Why should taking a payment over the phone feel like a security gamble every time the line rings? If you’re still scribbling card numbers on paper or wrestling with outdated systems, you’re exposing your business to unnecessary fraud risks. A virtual terminal for mail order telephone order (MOTO) transactions solves this by turning any web browser into a secure, professional payment hub. It removes the need for bulky hardware whilst keeping your customer data safe and your office clutter-free.

We understand that ‘card-not-present’ transactions often bring worries about high fees and the headache of PCI DSS compliance. It’s frustrating when traditional banks hold onto your money for days or hide costs in the small print. This guide promises to clear the fog around remote payments, showing you how to process orders securely and efficiently. We will break down the latest 2026 security standards, explain how to secure low transaction rates, and show you how next-day funding can keep your cash flow healthy.

Key Takeaways

- Discover how a virtual terminal for mail order telephone order turns any internet-connected device into a secure payment centre without the need for expensive physical hardware.

- Learn why strict adherence to the latest PCI DSS standards is non-negotiable for protecting your business from fraud and maintaining customer trust.

- Compare the cost-efficiency of software-based solutions against traditional card machines to identify significant savings on monthly rental fees.

- Master professional communication scripts that ensure your team handles sensitive cardholder data safely whilst staying within legal boundaries.

- Understand the impact of next-day funding on your business, ensuring that remote payments translate into available cash flow without unnecessary delays.

What is a Virtual Terminal for Mail Order Telephone Order?

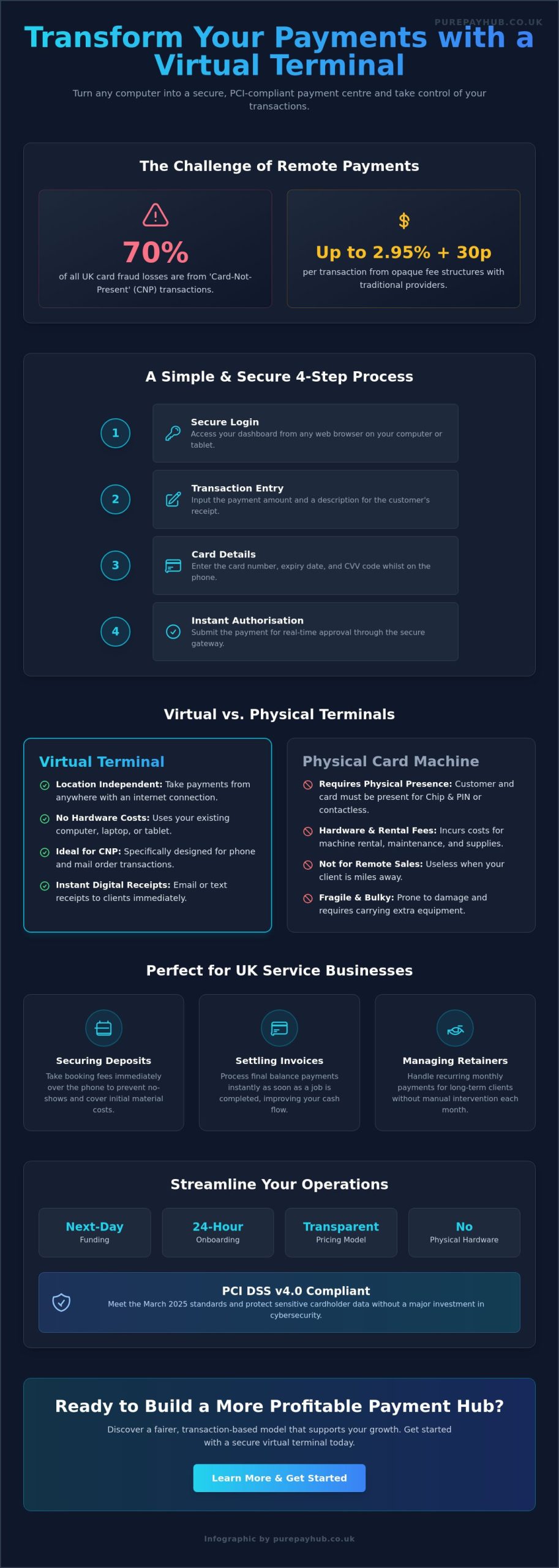

A virtual terminal for payment processing is a secure, web-based dashboard that allows you to take card payments manually. It functions like a digital version of a physical card machine but lives entirely within your web browser. You don’t need the customer to be standing in front of you, and you don’t need a piece of plastic to tap against a reader. Instead, you log into a secure portal, enter the card details provided by your customer, and process the transaction instantly. This setup is the backbone of any virtual terminal for mail order telephone order (MOTO) operation.

MOTO environments are unique because they rely on trust and speed. Whether you are taking an order over the phone or processing a payment form sent through the post, you need a system that handles sensitive data without the risks associated with physical paperwork. Whilst a standard payment gateway is built for e-commerce websites where the customer types in their own details, a virtual terminal is designed specifically for your staff to use. It gives you control over the transaction process whilst keeping the data entry environment isolated and secure.

Many UK businesses are currently moving away from using physical countertop machines for “card-not-present” entries. Keying in card numbers on a standard terminal is often clunky and slow. More importantly, it can lead to higher processing costs and compliance headaches. By switching to a dedicated virtual interface, you centralise your reporting and ensure that every remote payment is handled through a system built for that specific purpose.

The Mechanics of a Remote Payment

The process is designed for efficiency. Once you’ve logged into your secure browser-based portal, you simply enter the transaction amount and the customer’s card information. The system performs real-time authorisation, checking for available funds and validating the card details whilst you’re still speaking with the client. It’s a seamless experience that ends with an automatic digital receipt sent via email or SMS. This immediate confirmation builds confidence and keeps your records tidy without manual filing.

Who Benefits Most from MOTO Terminals?

Service-based professionals like accountants, solicitors, and tradespeople find these systems invaluable for taking deposits or settling invoices quickly. It’s far more professional than asking a client to perform a bank transfer. Wholesalers and distributors also rely on them to process high-volume orders received via phone or post. Even boutique retailers use them to expand their reach, allowing them to sell to customers across the country who might have seen a product on social media but prefer to pay over a friendly phone call.

Maximising Security and Compliance in Remote Processing

Security isn’t a luxury in the world of remote payments. It’s the foundation of your business reputation. When you use a virtual terminal for mail order telephone order, you handle sensitive cardholder data that requires constant protection. The most dangerous habit in many offices is scribbling card numbers on post-it notes or in paper ledgers. This creates a physical trail of data that is easily stolen or lost. A professional virtual terminal eliminates this risk by ensuring that sensitive information is typed directly into a secure, encrypted interface during the call.

Modern systems use high-level encryption to protect data. This means the card details never actually touch your local computer server or hard drive. They are scrambled and sent directly to the bank for authorisation. To add another layer of protection, multi-factor authentication (MFA) is now a standard requirement for accessing your merchant account. This ensures that even if a password is compromised, your funds and customer data remain shielded. If you want to move away from risky manual processes, you can explore secure payment solutions that put your business safety first.

The Importance of PCI DSS Compliance

The Payment Card Industry Data Security Standard (PCI DSS) is a set of rules all merchants must follow. Version 4.0.1 is the current standard. It’s non-negotiable for UK businesses. Failing to comply can lead to heavy monthly fines and the potential loss of your ability to process cards. PurePay Hub acts as a supportive ally here. We simplify the compliance process by providing a terminal that meets these rigorous standards out of the box. This allows you to focus on your customers whilst we handle the technical complexities of data safety.

Fraud Prevention Strategies for MOTO

Remote transactions are naturally higher risk because the card isn’t physically present. You can mitigate this by using the Address Verification Service (AVS). This checks if the billing address provided matches the one on file with the bank. You must also perform Card Security Code (CV2) checks. You are strictly prohibited from storing these three-digit codes after authorisation under PCI DSS rules. Identifying suspicious buying behaviour, such as unusually large orders from new customers, is your final line of defence. Staying vigilant keeps your chargeback rates low and your profits secure.

Virtual Terminal vs. Physical Card Machines: A Comparison

Choosing between hardware and software is about more than just having a piece of plastic on your desk. Physical card machines often come with hidden burdens that slow down a growing business. You pay for the monthly rental, the ongoing maintenance, and even the thermal paper rolls. A virtual terminal for mail order telephone order transactions removes these physical constraints entirely. It turns your existing computer, laptop, or tablet into a high-performance payment hub without requiring a single extra wire.

Mobility is a primary advantage here. A countertop machine is usually tied to a phone line or a power socket. In contrast, a virtual terminal follows you wherever you have an internet connection. This accessibility is vital for modern UK businesses that aren’t tied to a single desk. You can process a payment from a home office or a warehouse with the same level of security and professionalism. It’s a clean break from legacy hardware that often feels like a tether.

Transaction speed also improves when you move to a digital interface. Keying in a 16-digit card number on a small, rubber keypad is a recipe for manual errors. Using a full-sized computer keyboard is faster, more accurate, and more comfortable for your staff. This efficiency reduces the time spent on each call, allowing your team to handle more enquiries whilst improving the customer experience. Errors are caught instantly, preventing the frustration of a declined transaction after the customer has already hung up.

Scalability is equally straightforward. If your team grows, you don’t need to order and wait for new hardware to arrive in the post. You simply add a new user to your secure dashboard. This agility allows you to scale your operations up or down without being locked into expensive, long-term equipment leases that no longer fit your business model.

Cost-Benefit Analysis for UK SMEs

When you look at the total cost of ownership over a 12-month period, the savings often become clear. You eliminate the cost of paper rolls and the repair fees associated with physical units. Whilst transaction rates for a virtual terminal for mail order telephone order are typically higher than face-to-face rates due to “card-not-present” risks, the lack of fixed hardware costs balances the scales for many small businesses. You only pay for the service you use, rather than for a machine that sits idle during quiet periods.

Operational Flexibility

Operational freedom is the final piece of the puzzle. A virtual terminal allows your business to adapt to any environment. Consider these benefits:

- Remote working: Your staff can process orders from any location securely, supporting a modern hybrid work model.

- Integration: Many systems link directly with your accounting software to automate your bookkeeping and reduce manual data entry.

- Clean workspace: You maintain a professional, hardware-free reception centre or office, reducing clutter and technical failures.

This flexibility ensures your payment system moves with you. Whether you are moving offices or expanding your team, your terminal is always ready to work.

Best Practices for Taking Telephone and Mail Order Payments

Success with a virtual terminal for mail order telephone order isn’t just about the software. It’s about the human process. When your staff take card details over the phone, they represent your brand’s integrity. You should create a clear, professional script that guides the customer through the transaction. Tell them exactly when you’re opening the secure portal and when the payment has been authorised. This transparency builds trust and reduces the anxiety customers often feel when sharing sensitive data remotely.

Data protection must be your top priority. If you record your phone calls for training or quality purposes, you must never record the segment where card details are spoken. This is a critical PCI DSS requirement. Most modern call recording systems offer a “pause and resume” feature for this exact reason. Ensuring your workflow integrates payment collection at the right moment is also vital. Don’t wait until the end of a long order to ask for payment; confirm the total and process the card whilst the customer is still engaged. If a transaction fails, handle the decline with quiet professionalism. Suggest an alternative card or a different payment method without making the customer feel uncomfortable.

Staff Training and Behaviour

Educate your team on the weight of “card-not-present” security. They need to understand that a virtual terminal is a powerful tool that requires disciplined usage. We recommend setting up individual user permissions within your dashboard. This allows you to track who processed which transaction, providing a clear audit trail. Standardising your “thank you” process is equally important. Ensure every customer receives an immediate digital receipt. This small step confirms the transaction is complete and professional, leaving a positive lasting impression.

Managing Chargebacks and Disputes

MOTO transactions are naturally more prone to disputes because there is no physical PIN entry. To protect your business, keep detailed records of every order and proof of delivery. If a customer claims they didn’t authorise a payment, your evidence is your best defence. A transparent fee structure also helps. When a customer sees a clearly named charge on their bank statement, they’re less likely to be confused or raise a dispute. If you’re ready to start taking phone orders with a partner who values clarity, you can get started with PurePay Hub today for a straightforward setup process.

Streamline Your Remote Payments with PurePay Hub

PurePay Hub prioritises clarity and fairness. We know the payments industry is often viewed with skepticism due to hidden markups and complex contracts. Our approach is different. We provide a virtual terminal for mail order telephone order transactions that’s simple to use and easy to understand. You won’t find corporate jargon here. Instead, you get a reliable tool designed to help your business thrive. We act as a steady ally for regional merchants, moving away from the impersonal service of traditional banks.

We offer some of the most competitive rates in the UK. You can access debit rates starting at 0.3% and credit rates from 0.5%. These transparent prices ensure you keep more of your hard-earned revenue whilst avoiding the murky fee structures used by many competitors. Our no-nonsense setup means you can start taking payments without the stress of hidden costs or bulky hardware. It’s a modern solution built for the individual business owner who values efficiency and honesty.

Quick Onboarding and Next-Day Access

Getting started shouldn’t be a chore. We’ve streamlined our onboarding process so you can open your merchant account in record time. Once you’re set up, the benefits continue with next-day funding. Accessing your funds quickly is vital for restocking inventory and maintaining a healthy cash flow in 2026. You also gain access to personalised reporting and account management features. These tools give you a clear view of your business performance at a glance, allowing you to make informed decisions with confidence.

Integrated Financial Solutions

Your payment system should work as a unified force. By using our virtual terminal, you can manage both your online and telephone sales through one centralised dashboard. This reduces administrative clutter and simplifies your bookkeeping. If you need a boost to grow, our business cash advance offers strategic capital based on your future card turnover. It’s a flexible way to fund development without the stress of fixed monthly repayments. We are here to support your journey and provide the stability your finances need. Contact our team today to find your perfect payment fit.

Take Control of Your Remote Payments Today

Adopting a virtual terminal for mail order telephone order transactions is a strategic move for any modern UK business. You’ve seen how removing physical hardware reduces overheads whilst improving security and staff efficiency. By moving away from risky manual processes and towards encrypted digital portals, you protect both your reputation and your customers. Professionalism in every phone call builds the trust that drives long-term loyalty and repeat business.

PurePay Hub is ready to be your supportive ally in this transition. We provide a no-nonsense approach with debit rates starting at 0.3% and next-day funding as standard. You don’t have to navigate complex compliance or hidden fees alone. Our UK-based experts offer the honest guidance you need to keep your cash flow healthy and your operations secure. We believe in being a fair partner to regional merchants, ensuring your payment processing is as dependable as the service you provide.

It’s time to simplify your finances and focus on what you do best. Get a Transparent Quote for Your Virtual Terminal Today and discover a fairer way to process remote payments. We look forward to helping your business grow with confidence.

Frequently Asked Questions

What is a MOTO payment exactly?

MOTO stands for Mail Order Telephone Order. It’s a transaction where you take payment details from a customer who isn’t physically present at your premises. You manually enter their card number, expiry date, and security code into your system to process the sale. This method is the standard for businesses taking bookings or orders over the phone or through postal forms.

Is a virtual terminal secure for my customers?

Yes, using a virtual terminal for mail order telephone order is highly secure when managed through a compliant provider. The system encrypts data instantly and sends it directly to the bank for authorisation. This ensures that sensitive cardholder information never stays on your computer or office network. It’s far safer than writing details down, which is a major security and compliance risk.

Do I need a special merchant account for phone payments?

You do need a merchant account that is specifically configured for MOTO transactions. Banks view phone payments as a higher risk than face-to-face sales because the card isn’t physically swiped or PIN-verified. A dedicated account ensures you’re correctly insured and compliant with the latest financial regulations for remote processing, protecting your business from unnecessary liability.

How much does a virtual terminal cost per month?

Monthly costs for a virtual terminal vary depending on your provider and the volume of sales you process. Some providers charge a flat monthly subscription whilst others include the service as part of a wider payment package. You should look for transparent pricing structures that avoid hidden markups to ensure you get a fair deal that supports your business growth.

Can I use a virtual terminal on my mobile phone?

You can use a virtual terminal on almost any device with an internet connection, including your mobile phone. Since the terminal is a web-based application, you simply log in through your mobile browser to process payments securely. This gives you the flexibility to take orders whilst on the move or working from a temporary location without needing extra hardware.

How long does it take to set up a MOTO payment system?

Setting up a virtual terminal for mail order telephone order system is typically a very fast process. Once your merchant account application is approved, which often takes just a few business days, you can access your portal immediately. There is no physical hardware to wait for in the post, so you can start taking payments as soon as your secure login details arrive.

What is the difference between a payment gateway and a virtual terminal?

A payment gateway is the background technology that securely moves data from the merchant to the bank for online sales. A virtual terminal is the front-end interface your staff use to type in card details for phone or mail orders. Whilst the gateway handles the technical “plumbing”, the terminal provides the actual dashboard that makes manual data entry possible.

Are transaction rates higher for telephone orders?

Transaction rates for telephone orders are usually slightly higher than face-to-face rates. This is because “card-not-present” transactions carry a higher risk of fraud and chargebacks compared to physical PIN entries. However, by using a secure terminal and performing all required security checks, you can keep your rates competitive whilst protecting your business from potential losses.