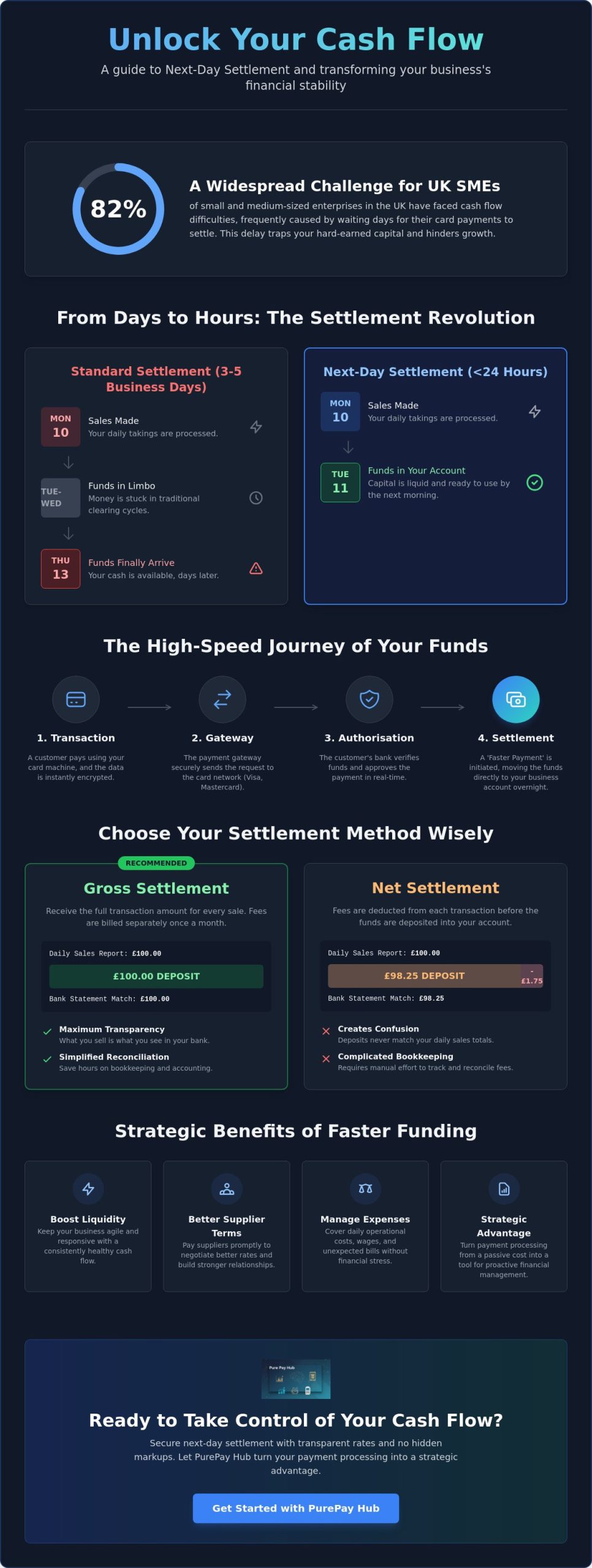

Did you know that 82% of UK SMEs have faced cash flow difficulties, often because they lack access to reliable next day settlement payment processing? It is a common frustration to see a healthy daily sales report whilst your bank balance remains stagnant for days. You have suppliers to pay and a business to grow, yet your hard-earned capital is trapped in a processing queue. This delay is a barrier to your stability.

We believe that access to your own money should be simple and reliable. This guide explains how to secure your funds within 24 hours and transform your cash flow. You will discover how to obtain faster funding without the burden of hidden costs or the confusing fee structures that often hide in the small print. At PurePay Hub, our goal is to provide the clarity you need to act as a confident partner in your own financial growth.

We will break down the latest 2026 payment regulations and provide a clear roadmap for achieving transparent, low transaction rates. We will also show you how to simplify your daily reconciliation so you can spend less time on paperwork and more time serving your customers. This is about turning your payment processing from a passive cost into a strategic advantage for your business.

Key Takeaways

- Shorten your funding cycle from several days to under 24 hours to ensure your business remains liquid whilst maintaining a healthy cash flow.

- Understand the technical steps behind next day settlement payment processing and how modern gateways bypass traditional banking delays.

- Discover how immediate access to capital allows you to negotiate better terms with suppliers and manage daily expenses without stress.

- Compare standard and next-day timelines to see exactly how Monday’s sales can reach your bank account by Tuesday morning.

- Learn how PurePay Hub organises the onboarding process to get your merchant account live with transparent rates and no hidden markups.

What is Next Day Settlement Payment Processing?

Next day settlement payment processing is a merchant service that ensures funds from card transactions reach your bank account within 24 hours. Historically, UK businesses accepted a 3-5 working day delay as an unavoidable cost of doing business. This is no longer the case. By 2026, the expectation for real-time or near-real-time funding has become the benchmark for operational efficiency. If you’re waiting a week for Monday’s takings to arrive, your business is effectively providing an interest-free loan to your bank.

There is a fundamental difference between authorisation and settlement. When your customer taps their card, an authorisation message confirms the transaction is valid. This is the moment of the sale, signified by the familiar “beep” of the card machine, but it isn’t the moment you get paid. The financial settlement process represents the actual transfer of value. Modern processing standards now allow this transfer to happen almost as quickly as the authorisation itself, moving money from a “pending” state into your available balance overnight.

The Difference Between Gross and Net Settlement

Choosing how you receive your funds is just as important as how fast they arrive. Gross settlement means you receive the total value of every sale. Your processing fees are calculated separately and usually collected via a single monthly direct debit. This model is often the favourite for UK business owners because it simplifies reconciliation. Every penny on your daily sales report appears in your bank statement, making your accounting process transparent and error-free.

Net settlement operates differently. Your provider deducts their commission from each transaction before the funds are deposited. Whilst this means you don’t have a large bill at the end of the month, it often creates a reconciliation headache. Your bank deposits will never quite match your till totals. For businesses prioritising clarity and simple bookkeeping, gross settlement is the superior choice for managing daily revenue.

Why High Street Banks Still Lag Behind

Traditional high street banks often struggle to provide these faster timelines. Many still operate on legacy systems that rely on batch processing. This method groups transactions together and processes them in fixed windows, often leading to significant delays over weekends and bank holidays. These institutions are frequently tethered to old-fashioned clearing cycles that were designed before the internet era.

Independent providers have disrupted this space by building modern, agile infrastructure from the ground up. They bypass the bureaucratic bottlenecks of traditional banking to deliver funds directly. Settlement is the final transfer of funds from the customer’s bank to yours. By choosing a partner that prioritises speed, you ensure your revenue is working for you, not sitting idle in a bank’s clearing account.

How the Next Day Settlement Process Works

The journey from a customer tapping their card to funds appearing in your balance involves several high-speed digital handshakes. In the past, these steps were separated by days of manual clearing and legacy banking delays. Today, the process is streamlined into a continuous 24-hour cycle. It’s a precise sequence where technology replaces bureaucracy to keep your cash moving.

- Step 1: The customer interacts with your hardware. Whether they use a Countertop Card Machine or a Portable Card Machine, the device captures and encrypts the transaction details instantly.

- Step 2: The payment gateway acts as a secure messenger. It transmits this data to the card networks, such as Visa or Mastercard, to request payment.

- Step 3: The issuing bank (the customer’s bank) checks for sufficient funds and fraud indicators. If the transaction is safe, they send an authorisation code back to your terminal.

- Step 4: This is where next day settlement payment processing differs from traditional models. Your acquiring bank uses the infrastructure of UK payment systems to initiate a ‘Faster Payment’ directly to your business account.

The Role of the Acquiring Bank

Your acquiring bank is the essential middleman in this process. They guarantee the funds to you before they’ve even fully collected them from the customer’s bank. This is why your choice of partner is vital. A modern acquirer provides the stability needed for reliable 24-hour funding. Older, traditional banks often have rigid “cut-off” times. If you miss their 4 pm window, you might wait an extra day for your money. Modern independent providers often offer much later cut-off times, ensuring your evening trade is included in the next morning’s payout. If you’re looking for a partner that prioritises this reliability, you can view our range of card machines designed for rapid funding. Having UK-based support is also a major advantage. If a technical glitch delays a settlement batch, you need a local expert who understands the UK banking landscape to resolve it quickly.

Security and PCI Compliance During Settlement

Speed never comes at the expense of safety. Every stage of the 24-hour cycle uses point-to-point encryption to protect sensitive data. Interestingly, faster settlement actually reduces your “risk window”. Because funds are cleared and settled quickly, there’s less time for certain types of transaction disputes to linger in a pending state. It creates a cleaner financial trail for your business. PCI DSS compliance is mandatory for all next day processing. This global standard ensures that your business and your customers remain protected against data breaches throughout the entire settlement journey.

Comparing Settlement Timelines: Next Day vs Standard

Understanding the difference between standard and next day settlement is best achieved by looking at a typical trading week. In a standard cycle, which is often the default for high street banks, a transaction made on Monday usually doesn’t arrive in your account until Friday. This is known as a T+3 or T+4 settlement period. It leaves your capital in a state of limbo for the majority of the working week.

By contrast, next day settlement payment processing ensures that those same Monday sales are available in your bank account by Tuesday morning. This shift significantly reduces the gap between making a sale and having the cash available to reinvest. This efficiency is made possible by the Faster Payment System, which allows for near-instant transfers between UK financial institutions once the initial card data is cleared.

The disparity becomes even more apparent when you consider weekends and bank holidays.

- Standard Model: Friday sales might not clear until the following Wednesday or Thursday.

- Next Day Model: Friday sales typically arrive on Monday morning, keeping your weekend revenue accessible for the start of the new week.

Bank holidays often act as “hidden” delays in the standard model, potentially stretching a 3-day wait into a 6-day ordeal. For a business with tight margins, this delay isn’t just an inconvenience; it’s a risk to operational stability.

The Real Cost of Waiting 3-5 Days

Waiting for your funds carries a measurable opportunity cost. When your money sits in a clearing account, it isn’t earning interest, paying off debt, or purchasing stock. Many UK businesses find themselves forced to use expensive overdrafts or short-term credit lines simply to bridge the gap created by their own slow payment processor. Research indicates that 82% of UK SMEs have faced cash flow difficulties, a statistic often driven by these avoidable delays. There is also a significant psychological benefit to seeing your bank balance reflect your hard work within 24 hours. It provides a sense of control and clarity that traditional banking simply cannot match.

Same-Day vs Next-Day: Is there a difference?

You might wonder if you should push for same-day settlement instead. For high-volume hospitality businesses that need to pay staff or buy fresh produce daily, same-day funding can be a necessity. However, it often comes with a higher fee premium that can eat into your profits. For the vast majority of UK SMEs, next day settlement is the “sweet spot”. It provides the speed required for healthy cash flow whilst keeping transaction costs low and manageable. It aligns perfectly with standard accounting practices, allowing for simple daily reconciliation without the added expense of ultra-fast funding options.

Strategic Benefits of Faster Funding for UK SMEs

Faster funding is more than a simple convenience; it is a strategic lever for growth. When you implement next day settlement payment processing, you improve your working capital ratio instantly. This ratio represents the difference between your current assets and your liabilities. By shortening the time it takes for sales to become cash, you make your business significantly more resilient. In 2025, 90% of UK companies experienced late payments. You can avoid this trap by ensuring your own revenue isn’t part of the problem.

Liquidity gives you the power to negotiate. You can often secure better terms or early settlement discounts with your suppliers by offering faster payments yourself. This directly boosts your profit margins. It also simplifies payroll management. If you employ casual or shift-based staff who expect prompt payment, having your weekend takings in the bank by Monday morning ensures you meet those obligations without relying on credit. You gain the freedom to make real-time decisions on stock levels and marketing spend based on the cash you actually have, rather than what you’re waiting for.

Managing Seasonal Peaks with Confidence

Retail and hospitality businesses know the pressure of a busy weekend or a bank holiday. Next day settlement allows you to restock your inventory by Monday afternoon, ready for the week ahead. You effectively close the funding gap that typically occurs during major UK sales events. This agility ensures you never miss a sale due to low stock levels. Learn how a business cash advance can further support your seasonal growth if you require a larger capital injection for a planned expansion.

Streamlining Your Bookkeeping

Reconciliation should be a simple task, not a daily chore. With next day settlement payment processing, your bank statement finally matches your card machine’s daily Z-report. This clarity reduces the time your accountant spends on unreconciled transactions. It also makes your financial reporting more accurate. Modern, integrated EPOS Systems are designed to track these fast-moving funds automatically. They provide a clear, real-time view of your financial health that traditional, slower systems simply cannot match. If you’re ready to take control of your revenue, you can explore our EPOS systems to see how they integrate with your funding cycle.

Securing Next Day Settlement with PurePay Hub

PurePay Hub is built on a foundation of transparency and honesty. We reject the opaque practices of traditional banks that treat fast funding as a luxury. Our commitment to next day settlement payment processing is standard for every UK merchant we partner with. We believe you should access your revenue without paying “express” fees or navigating complex markups. Our indicative rates are designed to be fair; typically sitting within the 0.3% range for debit cards and 0.5% for credit cards. This no-nonsense approach ensures your hard-earned capital stays where it belongs: in your business.

We organise our onboarding process to move at the speed of your business. We understand that every day spent waiting for a merchant ID is a day of restricted cash flow. Our team acts as a supportive ally, guiding you through the technical setup with clarity and discipline. We don’t use corporate jargon to hide costs. Instead, we provide a clean, dependable service that turns your payment processing into a stabilizing force for your finances. You deserve a partner that values efficiency as much as you do.

Hardware Options for Fast Funding

Every piece of hardware we provide is fully compatible with our rapid settlement cycle. Our Countertop Card Machine is the perfect anchor for retail stores, whilst our Portable Card Machine allows hospitality staff to take payments at the table. If you’re a service-based business or a mobile trader, our Mobile Card Machine ensures you get paid securely whilst on the move. We also provide a Virtual Terminal and Online Payment Gateway for those taking payments over the phone or internet. Every transaction, whether face-to-face or digital, is processed with the same commitment to 24-hour settlement.

How to Switch and Start Receiving Funds Faster

Transitioning from a legacy provider to a modern system is simpler than you might think. We follow a logical 3-step process to get you started. First, we provide a transparent comparison against your current rates. Second, we help you navigate the process of leaving your old provider, including assistance with understanding any exit fees. Finally, we setup your new merchant ID and ship your hardware. We handle the technicalities so you can focus on your customers. Get a transparent quote and start your next-day settlement journey today. It’s time to stop waiting for your money and start growing your business with a partner you can trust.

Secure the Financial Stability Your Business Deserves

The traditional wait for card payments is an unnecessary burden on your working capital. By choosing a partner that prioritises speed and clarity, you ensure that Monday’s revenue is ready for reinvestment by Tuesday morning. This shift allows you to manage stock, pay staff, and negotiate with suppliers from a position of strength. You gain control over your liquidity without the stress of pending balances or stagnant funds.

Implementing next day settlement payment processing is a decisive step toward a more resilient business model. At PurePay Hub, we make this transition seamless. We provide next-day access to funds as standard and offer industry-leading debit rates starting from 0.3%. If you’re worried about the cost of moving, we provide assistance with hidden exit fees from your current provider. We believe in being a fair partner to every merchant we serve.

Stop letting legacy banking cycles hold back your growth. Switch to PurePay Hub for transparent rates and next-day settlement and start putting your revenue to work immediately. We are ready to help you build a faster, fairer future for your business.

Frequently Asked Questions

Does next day settlement work on weekends and bank holidays?

Next day settlement typically operates on a working day basis. This means that transactions processed on Friday, Saturday, and Sunday will usually arrive in your bank account on Monday morning. Bank holidays are not classed as working days; therefore, your funds will settle on the next available business day following the holiday period.

Are there extra fees for next day settlement compared to standard processing?

Many traditional banks still charge “premium” or “express” fees for faster funding, but modern providers often include this as a standard feature. At PurePay Hub, we believe next day settlement payment processing should be transparent and accessible without hidden markups. You should always check your merchant agreement for any daily service charges that some legacy processors still apply.

Do I need to change my business bank account to get next day funding?

You do not need to switch your existing business bank account to access faster settlement. Your payment processor will link your merchant ID directly to your current account using the UK’s Faster Payment System. This allows you to keep your primary banking relationship whilst benefiting from a significantly improved cash flow cycle.

Is there a limit on the transaction volume for next day settlement?

There is generally no specific limit on the volume of transactions that can be settled within 24 hours. However, extremely large or unusual spikes in your daily sales may occasionally trigger a standard security review by the acquiring bank. These reviews are a necessary part of fraud prevention and ensure the safety of your business revenue.

How do I reconcile next day settlements with my accounting software?

The simplest way to reconcile your accounts is to use a gross settlement model where the total sales on your Z-report match your bank deposit exactly. Most modern EPOS systems and accounting platforms can integrate directly with your merchant service. This automation allows you to track next day settlement payment processing within your software, reducing manual data entry and accounting errors.

What is the ‘cut-off time’ for transactions to be included in the next day’s payout?

The cut-off time is the specific hour when your daily transactions are batched for processing. Traditional high street banks often have early cut-off times around 4pm, which can delay your evening sales. Modern independent providers frequently offer much later windows, sometimes up to midnight, ensuring your full day of trading is included in the next morning’s payout.

Can I get next day settlement for online payments and virtual terminals?

Yes, next day settlement is available for transactions made through an Online Payment Gateway or Virtual Terminal. The speed of your funding is determined by your contract with the processor rather than the hardware you use. This ensures that your e-commerce and phone-based sales provide the same liquidity as your face-to-face card transactions.

What happens if a settlement is delayed or doesn’t arrive as expected?

If your funds don’t arrive as expected, you should first verify if there is a UK bank holiday or a scheduled maintenance window for the Faster Payment System. If the delay persists, contact your provider’s UK-based support team immediately. A reliable partner will offer transparent tracking and a direct line of communication to resolve any technical or security-related delays quickly.