What if your business funding actually breathed with you, expanding when trade is booming and shrinking when the high street goes quiet? You likely already know the stress of rigid bank loans that demand the same heavy payment regardless of whether you’ve had a record-breaking Saturday or a silent Tuesday. It feels wrong to be penalised by a fixed schedule when your revenue naturally fluctuates; it is an outdated way to manage a modern shop or restaurant.

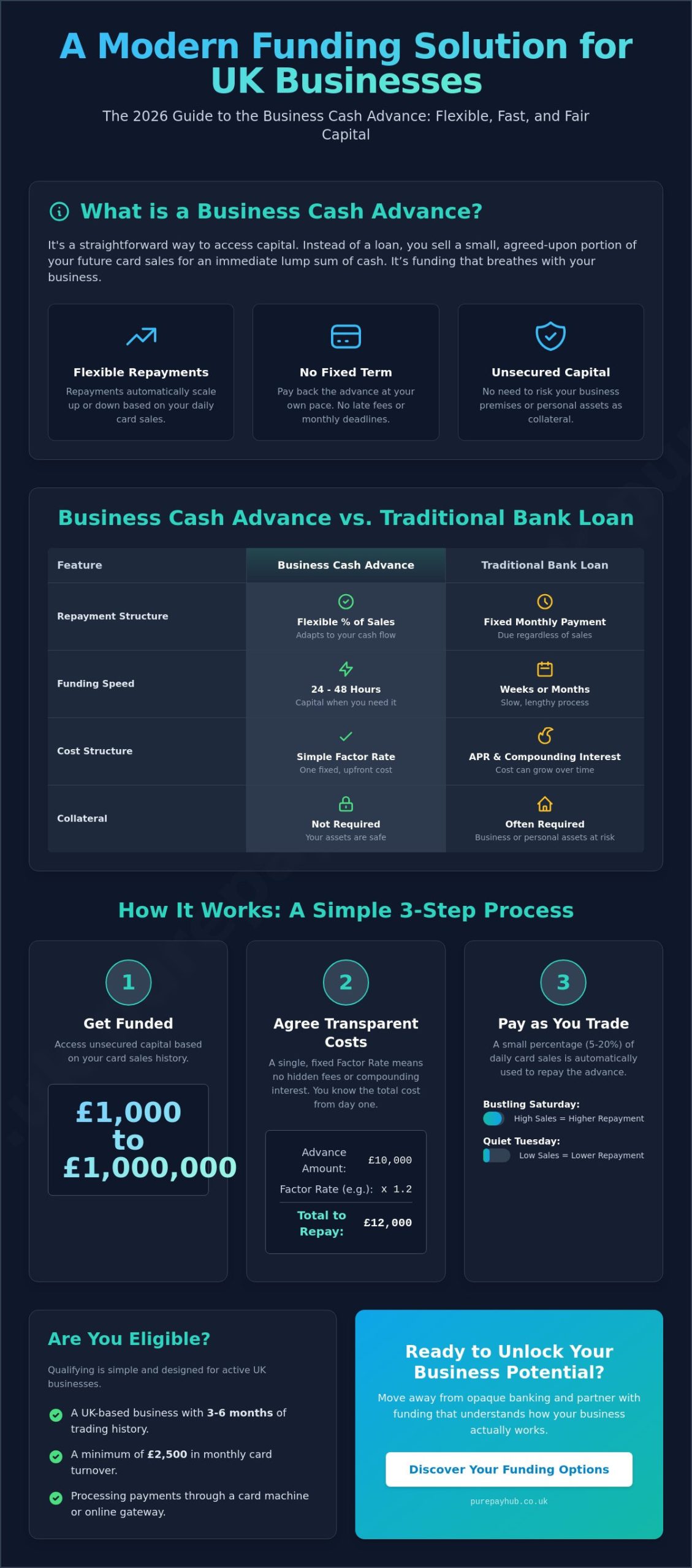

This guide explains how a business cash advance offers a more transparent, flexible alternative for UK merchants in 2026. You’ll discover how to access unsecured capital between £1,000 and £1,000,000, often within just 48 hours, whilst keeping your repayments perfectly mirrored to your daily card sales. We’ll break down the simple factor rate structure that replaces complex interest, the minimum turnover requirements you need to meet, and how this modern funding model ensures you never overextend your cash flow during a slow month. It is time to move away from opaque banking and toward a partnership that understands how your business actually works.

Key Takeaways

- Learn how a business cash advance provides a flexible funding solution where repayments automatically scale up or down based on your daily card sales.

- Understand the straightforward eligibility requirements for UK merchants, typically requiring just three to six months of trading history and £2,500 in monthly turnover.

- Discover the transparency of factor rates, which ensure you pay one fixed, agreed-upon amount without the worry of accruing interest or hidden monthly fees.

- See how PurePay Hub leverages your card machine data to offer next-day access to unsecured capital, removing the need for complex bank applications or collateral.

What is a Business Cash Advance? A Flexible Alternative for UK SMEs

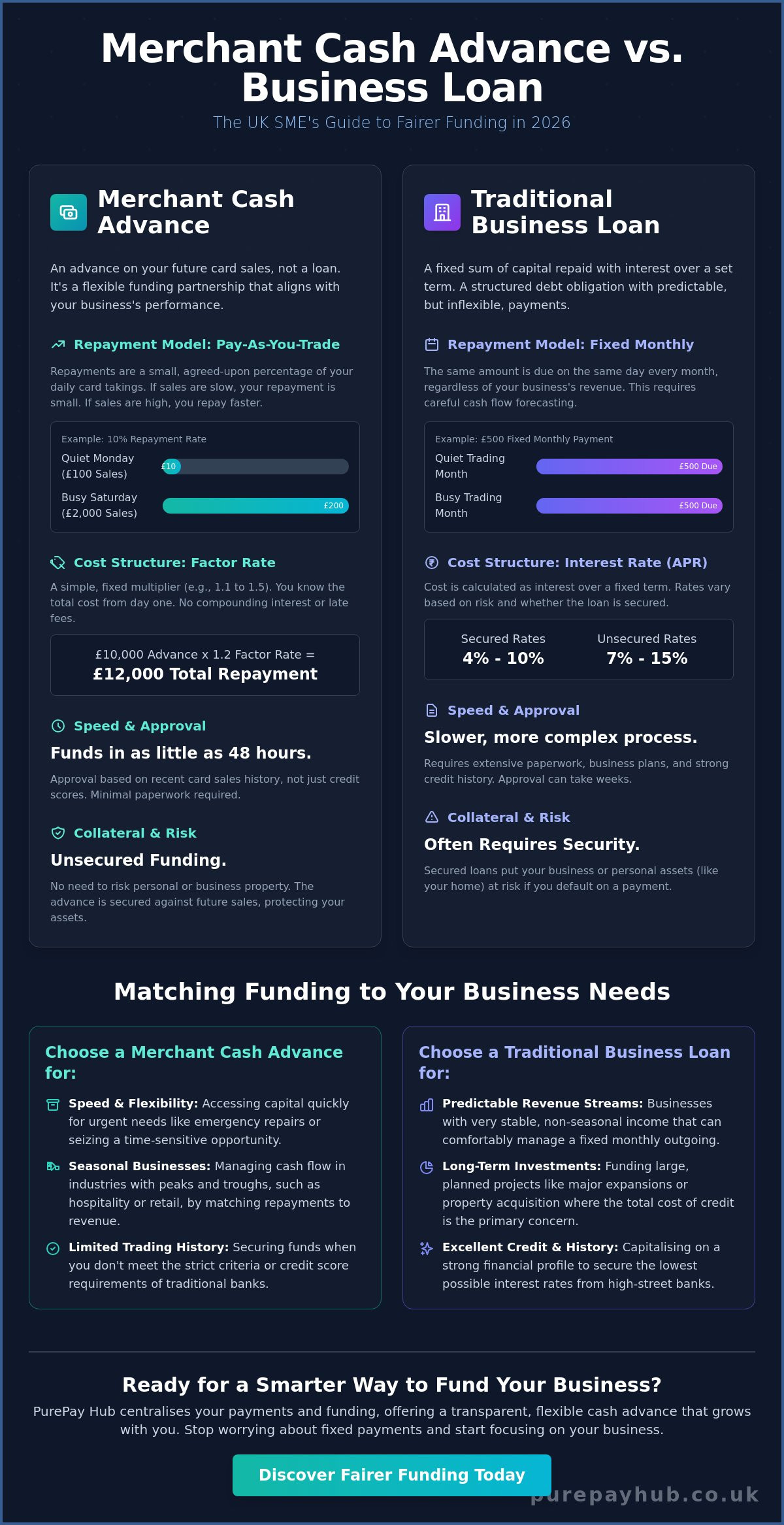

A business cash advance is a straightforward way to access capital without the rigid constraints of a traditional bank loan. Instead of borrowing money and paying it back with interest, you’re essentially selling a small portion of your future card sales in exchange for an immediate lump sum. This distinction is vital for your financial health. Because it’s technically a purchase of future receivables rather than a debt, it doesn’t sit on your balance sheet in the same way a loan does. This often protects your credit profile whilst giving you the liquidity needed to grow.

For a deeper dive into the technical background, you can read more about What is a Merchant Cash Advance? and how it differs from conventional lending. This model is particularly effective for businesses that process high volumes of card transactions, such as local boutiques, independent pubs, and busy restaurants. The core appeal is simple: your repayments breathe with your business. When trade is brisk, you pay back more; when things slow down, your repayments automatically reduce.

The Mechanics of Merchant Funding

The process involves a seamless partnership between you, the funding provider, and your payment processor. When you take a business cash advance, there are no fixed monthly instalments to worry about. Instead, a small, agreed-upon percentage of your daily card takings is automatically deducted from your daily batches. If you have a quiet day, you pay back less. If you’re closed for a bank holiday, you pay nothing at all. Crucially, this is unsecured capital. You don’t need to put your home or business premises at risk to secure the funds, making it a much safer prospect for independent owners.

Why UK Businesses are Moving Away from High-Street Banks

In 2026, many UK SMEs find themselves stuck in a “funding gap”. Traditional high-street banks have become increasingly risk-averse, often requiring mountains of paperwork and taking months to reach a decision. Modern merchants don’t have months to wait. Whether you need to repair a commercial oven or stock up for a seasonal rush, speed is everything.

A business cash advance can often be approved and funded within 24 to 48 hours. This agility is essential in a post-digital retail environment where consumer trends shift rapidly. You get the funds you need to stay competitive without the bureaucratic headaches of a 19th-century banking model. It’s about finding a partner that values your daily performance over a static credit score.

How Business Cash Advances Work: Factor Rates and Repayments

Understanding the mechanics of a business cash advance is the first step toward taking control of your cash flow. Unlike a bank loan where interest compounds over time, this funding uses a “factor rate”. This means the total cost of your capital is fixed from the very first day. You won’t face the anxiety of fluctuating interest rates or the pressure of a ticking clock that makes traditional debt so stressful for small business owners.

A factor rate is a fixed multiplier of the advance amount. For instance, if you secure a £10,000 advance with a factor rate of 1.2, your total repayment amount is exactly £12,000. There are no complex calculations to perform later and no surprises in your monthly statements. You know exactly what the facility costs before you even sign the agreement.

The repayment happens through an automated process often called a “sweep” or “holdback”. You agree on a percentage of your daily card sales, typically between 5% and 20%, which is automatically deducted before the funds reach your bank account. This percentage is designed to balance your growth goals with your daily operational needs. Most merchants find that a modest holdback allows them to settle the advance comfortably without feeling a pinch in their working capital. This automatic process removes the administrative burden of manual transfers, allowing you to focus on running your shop or restaurant whilst the technology handles the rest.

Factor Rates vs. APR: Calculating the Real Cost

Traditional loans use APR, which can be confusing when you’re trying to calculate short-term costs for a seasonal project. In contrast, a factor rate provides total clarity for short-term cash flow planning. You can find more details on how these structures fit into the wider market in the UK government guidance on Merchant Cash Advances. It’s a transparent model that prioritises your ability to manage daily overheads without the hidden markups often found in high-street banking products.

The Repayment Journey: Walking Through a Typical Month

Imagine a busy Saturday where your pub is packed; your repayment that day will be higher because your sales are higher. On a quiet Monday morning when you only serve a few coffees, the deduction is tiny. If you decide to close for a week for renovations and take £0 in card sales, you pay £0 that week. This flexibility prevents the “debt spiral” often triggered by fixed-cost loans that demand payment even when the till is empty. If you’re looking for a funding partner that offers this level of transparency, exploring a business cash advance through PurePay Hub could be the stabilising force your finances need.

Business Cash Advance vs. Traditional Loans: A Comparison

Choosing between a traditional bank loan and a business cash advance often comes down to what you value more: a rigid, low-cost structure for the long term or a flexible, high-speed solution for the present. Banks prioritise the past. They spend weeks auditing your historical accounts and scrutinising your personal credit score. If your score isn’t perfect or you don’t have property to offer as collateral, the door often stays shut. An advance shifts the focus to your future sales, using your current card turnover as the primary metric for approval.

The speed of funding is perhaps the most striking difference. Whilst a high-street lender might take a month to process a small business application, an advance can put capital in your bank account within 24 to 48 hours. This makes it a tactical tool for merchants who need to move quickly. Whether you’re jumping on a bulk stock discount or fixing a broken shopfront, you don’t always have the luxury of a thirty-day waiting period. Understanding what is a merchant cash advance helps clarify why it’s a “tactical” choice rather than a “structural” one; it’s about solving immediate cash flow needs without the bureaucratic weight of a bank.

When is a Traditional Bank Loan Better?

MCAs aren’t a universal fix for every financial need. If you’re planning a multi-year infrastructure project or purchasing the freehold for your premises, a traditional bank loan is usually the better choice. These long-term projects benefit from the lower overall cost of debt that banks provide over five or ten years. It’s also worth checking for early repayment penalties on bank products. Most business cash advance agreements don’t have them because there’s no fixed term, but a bank might charge you extra for clearing your debt ahead of schedule.

The Seasonal Advantage for Hospitality and Retail

For a local pub or a seasonal boutique, the “variable” nature of an advance is its greatest strength. Imagine using the funds to build a new beer garden in May. During the sun-soaked summer months, your repayments are high because your sales are booming. You settle the balance quickly whilst the cash is flowing. When the “quiet January” period arrives and footfall drops, your outgoings automatically shrink to match your lower takings. This synchronisation means the funding is effectively breathing with your business. You never have to worry about a fixed monthly overhead draining your accounts when the high street is empty.

Qualifying for Funding: Eligibility and Application

Qualifying for a business cash advance is often a refreshing experience for merchants used to the rigid demands of high-street banks. Instead of focusing on your personal assets or long-term credit history, lenders look at the health of your daily trade. The primary requirement is a consistent monthly card turnover, typically starting at £2,500. This ensures that your business has the natural “breathing room” to settle the advance through the small daily deductions we’ve already explored.

Most providers look for a minimum trading history of at least 3 to 6 months. This window provides enough data for real-time algorithms to assess your business health accurately. These systems aren’t looking for perfection; they’re looking for reliability. By analysing your digital footprint through card processing statements, lenders can reach an approval decision much faster than a human auditor ever could. It’s a modern approach that rewards active, trading businesses over those with the most collateral.

Preparing Your Application for Success

Speed is the hallmark of this funding model, but you can accelerate the process even further by having your records in order. Most lenders will request your last three months of merchant statements to verify your transaction volume and average sale value. You should also ensure your PCI compliance is up to date, as this demonstrates a level of professional management and security that reassures potential partners. A healthy mix of debit and credit sales improves approval odds by showing you have a varied and stable customer base. Having your bank records organised alongside these statements will often lead to an approval in hours rather than days.

Red Flags to Avoid

Whilst the approval rates are high, there are a few pitfalls to keep in mind. A sudden, unexplained drop in your card volume just before or during your application can trigger a deeper review from the underwriting team. If you’ve recently changed your business model or had a temporary closure, it’s better to be transparent about it from the start. Honesty regarding any existing business debt is also vital; lenders value clarity and are more likely to work with you if they have the full picture. Always look for a partner with a no-nonsense fee structure that avoids hidden “non-utilisation” charges. If you’re ready to see what you qualify for, you can start your application with PurePay Hub today to get a clear, fast decision.

Securing Your Advance with PurePay Hub: The Integrated Advantage

Most financial products feel disconnected from your daily operations. A business cash advance from PurePay Hub is different because it’s built directly into your merchant services. We don’t need to ask for mountains of paperwork that you’ve already provided elsewhere. Since we already manage your payment processing, we have a clear, real-time view of your business health. This integration removes the friction that usually slows down traditional lending. It’s a cleaner, more efficient way to fund your next project.

Speed is our standard. We focus on “Next-Day Access” to bridge the gap between your approval and the capital hitting your account. You won’t find any hidden markups or confusing corporate jargon in our agreements. We believe in straight-talking finance that supports your growth rather than complicating it. This approach provides a reliable foundation for your next big step, ensuring you have the liquid capital to act when opportunities arise. We’re not just a distant lender; we’re a stabilizing force for your business finances.

Why Our Merchants Choose Integrated Funding

Our role as your payment processor means we already understand the rhythm of your trade. Whether you’re using our countertop card machines or our EPOS systems, your transaction data tells a story of hard work and consistency. Having your funding and your payment hardware under one roof simplifies your administrative life. It also allows us to offer a fairer service specifically tailored to regional UK business owners who are often overlooked by national banks. We take pride in being a supportive ally, offering a modern fintech solution that hasn’t lost its focus on the individual merchant. Our commitment to transparency ensures you can plan for the future with absolute confidence.

Start Your Growth Journey Today

Getting a quote is a risk-free process that won’t affect your personal credit score. We can use the data from your portable card machine or virtual terminal to provide an accurate, transparent offer in minutes. Our team operates with a sense of calm advocacy; we’re here to help you find the right fit for your specific needs. You can secure the capital required to refurbish your premises or expand your inventory without the stress of traditional debt. It’s time to experience a funding partner that values your business as much as you do.

Get a transparent business cash advance quote from PurePay Hub

Fuel Your Business Growth on Your Own Terms

You now have a clear roadmap for securing capital that respects your cash flow. By choosing a business cash advance, you move away from the rigid constraints of traditional debt and toward a model that breathes with your daily sales. This guide has shown how factor rates provide absolute cost certainty and how integrated funding removes the bureaucratic hurdles that often block SME growth. It’s about having the financial agility to act when the time is right.

At PurePay Hub, we prioritise clarity and speed. Our merchants benefit from debit card rates starting from 0.3% and a no-nonsense fee structure that eliminates hidden surprises. With next-day funding available, you can bridge the gap between approval and action almost instantly. We’re here to provide the steady support you need to expand your shop, pub, or restaurant with confidence.

Apply for a transparent Business Cash Advance with PurePay Hub. Your business deserves a partner that values honesty and efficiency as much as you do.

Frequently Asked Questions

Is a business cash advance expensive compared to a bank loan?

A business cash advance is priced using a fixed factor rate rather than an annual interest rate (APR). Whilst the total cost might be higher than a traditional secured loan, you’re paying for speed and the lack of collateral requirements. There’s no compounding interest and no late fees; you simply pay back one agreed-upon total. This makes it a transparent choice for short-term tactical projects where speed is your main priority.

Will an MCA affect my business credit score?

Generally, this type of funding doesn’t appear as debt on your credit file because it’s a purchase of future sales. Most lenders perform a “soft” credit search during the application process which doesn’t impact your score. Because there are no fixed monthly deadlines, you don’t risk “late payment” markers during slow trading periods. It’s a safer way to protect your financial profile whilst accessing the capital you need to grow.

What happens if my business has a very slow month?

Your repayments automatically decrease during quiet periods. Since the deduction is a fixed percentage of your daily card sales, a drop in revenue leads to a smaller daily repayment. If your shop or restaurant has a day with zero card transactions, you pay nothing at all that day. This flexibility removes the stress of fixed overheads and ensures you always have enough working capital to manage your daily operations.

Do I need to change my card machine provider to get an advance?

You don’t always need to switch, but using an integrated provider like PurePay Hub can significantly speed up the approval process. When you use our countertop or portable card machines, we already have access to the data needed to verify your turnover. This allows for a much smoother “sweep” process where repayments are handled automatically. It’s a cleaner way to manage your funding and your merchant services under one reliable roof.

Can I pay off my business cash advance early?

You can usually settle the full balance ahead of schedule without facing early repayment penalties. However, it’s important to remember that the total cost is fixed at the start of the agreement via the factor rate. Paying it back faster doesn’t typically reduce the total amount owed, but it does clear your future revenue from further deductions. Always check your specific agreement to ensure there are no hidden fees for early settlement.

What can I use the funding for? Are there restrictions?

You have complete freedom to use a business cash advance for any legitimate business purpose. Most UK merchants use the funds for refurbishments, bulk inventory purchases, or seasonal marketing campaigns. Unlike some bank products that require a specific business case, this capital is yours to deploy wherever it adds the most value. It’s an excellent tool for bridging cash flow gaps or seizing unexpected opportunities that require immediate action.

How quickly will the money be in my bank account?

Speed is the primary advantage of this model; capital often reaches your bank account in just 24 to 48 hours. The digital application process removes the need for weeks of auditing and manual paperwork. Once your card processing data is verified and the agreement is signed, the funds are transferred electronically. This allows you to respond to business needs in real-time rather than waiting for a bank committee to reach a decision.