability.

The Lifecycle of a UK Payment Dispute

The dispute process follows a strict, time-sensitive path. It begins when a customer contacts their issuing bank to claim a transaction was unauthorised or the goods were faulty. The bank then notifies your ‘acquirer’, which is the bank that processes your card payments. Your acquirer will then alert you to the claim. You don’t have an indefinite amount of time to fight back. Merchants typically have between 20 and 45 days to provide evidence, such as proof of delivery or signed receipts. The issuing bank holds the final word, acting as the judge in the dispute resolution process. If you fail to respond within the deadline, the funds are permanently returned to the customer.

The Financial Impact: Why You Cannot Ignore Disputes

Disputes are an expensive drain on your business resources. When a customer triggers a reversal, you lose far more than the initial sale price. You lose the physical stock, the original shipping costs, and the merchant service charges. On top of this, you’re hit with a non-refundable chargeback fee that stands regardless of the outcome. For every £1 of fraud, UK merchants can spend up to 2.5 times the transaction value on related costs. This is why knowing how to prevent chargebacks UK is a financial necessity, not just a security preference.

Even if you win the dispute, the victory is often bittersweet. You’ve spent hours hunting down proof of delivery and communication logs. That time could have been spent growing your business or serving loyal customers. The card networks also record the incident regardless of the final decision. A history of frequent disputes makes you look like a high-risk partner. This reputational damage can lead to higher rolling reserves or restricted access to newer payment technologies. Using a secure payment gateway helps you keep these metrics in the green and your reputation intact.

Calculating the Total Cost of a Single Dispute

Let’s look at a typical UK retail scenario. Suppose you sell a jacket for £50. If that customer files a dispute, you lose the £50 immediately. You’ve already paid £25 for the stock and £5 for shipping. Your processor then charges a £20 dispute fee. Add in two hours of administrative time to gather evidence, and your £50 sale has morphed into a £150 total loss. These figures quickly erode the thin margins small businesses rely on to survive. For a regional merchant, just a few of these incidents a month can turn a profitable week into a deficit.

The ‘Chargeback Ratio’ and Your Merchant Account

Your chargeback ratio is a simple calculation: the number of disputes divided by your total monthly transactions. Card networks like Visa and Mastercard keep a close eye on this percentage. If your volume creeps too high, they place you into monitoring programmes like Visa’s Acquirer Monitoring Program (VAMP). As of 2026, the threshold for “excessive” disputes in the UK is just 1.50%. If you exceed this, you face higher processing rates or even the total termination of your merchant account. You can find this metric on your monthly merchant statements. Monitoring it allows you to spot trends early and adjust your fraud prevention settings before the banks intervene.

Identifying the Threat: Fraud vs. Friendly Fraud

To master how to prevent chargebacks UK businesses must first look beyond traditional theft. Whilst criminal fraud involves bad actors using stolen credentials, a much larger threat comes from your own customer base. Understanding the difference between these two categories is essential for protecting your revenue. Criminal fraud is a deliberate attack on your system, whereas ‘friendly fraud’ is often accidental or a result of consumer confusion. Both result in the same financial loss, but they require very different defensive strategies.

Traditional security tools are excellent at spotting stolen cards, but they struggle to identify a legitimate customer who later regrets a purchase. Research indicates that friendly fraud now accounts for between 75% and 86% of all chargebacks. This means the majority of your disputes aren’t coming from hackers, but from people who have actually walked through your doors or used your website. Recognising this shift is the first step toward a more secure payment environment.

Red Flags for Criminal Fraud in Your Shop

Why ‘Friendly Fraud’ is a Growing UK Problem

Friendly fraud is the primary cause of modern UK disputes, often occurring when a customer doesn’t recognise the business name on their bank statement. Confusing billing descriptors cost UK merchants over £128 million annually. If your bank statement name doesn’t match your shop sign, a customer might assume the charge is fraudulent and contact their bank immediately. We also see a rise in ‘buy now, regret later’ behaviour. A shopper might forget they signed up for a subscription or simply decide they want their money back without returning the item. Because these transactions involve legitimate cards and verified addresses, they bypass most standard fraud filters. This is why clear communication and recognisable branding on every transaction are your best defences in learning how to prevent chargebacks UK wide.

5 Practical Strategies to Minimise Chargeback Risk

Proactive prevention is your best defence. Whilst you cannot control every customer’s behaviour, you can certainly control your business’s response. Implementing these five strategies will help you build a more resilient payment environment. Learning how to prevent chargebacks UK merchants face involves closing the gaps where confusion and fraud thrive. By making a few simple adjustments to your daily operations, you can significantly reduce the likelihood of a bank reversing your hard-earned funds.

Perfecting Your Billing Descriptors

Confusion is the leading cause of ‘friendly fraud’. If a customer sees an unrecognisable name on their banking app, they will likely panic and report it. Take a moment to check exactly what appears on mobile bank statements for your transactions. Your billing descriptor should match your shop sign or website name perfectly. If your legal name is different from your trading name, update it with your payment provider immediately. Adding a phone number or a short URL to the descriptor is also a brilliant way to encourage customers to call you first before they call their bank.

Receipt Management and Evidence Gathering

Winning a dispute requires a solid paper trail. You need to gather specific evidence like tracking numbers, signed invoices, and IP addresses for digital sales. Banks operate on a very strict timeline. You must have these records organised and ready to go. An integrated EPOS System is invaluable here. It allows you to link every sale to a specific customer profile and transaction history. Having this data at your fingertips makes it much easier to respond within the narrow 20 to 45-day window that banks allow for evidence submission.

Communication as a Defence Mechanism

Clear communication stops disputes before they start. Send an instant email or SMS receipt for every transaction, even for in-person sales. If a delivery is delayed or a service is postponed, tell the customer immediately. Managing their expectations reduces the frustration that leads to chargebacks. Remember that a quick refund is always cheaper than a lost dispute. If a customer is unhappy, it’s often better to return the funds yourself rather than risk the administrative fees and reputational damage of a forced reversal.

Your hardware choice also plays a vital role in your security. Modern Countertop Card Machines and Portable Card Machines come with built-in encryption and 3D Secure support for remote payments. These features ensure that every transaction is authenticated and tracked, giving you the best possible protection against both criminal and accidental fraud. If you’re ready to upgrade your security, you can view our range of secure card machines to find the right fit for your business.

How PurePay Hub Helps You Protect Your Revenue

At PurePay Hub, we position ourselves as a fair partner to regional business owners rather than a distant financial institution. We understand the frustration of hidden costs and the complex fee structures that traditional providers often hide behind. Our mission is to provide a reliable, untainted service that lets you focus on your business growth. When you are researching how to prevent chargebacks UK, you will find that speed and clarity are your best weapons. We provide next-day access to your funds, ensuring your cash flow remains steady even whilst you are gathering evidence for a dispute. This immediate liquidity acts as a stabilising force for your finances.

We take a no-nonsense approach to security, stripping away the corporate jargon to provide tools that actually work. Our relationship is built on calm advocacy; we want to alleviate the stress caused by payment disputes through transparent reporting and robust hardware. By choosing a partner that values integrity over hidden markups, you can build a payment environment that is both efficient and highly dependable. We are here to help you navigate the 2026 landscape with informed confidence.

Secure Card Machines for Every Business

Our hardware is designed for maximum efficiency and transparency. Whether you use a Countertop Card Machine for your main till or a Portable Card Machine for floor service, you are protected by the latest encryption standards. These devices serve as your first line of defence against point-of-sale fraud. For remote transactions, our Virtual Terminal and Payment Links use 3D Secure authentication. This technology is vital because it shifts the liability for unauthorised claims away from your business and onto the card issuer. All PurePay Hub hardware is fully PCI compliant, ensuring you meet the highest security standards without the stress of navigating technical manuals alone.

Transparent Reporting and Support

We believe that informed confidence is the key to a successful business. Our merchant portal provides a clean, modern interface where you can track every transaction in real-time. This level of visibility allows you to spot suspicious patterns or duplicate charges before they trigger a bank reversal. If you are ever confused by your monthly statement, our UK-based support team is always available to help. We speak your language, not industry jargon, and we are committed to helping you understand how to prevent chargebacks UK wide. We avoid the opaque practices of our competitors, offering a straight-talking service that treats you as a direct partner. Protect your business with a secure PurePay Hub card machine today.

Secure Your Revenue and Minimise Dispute Risks

Managing payment disputes doesn’t have to be a source of constant anxiety. By refining your billing descriptors and maintaining meticulous records, you’ve already taken the most important steps in learning how to prevent chargebacks UK businesses encounter. Remember that clear communication often resolves a problem before it ever reaches a bank. Whether it’s an instant digital receipt or a proactive update on a delayed delivery, these small touchpoints protect your reputation and your bank balance.

You deserve a payment partner that prioritises your stability over hidden markups. PurePay Hub offers a transparent approach to card processing with debit card rates starting from 0.3% and next-day access to your funds. We’ve removed the surprise monthly fees found elsewhere, providing a clear and dependable service designed specifically for local merchants. You can focus on growth whilst we handle the technical security.

Switch to PurePay Hub for secure, transparent card processing. Take control of your payment security today and keep your focus on what you do best: running your business.

Frequently Asked Questions

Can I refuse a chargeback if I have proof of delivery?

Yes, you can challenge a chargeback using proof of delivery as your primary evidence. You must submit this during the representment phase, which usually lasts between 20 and 45 days. Signed delivery notes or GPS tracking data from your courier are incredibly effective for proving that the customer received the goods as described.

How long does a customer have to file a chargeback in the UK?

Customers generally have 120 days from the transaction date to file a claim with their bank. However, this window can extend up to 540 days if the goods or services were intended for a future date or were never delivered. It’s vital to keep your transaction records organised for at least two years to stay protected against late claims.

What is a ‘friendly fraud’ and how do I spot it?

Friendly fraud occurs when a legitimate customer disputes a valid purchase they actually made. You can spot this by looking for customers who claim they don’t recognise your business name on their bank statement. It often happens when your trading name differs from your legal name, causing confusion when the shopper reviews their monthly outgoings.

Does a refund stop a chargeback from happening?

A proactive refund stops a chargeback if you process it before the customer contacts their bank. This is a key strategy for how to prevent chargebacks UK retailers rely on to avoid high administration fees. Once the bank initiates the formal dispute process, a refund will no longer stop the non-refundable chargeback fee from being applied to your account.

What happens if my chargeback ratio goes above 1%?

Crossing the 1% threshold often triggers “high-risk” monitoring from card networks like Visa and Mastercard. You’ll likely face higher processing fees and more frequent audits from your acquirer. If the ratio reaches 1.5%, you risk having your merchant account suspended or terminated entirely, which would stop you from accepting card payments.

Are chargeback fees refundable if I win the dispute?

No, chargeback administration fees are almost never refundable. Even if you win the dispute and recover the original sale amount, the £15 to £25 fee is usually kept by the processor. This fee covers the administrative time and resources required to manage the communication between the issuing and acquiring banks.

How do I change the name that appears on my customer’s bank statement?

You must contact your payment processor to update your “billing descriptor”. This is the text that appears on mobile banking apps and paper statements. Ensure it matches your shop sign or website branding perfectly so customers recognise the charge immediately and don’t report it as suspicious activity.

Is it better to fight a chargeback or just accept it?

You should always fight a dispute if you have clear evidence of a valid sale and successful delivery. Accepting every claim makes your business look like an easy target for ‘friendly fraud’ and sets a dangerous precedent. It also keeps your chargeback ratio high, which threatens your long-term ability to maintain a merchant account.