The cheapest monthly rental price on your screen today might actually be the most expensive mistake your business makes this year. Many UK merchants sign contracts believing they’ve secured a bargain, only to discover that card machine lease agreement pitfalls are hidden deep within the small print. You likely feel frustrated by unexpected monthly fees or the realisation that you can’t cancel without facing a massive penalty. It’s a common experience in an industry that often thrives on complexity and opaque terms.

We believe you deserve a partner, not a distant financial institution. This guide will help you identify red-flag clauses, understand the true total cost of ownership, and avoid predatory fees that drain your hard-earned margins. We’ll break down the jargon so you can secure a fair deal for your payment hardware. We’re going to explore how to spot transparent alternatives that prioritise your business growth over restrictive contracts.

Key Takeaways

- Identify the most common card machine lease agreement pitfalls, including auto-renewal traps that can double your contract length without warning.

- Learn how to calculate the total cost of ownership to avoid paying for hardware that becomes obsolete before your lease ends.

- Master a two-step review process to locate hidden “Evergreen” clauses and non-standard fees in any merchant service contract.

- Understand why the lure of low upfront costs often leads to higher long-term expenses through hidden minimum monthly charges.

- Discover how a transparent partner provides next-day funding and clear rates whilst avoiding the industry’s usual jargon.

The Reality of Card Machine Lease Agreements in the UK

Signing a contract for a new payment terminal often feels like a quick win for a busy business owner. You need to accept card payments; the provider offers a sleek machine for a small monthly fee. It seems straightforward. However, this simplicity is often a facade. Most UK merchants aren’t just renting a piece of kit. They are entering a rigid financial commitment that can last for years. This initial lack of clarity is exactly how many card machine lease agreement pitfalls begin to take root.

The “Low Upfront Cost” lure is particularly effective at blindsiding entrepreneurs. When you’re managing staff, stock, and daily operations, a low entry price looks like a smart way to protect your cash flow. It’s a calculated tactic used by many traditional providers. They lead with the hardware price whilst burying the long-term cost in the fine print. At PurePay Hub, we believe your payment hardware should be a tool for growth. It should never be a weight that stifles your business with hidden markups or restrictive terms.

Why Leases are Common Amongst UK SMEs

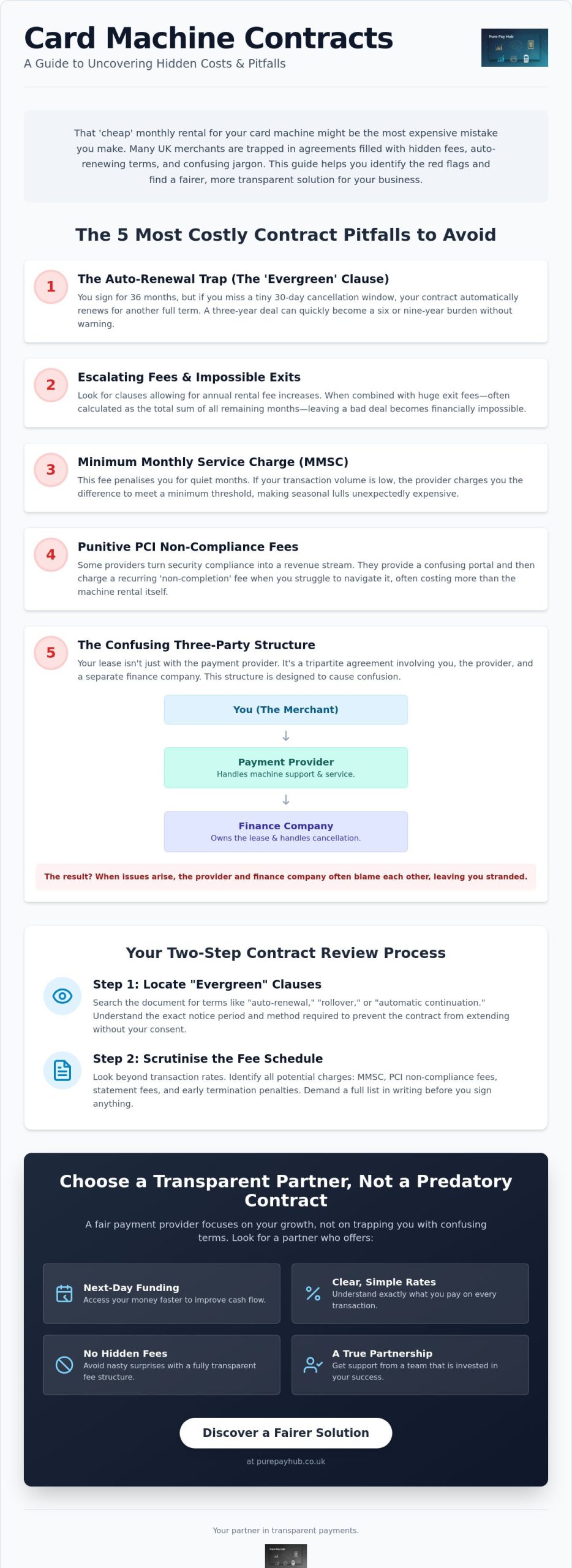

Leasing is a frequent choice because it allows businesses to access the latest countertop or portable technology without a large capital outlay. This helps you keep your funds available for more urgent needs, such as seasonal stock or payroll. Independent Sales Organisations (ISOs) usually facilitate these deals. They act as a bridge between the merchant and the technology. Whilst a 36-month term is often sold as the “standard” industry duration, the reality is that these contracts can be incredibly difficult to exit if your business model evolves or if you find a better service elsewhere.

The Three Parties Involved in Your Contract

One of the most confusing aspects of these agreements is that they involve more than two people. A lease is a tripartite agreement involving the merchant, the payment provider, and a third-party finance company. This structure is the root cause of many support and cancellation frustrations. If the machine breaks, you call the provider. If you want to cancel the contract, you have to deal with the finance house. This separation often leads to a cycle of finger-pointing that leaves the business owner stranded. Understanding that you are essentially taking out a loan to pay for the equipment is the first step toward avoiding common card machine lease agreement pitfalls.

The 5 Most Costly Pitfalls in Merchant Service Contracts

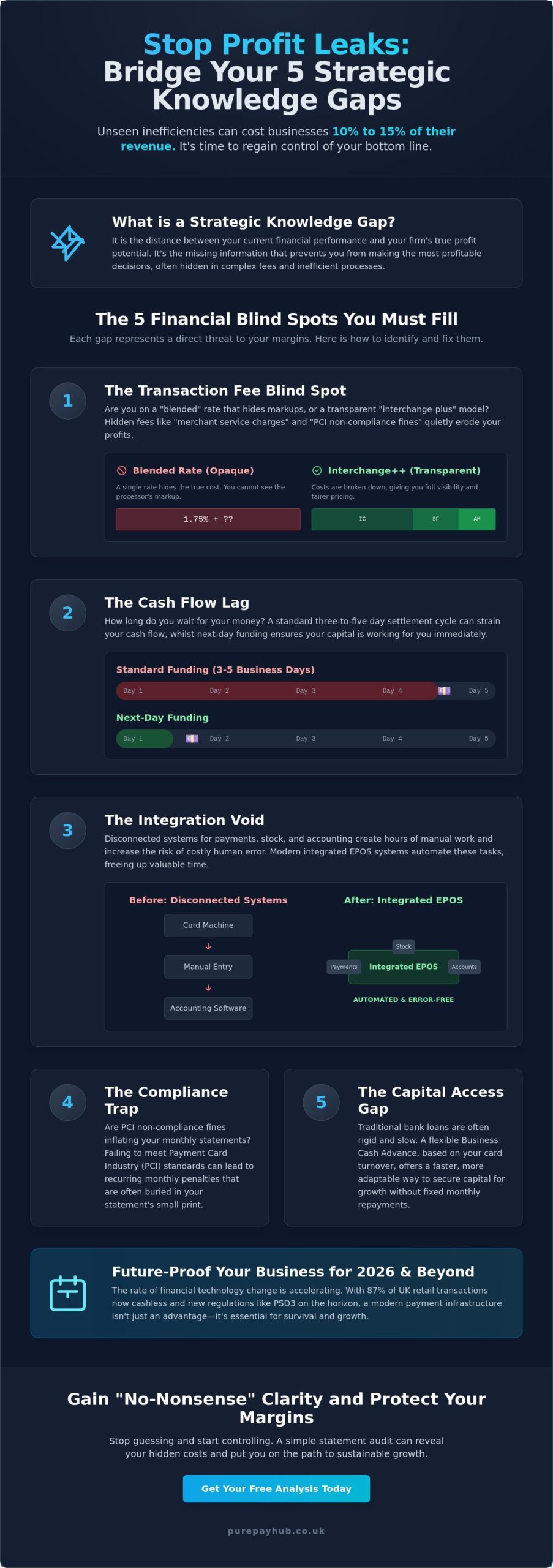

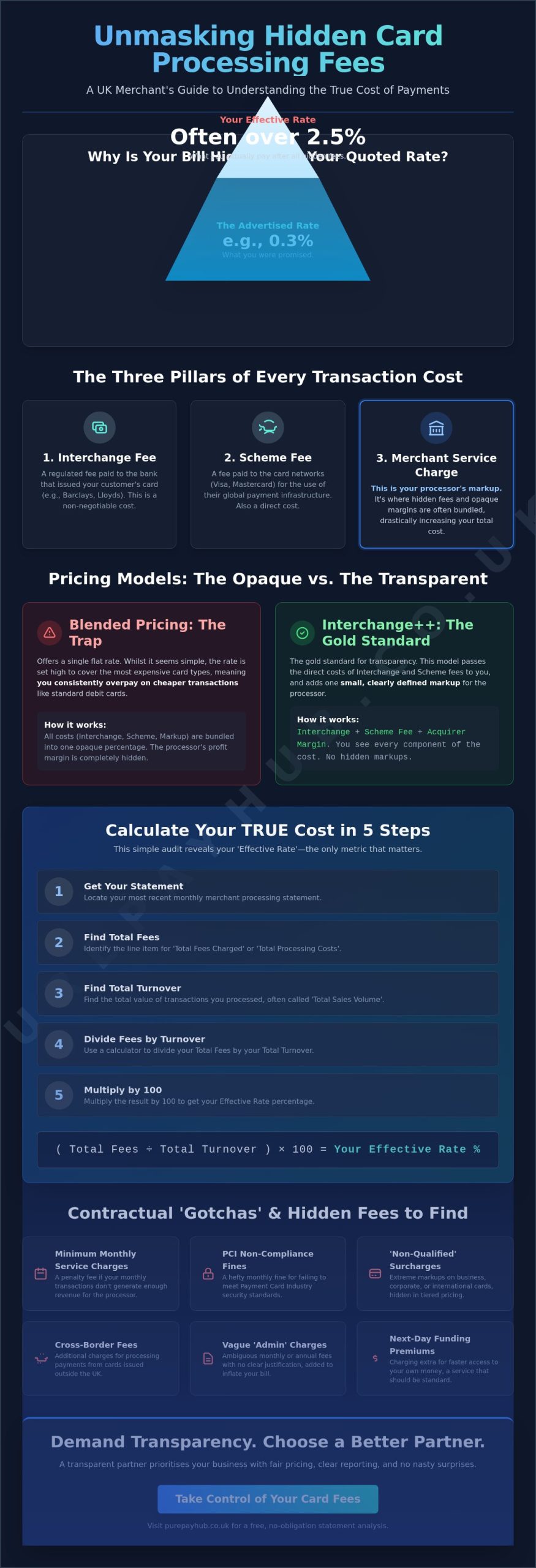

Contractual fine print is where many businesses lose their hard-earned profit. One of the most aggressive card machine lease agreement pitfalls is the ‘Auto-Renewal’ trap. You might sign what you believe is a 36-month deal, but if you don’t cancel within a specific 30-day window, the contract often rolls over for another full term. It’s a predatory cycle that can turn a short-term commitment into a decade-long burden. Many merchants only realise they are trapped when they try to switch providers, only to be told they missed their notice window by a single day.

Additionally, keep a sharp eye out for clauses that allow for annual rental fee increases. These escalating fees often fly under the radar during the initial sales pitch. When combined with exit fees, which are often calculated as the total sum of all remaining months in the lease, leaving a bad deal becomes financially impossible. Aligning your contract with the Crown Commercial Service guidance on merchant services can help you understand the standard components you should expect, rather than these hidden extras. These hidden costs are why understanding card machine lease agreement pitfalls is vital before you put pen to paper.

The Minimum Monthly Service Charge (MMSC) Explained

The MMSC is a common fee that catches seasonal businesses off guard. It sets a minimum floor for transaction fees. If your monthly card volume is low and your processing fees don’t reach this threshold, the provider charges you the difference. This essentially penalises you for having a quiet month or taking a holiday. For a small gift shop or a seaside cafe, this can make winter months significantly more expensive than they need to be. When reviewing new agreements, try to negotiate a zero-MMSC term to ensure you only pay for what you actually use.

PCI DSS Compliance and Non-Completion Fees

Every UK business must be PCI compliant to protect customer data. However, some providers treat this as a recurring revenue stream rather than a security measure. They might provide a complex, confusing portal for compliance and then charge a monthly ‘non-completion’ fee when you struggle to navigate it. These fees can quickly add up, often costing more than the actual rental of the machine. We take a different approach at PurePay Hub, providing proactive support to ensure you stay compliant without the stress of recurring fines. We believe in building partnerships based on clarity, not penalties.

Calculating Total Cost of Ownership: Lease vs. Buy vs. Rental

Choosing how to acquire your payment hardware is a balancing act between upfront capital and long-term commitment. Whilst the initial price tag is important, the true cost of ownership includes transaction rates, monthly subscriptions, and the eventual cost of replacement. Many business owners overlook the reality that card machines are essentially specialised computers. Like any computer, they require regular updates and eventually become obsolete. This is where many card machine lease agreement pitfalls become painfully clear; you might find yourself paying for a device that is technically out of date long before the contract ends.

A typical lease might look attractive because it spreads the cost of high-end hardware over several years. However, this often locks you into transaction rates that are higher than the market average. When you add up the monthly lease payments and the inflated processing fees, the total cost often far exceeds the value of the machine. At PurePay Hub, we advocate for a middle ground that provides the latest technology without the predatory strings of a traditional finance deal.

The Hidden Costs of Owning Your Hardware

Buying a machine outright is often marketed as the ultimate way to save money. It’s true that you avoid monthly rental fees, but you also take on all the risk. If a countertop machine fails on a busy Saturday morning, you don’t have a ‘swap-out’ service to rely on. You have to buy a new one and wait for delivery, losing sales in the meantime. Additionally, security standards like P2PE and NFC evolve rapidly. A machine purchased today might not support the security requirements or payment methods of 2029. Without a managed service, you’re responsible for every repair and every firmware update, which can lead to your hardware becoming an expensive paperweight.

The Rental Alternative: Flexibility and Support

Our rental model is designed to offer the stability of a managed service with the flexibility that modern businesses need. We provide clear monthly costs that include ongoing technical support and hardware maintenance. This means if your portable card machine develops a fault, we handle the resolution so you can focus on your customers. Having your hardware and merchant account managed under one roof simplifies your operations and removes the friction often found in tripartite leases. We also provide next-day access to funds, ensuring your cash flow remains as healthy as your technology. It’s a transparent approach that avoids common card machine lease agreement pitfalls by putting your business needs first.

How to Review a Card Machine Contract Before Signing

Reviewing a contract is your final line of defence. Do not rely on verbal promises from a sales representative. Instead, conduct a systematic audit of the physical or digital document. The first step is to locate the ‘Term and Termination’ clause. Look specifically for ‘Rolling’ or ‘Evergreen’ language. These terms often indicate that your contract will renew automatically for another full term unless you cancel within a tiny, specific window. This is a classic example of card machine lease agreement pitfalls that catch busy merchants off guard.

Next, scrutinise the ‘Schedule of Fees’. Sales pitches often focus on the headline transaction rate whilst ignoring authorisation and statement fees. These small charges add pennies to every transaction; they can significantly impact your monthly margins. Demand a written confirmation of the total monthly cost, including every ‘extra’ service like premium support or reporting tools. Finally, check the notice period. A 30-day notice period is fair and standard. If you see a 12-month notice requirement, treat it as a massive red flag and consider looking elsewhere.

Red Flag Phrases to Spot in the Fine Print

Keep an eye out for ‘Liquidated Damages’. This legal phrase means you might be liable for the full remaining value of the contract if you try to leave early. You should also watch for ‘Variation of Terms’ clauses. These allow providers to increase your rates without your consent whilst keeping you locked into the agreement. It’s also vital to verify if the contract is an ‘exclusive’ or ‘non-exclusive’ agreement. An exclusive deal prevents you from using any other provider, even if your current service fails or becomes too expensive.

Questions to Ask Your Sales Representative

Before you sign, ask direct questions and ensure the answers match the written contract. Does the provider charge a ‘restocking fee’ if you return the equipment? Are your rates ‘blended’ or based on ‘Interchange Plus Plus’? Blended rates are simpler but often more expensive for larger businesses. Finally, ask what happens if your business closes or is sold. A fair partner will have a clear, reasonable exit strategy that doesn’t involve bankrupting you. If you want a contract that values transparency over traps, request a clear quote from PurePay Hub today. We provide straightforward terms designed to support your business, not trap it.

Choosing a Transparent Payment Partner for Your Business

Finding a partner that values your success is the best way to move past the frustration of traditional banking. At PurePay Hub, we prioritise a no-nonsense approach to merchant services. We don’t believe in hiding behind complex jargon or confusing fee structures. Instead, we offer competitive debit rates starting at 0.3% and provide next-day funding as standard. This ensures your capital stays in your business where it can do the most good. By moving away from the common card machine lease agreement pitfalls, you can establish a foundation for long-term growth and stability.

Our integrated EPOS systems are designed to do more than just process payments. They help you organise your business behaviour by providing clear insights into your sales patterns and inventory levels. This level of efficiency is often missing from basic lease deals that only provide the hardware without the supporting ecosystem. We provide the tools you need to run a modern, data-driven business whilst keeping your costs transparent and predictable. We believe a partnership should be built on trust; not restrictive small print.

The PurePay Hub Difference: Calm Advocacy

We act as a supportive ally for regional business owners in a market that is often crowded and confusing. Our commitment to honesty and integrity means we won’t trap you in a deal that doesn’t fit your needs. If you’re currently stuck in a restrictive contract, we can help you switch providers whilst navigating the common exit fee traps that traditional finance houses use. We also understand that growth sometimes requires a capital boost. Our business cash advance offering supports your cash flow without the burden of fixed monthly interest, allowing you to repay as you earn. It is a flexible solution for a modern economy.

Next Steps: Getting a Fair Quote

Securing a better deal starts with a clear understanding of your current costs. To prepare for an honest comparison, gather your most recent merchant statements. We will help you look past the headline rates to see the true total cost of ownership. Onboarding with a partner that values clarity over jargon is a straightforward process. We handle the technicalities so you can focus on serving your customers. Get a transparent quote from PurePay Hub today and experience a partnership built on trust and reliability. We are here to help you avoid card machine lease agreement pitfalls for good.

Take Control of Your Payment Hardware

You now have the tools to navigate the complex world of merchant services with confidence. By identifying auto-renewal traps and scrutinising the fine print for hidden charges, you’ve already taken the most important step toward protecting your margins. Avoiding card machine lease agreement pitfalls isn’t just about saving money; it’s about ensuring your business remains agile and unburdened by restrictive, long-term debt. Your hardware should be a catalyst for growth, not a source of constant frustration.

We believe that fairness should be the industry standard. That’s why we offer a transparent alternative that puts your needs first. With debit card rates from 0.3%, next-day access to your funds, and a complete absence of opaque fee structures, we provide a stabilising force for your finances. You don’t have to settle for a contract that feels like a trap. Switch to a fairer deal with PurePay Hub and experience the difference of a partnership built on integrity. Your business deserves a partner that works as hard as you do.

Frequently Asked Questions

How do I get out of a card machine lease agreement early?

Terminating a lease early usually requires paying a settlement figure, which often equals the total sum of all remaining monthly payments. You must check your contract for a specific ‘buy-out’ clause or cancellation fee. Always provide your written notice within the required window, typically 30 days before the contract is due to renew. If you are struggling with a restrictive deal, some transparent providers can help you navigate the exit process safely.

What is the standard length for a card machine contract in the UK?

Card machine contracts in the UK are typically 12 to 18 months in length. However, some providers may offer longer terms of up to 36 or 48 months to lower the headline monthly rental cost. Whilst a longer deal might seem attractive for your cash flow, it increases the risk of being stuck with obsolete hardware. Always confirm the initial term and the notice period required to prevent an automatic rollover.

Are there hidden fees in every card machine lease?

Not all agreements contain hidden fees, but many traditional contracts include non-standard charges that aren’t highlighted during the sales process. You should look for authorisation fees, statement fees, and minimum monthly service charges (MMSC). These are common card machine lease agreement pitfalls that can quietly drain your profits. Choosing a partner that values clear, honest pricing is the best way to avoid these unexpected costs and protect your margins.

Can I switch card machine providers if I am still in a lease?

Yes, you can switch your payment processing to a new provider whilst still being tied to a hardware lease. Since the lease is often a separate tripartite agreement with a finance house, it doesn’t always end when you move your merchant account. You can continue to pay the monthly rental for your existing equipment whilst benefiting from the fairer transaction rates and better service of a new, transparent payment partner.

What happens to the card machine if my business closes?

Closing your business doesn’t usually terminate the financial obligation of a lease. Most finance companies expect the remaining balance of the contract to be paid in full as a ‘liquidated damages’ settlement. It’s vital to check if you signed a personal guarantee, as this could make you personally responsible for the debt even if your limited company is dissolved. Always discuss your situation with your provider to see if they offer any flexibility.

Is it better to lease or buy a card machine for a new small business?

Buying a machine outright for £20 to £180 is often best for very small businesses with lower transaction volumes. However, leasing or renting becomes more beneficial for businesses with a monthly turnover above £8,000, as it provides access to lower transaction rates and included technical support. Renting offers a flexible middle ground, giving you the security of a managed service without the long-term debt of a traditional lease agreement.

Why is my merchant statement higher than the agreed transaction rate?

Your statement total is often inflated by authorisation fees, PCI non-compliance penalties, or higher rates for international and business cards. Domestic interchange fee caps of 0.2% for debit and 0.3% for credit only apply to UK-issued consumer cards. If you process many cross-border transactions, your costs will naturally be higher. Reviewing each line item helps you identify where hidden markups might be affecting your final bill every month.

What is a non-compliance fee and why am I being charged it?

A non-compliance fee is a penalty for not completing your annual PCI DSS security assessment. Every UK merchant must prove they handle card data securely to protect their customers. Some providers make this process confusing and then profit from the resulting fines. We take a different approach, providing proactive support to help you stay compliant. This ensures your business is secure whilst avoiding the stress of recurring, unnecessary penalties.