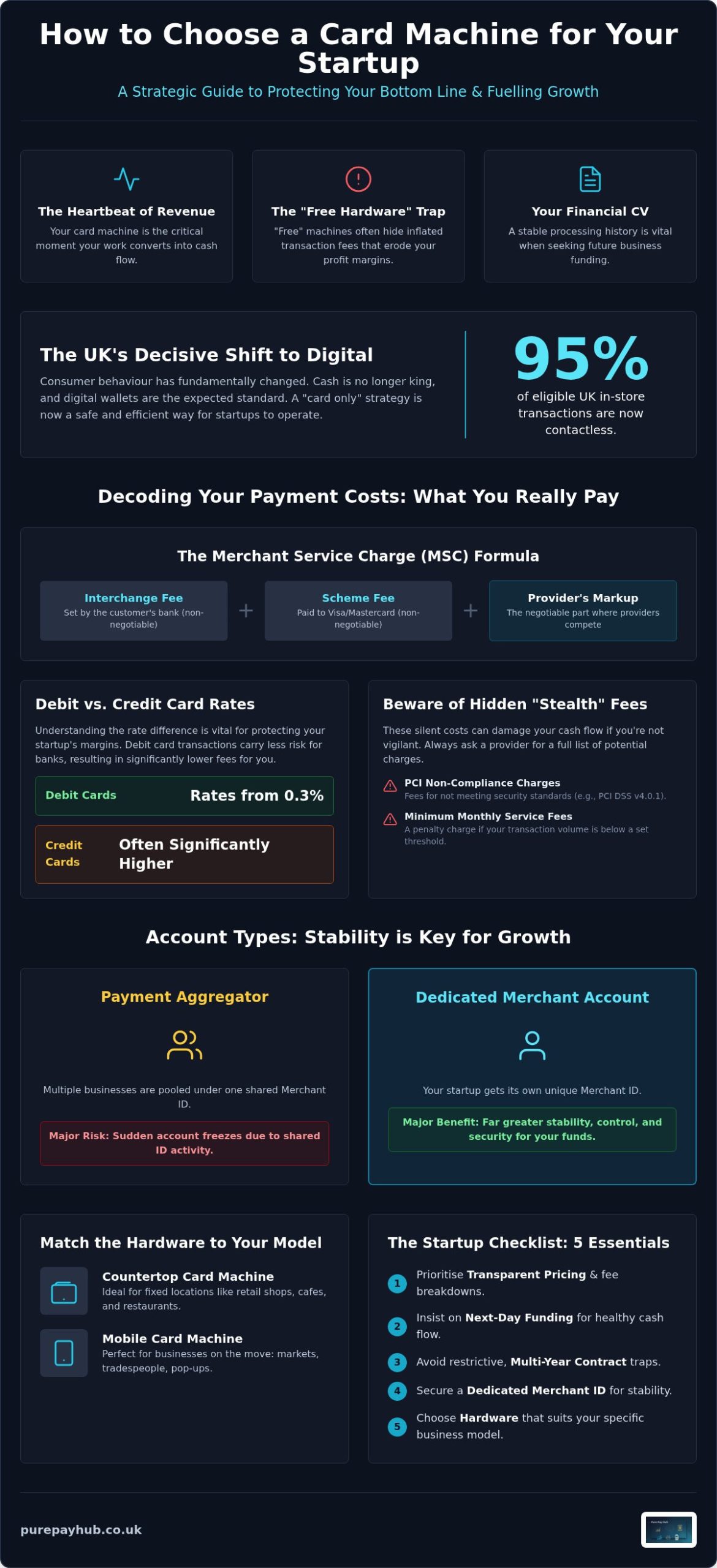

The slickest-looking card reader on the market could be the very thing that drains your startup’s bank account before you’ve even found your feet. Many founders focus on the hardware’s aesthetic, but learning how to choose a card machine for a startup is actually about protecting your bottom line from predatory fee structures. In 2026, with nearly all UK transactions being contactless and the FCA relaxing limit caps, the stakes for your cash flow have never been higher.

You’re likely feeling the pressure of hidden monthly costs and the confusing jargon of interchange fees versus merchant service charges. It’s frustrating to feel like you’re signing away your freedom to a long-term contract just to take a simple payment. We understand that anxiety. This guide will show you how to secure transparent pricing and next-day funding whilst choosing hardware that looks professional to your customers. We will break down the technicalities of PCI DSS v4.0.1 and show you exactly how to find a payment partner that scales with your ambition rather than holding it back.

Key Takeaways

- Understand why your card machine is the heartbeat of your revenue and why “free” hardware often hides the most expensive transaction rates.

- Learn to decode the Merchant Service Charge and discover why lower debit card rates offer a vital boost to your startup’s margins.

- Select the right hardware for your specific business model, whether you require a Countertop Card Machine for a fixed location or a Mobile Card Machine for life on the move.

- Master how to choose a card machine for a startup by prioritising next-day funding speed and avoiding restrictive, multi-year contract traps.

- Discover how to scale your venture with transparent payment solutions that prioritise clarity and cash flow over complex, hidden markups.

Why Your Choice of Card Machine is a Strategic Startup Decision

Your card machine is the heartbeat of your startup’s revenue stream. It represents the exact moment your hard work converts into liquid cash. Many founders treat this as a last-minute errand, but understanding how to choose a card machine for a startup is a vital strategic move. A poor choice doesn’t just look unprofessional; it can actively stifle your growth by locking you into high rates or delaying access to your own money.

Beware of the “free hardware” lure. In the payments industry, “free” usually means you’ll pay significantly more through inflated transaction fees. These costs eat into your margins every time a customer taps their card. For a new business, those pennies add up to pounds that could have been reinvested in stock or marketing. Beyond the cost, there is a psychological weight to payment reliability. If your machine fails during a peak period, you lose more than a sale; you lose the trust of a first-time customer.

Your processing history also acts as a financial CV. When you eventually look for a Business Cash Advance or other forms of growth capital, lenders will scrutinise your transaction data. A stable, professional setup shows your business is a reliable prospect for future funding. It demonstrates that you have a disciplined approach to your finances from day one.

The Shift from Cash to Contactless in the UK

The UK has moved decisively away from cash. In 2024, nearly 95% of eligible in-store transactions were contactless. Consumer behaviour has shifted toward digital wallets like Apple Pay and Google Pay as a minimum standard. For a startup, a “card only” strategy is no longer a risk; it’s often a safer, more efficient way to operate that reduces the security burden of handling physical cash. Ensuring your Payment Terminal is equipped with the latest NFC technology is essential for meeting these expectations.

Merchant Accounts vs. Payment Aggregators

When deciding how to choose a card machine for a startup, you must consider the difference between sharing an ID and having your own. Startups often begin with aggregators because the setup is fast. However, these platforms pool multiple businesses under one Merchant ID, which can lead to sudden account freezes if your sales spike. A dedicated merchant account provides far more stability. PurePay Hub offers this professional stability whilst keeping the onboarding process fast and transparent. By securing your own Merchant ID, you gain more control over your funds and build a resilient foundation for your growing venture.

Decoding Startup Payment Costs: Rates, Rentals, and Hidden Fees

Every penny counts during your first year of trading. Understanding the Merchant Service Charge (MSC) is the first step in mastering how to choose a card machine for a startup. This charge is the total percentage you pay on every transaction. It isn’t a single fee, but a combination of three distinct costs: interchange fees, scheme fees, and the provider’s markup. Many traditional banks bundle these together, making it nearly impossible to see where your money is actually going.

The most significant cost difference you’ll notice is between debit and credit cards. Debit card rates can start as low as 0.3%, whilst credit cards are often significantly higher. This is because debit transactions carry less risk for the banks; the money is already in the customer’s account. Before signing any contract, it’s wise to review the standard steps to accept card payments to ensure you aren’t skipping vital security or registration requirements that could inflate these rates later.

Stealth fees are the silent killers of startup cash flow. You might encounter PCI non-compliance charges if you don’t keep up with the latest v4.0.1 security standards. Some providers also enforce a “minimum monthly service fee.” If you don’t process enough transactions to meet their threshold, they’ll charge you the difference anyway. Whilst you compare these structures, consider how a transparent pricing model can simplify your monthly overheads and keep your margins predictable.

Interchange Fees and Scheme Fees Explained

Interchange fees are set by the card issuer (the customer’s bank), whilst scheme fees are paid to the card brand, such as Visa or Mastercard. These are non-negotiable base costs. A trustworthy partner will be open about these “at-cost” rates. If a provider refuses to show you the breakdown between the base rate and their own markup, they’re likely hiding a heavy commission that will hurt your business as it scales.

The Real Cost of “No Monthly Fee” Models

Many startups are drawn to providers that offer “no monthly fees” and high flat-rate transaction costs, often around 1.75%. This feels safe when you’re starting out, but the “break-even” point arrives sooner than you think. If your startup processes £5,000 a month, a 1.75% fee costs you £87.50. In contrast, a how to choose a card machine for a startup strategy that includes a small monthly rental and a 0.3% debit rate could save you over £50 every single month. Those savings are better spent on your own growth than on a processor’s bottom line.

Choosing the Right Hardware for Your Startup Business Model

The physical environment of your business dictates your technical requirements. A coffee shop in a busy city centre has vastly different needs compared to a plumber working from a van. When researching how to choose a card machine for a startup, you must first map out your customer’s journey to the payment point. Is the transaction happening at a fixed counter, or are you bringing the machine to a table? Your choice here affects everything from transaction speed to the perceived legitimacy of your brand.

For hospitality ventures, integrated EPOS Systems are a non-negotiable requirement. These systems sync your sales data with your inventory and accounting software in real-time. This level of integration prevents human error and saves hours of manual reconciliation at the end of the day. When Choosing the Right Payment Processor, the hardware you select becomes the physical face of your brand. A sleek, heavy countertop unit suggests permanence and reliability, whilst a tiny, plastic mobile reader might not provide the same sense of security for high-value transactions.

Countertop and Portable Terminals

A Countertop Card Machine is the bedrock of retail shops and boutiques. These units connect via Ethernet or phone lines, providing unmatched connection stability. They don’t rely on battery life; this makes them perfect for high-volume environments where you can’t afford a device dying mid-afternoon. If your business requires movement within a fixed premises, a Portable Card Machine is the logical step. These units use Bluetooth or Wi-Fi to allow for “at the table” payments. They offer the flexibility of movement whilst maintaining a professional, robust appearance that customers recognise and trust.

Mobile Readers and Virtual Terminals

Mobile Card Machines are designed specifically for the modern tradesperson or mobile service provider. These devices use 4G connectivity via a built-in SIM card, ensuring you can take a payment anywhere with a mobile signal. This eliminates the awkwardness of asking a customer for their Wi-Fi password. For businesses that don’t need physical hardware at all, a Virtual Terminal allows you to process card details securely over the phone. You can also utilise Payment Links to send secure checkout pages via social media or email. These digital-first solutions are excellent for startups that operate remotely or sell primarily through digital consultations.

The Startup Checklist: 5 Essentials Before Signing an Agreement

Before you put pen to paper, you must look beyond the shiny hardware. Learning how to choose a card machine for a startup involves a deep dive into the small print that affects your daily operations. Your agility as a new business depends on the terms you accept today. Here are the five essentials every founder must verify before committing to a provider.

- Funding Speed: Your cash flow is your lifeblood. Some providers wait three to five working days to settle your funds. For a new business, this delay is unacceptable. Demand next-day access to your money to keep your stock levels high and your bills paid.

- Contract Flexibility: Avoid the multi-year trap. Many traditional banks lock you into three-year terms with heavy exit fees. If your business model shifts, you’re stuck. Seek out rolling contracts or short-term agreements that respect your need for flexibility.

- Onboarding Support: Some platforms claim you can sign up in minutes, but getting your hardware delivered and your account fully verified can take weeks. Ask for a clear timeline on when you’ll actually be taking your first payment.

- PCI Compliance: This isn’t just a tick-box exercise. It’s a security standard that protects your customers. A partner that manages this for you saves you from the stress of monthly non-compliance fines.

- Technical Support: When your machine stops working on a busy Saturday afternoon, a chatbot won’t help. You need to speak to a human expert immediately whilst your customers are waiting.

Security and Compliance for New Founders

PCI DSS v4.0.1 is the current security gold standard. It ensures that every transaction is encrypted from end to end. If you don’t meet these requirements, you face significant financial penalties. A professional provider will guide you through the compliance process, turning a complex technical hurdle into a simple, manageable task. This protection preserves your reputation and maintains your favour amongst your first customers.

Integration and Future-Proofing

Your card machine shouldn’t be an island. It needs to talk to your accounting software and your EPOS Systems. Real-time reporting allows you to track your early growth without manually entering data into spreadsheets. Choosing a scalable system now prevents a painful and expensive migration once your transaction volume increases. Ready to secure a partner that values your cash flow as much as you do? Explore our transparent merchant services and get your startup live with next-day funding.

Scaling Your Venture with PurePay Hub’s Transparent Solutions

Traditional banks often view new ventures with suspicion, hiding high rates behind complex corporate jargon. PurePay Hub is the straight-talking alternative. We prioritise clarity and fairness because we know that a startup’s success depends on predictable overheads. When you’re deciding how to choose a card machine for a startup, you need a partner that advocates for your growth rather than one that merely provides a piece of hardware. We position ourselves as a supportive ally to the local merchant community.

Our 0.3% debit rates provide an immediate boost to your margins. In the early stages of a business, every saved pound is capital you can use to hire your first employee or expand your product line. We don’t believe in the murky markups used by traditional competitors. Instead, we offer a modern fintech experience that keeps its focus on the individual business owner. This transparency builds the trust necessary for a long-term professional partnership.

Next-Day Funding: The Startup Lifeline

Waiting three to five working days for your money to clear is a relic of a slower era. In 2026, your supply chain moves fast. You need your revenue available to restock inventory or settle urgent invoices immediately. PurePay Hub’s quick settlement ensures your cash flow remains fluid and your momentum never stalls. Next-day funding is the standard for modern UK merchant services.

Unlocking Capital with Business Cash Advances

Scaling a business often requires a sudden injection of capital. Whether you need to fund a marketing push or buy stock in bulk, a Business Cash Advance offers a flexible solution. Unlike traditional loans, this is unsecured capital based on your card turnover. You repay the advance as a small, agreed percentage of your daily card sales. This means your repayments always stay in proportion with your actual income.

This model is particularly safe for seasonal startups. If you have a quiet week, your repayments automatically reduce. It’s a supportive way to grow that mirrors the actual performance of your venture. Our UK-based support team is here to guide you through every step of this process, providing the expert partnership your startup deserves. Understanding how to choose a card machine for a startup is just the beginning of our journey together. We are ready to help you scale with confidence and clarity.

Get your startup started with a PurePay Hub card machine today.

Secure Your Startup’s Financial Future Today

Choosing your payment partner is one of the most significant hurdles you’ll face as a new founder. By prioritising funding speed and transparent fee structures, you protect your business’s ability to scale without being weighed down by predatory costs. Mastering how to choose a card machine for a startup isn’t just about selecting a device; it’s about building a resilient revenue stream that works as hard as you do. You now understand that “free” hardware often masks expensive transaction rates and that next-day funding is essential for maintaining a healthy supply chain.

We believe in a straight-talking approach that puts the business owner first. With debit rates from 0.3% and next-day funding as standard, we ensure your hard-earned money stays where it belongs: in your bank account. Our no-nonsense UK-based support team acts as a reliable expert to help you navigate any technical challenges whilst you focus on growth. Join the UK startups choosing transparency with PurePay Hub and take control of your payments from day one. Your ambition deserves a partner that values clarity over complexity. We are ready to help you turn your vision into a thriving, profitable reality.

Frequently Asked Questions

How long does it take to set up a card machine for a new business?

You can typically expect your card machine to be live and ready for use within three to five working days. This timeframe includes the necessary security checks and the physical delivery of your hardware. Whilst some providers claim near-instant setup, these often lack the stability of a dedicated merchant account. We prioritise a thorough but efficient onboarding process to ensure your business is protected and compliant from day one.

Can I get a card machine if I have a poor credit history as a founder?

Yes, a poor credit history doesn’t automatically disqualify you from accepting card payments. Merchant service providers focus primarily on the risk associated with your business model rather than just your personal credit score. You might find that some providers require a rolling reserve or slightly different terms initially. We look at the potential of your venture and provide a fair assessment based on your projected transaction volumes and business type.

Is it cheaper to buy or rent a card payment terminal?

Renting is often the more cost-effective choice for startups because it includes ongoing technical support and automatic hardware upgrades. Buying a device outright involves a larger upfront cost and leaves you responsible for repairs or replacements if the technology becomes obsolete. When deciding how to choose a card machine for a startup, consider that rental models often provide better long-term value through inclusive maintenance and security updates.

What documents do I need to provide for a startup merchant account?

You will generally need to provide valid photo identification, proof of your home address, and a recent business bank statement. If you’ve incorporated, you’ll also need your Companies House registration details. These documents help providers verify your identity and ensure your business is legitimate. Providing clear, digital copies of these files during your application will significantly speed up the verification process and get you trading sooner.

Do I need a separate business bank account for my card machine payments?

Yes, having a dedicated business bank account is essential for maintaining clear financial records and is a requirement for most professional merchant services. It ensures that your business revenue is never blurred with your personal finances, making tax returns and accounting much simpler. Using a separate account also builds a professional profile for your startup, which is vital when you eventually seek further business funding or growth capital.

Can my startup take payments over the phone or via email links?

You can easily accept payments remotely using a Virtual Terminal or secure Payment Links. A Virtual Terminal turns your computer or tablet into a card reader for phone orders, whilst Payment Links allow you to send a secure checkout page directly to a customer via email or social media. These tools are perfect for startups that don’t always interact with their customers in a face-to-face retail environment or those offering remote consultations.

What happens if my Wi-Fi goes down during a transaction?

Most modern machines, such as a Mobile Card Machine, feature a built-in SIM card that automatically switches to a 4G mobile network if your Wi-Fi fails. This ensures you never miss a sale due to a poor internet connection. If you’re using a fixed Countertop Card Machine, having a backup mobile hotspot or choosing a device with dual-connectivity is a smart way to protect your revenue during local technical outages.

Are there any hidden exit fees if my startup needs to switch providers?

Some traditional providers hide steep cancellation charges in the small print of long-term contracts. It’s crucial to check for these fees before you sign any agreement. We advocate for contract flexibility, offering rolling agreements that don’t trap you if your business needs change. When researching how to choose a card machine for a startup, always prioritise providers that allow you to leave without facing punitive financial penalties or complex notice periods.