Did you know that 46% of UK businesses operate without a formal marketing strategy? It is a startling figure from April 2026 that explains why so many owners feel they are shouting into a void. The Gap: Small businesses think marketing is just social media posts and expensive adverts, but this narrow view often leads to wasted budgets and empty results. You might feel overwhelmed by the constant noise or frustrated when your latest campaign fails to deliver a return.

We understand that you want clarity rather than corporate jargon. Marketing should not feel like a gamble or a distraction from your core work. This article shows you how to move beyond simple shouting to build a system that actually grows your business. You will learn how to clarify the difference between your brand and your operations whilst discovering practical ways to keep your existing customers coming back. We will also explore how smarter payment processes can improve your cash flow and simplify your daily tasks.

Key Takeaways

- Understand why The Gap: Small businesses think marketing is just … social media and adverts is preventing many UK firms from reaching their full potential.

- Move away from “gut feeling” tactics and learn how to organise a promotional budget that relies on clear, actionable data.

- Recognise the checkout as a vital marketing touchpoint where professional card machines protect your hard-earned reputation.

- Learn a practical five-step process to audit your customer journey from the first interaction to the final payment.

- Discover how transparent payment structures and modern EPOS systems can protect your margins whilst improving your business image.

What is the Marketing Gap for Small Businesses?

Many UK business owners feel they are running on a treadmill. They post daily on LinkedIn and pay for digital adverts, yet the phone doesn’t ring as often as it should. This frustration usually stems from a fundamental misunderstanding of how growth works. The Gap: Small businesses think marketing is just about getting seen, but visibility is worthless without a seamless experience to back it up. If your social media looks professional but your service feels chaotic, you’ve created a disconnect that drives customers away.

We define the marketing gap as the failure to align business operations with customer expectations. It’s the space between the promise you make in an advert and the reality a customer faces when they try to buy from you. In the past, business growth relied on “outbound” shouting. You bought a billboard or a radio slot and hoped for the best. Today, the focus has shifted to “inbound” trust-building. Customers in 2026 are more informed than ever. They’ve likely used AI tools to research your industry before they even click your link. If your operations don’t match your promises, they’ll leave immediately.

The “Just Promotion” Trap

Social media is often the first place owners turn, but it usually represents only 10% of a healthy marketing mix. This is a common trap. Shouting for attention on TikTok doesn’t help if your internal processes are weak. You end up chasing new leads whilst your existing customer base feels forgotten. This “shouting” without a foundation leads to a wasted budget and high frustration. It’s much harder to win a new customer than it is to keep an old one, yet many SMEs ignore their current fans in favour of the next “viral” post.

Marketing vs. Advertising: Knowing the Difference

It is vital to distinguish between these two terms to avoid wasting money. Advertising is a specific tool you use to reach people, whereas marketing is the overarching strategy. To truly understand What is Marketing?, you must look at the entire journey from discovery to the final payment. Advertising gets them to the door; marketing ensures they want to walk through it and come back again.

In a 2026 context, the traditional 4 Ps have evolved. Your “Product” now includes the ease of your digital service. Your “Promotion” must be supported by “Place” (your digital presence) and “Price” (your financial transparency). If these elements don’t work together, your advertising spend is simply subsidising your competitors’ growth. You educate the customer, but they buy from the person who offers the smoother experience.

Why Most UK SMEs are “Marketing in the Dark”

Operating a business on “gut feeling” is a tradition for many UK entrepreneurs. Whilst intuition is valuable for spotting opportunities, it is a dangerous way to organise your promotional budget. In 2026, British small businesses face significant pressure from rising inflation and energy costs. You cannot afford to guess where your next customer is coming from. Precision is no longer a luxury; it is a survival requirement. When every pound counts, “random acts of marketing”—like a one-off advert or a sporadic social media post—simply drain your cash flow without providing a clear return.

The Gap: Small businesses think marketing is just about following trends or copying what the shop next door is doing. This lack of data-driven decision-making keeps many owners in the dark. Without a documented roadmap, you’re essentially throwing darts at a board in a pitch-black room. You might hit the target eventually, but you’ll waste a lot of resources in the process. Understanding the specific Small Business Marketing Challenges of the current year is the first step toward switching on the lights.

The Missing Roadmap

As of April 2026, 46% of UK businesses operate without a formal marketing strategy. This lack of planning is why many fail to scale. You don’t need a 50-page document or a complex agency retainer to succeed. A simple one-page strategy that outlines what you are doing, why you are doing it, and how you will measure success often outperforms a bloated corporate plan. Set SMART goals that relate directly to your bank balance. If a marketing activity doesn’t clearly lead to a sale or a lead, it shouldn’t be on your roadmap.

The Data Disconnect

Your best marketing tool is often sitting right on your counter. Your sales data holds the key to understanding customer behaviour. By looking at when and how people pay, you can identify your “favourite” customers—those who spend the most and return most frequently. You don’t need a degree in data science to track your ROI. Simple methods, such as checking your transparent payment solutions for sales peaks after a campaign, can tell you exactly what is working. Use these insights to double down on successful tactics and cut the ones that only add to the noise.

The Invisible Marketing: Why Payments Matter

Marketing is often viewed as a way to get people through the door. However, the experience doesn’t stop once a customer decides to buy. The checkout is the final “marketing” touchpoint of every transaction. If a customer has a great time in your shop but struggles at the till, that frustration is what they’ll remember. A slow or unreliable card machine doesn’t just delay a sale; it actively damages your brand reputation. The Gap: Small businesses think marketing is just what happens before the sale, but the payment process is where you prove your professionalism.

Checkout Speed as a Competitive Advantage

The “payment moment” is psychologically sensitive. Customers are handing over their hard-earned money, and any friction during this process creates anxiety. Long queues caused by clunky hardware can kill referrals and discourage repeat visits. By using integrated EPOS systems, you reduce waiting times and keep the customer’s mood positive. A seamless payment is a silent promise of professional service. It tells the customer that you value their time as much as their money. When you look at Local Marketing Strategies, efficiency at the point of sale is often the most underrated way to stand out from your competitors.

Trust and Transparency

Your choice of merchant services says a lot about your brand’s values. If your provider uses murky fee structures or hidden markups, it becomes harder for you to remain transparent with your own customers. Honesty is a powerful marketing tool. Being “easy to do business with” is a reputation that pays dividends for years. The Gap: Small businesses think marketing is just about the initial attraction, but the physical act of paying is where trust is truly solidified. This includes offering modern payment flexibility. Accepting Apple Pay and Google Pay isn’t just a technical requirement; it’s a way to build customer loyalty whilst meeting them where they are.

Modern hardware also allows you to extend your marketing beyond the transaction. Using your card machine to provide professional digital receipts or payment links creates a clean, high-tech impression. It shows you’re a forward-thinking business that respects modern standards. By removing the hidden costs of a poor payment experience, you bridge the gap between a one-time lead and a loyal advocate. You don’t need to shout for attention when your operations speak for themselves.

5 Steps to Close the Marketing Gap in 2026

Bridging the distance between effort and profit requires a disciplined approach. You don’t need a massive budget to start seeing results; you need a system. The Gap: Small businesses think marketing is just about finding new people to talk to, but true growth starts with the people who are already standing in front of you. By shifting your focus from shouting for attention to refining your internal processes, you can build a more resilient company.

Audit the Customer Journey

Start by walking in your customer’s shoes to find points of friction. Visit your own website on a mobile phone. Stand at your counter and time how long it takes to complete a transaction. These small moments are where you find “leaks” in your sales funnel. If a customer struggles to find information or waits too long to pay, they will likely drop off and head to a competitor. Fix these basic operational issues before spending a single penny on new adverts. A smooth journey is the most effective promotional tool you have.

For inspiration on seamless customer journeys, look at the luxury sector; when you explore Ocean Cruises with a specialist like The Russell Travel Team (Lightning Travel), every detail is managed to ensure the reality matches the high-end promise.

Focusing on Customer Lifetime Value (CLV)

It is five times cheaper to keep an existing customer than it is to find a new one. Your best marketing tool is a happy repeat buyer who refers their friends. Focus on increasing your CLV by making every interaction feel professional and effortless. If you need to scale up your stock levels to meet this demand, consider a Business Cash Advance to fund inventory that drives sales. By rewarding loyalty through seamless, integrated systems, you turn a one-time visitor into a long-term advocate for your brand.

Document your plan clearly. Write down what you are doing, why you are doing it, and how you will measure the result. This prevents “random acts of marketing” and ensures every decision relates to your bank balance. Optimise your operations by ensuring your hardware and software support your growth. High-quality EPOS Systems and reliable Card Machines make your business look larger and more established. Build your local authority through genuine partnership and professional reliability. When you are easy to do business with, your reputation grows naturally without the need for constant shouting.

If you are ready to professionalise your checkout and protect your margins, you can explore our transparent payment solutions today.

How PurePay Hub Bridges the Gap for UK SMEs

Operational friction is the silent killer of brand reputation. We have explored how a clunky checkout can undo hours of hard work spent on social media or advertising. PurePay Hub exists to remove that friction. We provide the professional hardware that makes small businesses look big. Whether you use a Countertop Card Machine for your permanent till or a Portable Card Machine for service on the move, our tools ensure a professional finish to every customer interaction. The Gap: Small businesses think marketing is just about the initial attraction, but we believe it is about the steady promise of a better, fairer service.

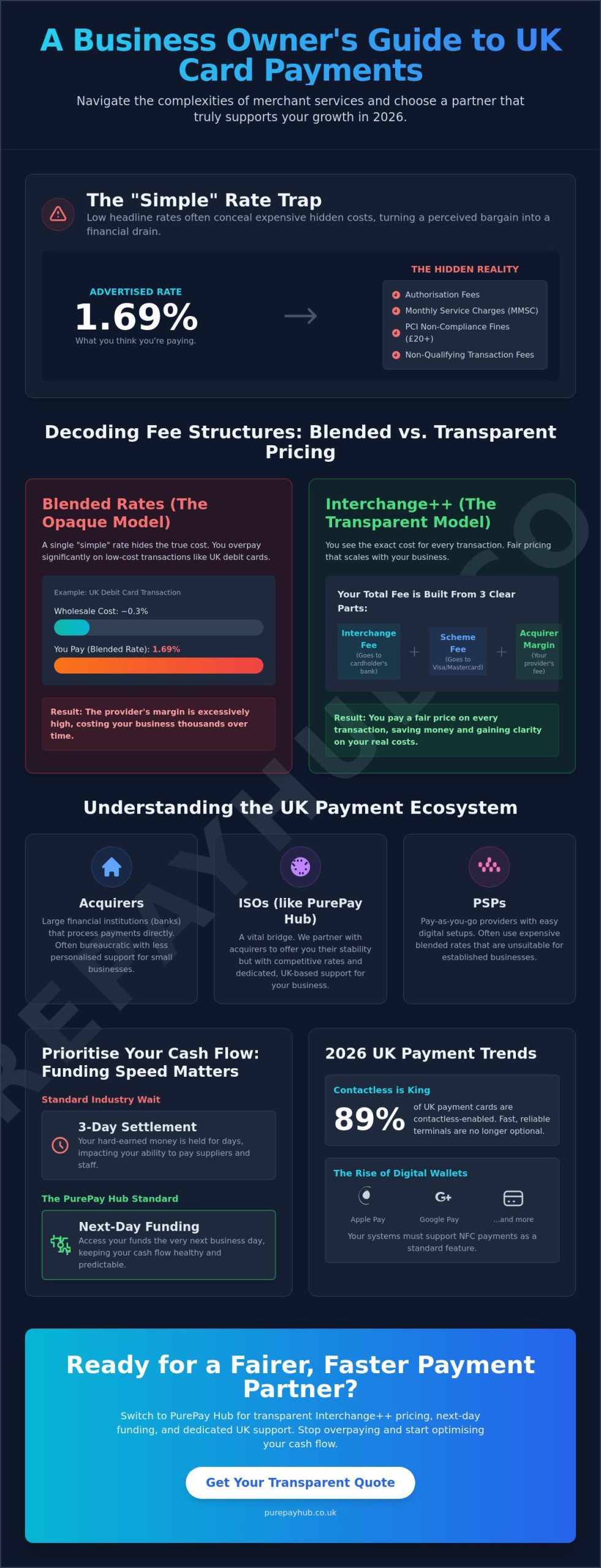

Fairness is our priority. We offer transparent, no-nonsense rates, such as 0.3% for debit transactions, to protect your hard-earned margins. This clarity ensures that your marketing budget isn’t quietly drained by hidden markups or complex fee structures. We also provide next-day funding as standard. This ensures your cash flow keeps up with your growth, allowing you to reinvest in your business without waiting days for your own money to arrive. When your finances are stable and predictable, you can plan your next move with total confidence.

A Partner, Not Just a Provider

We position ourselves as a supportive business ally rather than a distant financial institution. Our “no-jargon” approach mirrors the clarity you need in your own marketing strategy. You don’t have time to decode complex contracts or hidden costs. By providing reliable hardware and straight-talking support, we ensure you are never “marketing in the dark” regarding your operational expenses. Our systems act as a stabilising force for your business, allowing you to focus on building relationships with your customers whilst we handle the technicalities of the transaction.

Fueling Your Marketing Strategy

Effective marketing often requires a capital injection at the right moment. We support your expansion through flexible Business Cash Advances based on your actual sales. You can use this funding to launch seasonal marketing campaigns, upgrade your inventory, or professionalise your digital presence. Because the repayments are linked to your sales, the process feels fair and manageable even during quieter periods.

Data is the final piece of the puzzle. Our integrated EPOS Systems provide the insights you need to understand your busiest periods and customer behaviours. This information allows you to target your promotions with precision rather than relying on gut feeling. When you combine professional hardware with data-driven strategy, you close the gap between simply “shouting” and achieving actual, sustainable growth. Organise your payments with PurePay Hub and close the gap today.

Bridge the Gap for Sustainable Growth

The Gap: Small businesses think marketing is just promotion, but actual growth comes from aligning your operations with your promises. By auditing your customer journey and focusing on retention, you turn one-time shoppers into loyal advocates. Every touchpoint matters. The moment of payment is your final chance to prove your professionalism and build lasting trust.

You don’t have to navigate these challenges alone. We provide the tools and transparency needed to protect your margins whilst you scale. You can get a transparent quote on card machine rates from PurePay Hub to start professionalising your operations today. Our fair model includes debit card rates from 0.3%, next-day access to funds, and PCI compliance management as standard.

Take control of your business narrative. With the right systems in place, your brand will look larger, act faster, and grow more reliably.

Frequently Asked Questions

What is the biggest marketing mistake small businesses make?

The biggest mistake is treating advertising as the entire marketing strategy. The Gap: Small businesses think marketing is just about social media or adverts, but it actually encompasses your whole customer journey. Ignoring your operations and current customers whilst chasing new leads leads to wasted budgets and high friction. You must fix your internal processes and ensure your service is reliable before you start shouting for attention.

How can I market my small business with no budget?

You can market effectively with no budget by optimising your Google Business Profile and encouraging word of mouth through exceptional service. Focus on being easy to do business with by ensuring your payment process is seamless and professional. High quality service is your most powerful promotional tool. It costs nothing but your time and attention to turn a one-time visitor into a loyal advocate for your brand.

Why do I need a marketing plan if I am a sole trader?

A plan ensures your effort translates into profit rather than just noise. Even for a sole trader, a documented roadmap prevents you from wasting time on tactics that do not suit your specific goals. It helps you stay disciplined and ensures your promotional activities actually relate to your bank balance. Without a plan, you risk falling into the trap of random acts of marketing that drain your energy and cash.

Does my card machine really affect my marketing?

Yes, your card machine is the final physical touchpoint of your brand experience. A slow or unreliable machine creates friction and anxiety at the most sensitive moment of the sale. Professional hardware signals that you are a dependable business, which encourages repeat visits and positive referrals. Providing a seamless payment experience is a silent promise of professional service that protects your hard-earned reputation and ensures customers leave with a positive impression.

How do I measure the ROI of my marketing efforts?

You measure ROI by comparing your marketing spend against the specific sales growth it generates over a set period. Use your EPOS reports to track sales peaks during campaign periods and identify which products are performing best. This data-driven approach removes the guesswork from your budget. It helps you identify which favourite customers are driving your revenue so you can double down on the tactics that actually work for your business.

What is the difference between a merchant account and a business bank account?

A business bank account is where you store your company’s cash and pay your regular bills. A merchant account is a specific type of account that allows you to accept and process card payments from your customers. The funds from your card sales are held in the merchant account during security checks before being deposited into your bank account. Both are essential for a modern business to operate professionally and transparently.

Can a business cash advance help with my marketing?

A business cash advance is an excellent way to fund seasonal marketing or inventory boosts without the pressure of fixed monthly payments. Unlike traditional loans, repayments are linked directly to your future card sales. This makes it a flexible option for businesses looking to bridge a gap in their growth strategy. You can use the funds to launch new campaigns or upgrade your hardware, paying back only when you are actually making sales.

Why is customer retention considered part of marketing?

Retention is a vital part of marketing because it is five times cheaper to keep a customer than to find a new one. The Gap: Small businesses think marketing is just about the first sale, but the real profit lies in the lifetime value of a customer. Happy repeat buyers are the foundation of any sustainable growth strategy. By focusing on retention, you ensure your business remains resilient whilst reducing the constant pressure to find new leads.