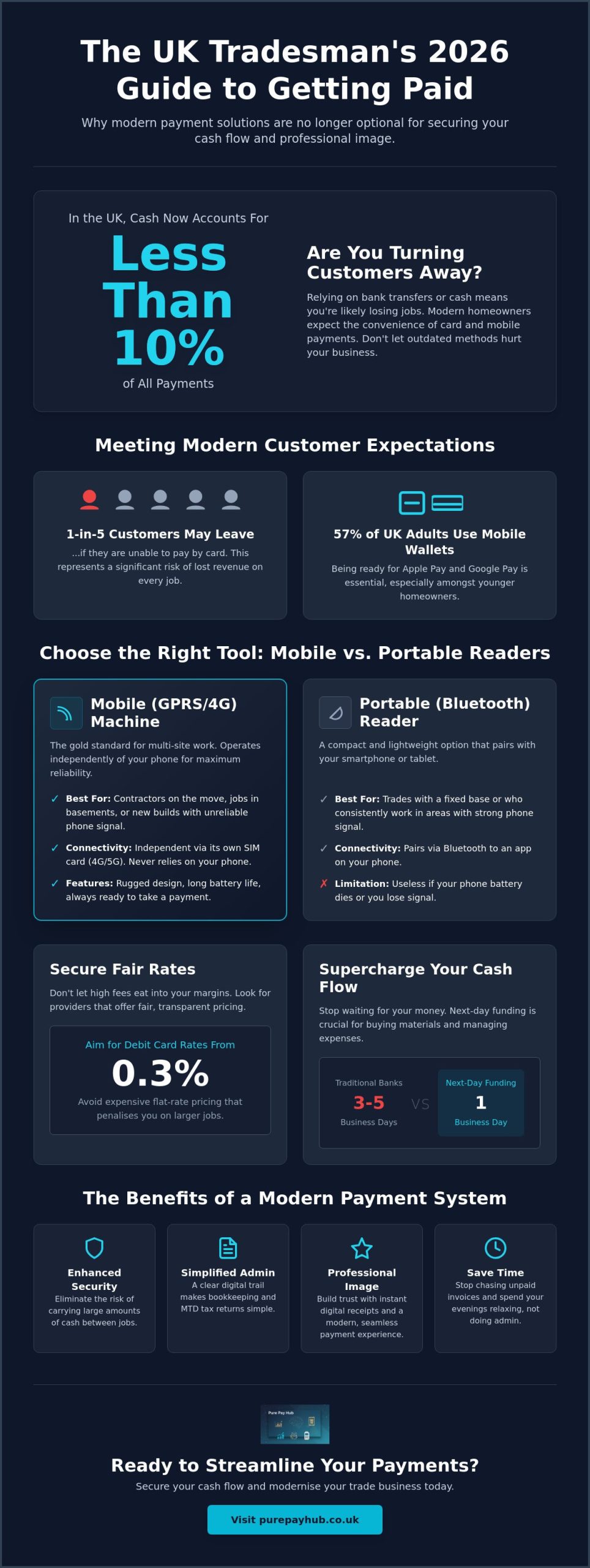

Did you know that cash now accounts for less than 10% of all UK payments? If you’re still relying on bank transfers or paper invoices, you’re likely losing customers who simply don’t carry notes anymore. Most tradesmen find themselves stuck in a cycle of chasing late payments whilst paying high fees to traditional banks. You finish a hard day’s work. You shouldn’t spend your evening sending “just checking in” emails. Finding the right payment solutions for tradesmen UK isn’t just about convenience. It’s about securing your cash flow and looking professional on every job site.

We’ve designed this 2026 guide to help you eliminate those payment delays and secure the lowest transaction rates for your business. You’ll discover how to provide a seamless experience that makes it easy for your customers to pay instantly. We’ll explore the latest mobile card machines, the move toward smartphone-based payments, and how to avoid the hidden costs that eat into your margins. This guide gives you a clear roadmap to a more efficient, profitable trade business.

Key Takeaways

- Learn why accepting digital payments is now essential for maintaining a professional image and meeting the expectations of modern UK homeowners.

- Discover the critical differences between GPRS mobile units and Bluetooth portable readers to ensure you always have a reliable signal on every job site.

- Understand how to evaluate payment solutions for tradesmen UK to secure fair debit rates from 0.3% whilst avoiding the expensive traps of flat-rate pricing.

- Find out how next-day funding protects your cash flow, allowing you to purchase materials for the next project without the typical 3-5 day wait for funds.

- Explore how rugged, field-ready card machines can streamline your administration and finally eliminate the frustration of chasing unpaid invoices.

Why UK Tradesmen are Moving Away from Cash in 2026

The UK payment landscape has transformed. Relying on “cash only” isn’t just old-fashioned; it’s a significant business risk. In 2024, cash accounted for less than 10% of all transactions, and that figure continues to shrink. By 2026, many homeowners simply don’t have enough physical money in the house to pay for a boiler service or a consumer unit upgrade. If you want to be the preferred choice for local jobs, you need modern payment solutions for tradesmen UK that match how people actually live.

Accepting cards signals that you’re a legitimate, professional business rather than a “cash-in-hand” outfit. It removes the friction of the “invoice dance” entirely. Instead of waiting for a client to log into their bank later that evening, you can settle the bill before you’ve even packed your tools. This shift is supported by the Faster Payment System, which ensures that digital transactions move quickly and reliably across the country. It saves you from those dreaded “admin evenings” spent chasing unpaid invoices whilst you could be relaxing. You also avoid the hidden costs of cash, such as the time spent driving to a branch and the fees banks charge for processing manual deposits.

Consumer Behaviour and the Cost of Lost Jobs

Customers expect ease above all else. Industry reports suggest that 1-in-5 customers may abandon a purchase or choose a different provider if they can’t pay by card. There’s also a clear psychological link between card payments and higher spending. When a customer knows they can tap their phone or use a mobile card machine, they’re more likely to agree to “extra bits” or upgrades on the spot. Amongst younger homeowners, the adoption of mobile wallets is nearly universal; 57% of UK adults were already registered for services like Apple Pay and Google Pay by 2024. If you aren’t equipped to take these payments, you’re essentially handing work to a competitor who is.

Security and Accountability for the Modern Tradesman

Carrying large amounts of cash makes you a target for theft and creates unnecessary stress on the road. A digital-first approach keeps your earnings safe in the cloud until they hit your bank account. It also simplifies your life during tax season. Every transaction creates a digital paper trail that fits perfectly with Making Tax Digital (MTD) requirements, reducing the time you spend on bookkeeping. Most importantly, it builds immediate trust. Providing an instant digital receipt gives the customer peace of mind that the transaction is recorded and professional. This transparency is a cornerstone of a reliable trade business.

Mobile vs. Portable Card Machines: Which is Best for Your Trade?

Your tools are only useful if they work when you need them. The same applies to your card reader. Choosing between mobile and portable hardware is the first step in setting up effective payment solutions for tradesmen UK. If you are an electrician working in a new build or a plumber in a basement, signal reliability becomes your biggest hurdle. You need a device that doesn’t drop the connection just as the customer taps their card. A failed transaction at the end of a long day is a frustration you don’t need.

The data backs this shift toward digital reliability. According to UK Finance’s 2025 payment markets report, the rapid growth of contactless payments has changed customer expectations forever. They expect a quick, seamless tap. If your hardware lags, it reflects poorly on your professional image. Modern devices are built to handle this pressure, but you must choose the right connectivity model for your specific working environment.

Comparing Hardware Options for On-Site Work

Mobile card machines are the gold standard for multi-site contractors. These units contain their own SIM cards and connect directly to 4G or 5G networks. They operate independently of your smartphone. This is ideal if you often work in areas where your phone signal might be patchy but a dedicated data roaming SIM can find a stronger mast. They are built for the road. They often feature longer battery lives and ruggedised casings that survive the occasional drop on a concrete floor. This independence ensures you are never tethered to a single device’s battery life.

Portable card machines work differently. They usually connect via Bluetooth to an app on your phone or tablet. They are often smaller and more lightweight. These are perfect for trades with a fixed base or those who always have their phone nearby with a strong signal. However, if your phone battery dies, your ability to take payments goes with it. For most field-based trades, the independence of a mobile unit is usually worth the investment. You can find ruggedised Portable Card Machine options that bridge this gap by offering high durability for site work.

Digital Solutions: Beyond the Physical Reader

Taking payments doesn’t always require a physical card present. Virtual Terminals allow you to take payments over the phone securely. This is a game-changer for securing deposits or covering material costs before you even arrive on-site. It protects your cash flow and ensures the customer is committed to the job. You simply log into a secure web portal, enter the card details, and the funds are processed instantly. This professional approach builds immediate confidence with new clients.

Payment links offer another layer of flexibility. You can generate a unique link and send it via WhatsApp, SMS, or email. The customer clicks the link and pays on their own device. It is a brilliant way to get invoices settled whilst you are still sitting in the van. It removes the friction of bank transfers and gives you a digital paper trail for your accounting software. Integrating these tools ensures your business stays profitable and organised without the constant need for manual admin.

Navigating Merchant Fees: Finding the Lowest Card Machine Rates

Don’t let complex fee structures drain your hard-earned profits. Many providers lure you in with a simple “flat rate” that actually costs you more in the long run. If you are processing a high volume of transactions, a flat rate of 1.75% is often a trap. You should look for payment solutions for tradesmen UK that offer a clear breakdown of costs. This ensures you aren’t overpaying for the convenience of a simple headline figure. Understanding the difference between debit and credit rates is the first step toward significant savings.

The Merchant Service Charge (MSC) is the total fee you pay on every transaction. It is made up of three parts: the interchange fee, the scheme fee, and the provider’s margin. In the UK, interchange fees are capped at 0.2% for consumer debit cards and 0.3% for consumer credit cards. When you see market-leading rates around 0.3% for debit and 0.5% for credit, you are seeing the benefit of these caps passed directly to you. Providers who charge a flat 1.5% or higher are keeping the difference as extra profit.

Breaking Down the Fee Structure

Interchange fees are the base costs set by card schemes like Visa and Mastercard. These are non-negotiable, but how your provider handles them matters. Interchange-plus pricing is the transparent standard for 2026 that separates the actual cost of the transaction from the provider’s markup. This model allows you to see exactly what you are paying for rather than being bundled into a generic, expensive tier. It is the only way to ensure your trade business isn’t subsidising the higher costs of international or business cards used by other merchants.

You also need to weigh up hardware costs. Buying a reader outright for £19 to £39 is popular for sole traders starting out. However, established businesses often find that renting a high-spec mobile unit for £15 to £40 a month offers better value. Rental usually includes faster support and automatic hardware upgrades. This prevents you from being stuck with an obsolete device when security standards change.

Transparency and Hidden Costs to Watch For

Hidden costs can appear in your monthly statement if you aren’t careful. Minimum Monthly Service Charges (MMSC) can be a burden for seasonal trades, such as landscapers or roofers, who might have quieter months. If your turnover drops, you might still be charged a baseline fee. Always check for exit fees and the length of your contract. You need the flexibility to switch if your provider stops being competitive.

PCI non-compliance fines are another avoidable drain on your bank balance. These monthly penalties occur if you don’t keep your security self-assessment up to date. A supportive partner will help you navigate this paperwork to ensure you stay compliant and avoid unnecessary charges. Reliable payment solutions for tradesmen UK should provide transparent reporting that makes these costs easy to spot and manage.

Managing Cash Flow: Next-Day Funding and Business Cash Advances

Waiting three to five days for your money to clear is a cash-flow killer. For a builder or a plumber, that delay means you cannot restock materials for the next job. You are effectively lending your own money back to the bank whilst your business grinds to a halt. Modern payment solutions for tradesmen UK must do more than just process a transaction. They need to act as a liquidity engine for your daily operations. When you settle a bill on a Tuesday, you need that capital in your account by Wednesday morning to keep your projects moving.

Speed is the ultimate tool for a growing trade business. Traditional banking structures often ignore the reality of site work, where material costs are high and margins are tight. By choosing a provider that prioritises rapid settlement, you eliminate the stress of “floating” costs on personal credit cards. This immediate access to your earnings provides the stability needed to manage multiple sites and larger teams without the constant fear of a depleted bank balance.

The Power of Next-Day Access to Funds

Instant liquidity allows you to take on larger contracts with confidence. You no longer have to worry about whether you can afford the next pallet of bricks or a new boiler unit whilst waiting for the previous client’s funds to land. This reliability reduces your reliance on high-interest debt and keeps your credit clean. PurePay Hub’s commitment to fast onboarding and rapid settlement ensures you aren’t left in the dark. Their systems are built for the field, providing a dependable flow of cash that matches the pace of your work. If you are ready to stop waiting for your money, you can apply for a Business Cash Advance to fuel your next stage of growth.

Using Business Cash Advances for Trade Growth

Sometimes your daily takings aren’t enough to cover a major leap forward. You might need to upgrade your van or invest in specialised equipment to win bigger tenders. A Business Cash Advance offers a supportive, unsecured alternative to traditional bank loans. Eligibility is determined by your card sales history rather than just a rigid credit score. This is a fairer way to assess a trade business that has a proven track record of steady work. A Business Cash Advance is repaid as a fixed percentage of daily card takings. This structure is inherently flexible. If you have a quiet week or take time off for a holiday, your repayments automatically scale down. It is a disciplined, modern way to fund development without the pressure of fixed monthly bills that don’t care about your schedule.

Streamline Your Trade Business with PurePay Hub

Choosing the right partner is about more than just hardware. It’s about finding a service that respects your time and your margins. PurePay Hub provides payment solutions for tradesmen UK that are built on transparency and fairness. We offer competitive debit card charges starting from 0.3% for UK merchants. This isn’t a temporary teaser rate. It’s a commitment to keeping more of your hard-earned money in your business. We don’t hide behind complex jargon or murky fee structures. Our goal is to provide clarity in an industry that often lacks it.

Our hardware is designed for the reality of your working day. We provide rugged, reliable mobile and portable card machines that handle the dust of a building site or the damp of a plumbing job. These units are built to last. They offer the connectivity you need to process payments instantly, wherever the job takes you. You also get next-day access to your funds as standard. We know that material costs don’t wait, so your money shouldn’t either. If you run into a technical snag, our expert UK-based support team is ready to help you organise your payments without delay.

The PurePay Hub Advantage for Tradesmen

We’ve removed the hurdles from the onboarding process. You can get up and running whilst you focus on your current projects. Our fee structures are entirely transparent. You won’t find hidden markups or surprise monthly costs on your statement. Whether you are a sole trader with a single van or a large contracting firm managing multiple teams, we provide tailored solutions that fit your scale. We act as a stabilising force for your finances, allowing you to grow with confidence.

How to Get Started Today

Switching your provider shouldn’t be a headache. We’ve simplified the process to ensure you don’t lose a single day of trading. You can start by requesting a quote tailored to your specific trade and annual turnover. We’ll look at your current statements and show you exactly where you can save. It’s a straightforward, honest comparison that puts you in control. Our team handles the heavy lifting of the transition, ensuring your new equipment arrives ready to use. Join the hundreds of UK tradesmen switching to PurePay Hub and take the first step toward a fairer way of taking payments.

Future-Proof Your Trade Business Today

The shift to a cashless society is no longer a prediction; it is your current reality. By embracing modern payment solutions for tradesmen UK, you do more than just accept cards. You eliminate the frustration of chasing late invoices and ensure your cash flow remains healthy with next-day access to your funds. Whether you choose a rugged mobile reader for site work or a flexible virtual terminal for deposits, the goal is to look professional whilst keeping your margins protected from hidden fees.

We’re here to act as your fair partner in this transition. You shouldn’t have to navigate murky contracts or wait days for your own money. With debit card rates starting from 0.3%, next-day funding as standard, and no-nonsense UK-based support, we provide the stability your business needs to grow. It’s time to stop worrying about bank deposits and start focusing on the next job. Get a transparent quote for your trade business payments and see how much you could save. You’ve built a great business; let’s ensure you’re paid fairly and quickly for it.

Frequently Asked Questions

What is the cheapest card machine for a sole trader in the UK?

The upfront cost of a reader isn’t the only factor you should consider. Whilst buying a basic reader is often the cheapest initial investment, the per-transaction rates are usually higher. For tradesmen with a steady turnover, a rental model with lower debit rates often works out cheaper over a full year. You should evaluate the total cost of ownership rather than just the initial price tag to find the most cost-effective payment solutions for tradesmen UK.

Can I take card payments if I have no Wi-Fi on a building site?

You don’t need a Wi-Fi connection if you use a mobile card machine. These devices come equipped with built-in roaming SIM cards that connect directly to 4G or 5G networks. If you are using a portable reader, you can simply tether it to your smartphone’s data connection via Bluetooth. This ensures you can process a tap or chip-and-pin transaction even in the middle of a remote building site or a new housing development.

How long does it take for the money from a card payment to reach my bank account?

Standard processing times in the industry usually range from three to five business days. However, this delay can be a massive hurdle for your cash flow when you need to purchase materials for your next project. Modern providers now offer next-day funding as a standard feature. This means money cleared today hits your business bank account by tomorrow morning, giving you the liquidity needed to keep your jobs moving without relying on personal credit.

Do I need a separate merchant account to take card payments?

Yes, you need a merchant account to act as the secure bridge between the customer’s card and your business bank account. This account verifies the transaction and holds the funds during the clearing process. Most modern payment providers bundle this setup into their onboarding process, so you don’t have to deal with a traditional bank’s complex paperwork. It is a straightforward process that gets you ready to take professional payments very quickly.

Are there any hidden fees I should look out for with card readers?

You should keep a sharp eye out for PCI non-compliance fines and Minimum Monthly Service Charges (MMSC). These are common hidden costs that can drain your profits if you aren’t proactive with your paperwork. Some providers also hide expensive exit fees in the small print of their contracts. Reliable payment solutions for tradesmen UK should provide transparent reporting so you can see exactly where every penny of your transaction fee is going each month.

Can I take payments over the phone for deposits or call-out fees?

You can easily take remote payments by using a Virtual Terminal or a Payment Link. A Virtual Terminal allows you to enter card details into a secure web portal whilst you are speaking with a customer on the phone. Alternatively, you can generate a Payment Link and send it via WhatsApp or SMS. This is an excellent way to secure deposits or cover your call-out fees before you even leave the van for a job.

Is it better to buy a card machine or rent one monthly?

Buying is often the best choice for new sole traders with lower or unpredictable turnover. However, as your business grows, renting a mobile card machine becomes the more professional and cost-effective choice. Rental agreements usually include automatic hardware upgrades and much faster technical support. This ensures you aren’t left with an obsolete device that doesn’t meet the latest security standards whilst you are trying to settle a bill on-site.

What happens if my card machine stops working whilst I am on a job?

If your hardware fails, you can use your smartphone to generate a Payment Link for the customer to pay on their own device. This serves as a reliable backup that ensures you don’t leave a job site without being paid for your hard work. Choosing a provider with expert UK-based support is also vital. They can often troubleshoot the issue over the phone or arrange a replacement device quickly to minimise any disruption to your schedule.