Did you know that 65% of business owners mandated for the April 2026 Making Tax Digital rollout still haven’t registered? It’s a staggering figure that highlights how daunting HMRC requirements feel when you’re already busy running a company. Many merchants feel stuck between complex regulations and merchant services that hide true costs in fine print. Our mission is to teach them to move their tax and payment systems into a unified digital environment that prioritises clarity over confusion.

You likely agree that the stress of cash flow gaps during tax season is a distraction you don’t need. This guide promises to help you demystify tax management by implementing a system that organises your revenue automatically. We will explore the tools that provide a transparent view of every pound earned, from portable card machines to online payment gateways. By the end of this article, you’ll understand how to set aside tax effortlessly and maintain total peace of mind regarding PCI compliance.

Key Takeaways

- Shift your mindset by treating tax management as a proactive growth strategy rather than an annual administrative burden.

- Discover how to teach them to move their tax and revenue streams into automated digital buckets to protect your profit margins.

- Learn to spot hidden fees in traditional merchant services that complicate your accounting and drain your business capital.

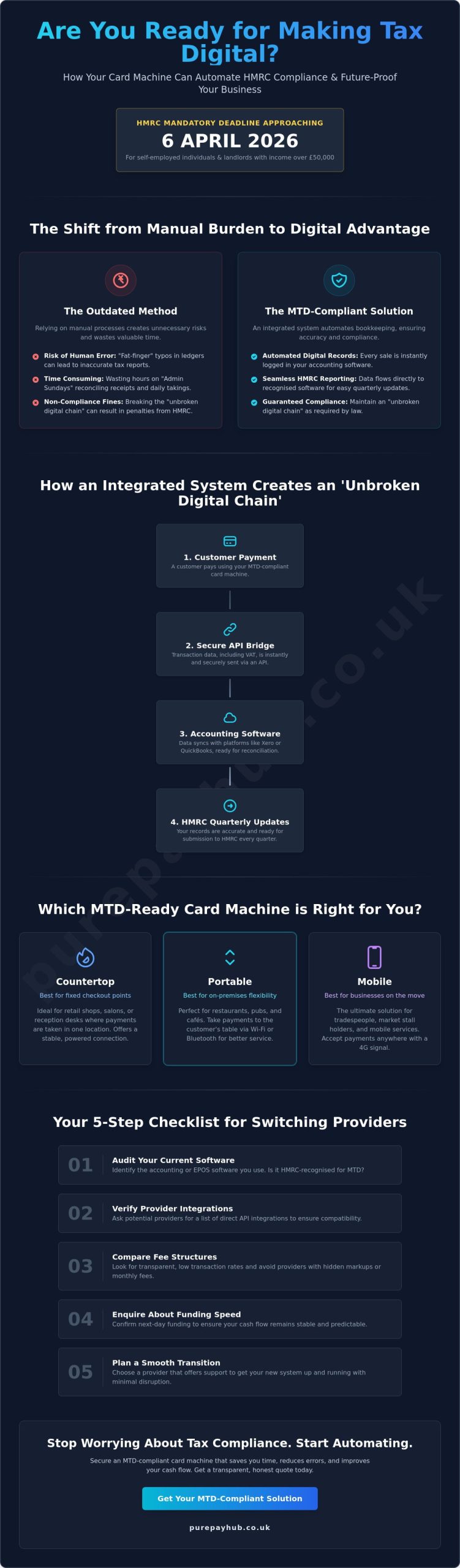

- Utilise integrated systems like a countertop card machine to capture precise data for effortless HMRC compliance.

- Maximise your liquidity with next-day funding to ensure you always have a transparent view of your available tax reserves.

The Reality of Tax Education: Why Every Business Owner Needs a Strategy

Most UK business owners view tax as a reactive chore. It’s the seasonal headache that arrives with an HMRC envelope. True tax management is actually a proactive growth strategy. It isn’t just about compliance; it’s about maintaining a transparent view of your business health. When you treat tax as a fundamental part of your daily operations, you stop being a victim of deadlines and start becoming a master of your cash flow.

The UK national curriculum often fails to prepare merchants for the complexities of VAT and Corporation Tax. Most people enter the business world with very little financial education. This gap forces many into a cycle of confusion. We aim to teach them to move their tax and payment workflows into a digital environment where every penny is accounted for. Ignorance carries a heavy price tag. HMRC late payment interest rates reached 7.75% in mid-2026. These avoidable costs drain your capital and limit your ability to secure a Business Cash Advance when you need to scale.

Bridging the Knowledge Gap in Your Business

Transparency starts with your team. Every person handling a sale should understand the gross versus net reality of that transaction. It’s vital to encourage healthy financial behaviour amongst your staff. Clarity reduces the collective stress of HMRC deadlines. When everyone knows that a portion of every pound belongs to the taxman, the business operates with more discipline. We act as a supportive ally to help you simplify these complex structures and build a team that values financial integrity.

Moving Beyond Spreadsheets

Manual record-keeping is the favourite hiding place for hidden costs. Spreadsheets are prone to human error and often mask the true impact of merchant fees. The shift towards digital-first financial management in the UK is no longer optional. Modern e-commerce payment systems and smart EPOS systems now provide the centre for all your business data. When you teach them to move their tax and cash flow tracking to a modern system, you remove the guesswork from your quarterly updates. You gain a reliable, real-time view of what you actually owe, ensuring that your profit stays in your pocket.

Teach Them to Move Their Tax: How to Organise Your Revenue Streams

Managing revenue effectively requires a shift from seeing money in the bank as yours to seeing it as a collection of distinct obligations. You must establish a tax-first mindset. This means identifying the tax portion of every sale and moving it immediately. If you wait until the end of the quarter to calculate what’s owed, you’re playing a dangerous game with your liquidity. The goal is to teach them to move their tax and revenue into organised streams that reflect the true state of the business at any given moment. This ensures you never accidentally spend money that belongs to HMRC.

Categorising your revenue into operational, tax, and profit buckets is the only way to guarantee you stay solvent. When funds are lumped together, it’s easy to overspend on stock or overheads. By separating these streams, you protect your profit margins and ensure that your tax reserve remains untouched. This level of discipline turns a chaotic bank balance into a structured financial roadmap.

The 5-Step System for Moving Tax

- Step 1: Identify your effective tax rate. This includes VAT, which is currently 20% for most goods, and Corporation Tax. Check the latest UK business tax obligations to ensure your percentages are accurate.

- Step 2: Automate the transfer. Set up your banking or payment system to move a fixed percentage of daily takings into a dedicated tax account.

- Step 3: Use integrated POS data. Your EPOS systems should track these liabilities in real-time. This eliminates the need for manual calculations at midnight before a deadline.

- Step 4: Categorise your streams. Split every pound into operational costs, tax reserves, and actual profit.

- Step 5: Review weekly. Compare your organised funds against your real-time liability to ensure they match exactly.

Creating a Culture of Financial Transparency

Accurate transaction logging isn’t just a task for the accountants; it’s a vital duty for every member of staff. You need to explain the cost of doing business to your employees so they understand why precision matters. If a staff member fails to log a refund or a specific tax-exempt sale correctly, it creates a ripple effect that complicates your final return. Use simple, punchy reports to show the health of the company. When the team sees that the business is disciplined, they’re more likely to follow suit. Honest financial behaviour starts at the top. If you’re transparent about the company’s obligations, your team will respect the systems you’ve put in place. By using a centralised platform like PurePay Hub, you can share these insights easily without getting bogged down in jargon.

Common Misconceptions: Why Tax Management Doesn’t Have to be Opaque

Many merchants believe they need an ACA qualification to understand their own cash flow. This is a common myth that keeps business owners in a state of financial anxiety. You don’t need a professional degree to see where your money goes. The goal is to teach them to move their tax and payment tracking into a system that uses plain English instead of technical jargon. When you understand your data, you regain control of your business destiny.

Hidden markups in financial services are another significant hurdle. Traditional merchant services often promise the “lowest rates” but hide complex fee structures in the fine print. These opaque practices make accounting much harder than it needs to be. A headline rate of 0.5% might look attractive until you see the added costs for “premium” cards or “minimum monthly service” fees. These layers of complexity create confusion when you try to calculate your true profit. There is a vital difference between your total turnover and your actual profit after the HMRC slice. Clarity here is the difference between a thriving business and a cash flow crisis.

Simplifying the Jargon

Financial terminology often feels like a barrier to entry. BACS (Bankers’ Automated Clearing System) is simply a way to send money between bank accounts over three days. CHAPS (Clearing House Automated Payment System) does the same thing but faster and for a higher cost. Your Merchant Service Charge (MSC) is the total fee you pay for every card transaction. Using no-nonsense terminology is your best friend during tax season. If you can’t explain a charge on your statement, it shouldn’t be there. Spotting opaque practices starts with demanding a clear breakdown of every penny you spend on processing.

The Truth About PCI Compliance

PCI compliance is often viewed as a frustrating tick-box exercise. In reality, it’s a critical security standard that protects your revenue from fraud. Non-compliance fines are avoidable costs that drain your tax bucket and damage your reputation. By using secure, modern hardware like a countertop card machine or an integrated EPOS system, you ensure your data remains protected. We teach them to move their tax and payment processing to platforms that prioritise security. This proactive approach keeps your funds safe and ensures you aren’t wasting capital on penalties that could have been avoided with better equipment.

Managing your obligations becomes much simpler when you have a direct line of sight to your liabilities. You should regularly check your HMRC business tax account to stay updated on your current standing. Combining this government data with your real-time payment reports provides the ultimate shield against financial surprises at the end of the year.

Integrating Your Payment Systems with Your Tax Obligations

Your countertop card machine is more than a tool for accepting payments. It serves as your primary data source for tax. Every transaction logged through a modern terminal creates a digital audit trail that HMRC values. This level of precision is the cornerstone of a successful financial strategy. We teach them to move their tax and revenue tracking away from manual entry and into these automated hardware solutions. It ensures that every pound is accounted for from the moment a customer taps their card.

Next-day funding is a game-changer for maintaining an organised tax reserve. Traditional merchant services often hold your money for several days. This delay creates a gap in your cash flow that makes it difficult to see your true liability. With faster access to your funds, you can move the tax portion of your sales into your dedicated account immediately. For hospitality businesses, integrated EPOS systems are the favourite tool for staying tax-efficient. They sync sales data directly with accounting software, making the quarterly update process much smoother.

Seamless Data Flow from Till to Tax Return

Digital receipts and transaction logs significantly reduce manual errors. When your payment gateway and POS system talk to each other, you eliminate the risk of missing a sale or miscalculating VAT. Having a single hub for all card payment types, including online sales via Payment Links or a Virtual Terminal, keeps your records tidy. Real-time reporting is no longer a luxury. It’s a necessity for Making Tax Digital (MTD). With the April 2026 deadline approaching for those with qualifying income over £50,000, having your data ready is vital. You can explore integrated payment solutions that simplify this transition today.

Leveraging Business Cash Advances Responsibly

Seasonal dips can make tax deadlines feel overwhelming. A Business Cash Advance based on your card sales can help you manage these gaps without the stress of traditional debt. Unlike a bank loan with fixed monthly payments, this advancement is repaid as a small percentage of your future card sales. This means if you have a slow month, your repayments reduce automatically. It’s a flexible way to keep your finances organised whilst ensuring you have the liquidity to meet your HMRC obligations on time. This approach keeps your business moving forward without the rigid pressure of a standard financial institution.

PurePay Hub: Simplifying Financial Clarity for UK Merchants

PurePay Hub stands as a transparent partner for UK business owners who are tired of the opaque practices of traditional banks. We believe that financial processing should be a stabilising force for your company, not a source of confusion. By offering debit card rates starting at 0.3%, we ensure you maximise your profit margins on every transaction. This isn’t just about saving money on fees. It’s about having more capital available to meet your tax obligations without the usual stress. Our no-nonsense approach prioritises your business growth over corporate markups.

The road to the April 2026 Making Tax Digital rollout requires a reliable, integrated system. We teach them to move their tax and payment data into a centralised environment that is fully ready for these new HMRC regulations. Our onboarding process is designed to be swift and clear. We get you set up with the right hardware, such as a portable card machine or an online payment gateway, without the corporate jargon that usually complicates switching providers. With next-day access to your funds, you can move your tax reserves into their dedicated accounts faster than ever before.

Our Commitment to Transparency

Trust is built on honesty and clarity. We avoid the hidden markups and confusing fee structures that make manual accounting a nightmare for regional merchants. Your monthly hardware rental fees for a countertop card machine or mobile unit are clearly structured and easy to understand from day one. Having a reliable, local expert in your corner means you can focus on your customers whilst we handle the technicalities of your transaction data. We act as a supportive ally, ensuring your financial behaviour remains disciplined and your records stay untainted by unexpected costs or service charges.

Get Started with a Fairer Payment Solution

Switching providers doesn’t have to be a stressful experience for your team. Our specialists manage the transition to ensure your business continues to process sales smoothly without any downtime. Fairer rates have a significant impact on your long-term tax planning and overall business development. When you aren’t overpaying for every tap and swipe, your cash flow becomes more predictable and easier to manage. This predictability is the foundation of a healthy, sustainable business. You can organise your business payments with PurePay Hub and start building a more transparent financial future today.

Secure Your Financial Future Today

Moving your tax and payment systems online is more than a compliance requirement; it’s a step toward total business clarity. You’ve seen how a proactive strategy replaces reactive stress. By categorising revenue streams and using integrated data from your card machines, you ensure that HMRC deadlines never cause a cash flow crisis. We want to teach them to move their tax and financial records into a space where every pound is visible and every fee is fair.

PurePay Hub is here to act as your supportive ally. We provide a no-nonsense service with debit card charges starting from 0.3% and next-day access to your funds. You won’t find any hidden markups or corporate jargon in our agreements. It’s time to stop overpaying for processing and start focusing on your growth.

Discover fairer card machine rates with PurePay Hub and take control of your business health. You have the tools to build a more transparent, disciplined company. We’re ready to help you make it happen.

Frequently Asked Questions

How can I teach my staff to move their tax mindset toward profitability?

Start by explaining that every sale includes a portion that belongs to HMRC. When your team understands the “gross versus net” reality of a transaction, they become more accurate with transaction logging. Transparency about the company’s obligations builds a disciplined team that values financial health over simple turnover figures.

What is the best way to organise business finances for a sole trader in the UK?

Use a dedicated business account and separate your revenue the moment it hits your bank. Categorise your funds into three distinct buckets: operational costs, tax reserves, and actual profit. Automated systems that track your income in real-time are far more reliable than manual spreadsheets for maintaining a clear view of your available capital.

Can a card machine help me with my Making Tax Digital (MTD) obligations?

Yes, a modern card machine serves as a primary data source for MTD by creating a secure digital audit trail for every sale. We teach them to move their tax and payment records into integrated systems that sync directly with accounting software. This ensures your quarterly updates to HMRC are based on precise, real-time transaction data rather than guesswork.

Why is next-day funding important for managing my tax reserves?

Faster access to your cash allows you to move the tax portion of your sales into a separate account immediately. Traditional merchant services often hold funds for several days, which creates confusing cash flow gaps. Next-day funding ensures your tax reserves are always up to date and reflective of your true, current liability.

Is it better to use a separate bank account for VAT and Corporation Tax?

Yes, using a separate account for your tax liabilities is a highly effective way to prevent accidental overspending on stock or overheads. It provides a physical barrier between your operational cash and the money you owe the government. This simple structure ensures you always have the liquidity to meet your deadlines without financial stress.

How do high transaction fees impact my ability to save for tax?

High fees and hidden markups directly drain your profit margins, leaving less capital available for your tax bucket. When you use a provider with fair, transparent rates, you keep more of every pound you earn. This extra margin makes it much easier to build a robust tax reserve whilst maintaining a healthy, growing business.

What are the common hidden costs in merchant services that complicate tax prep?

Many providers hide costs like “minimum monthly service fees” or “PCI non-compliance penalties” deep within their fine print. These unexpected charges create discrepancies in your accounts and make tax reconciliation much more difficult. Choosing a partner with transparent pricing ensures your financial records remain clear and easy for your accountant to process.

How does a business cash advance affect my tax liability?

A Business Cash Advance is an advancement against future card sales rather than a traditional loan, so it doesn’t typically increase your tax liability. However, you should always consult your accountant regarding the specific reporting of these funds. We teach them to move their tax and cash flow management toward these flexible solutions to handle seasonal dips without the rigid pressure of bank debt.