Why does your monthly statement show a 2.5% charge when you signed a contract for 0.5%? Most UK business owners find that their “headline rate” is little more than a marketing myth. You might think you’ve secured a competitive deal, only to see your profits eroded by unexpected “admin” charges or “non-compliance” penalties. Calculating the true cost of card payments shouldn’t require a degree in forensic accounting. It’s time to pull back the curtain on the opaque fee structures that legacy providers use to hide their markups.

We know how exhausting it is to navigate a sea of jargon just to understand your own finances. At PurePay Hub, we believe you deserve a partner who treats your business with honesty and provides total clarity. This guide will help you decode every line item on your statement, from domestic interchange caps to the steep 1.50% cross-border fees on EEA credit cards. We’ll provide the exact formula to calculate your “effective rate,” which is the only metric that truly reflects your processing costs. By the end, you’ll be able to compare provider quotes with confidence and negotiate the fair terms your business deserves.

Key Takeaways

- Discover why the low “headline rate” on your contract often bears little resemblance to the actual amount deducted from your bank account.

- Identify the specific “admin” and “non-compliance” surcharges that frequently clutter UK merchant statements and inflate your monthly processing bills.

- Learn the three pillars of payment costs; Interchange, Scheme Fees, and Acquirer Margin; to understand exactly how your fees are structured.

- Master a simple, step-by-step formula for calculating the true cost of card payments to audit your provider’s performance with total accuracy.

- Find out how switching to a transparent model with next-day funding can stabilise your cash flow and eliminate the frustration of hidden markups.

Beyond the Headline: Why Calculating the True Cost of Card Payments Matters

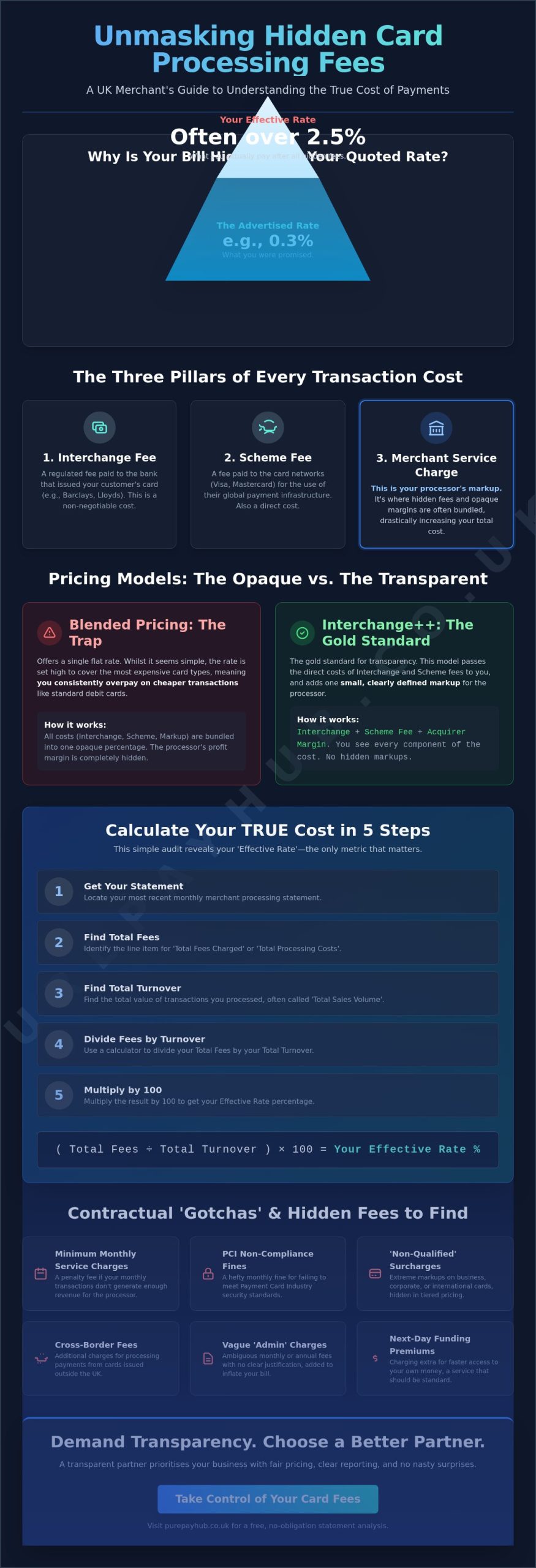

The headline rate you see on a provider’s marketing materials is often a distraction. For many UK merchants, a quoted rate of 0.3% for debit or 0.5% for credit sounds like an unbeatable bargain. However, the “True Cost” of your processing is the total sum of every transactional charge, fixed monthly fee, and administrative surcharge combined. Without calculating the true cost of card payments across your entire turnover, you’re essentially flying blind. This section explores why the headline figure is rarely the final figure on your bank statement.

Most traditional providers use these low figures as a hook. They know that once you’ve integrated their hardware and signed a lengthy contract, the secondary charges will begin to accumulate. These hidden costs often turn a “cheap” deal into a significant financial burden. Understanding the difference between what you were promised and what you’re actually paying is the first step toward taking control of your business’s financial health.

The Difference Between Headline Rates and Actual Costs

Teaser rates are designed to lure businesses into long-term agreements. These rates usually apply only to the most basic consumer debit cards issued within the UK. In reality, your daily sales include a complex mix of premium rewards cards, corporate cards, and international transactions. Each of these carries a different Interchange fee, which is the underlying cost paid between banks to process the payment. When your provider adds their markup and various “scheme fees” on top, that 0.3% headline rate quickly vanishes. You might find yourself paying three or four times your quoted rate for a significant portion of your transactions, whilst still being charged for terminal rental and PCI management on top.

How Processing Fees Erode SME Profitability

In high-volume sectors like hospitality or retail, profit margins are often razor-thin. A 1% difference in your processing rate might seem negligible on a single transaction, but it equates to thousands of pounds in lost revenue over a trading year. This is money that could have been reinvested in staff, stock, or marketing. Calculating the true cost of card payments reveals exactly how much of your hard-earned profit is being diverted to your acquirer’s bottom line.

Beyond the transaction itself, there’s the “invisible” cost of slow funding cycles. If your provider holds onto your money for three to five days, your cash flow suffers. This delay can prevent you from paying suppliers or managing daily overheads effectively. To gain total clarity, you must look at your “Effective Rate.” The Effective Rate is the total monthly cost of all fees and charges divided by your total card sales volume.

Decoding Your Merchant Statement: Identifying Hidden Fees and Surcharges

Reading a merchant statement often feels like deciphering a dead language. Legacy banks frequently use complex layouts and technical jargon to obscure the true price of their services. Whilst the first page might look straightforward, the real story is usually buried in the granular breakdown on the following pages. To master calculating the true cost of card payments, you must learn to spot the line items that don’t belong to the transaction rate itself. These fees are often listed separately to keep the headline rate looking artificially low.

Most statements follow a predictable pattern. You will see a summary of your total turnover, followed by a list of transaction types and then a section for “surcharges” or “service fees.” It is in this final section where most of the hidden costs reside. If your current provider makes it difficult to find these numbers, it is likely by design. A transparent partner should provide a clear, honest view of every penny leaving your account.

Common Fixed Costs on Your Monthly Bill

Fixed costs are the baseline expenses you pay regardless of how many sales you process. Terminal rental fees are the most common, covering the physical hardware like your Countertop Card Machine or Portable Card Machine. You should also look for PCI DSS compliance fees. Whilst data security is essential, many providers also levy “non-compliance” fees. These are essentially penalties for missing a paperwork deadline, often costing businesses £30 or more each month. Finally, watch out for authorisation fees. This is a small “ping” fee charged every time your machine contacts the bank, which can quietly add up to a significant sum by month-end.

Variable Surcharges to Watch Out For

Variable surcharges fluctuate based on your card mix and how you take payments. The Minimum Monthly Service Charge (MMSC) is particularly punishing for seasonal or low-volume traders. If your total transaction fees don’t reach a set threshold, the bank charges you the difference. You should also check for Card Not Present (CNP) surcharges, which apply whenever you use a Virtual Terminal or take a payment over the phone. Because these are deemed higher risk, legacy providers often add a significant markup. If your statement is cluttered with these confusing extras, you might prefer a partner that prioritises transparent card processing without the murky markups.

International and corporate cards are another area where costs can spiral. These cards aren’t subject to the same regulatory caps as UK consumer cards, allowing acquirers to justify much higher rates. When calculating the true cost of card payments, these variable surcharges are often the reason your effective rate ends up much higher than your contract suggested, though high-volume B2B specialists like P2EZPay Merchant Services can help navigate these specific complexities.

The Three Pillars of UK Card Processing Costs

Every time a customer taps their card on your Countertop Card Machine, the transaction fee you pay is split into three distinct parts. These components combined form your Merchant Service Charge (MSC). Understanding this structure is the only way to succeed in calculating the true cost of card payments. Many legacy providers bundle these costs together to hide exactly how much profit they are taking from each sale. By breaking them down, you can see where your money is actually going.

The UK payment landscape is governed by specific regulations that dictate these costs. Whilst some elements are fixed by international card schemes, others are entirely within your provider’s control. A transparent partner will always be happy to show you the “unbundled” view of these three pillars.

Interchange Fees: The Non-Negotiable Core

The interchange fee is the largest portion of the transaction cost. This is the fee paid to the bank that issued the customer’s card. In the UK, the Interchange Fee Regulation (IFR) caps these costs for domestic consumer cards at 0.2% for debit and 0.3% for credit. These caps are designed to protect merchants from spiralling costs. However, these regulations don’t apply to every card. Business cards, premium rewards cards, and international cards often carry much higher rates. For example, as of July 2026, cross-border transactions between the UK and the EEA attract uncapped fees of 1.15% for debit and 1.50% for credit. This is why your “headline rate” rarely reflects your actual monthly bill.

Scheme Fees and Acquirer Markups

Scheme fees are essentially a toll paid to Visa or Mastercard for the right to use their global payment networks. These fees are set by the card brands themselves and are passed on to you by your acquirer. The final pillar is the Acquirer Margin. This is the markup your provider adds to cover their own operational costs, risk management, and profit. When calculating the true cost of card payments, this is the only part of the transaction fee that is truly negotiable. If your provider uses a “Blended” pricing model, they charge you one flat rate for everything. This might seem simple, but it often allows them to pocket the difference when you process low-cost domestic debit cards.

Smart business owners prefer “Interchange Plus” pricing. This model separates the interchange and scheme fees from the provider’s markup. It ensures you benefit from the lower regulatory caps on UK consumer cards rather than paying a high flat rate across the board. This level of transparency is essential for any business looking to protect its margins from unnecessary markups.

The Effective Rate Formula: A Practical Guide to Auditing Your Costs

You can’t manage what you don’t measure. Calculating the true cost of card payments requires moving beyond individual line items to see the bigger picture. The most reliable way to do this is by finding your “Effective Rate.” This single percentage represents the total impact of processing on your revenue. It strips away the marketing fluff and reveals the reality of your overheads. By aggregating every charge from your merchant statement, you gain the clarity needed to decide if your current deal is actually fair.

Before you begin, gather your statements from the last three months. Auditing a single month can be misleading, especially if your sales are seasonal. A three-month average provides a more stable view of your business’s health. It’s also vital to treat one-off setup costs separately from your ongoing rate. Whilst setup fees impact your first-year profits, they don’t reflect your monthly processing efficiency.

Step-by-Step: Calculating Your Business Effective Rate

Follow these three steps to find your true cost. First, total every fee listed on your statement. This must include your transaction rates, terminal rental, PCI compliance charges, and any authorisation “ping” fees. If you’re VAT-registered, use the net fee amount to see the service cost, or the gross amount to see the total cash impact. Second, identify your total gross card turnover for that same period. Do not subtract refunds or chargebacks yet; we want the raw volume processed through your Portable Card Machine or Online Payment Gateway.

Third, divide your total fees by your gross turnover and multiply by 100. For example, if you paid £200 in total fees on £10,000 of sales, your effective rate is 2%. An effective rate above 2.5% for a standard retail business may indicate overcharging. If you need help Understanding Your Merchant Account Fees, we recommend starting with this simple audit to identify where your money is going.

Benchmarking Your Results Against Industry Standards

Once you have your number, you need to know how it stacks up. In 2026, a “Good” effective rate for a high-volume UK retail business typically sits below 1.5%. A “Fair” rate ranges between 1.6% and 2.2%, whilst anything above 2.3% is generally considered “Poor” for standard domestic trade. These benchmarks change if you have a low average transaction value (ATV), as fixed authorisation fees will represent a larger slice of each sale.

Business volume also plays a role. Higher turnover usually grants you more leverage to negotiate the acquirer margin. If your audit reveals a poor rate, it’s time to speak with a partner that offers transparent card machine pricing without hidden markups. Understanding your data is the first step toward reclaiming your profit margins.

Optimising Your Payment Strategy with PurePay Hub

You’ve done the hard work. By following our formula, you now have a clear view of your effective rate and how it stacks up against the UK market. If your audit revealed that you’re paying more than 2.3% for standard domestic trade, your business is likely subsidising your provider’s hidden markups. Calculating the true cost of card payments is only the first step; the second is choosing a partner that prioritises your profitability. At PurePay Hub, we believe that transparency is the foundation of a fair business partnership.

Switching your provider shouldn’t be a source of stress. We’ve designed our service to act as a stabilising force for your finances, replacing murky fee structures with absolute clarity. Whether you use a Countertop Card Machine in a local shop or an Online Payment Gateway for national sales, you deserve to know exactly where every penny goes. Our team specialises in “Switch and Save” audits, where we help you identify every unnecessary surcharge on your current statement and provide a straightforward alternative.

Transparent Pricing with No Hidden Markups

PurePay Hub simplifies your monthly reporting by eliminating the jargon that legacy banks use to hide their margins. We offer competitive debit rates starting from 0.3% and credit rates from 0.5%, ensuring your business keeps more of every sale. By providing a centralised “hub” for your payments, we help you manage everything from a Mobile Card Machine to Payment Links through a single, easy-to-read interface. This integration extends to our EPOS Systems, which reduce administrative overheads by automatically reconciling your sales and fees. You’ll spend less time on forensics and more time on growth.

Next-Day Access to Your Hard-Earned Funds

Cash flow is the lifeblood of any UK SME. Waiting three to five days for your funds to clear can stall your operations and make it difficult to manage supplier payments. We solve this by providing next-day access to your funds, ensuring your hard-earned money is back in your account when you need it most. This rapid settlement cycle is a core part of our commitment to supporting regional business owners. For those looking to expand, we also offer a Business Cash Advance based on your card sales, providing a flexible way to fund new equipment or stock without the rigid constraints of traditional bank loans.

Taking control of your overheads starts with an honest conversation. If you’re ready to stop calculating the true cost of card payments and start enjoying a fairer rate, our specialists are here to help. We’ll review your current statement and show you exactly how much you could save by moving to a transparent model. Request a transparent quote from PurePay Hub today and experience the difference that professional, no-nonsense card processing can make to your bottom line.

Reclaiming Your Profit Margins with Total Clarity

You now have the tools to audit your merchant statement and identify the hidden surcharges that erode your bottom line. By calculating the true cost of card payments, you’ve moved from confusion to informed confidence. You understand that the “headline rate” is often a distraction and that your effective rate is the only metric that truly reflects your processing efficiency. Knowledge is your best defence against the opaque practices of legacy providers.

It’s time to stop overpaying for murky services and start working with a partner that values your business. PurePay Hub offers a fair, no-nonsense alternative with debit rates starting from 0.3% and next-day funding provided as standard. We eliminate complex jargon and hidden markups to ensure you always know exactly what you’re paying. Get a transparent card payment quote from PurePay Hub

Your hard-earned revenue belongs in your bank account, not your provider’s pocket. Take the first step toward a more profitable future today. We’re ready to help you stabilise your finances and grow with confidence.

Frequently Asked Questions

What is a typical credit card processing fee for small businesses in the UK?

Typical effective rates for UK small businesses often range between 1.0% and 2.5%, depending on your industry and card mix. Whilst domestic consumer credit cards have an interchange cap of 0.3%, your final fee includes scheme fees and the acquirer’s markup. Businesses with lower turnover or those processing many international cards will usually see rates at the higher end of this scale.

Why is my merchant statement so much higher than my agreed transaction rate?

Your agreed rate is likely a “headline rate” that only applies to basic UK consumer cards. When calculating the true cost of card payments, you must account for premium, corporate, and international cards that carry much higher surcharges. Statements also include fixed monthly costs like terminal rental, authorisation fees, and PCI compliance charges that aren’t part of your transaction percentage.

Can I negotiate my card processing fees with my current provider?

You can negotiate the acquirer margin, which is the specific markup your provider adds to cover their own costs and profit. Interchange fees and scheme fees are set by the banks and card brands and are non-negotiable. If you’ve been with the same provider for several years, you likely have room to secure a fairer deal by auditing your current effective rate.

What is the difference between a merchant account fee and a transaction fee?

A merchant account fee is a fixed monthly cost you pay regardless of how many sales you make, such as terminal rental or PCI management fees. A transaction fee is the variable cost charged every time a customer uses their card. Understanding the balance between these two is essential for calculating the true cost of card payments across your total turnover.

Are there hidden costs associated with “free” card machine offers?

Providers often recoup the cost of “free” hardware by charging significantly higher transaction rates or locking you into long, restrictive contracts. You might also find higher monthly “admin” or “service” fees buried in the small print. It is often more cost-effective to pay a transparent monthly rental for a high-quality Portable Card Machine than to accept a “free” offer with murky markups.

How do PCI compliance fees work and can I avoid them?

PCI fees cover the administrative costs of ensuring your business handles card data securely. Whilst you can’t avoid the security requirements, you can avoid expensive “non-compliance” penalties by completing your annual self-assessment questionnaire. Many modern providers now include basic compliance management in their service to help you stay protected without facing unexpected monthly fines.

What happens if my business does not meet the Minimum Monthly Service Charge?

If your total transaction fees for the month don’t reach the Minimum Monthly Service Charge (MMSC) threshold, your provider will charge you the difference. This ensures they maintain a minimum level of revenue from your account even during quiet periods. This fee can be particularly frustrating for seasonal traders or new businesses that are still building their customer base.

Is it cheaper to accept debit cards or credit cards in the UK?

Debit cards are significantly cheaper to process because their domestic interchange fees are capped at 0.2%, compared to 0.3% for credit cards. This lower baseline cost means your provider can offer much more competitive rates for debit transactions. Encouraging customers to use debit cards can be a simple way to protect your profit margins and reduce your overall processing overheads.